Ball Corp. (BLL) is one of the stocks which has been long ignored by the market despite its excellent fundamentals. The ongoing coronavirus pandemic has finally brought this leading supplier of aluminum packaging products to the forefront. Although the company’s clients involve manufacturers of beverage, personal care, and household products, the key focus is on the beverages segment. The company's largest product line is aluminum beverage containers, but it also produces extruded aluminum aerosol containers and aluminum slugs.

While the beverages segment is not completely immune to the pandemic, it is definitely one amongst the least affected. In recessionary environments, people would most likely forego costlier purchases first. Hence, although Ball Corp.’s packaging business is not very exciting, it is definitely one of the few coronavirus resilient ones in the market. I believe Ball Corp. can prove to be a stable and attractive investment for retail investors, especially during the coronavirus pandemic.

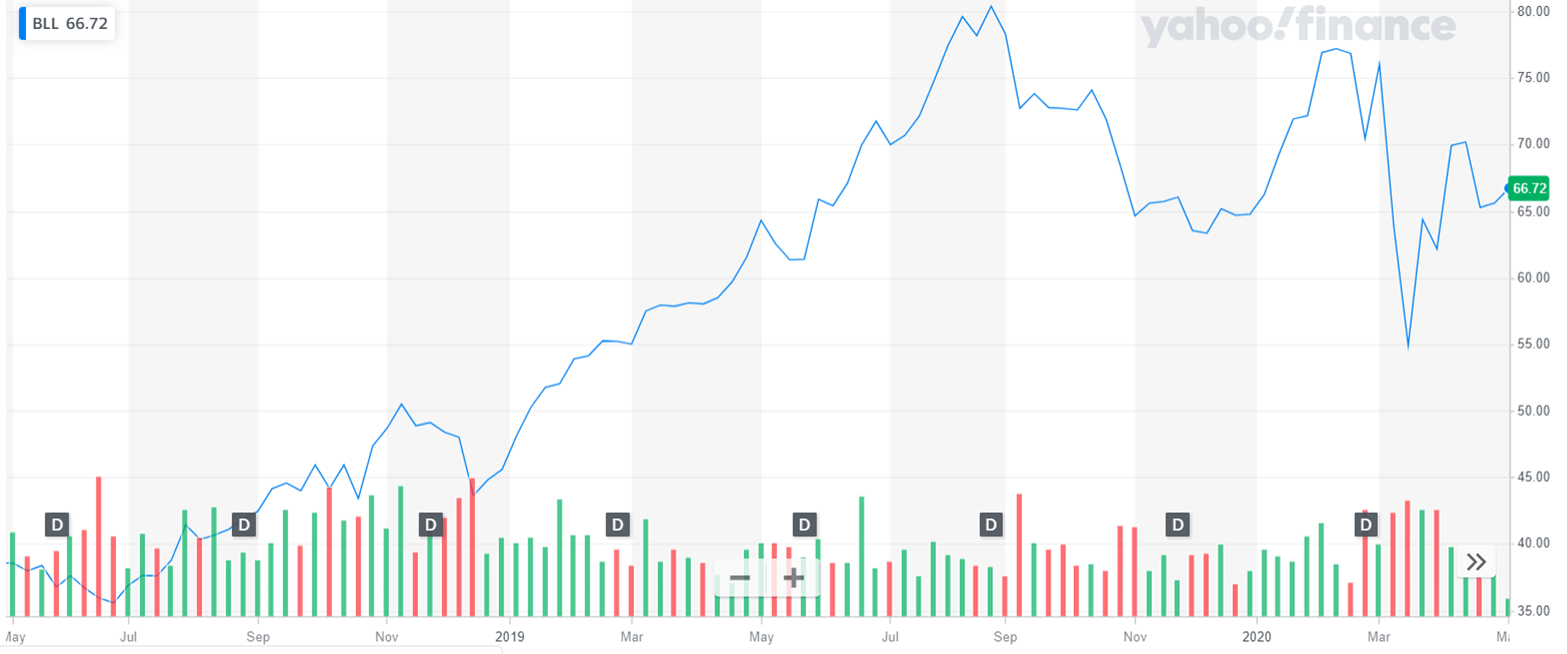

Ball Corp. revenues have a safety net during the COVID-19 pandemic

Ball Corp. is mainly in the business of supplying aluminum cans to beverage companies. The end-demand for beverages is generally less cyclical as compared to many other products. According to a new study by Fact.MR, the non-alcoholic beer market will grow at a CAGR of 7% from 2019 to 2027. Recent Nielsen data also highlights a solid boost in demand for alcoholic drinks.

Both these trends will help Coca-Cola (KO) and Anheuser-Busch InBev (BUD), two of Ball Corp.’s biggest customers. Anheuser-Busch InBev is the largest brewer in the world. I do not expect these beverage companies to remain completely unaffected in these uncertain times. Notably, Coca-Cola has highlighted the negative revenue impact of COVID-19 on sales, especially due to ongoing lockdowns in international markets in the first quarter of 2020. However, the impact has been partly offset due to the resilience