Looking at lodging-specific REITs, I wouldn’t blame you if the Eagles’ “Hotel California” comes to mind.

Do you feel as if, as the song goes, you’ve been “on a dark, desert highway” since late February?

Are you seeing shimmering lights in front of you? Is your head growing heavy and your sight growing dim? Do you feel like you have “to stop for the night,” but the only places in sight seem questionable?

Very, very questionable?

It’s enough to make you wonder if you should just sleep in the car.

After all, you can’t be sure if investing in such cheap, cheap stocks is going to be heaven or hell… especially when this market has already put you through the latter far more than enough.

It’s completely understandable if you feel wary about the situation in front of you and the possibilities it offers. If you ask me, that’s probably an appropriate stance.

Personally, I wouldn’t check in to the Hotel California anytime soon. Actually, I wouldn’t check in to the Hotel California at all.

But that’s not to say there aren’t other worthwhile lodgings to at least look at right now.

Picking and Packing Back Up

I’ll be the first to admit that I haven’t done much traveling as of late. There’s been no hopping on airplanes or staying at hotels for me. I’ve been home, with some of my biggest trips being to the kitchen for my afternoon meals (ok, busted, I ate the last cookie in the cookie jar).

Chances are good you can relate.

Or perhaps it’s better to say that you could relate. We’ve all been shut in for months now, and with the summer fast-approaching, some of us are getting tired of it.

To show as much, a disapproving NBC cited:

- The bar in Lake of the Ozarks, Missouri, that threw a “Zero Ducks Given Pool Party” over the weekend. The offer “drew a large crowd of partygoers, many of whom did not appear to be following the social distancing guidelines.” (With all due respect to the article’s writer… That shouldn’t come as any surprise considering the event’s given name.)

- A crowded Ocean City, Maryland, boardwalk, where people were also seen not wearing masks. (Incidentally, the state lifted its lodging restrictions in expectation of such traffic.)

- A club in Houston, Texas, that hosted its own “packed pool party” despite a 25%-capacity rule for such establishments.

- Point Pleasant Beach along the Jersey Shore, where hundreds of people gathered to protest continuing restrictions imposed by Governor Phil Murphy. “Many of those at the rally held flags and signs and seemed to ignore rules that people stay at least [six] feet apart.”

- The large crowds Daytona Beach authorities kept breaking up over the long weekend.

I don’t mention any of that to be controversial, only to say that – whether you like the lockdowns or not – the U.S. does seem to be reopening… and with or without government approval. That’s bound to have economic effects.

Which, in turn, will have investible effects too.

Source (Beachgoers and tourists walk the Myrtle Beach boardwalk on Saturday)

Airlines, at Least, Are Climbing

I recently read a piece where someone questioned why anyone would invest in hotels when they wouldn’t dare invest in airlines right now.

It’s a good question since the two industries are, of course, very closely connected.

Here’s the thing though… Investors are actually starting to warm up to the flying part of that relationship. As Adam Levine-Weinberg wrote just a few days ago:

“Airlines have been among the hardest-hit businesses during the COVID-19 pandemic. For much of the spring, nearly all states were requiring people to stay home except for essential activities. In any case, with conventions canceled, businesses moving to remote work, them parks closed, hotels offering limited service, and international travel severely restricted by travel bans, most Americans have had nowhere to go.

“The resulting plunge in air travel demand caused airlines to begin hemorrhaging cash. As a result, shares of major airlines… have lost half to two-thirds of their value over the past three months.”

As Levine-Weinberg goes on to note in the very next paragraph, however, “airline stocks bounced back in a big way this week, lifted by signs that travel demand is starting to recover.”

And if that’s true, lodging should follow.

Now, before you go all-in on related holdings, please be aware I’m not really recommending anything in this sector just yet. The one stock I’m willing to stick my neck out for so far is Apple Hospitality (APLE). As explained in a recent iREIT on Alpha post, it’s a Speculative Buy for some pretty compelling reasons.

Like targeted annual returns of 40%.

With that said, we are now starting to put together a lodging-specific REIT watchlist, recognizing that shares in some of the best hotel REITs in America are trading at dirt cheap prices.

When You’re Ready to Travel, These Might Be Worth Staying At

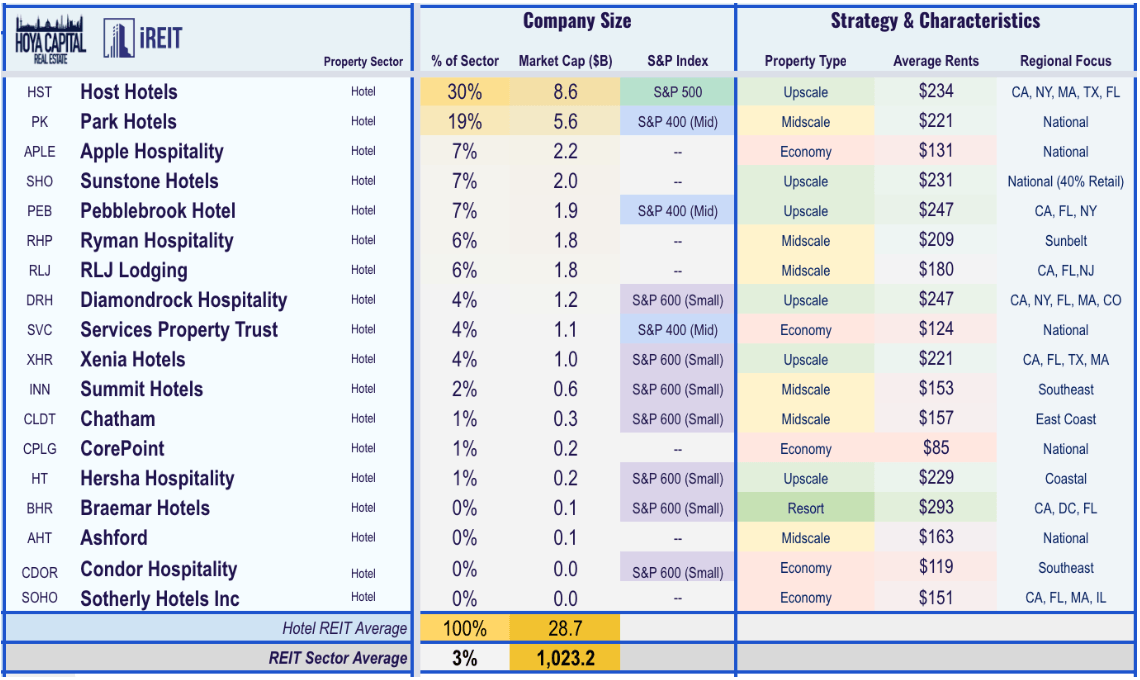

At iREIT on Alpha we provide research on all 18 Lodging REITs including:

- Host Hotels (HST)

- Park Hotels (PK)

- Apple Hospitality (APLE)

- Sunstone Hotels (SHO)

- Pebblebrook Hotel (PEB)

- Ryman Hospitality (RHP)

- RLJ Lodging (RLJ)

- Diamondrock Hospitality (DRH)

- Services Property Trust (SVC)

- Xenia Hotels (XHR)

- Summit Hotels (INN)

- Chatham Lodging (CLDT)

- CorePoint (CPLG)

- Hersha Hospitality (HT)

- Braemar Hotels (BHR)

- Ashford (AHT)

- Condor Hospitality (CDOR)

- Sotherly Hotels (SOHO)

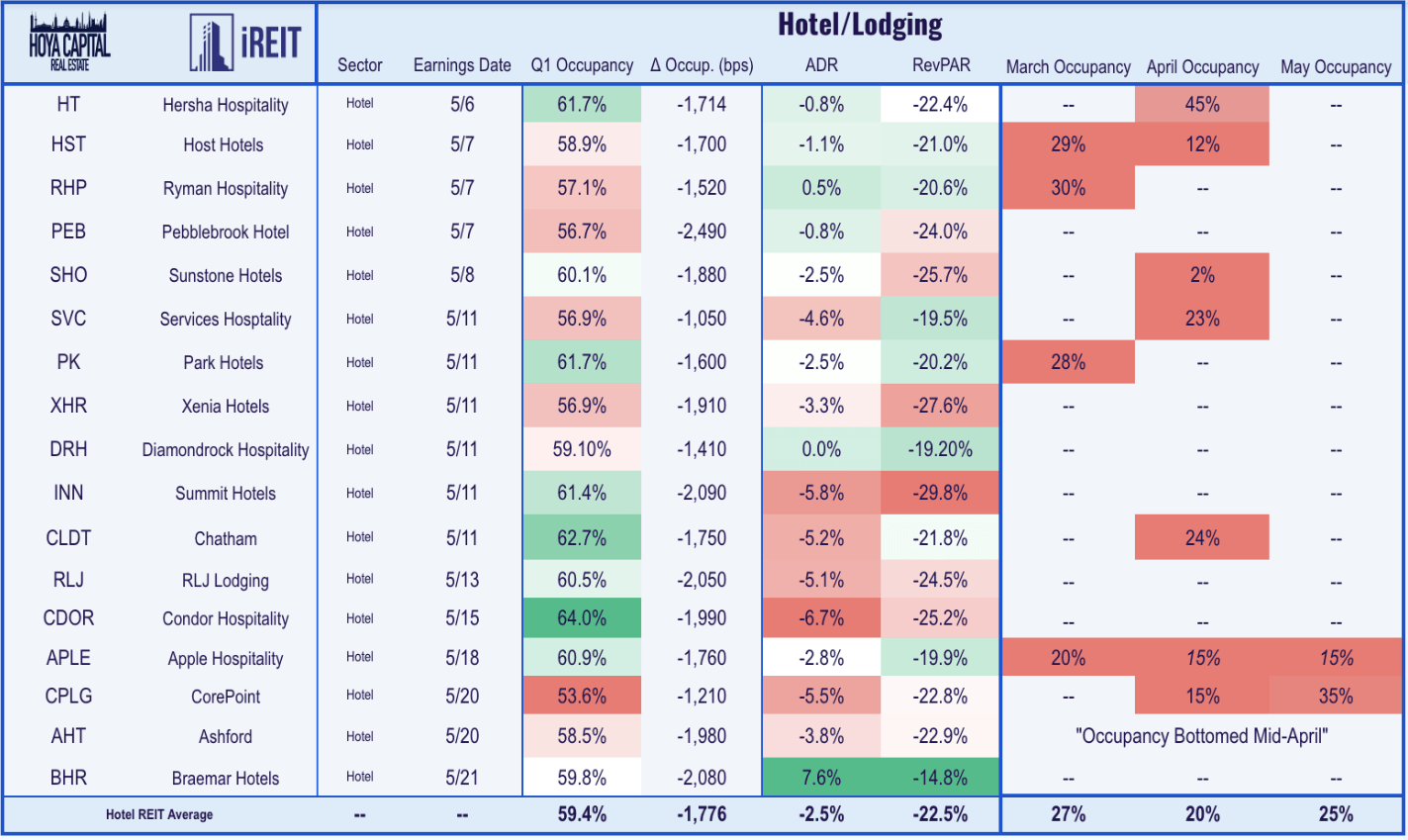

As illustrated below, occupancies declined substantially in March, April, and May. RevPAR declined by an average of 22.5% in Q1-20 and based on March and April news, it appears that Q2-20 will be a “bloodbath”.

Host Hotels, the largest Lodging REIT, reported a 23.4% drop in US RevPAR in the quarter as demand and travel, generally, collapsed in March.

Pebblebrook reported weak results in Q1-20 as March RevPAR was well below estimates and left the company scrambling to cut operating costs.

The focus for REIT investors going forward is the outlook for the cash burn rate and the company’s positioning for a recovery in demand later this year and beyond. Let’s take a look at Lodging REITs balance sheets below:

As you can see (above), it doesn’t look so good for the high leveraged REITs such as Sotherly, Ashford, Braemar Hotels, and CorePoint. Given this grim outlook, we believe that there could be some vulture activity on the horizon as certain REIT business models become tested. As Warren Buffett reminds us,

“Only when the tide goes out do you discover who's been swimming naked."

The distress within the Lodging REIT sector is far-reaching, as illustrated below:

The question that investors need to be asking is whether or not the business models will return to normal? Or, will COVID-19 provide long-lasting damage as hotels and their operators must adapt to post-COVID-19 safety and security protocols?

As viewed below, the Lodging REIT sector is the second-worst performing property sector YTD:

Apple Hospitality: Rising from the Ashes

Recently we provided iREIT on Alpha members with our very first upgrade in the Lodging REIT sector. While we know it’s way too early to initiate sweeping upgrades in the sector, we feel as though Apple has a strong case for the upgrade.

This REIT invests in upscale and upper-upscale hotels and is one of the most diverse Lodging REITs with a portfolio of 233 hotels (with 28,000 rooms) and is also has highly concentrated brand ownership that includes Hilton and Marriott and is ranked among the top five largest owners for both Hilton and Marriott.

The REIT benefits from industry-leading brand affiliation and exclusive ownership of Hilton and Marriott branded hotels with concentration on efficient, rooms-focused properties.

Apple has less exposure to urban, gateway markets, and we believe this will enable the company to mitigate COVID-19 risks due to its geographic focus. As of May 15th, all of Apple’s hotels were surprisingly open and operational, and occupancy remains highest among the peers. Here’s a summary of Q1-20 earnings:

- RevPAR growth -20.7%

- FFO/sf of $.17 per share

- Adj. EBITDA of $53.8 million

- Hotel EBITDA decreased 40.1%

Apple’s largest geographic segment is Suburban (55%) which should allow the company to ramp up faster than most peers. The urban (20%) and resort (6%) exposure will likely be slower to recover.

Apple’s balance sheet is in good shape, with nearly $440 million in cash that includes the draw down revolver funds. Using average occupancy of 20%, Apple’s burn rate is around 24 months. There are limited debt maturities through 2021.

Apple did close on a dual-branded Hampton Inn & Suites and Home2 Suites recently in Cape Canaveral, FL for $47 million ($201k/key). The company terminated an acquisition for a Courtyard in Denver ($49 million) and the company has two other hotels under contract.

Apple recently repurchased around 1.5 million shares for $14.3 million ($9.42 per share) and the company has since suspended its buyback activity.

Source: FASTGraphs

As viewed above, Apple shares are trading at $9.15 and while the dividend is suspended, we believe there’s value to consider: our 12-month price target is $12.00 which represents a 10.0x LTM EBITDA estimate. Given the substantial sell-off, Apple has returned -45% year-to-date, we are forecasting shares to return 40% annually over a 2-year hold.

Source: FASTGraphs

While the Lodging REIT sector is definitely a higher risk play right now, we are beginning to see opportunity, but we are highly cautious. APLE is our only official (Lodging REIT) buy right now, and a speculative one at that. We will soon be adding this REIT to our new DIY REIT portfolio (be on the lookout tomorrow).

Could Lodging REITs Boom After COVID-19?

Lodging REITs have underperformed as travel has been all but halted across the globe. As a result, management teams have swiftly shifted to counteract the impact by reducing staff and suspending operations. Many companies took the steps to preserve liquidity (i.e. cut dividends and draw down lines) to limit their cash burn.

The timeline for reopening remains difficult to predict, with the potential for various segments to behave differently. We are reluctant to recommend Lodging REITs given limited to no visibility on fundamentals and the impact to balance sheets.

We believe it could be an attractive time to enter the space, especially in the drive-to-leisure segment as lockdown easing continues. As we have learned in China, the first traveler to come back has been the domestic leisure traveler.

I look forward to your comments below, and as always, thank you for the opportunity to be of service.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Markets will eventually recover, and may reward patient investors...

Investors need to remain disciplined with their investment process throughout the volatility. At iREIT on Alpha we offer unparalleled research that now includes a "daily" vodcast and mortgage REIT coverage. "There is great opportunity" to take advantage of the selloff.. subscribe to iREIT on Alpha (2-week free trial).

Don't miss our latest CEO interviews including Essex Property (ESS), Farmland Partners (FPI), and Getty Realty (GTY).

![]()

Disclosure: I am/we are long BPYU. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it