Protagonist Therapeutics (NASDAQ:PTGX) is a relatively unknown biotech company focused on the development of novel peptide drugs. The company has recently shown exciting data for their hepcidin mimetic drug PTG-300 in Polycythemia Vera ("PV") which resulted in a doubling of their share price. In this article, I will outline why I believe the market has still not fully appreciated the opportunity of this drug in PV, nor has it properly valued the possibilities for this product in Hereditary Hemochromatosis ("HH"). The company has two other pipeline products that, while earlier stage, each bolster the investment opportunity further.

Company Overview

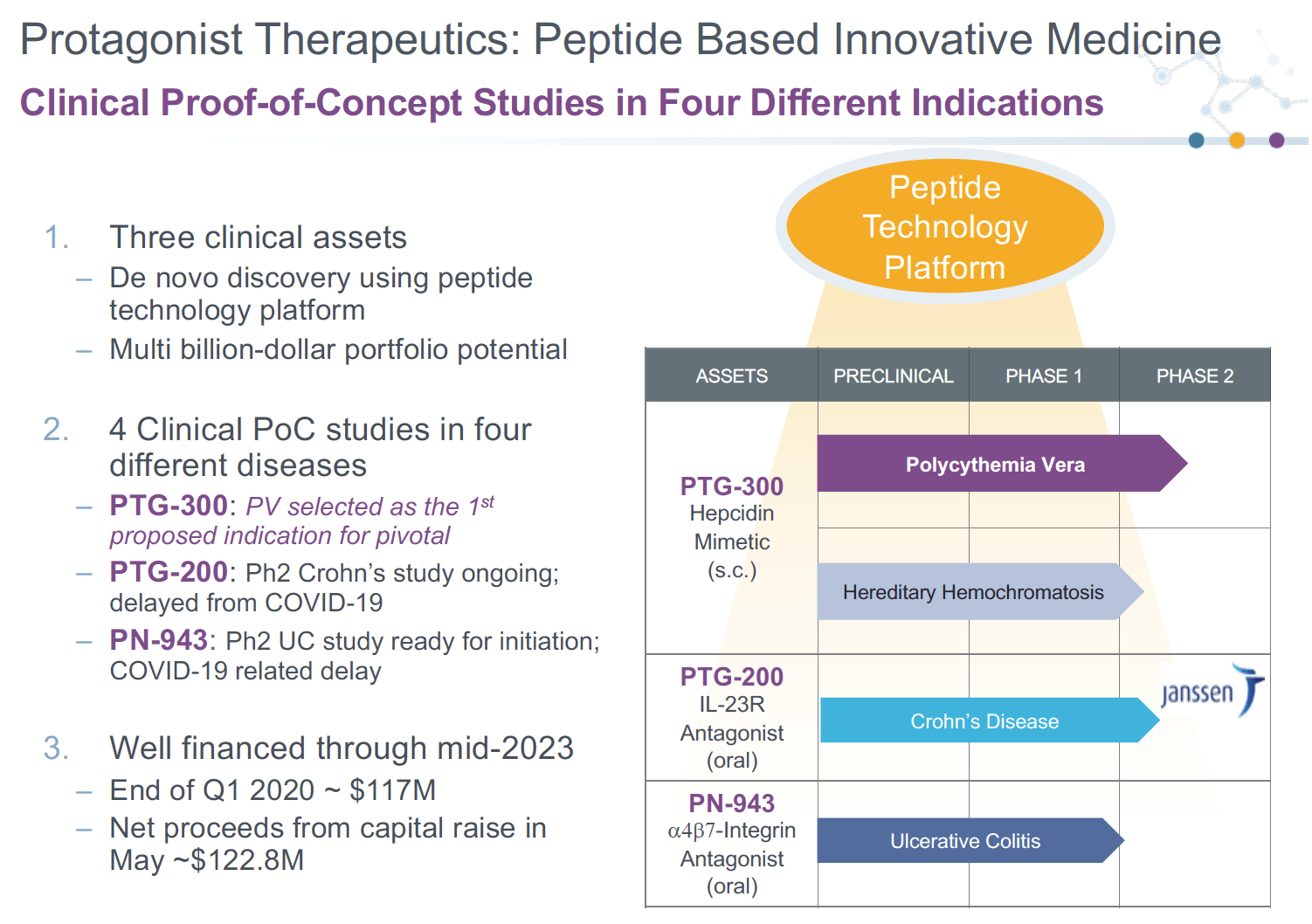

PTGX has a market capitalization of ~$590 million and cash on hand of ~$240 million. They have stated they have enough cash to fund pipeline programs through mid-2023. Their pipeline consists of three drugs as shown below.

Source: Company Presentation

PTG-300 is a hepcidin mimetic, and endogenous hepcidin is a master regulator of iron homeostasis. Given that iron homeostasis has an important role in the formation of red blood cells, the company has focused on blood and iron-deficiency disorders such as beta-thalassemia ("BT"), PV and HH. Interestingly, this drug actually has better drug-like properties than natural hepcidin, which should allow for convenient dosing regimens.

Source: Company Presentation

PTG-300 in Beta Thalassemia

In December 2019, the company showed that the drug improved baseline serum iron levels and transferrin saturation in BT, but it was unknown whether these iron homeostasis improvements would subsequently improve transfusion dependency and other clinical measures in this indication. Given that they have now de-prioritized this indication in favor of PV and HH, it is unlikely that there was a substantial clinical impact. Nevertheless, I am interested to see the interim results of this study on June 12 which will provide more color on this indication.

PTG-300 in Polycythemia Vera

Polycythemia Vera is a disease characterized by an excessive proliferation of red blood cells. Many patients with PV need regular phlebotomy in order to keep hematocrit levels below 45%. Otherwise, they are at a much higher risk of thrombosis and cardiovascular complications. PV patients are also chronically iron-deficient, leading to symptoms like fatigue, weakness, and chest pain. As can be seen by the preliminary data below, PTG-300 dramatically reduced phlebotomy in these patients. PTG-300 also raised ferritin levels - a marker of iron homeostasis - and rescued most of these patients from iron deficiency.

Source: Company Presentation

While these data are early, they are very robust. 6 out of 6 dose-compliant patients are phlebotomy-free through 4-24 weeks, and almost all of these patients showed significant improvements in iron levels. Even if some additional phlebotomy is required, this drug profile compares very favorably to existing treatment paradigms. The mainstay of treatment is frequent phlebotomy, but it is expensive and labor-intensive, and it exacerbates iron deficiency. Cytoreductive therapies like hydroxyurea are used off-label, but it is essentially a chemotherapy agent which can cause vomiting, diarrhea, constipation, infertility and more. Jakafi is the only approved drug (for hydroxyurea-intolerant patients) but is also cytoreductive and can cause side effects such as bruising, dizziness, headache, and diarrhea.

Market Opportunity in PV

Source: Company Presentation

Assuming phlebotomy can be substantially avoided with minimal side effects, PTG-300 could become a standard of care in PV. This is a substantial market opportunity. Per company estimates, there are ~100,000 patients in each of the US and EU, and according to the most recent PTGX investor call, Jakafi only addresses 5,000 patients and has over $600M in sales in this indication for 2019. If you extrapolate a market share of 30% in PV for PTG-300 in the US alone, and assuming similar pricing to Jakafi, that could mean peak sales of greater than $3.5 billion for PTG-300. Given that commercial-stage companies are often valued at >3x peak sales, this could mean a valuation of >$10 billion post-approval for PV. This would represent a 17-fold increase in valuation by the time it reaches commercial approval from this indication alone.

Granted this is a back-of-the-envelope calculation, and there should be some accounting for dilutive financing, but even if this estimate is off by 50%, the company appears to be substantially undervalued at current levels.

PTG-300 in Hereditary Hemochromatosis

PTGX is also evaluating PTG-300 in HH, which is a deficiency of hepcidin in the body. If untreated, it leads to iron overload, which causes symptoms such as enlarged liver, diabetes, cardiomyopathy, diastolic dysfunction, heart failure, and more. There are over 1 million people diagnosed with HH, but most have few symptoms and do not require treatment. Treatment in serious cases is primarily phlebotomy.

It makes sense that a hepcidin mimetic should be an ideal form of therapy for a hepcidin deficiency. In essence, PTG-300 would act as a hormone replacement therapy for people with HH. The phase 2 study that is currently enrolling is structured much the same as the PV phase 2 study, and I am hopeful that results will be similar (reduced phlebotomy and increased ferritin). Timing is uncertain for a first look due to COVID-19, but if they can continue enrolling soon, we should be able to see some data in 2H 2020.

Other Drugs

PTGX is developing a drug called PN-943, which targets the α4β7 integrin for Crohn's disease and irritable bowel syndrome. The best comparable drug is Takeda's (TAK) IV drug Entyvio (Vedolizumab) which has the same mechanistic target and had $778 million in sales in Q4 2019. PN-943 is an oral drug versus IV Entyvio which offers commercial advantages. The drug will soon enter Phase 2 studies. Given strong pre-clinical and phase 1 results, I am optimistic on the likelihood of success and also believe it is possible the drug has an improved efficacy profile over Entyvio.

Source: Company Presentation

PTGX also is developing a drug called PTG-200 with Janssen (JNJ), an IL-23 targeted drug, in Crohn's disease. Through this partnership, PTGX may obtain lucrative milestones payments, and the partnership with Janssen offers external validation of the company's peptide drug development platform.

Competition

The only other hepcidin mimetic I am aware of is owned by La Jolla Pharmaceutical (LJPC). LJPC-401 showed some interesting early data in HH, despite significant challenges with this drug's profile (very poor pharmacokinetics and half-life compared to PTG-300). LJPC has de-prioritized the drug, and so PTG-300 may not have competition in the foreseeable future besides existing cytoreductive therapies with limiting side-effects.

Risks

PTGX harbors risks typical to all biotech companies such as possible unforeseen side effects emerging, clinical trial failures, and dilutive financing. One of the reasons PTGX is exciting is that their diversified pipeline and strong cash position help mitigate these risks. In addition, the fact that proof of concept data in PV is very strong and the drug being used is a mimetic of an existing hormone, both are encouraging from the perspective of handicapping good odds on pivotal trial success.

The Path Forward

I wonder if a possible reason why the market has not fully matured to the opportunity is a lack of insight into what the requirements are for pivotal studies in PV. The company has said that, while the Phase 2 study continues, they are meeting with key opinion leaders and regulators to map out a path to regulatory approval. Hopefully, by the end of 2020, the company will be able to crystallize next steps, and the reduced uncertainty will make it easier for investors to commit capital. Personally, I am not concerned, given the unmet need in this population and the strong signal of efficacy. FDA has been very collaborative and thoughtful in allowing companies to bring therapies like these to market in reasonable time frames. I would speculate that trials could be expedited toward approval in the 2023 time frame, plus or minus a year.

Summary

PTGX's compelling PV data in May was a surprise to the market, and I don't think the investment community has had time to fully appreciate the ramifications. Given the probability of success and competitive profile of PTG-300, the opportunity in PV is being dramatically underappreciated. Moreover, the company has numerous other shots on goal with large market opportunities that offer further upside.