Background

Acamar Partners Acquisition Corp. (ACAM) is a blank check company incorporated in November 2018. The management team is top-notch with decades of experience at the global PE firm Advent International ($54B AUM). The focus was to target a business in the consumer and retail sectors. Acamar Partners had a $305M SPAC IPO in April 2019.

On October 22, 2020, Acamar announced a definitive agreement to combine with CarLotz, a used vehicle retail disruptor with a consignment-to-retail sales platform. The indicative Enterprise Value is $827M and the deal is projected close next quarter. Once the deal closes, the combined company will be named CarLotz, Inc., and the resultant entity will remain listed on Nasdaq and trade under the new ticker LOTZ.

Note: Compared to most other equity investment opportunities, SPACs have a unique property that there is a built-in downside protection - the redemption rights allow exiting when the deal closes, if they don't like the deal. Also, when evaluating SPACs (especially those that are yet to announce a deal), it is critical to look at the expertise of their management team, as you are betting on that team's ability to come up with a good target.

Business Combination Highlights

To analyze the structure of the transaction, it is best to start with Acamar's transaction summary sheet in its Investor Presentation published at the time of the deal.

Here are the key items gleaned from the presentation:

- Sponsor/Founder Share Dilution: It is projected to have 114.8M shares outstanding excluding earn-outs (see below). These include 3.8M in sponsor shares. So, the net dilution due to sponsor shares is 3.3%. This is in the low end of the range for SPAC deals. Note: Sponsor shares are dilutive because the sponsors acquire these shares for a nominal price instead of the ~$10 per share paid by retail investors. In general, the higher the percentage ownership of the sponsors in the target business, the higher the dilution, as 20% of sponsors' equity is sponsor shares. The only exception to this "rule" was Bill Ackman's Pershing Square Tontine (PSTH) which had no such dilution.

- Cash-Outs: Original CarLotz shareholders are rolling ~95% of their investment. In other words, CarLotz shareholders are cashing out ~5% of their investment for $33M. There is also a $33M outlay to redeem preferred stock held by TRP Capital partners which led its most recent funding round in September 2017. Note: The best outcome for new investors is if the original investors of the target were to roll their entire holdings. In general, a high cash-out ratio is a bad sign as that implies they don't have the confidence in the business to hold their position past deal close. Low ratios such as this can be due to the original investors seeking to exit for portfolio management related reasons. As such, it is less of a negative.

- Earn-outs: CarLotz shareholders are receiving 7.5M shares in earn-outs while Acamar Partners agreed to defer 3.8M shares (50% of the original founder shares) as earn-outs: half each earned if PPS hits $12.50 and $15 within five years of close. Note: Earn-outs are incentives to the shareholders of the sponsor and/or target. They are usually structured to vest at higher price points. Although the implied dilution is a negative, substantial earn-outs at higher price-points show some level of confidence in the business as well as alignment of interests.

- Valuation: Pro Forma Enterprise Value of ~$827M implies a 0.88x revenue-multiple on $945M projected 2022 estimated revenue and $122M gross profit. Assuming no redemption, the business will have $321M in cash on the balance sheet.

Business Background

CarLotz was founded in 2011 as a consignment business for used cars with a single location in Richmond, VA (Midlothian Turnpike). The initial capital came from the founders Michael Bor, Aaron Montgomery, and Will Boland along with their friends and family. Over the next two years, they expanded to two more locations. During 2011, they also raised $2M through a couple of capital raises. That money was primarily used to build up the technology platform. They then did a more substantial $5M capital raise in August 2014. This time, the money came from PE firms specialized in retail expansion and so more stores (hubs) were definitely in the cards. The business model at the time was very simple:

- To sell, an owner would bring their vehicle to the closest CarLotz location and pay a $199 fee. The fee is to prep the car for sale. The asking price is up to the owner, although CarLotz suggests one.

- CarLotz then takes over and handles the rest of the process including test drives.

- When the car is sold, CarLotz takes a flat $699 fee and issues a check for the rest to the owner.

While the model was very simple and catered well to sellers wanting a better deal than the trade-in offers, there was one major flaw that would preclude them from really disrupting the used-car retail industry: the consignment model only works for a minority of the people who are looking to sell their cars. Sellers usually need a replacement vehicle immediately which is partly funded using the money from selling their existing vehicle. The consignment model therefore causes a mismatch: sellers have to either raise cash to replace the money that is tied up or have to go without a car for ~30 days. One way to solve the problem would have been to offer cash advances to sellers, but the company probably did the right thing and opted not to pursue that, as that would have involved taking on credit risk - a risky proposition, given its status as a small business.

During the period through 2017, it added two more stores. In the interim, it became increasingly clear that it needed a business transformation to grow profitably. Such an opportunity came to light with the hiring of Brent Garrett, who had a background in remarketing and fleet management. He saw an opportunity to address the flaw in the consignment model: rather than trying to disrupt the sell-side which is what most of the competition is doing any way, why not disrupt the buy-side by sourcing cars from fleets. This insight proved to be a stroke of genius/luck: in the crowded user-car retail arena, it stumbled onto an unexploited niche ripe for disruption. Below is a slide from its investor presentation that shows the dealer/wholesaler/auction loop being bypassed by its process:

Its most recent capital raise was for $30M from TPG Capital Partners in September 2017. Overall, the total amount raised since founding was $37M. This is stunningly low compared to its peers. CarLotz has a revenue to "pre-IPO capital-raise multiple" of 3.1x, which is multiples above its peers. OTOH, its revenue projection for the next three years, is very conservative as it is multiples below what its more mature peers Carvana (CVNA) and Vroom (VRM) achieved after they went public. Below is a comparative sheet that summarizes this:

CarLotz grew revenue from zero to $110M during the last nine years. The low capital used to achieve this growth is also indicative of a superior capital-efficient business model compared to peers.

Growth Prospects and Defensibility

Used-car retail disruption has been a thing since the early 1990s. CarMax (KMX) which arguably is the granddaddy of this theme was founded in 1993 and became public four years later. Given this, one could question how such an opportunity could still exist in the space. A look at the competitive landscape is educational to see what is going on:

- Used-car retail sites that are primarily modern versions of classifieds: Autotrade.com, Cars.com, CarsDirect, CarGurus, etc. belong in this space. These sites generally act as another channel for all types of sellers, and so there is no true disruption happening.

- CarMax and the newer public peers Carvana, Vroom, and Shift Technologies (SFT): All of these businesses source their vehicles from trade-ins and dealers. CarMax also does on-site wholesale auctions to dealers on inventory that do not meet its retail standards. But even CarMax is still not attempting to solve the inefficiencies in the original "wholesale-auction-dealer" loop.

- ACV Auctions: Its model is attempting to disrupt this niche by offering an easy process for dealers to buy and sell cars through 20-minute auctions online. Its focus is on providing trust and transparency in the wholesale market. Compared to dealers having to go to auctions physically, its technology stack and a support team of inspectors offer the same experience online. While this makes the dealer's job easier, ACV's solution does not address the inefficiencies due to the "wholesale-auction-dealer" process itself. Rather, they seek to make the existing process more efficient.

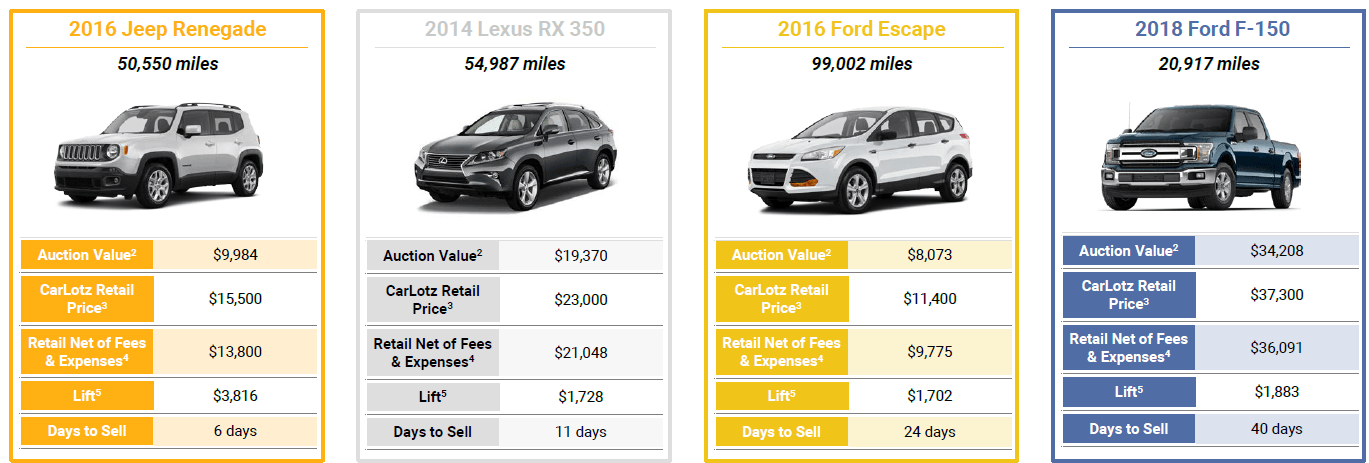

The differentiation with CarLotz's offering is that it is attempting to shrink the inefficient "wholesale-auction-dealer" loop by filtering out the vehicles that can skip that process and go directly to the retail market. But why should inventory that should go directly to retail end up in the "wholesale-auction-dealer" loop in the first place? The reason has to do with the way Fleet Management Companies (FMCs) and other corporate fleets work. FMCs are in the business of handling the full life cycle of vehicles for their clients. To keep the vehicles renewed perpetually, they annually remarket roughly one-fifth of their total inventory. This is done through wholesalers and that is how corporate vehicles enter the "wholesale-auction-dealer" loop. CarLotz instead routes the vehicles directly to its retail channel. The fleet owners are enthusiastic to work with CarLotz as they see immediate value-add. Representative case-studies as below along with fleet owner experience once CarLotz gets its foot in the door accelerates adoption:

The growth plan going forward can be summarized as follows: open 2-3 hubs per quarter at locations that its customers (fleet owners) suggest thereby penetrating existing accounts further, add new corporate accounts by marketing to fleets located at close proximity to the new hubs, and run more volume through the hubs. This looks reasonable and below are its growth projections:

Revenue is projected to grow almost 15x over the next three years at a stunning 145% Compounded Annual Growth Rate (CAGR). While this sounds wildly optimistic, there are a few factors that could help them pull this off:

- ~12M vehicles pass through used vehicle auctions annually of which around half originate from fleet management companies (FMCs) and other corporate channels. The ~$1.6B revenue estimate for 2023 is based on selling ~82K vehicles. So, projection implies penetration of less than 1% of the market of the available inventory. Looking through that lens, the projection appears conservative.

- The model is naturally capital-light, and that is an operational edge compared to peers: Fleets have historically consigned to wholesalers and so it is natural for fleets to consign vehicles when routing through CarLotz's retail channel. But this is a huge advantage for CarLotz - it is able to physically hold inventory at no upfront cost. Its only cost is the retail hub lease and maintenance expenses which is the same for everybody. This is unlike its peers whose capital requirements are directly proportional to the inventory held.

- As CarLotz is the only player in the retail remarketing space currently, vehicle sourcing is largely non-competitive and that is another operational edge. As new hubs get added near sourcing partner inventory locations, they are able to penetrate existing accounts more and bring in new corporate accounts. This results in a feedback loop.

- CarLotz has the lowest CAC (customer-acquisition-cost) per unit in the industry at $315. This is compared to CACs per unit well above $1,000 for peers. Note: The growth plan calls for $1.5M in marketing investment per newly opened hub which it has never done before. This should help with improving sell-throughs and building awareness among retail buyers. But this would also undoubtedly pressure the outstanding CAC number achieved so far.

- Its peers Carvana and Vroom have already demonstrated similar growth rates after their IPOs and so it should be possible for CarLotz to do the same, given its operational edges. Also, as the TAM is huge (~$840B) and the penetration is still very low, there is plenty of room for multiple-billion-dollar players to show high growth rates going forward.

- The technology platform and customer-experience-focused approach have resulted in an industry-leading net promoter score (NPS) of 84. On the sell-side, fleets send them assets and they maximize its value. In addition, the technology platform with interfaces that provide condition reports, forecasting, recommendations, and other analytics keeps the sellers up-to-date. On the buy-side, the technology platform offers a frictionless transaction that still offers huge value to buyers.

Once competition gets wind of this new sourcing idea, it would only be a matter of time before there is competition in the sourcing arena. Said differently, is there anything preventing competition from entering the space and destroying the non-competitive-sourcing edge that CarLotz has? - Turns out, it has foreseen this problem and is attempting to build a durable moat as follows:

- Technology Platform for Sellers: CarLotz has built the world's only retail remarketing asset management solution. The solution works as follows: sellers assign vehicles to CarLotz through its portal application or from another interface using its API plug-ins. Once CarLotz gets physical possession of a vehicle, it goes through its proprietary reconditioning and reporting apps which builds a digitized representation of the vehicle as well as its condition. Its technology stack with AIML (Artificial Intelligence Markup Language) interfaces provide deep integration with its corporate vehicle sourcing partners and that makes possible the availability of information in real-time in the format it expects. The idea is to make all the information it has available to its clients in real time. The analytics that are passed through include reports on how their vehicles are selling, what is/not selling well, and intelligence on other types of vehicles that they are not yet sending to CarLotz. This allows it to look through its portfolio and ensure that CarLotz gets the best vehicles that will sell the best at retail. Over time, the intelligence developed about the fleets of its clients should act as a durable moat as fleets are incentivized to use its platform more.

- Human Resource integration: Remarketing departments of the top fleet management accounts are offered a physical resource to help them decide which of their vehicles are best suited for remarketing through CarLotz and which should go to their remarketing team to be distributed across the auction channels. Over time, this type of integration should create a wide moat.

The technology platform on the buy-side is also impressive. It is an omni-channel interface that allows the buyer to step on and off the digital journey whenever they like. Customers can pick a car, set up trade-in details, choose financing/warranty/etc. options, and have the vehicle delivered. Or they can choose to do everything face-to-face or step off the digital platform somewhere in between.

Valuation and Summary

The common shares have barely budged since deal announcement and so you can still buy the shares at close to redemption value. At that level, the valuation is an ~8x multiple on 2020 estimated revenue. This is a little above the multiple that Shift Technologies is currently trading at. But you are paying that premium for a business that has far greater growth prospects. Also, its profitability measures are much higher, as seen below:

Note: Shift is the closest comparable public peer and it came to market recently through the same De-SPAC route.

The consignment-to-retail sales model is unique, and the total addressable market (TAM) is huge. Despite several larger players sharing the used-car retail disruption pie, CarLotz has a first-mover advantage in its retail remarketing niche. There are two key factors that should allow it to capitalize on this first-move advantage:

- Building hubs near its corporate client premises, and

- embedding its technology platform at client sites thereby building cohesion. This should result in a strong moat over time.

There is an apparent bubble in the De-SPAC space. The valuations look out-of-whack with reality among a number of names that have done deals with EV businesses recently. But, outside of EV, there are several names trading near redemption cash value. The Acamar-CarLotz transaction is one such deal. The business prospects of CarLotz are compelling, and so the valuation should re-rate higher in the near term.