Elevator Pitch

I assign a Neutral rating to automotive supplier Lear Corporation (NYSE:LEA).

Lear Corporation's Seating business has set a target of expanding its market share in the global automotive seating market from 23% to 28% in the medium term. The significant $700 million in conquest wins year-to-date suggest that the Seating business has continued to take market share from its competitors. Separately, the E-Systems business' electrification sales are expected to quadruple from $250 million in 2020 to $1 billion in 2025, but there are downside risks to margins in the short term.

Lear Corporation is expected to pay lower dividends for FY 2020 and FY 2021, due to reduced earnings, the dividend suspension in early 2020, and an increase in growth investments. The stock's consensus forward FY 2020 and FY 2021 dividend yields are unattractive at 0.5% and 0.6%, respectively.

Lear Corporation's consensus forward FY 2021 P/E of 11.6 times is not expensive, but I will prefer to upgrade my rating on the stock to Bullish, when its E-Systems business' revenue growth and margin expansion exceed expectations, and the company raises its dividend.

Company Description

Started in 1917 in Detroit, Michigan and listed on the New York Stock Exchange in 1994, Lear Corporation is a Tier-1 supplier in the automotive industry, and its products include seating, electrical distribution systems and electronic modules.

The company generated 76% and 24% of its FY 2019 revenue from its Seating and E-Systems segments, respectively. In terms of earnings contribution, the Seating and E-Systems segments accounted for 73% and 27% of the company's operating income, respectively in the most recent fiscal year.

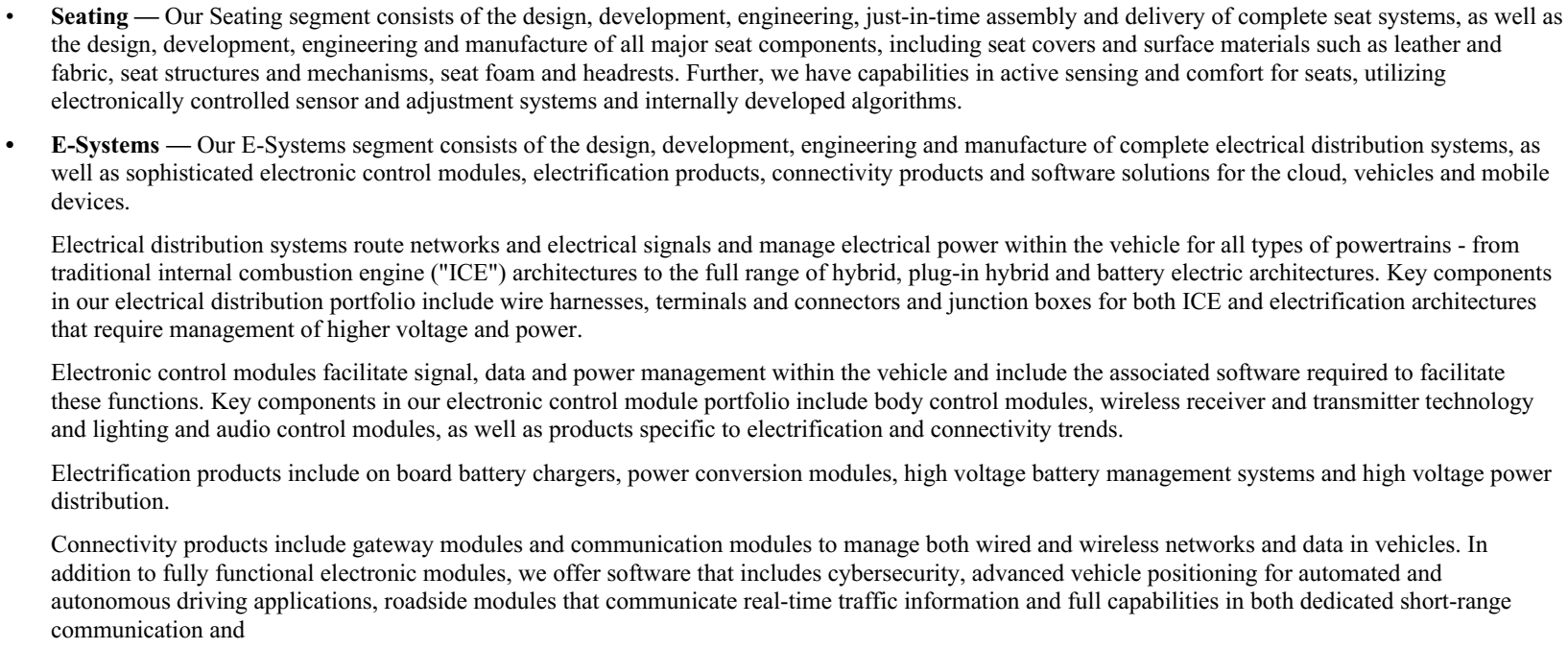

An Overview Of Lear Corporation's Two Key Segments

Source: Lear Corporation's FY 2019 10-K

Source: Lear Corporation's FY 2019 10-K

With respect to geographic sales mix, Lear Corporation derived 37%, 39%, 20%, and 4% of the company's top line from the North American, Europe & Africa, Asia

Asia Value & Moat Stocks is a research service for value investors seeking value stocks with a huge gap between price and intrinsic value, leaning towards deep value balance sheet bargains (i.e. buying assets at a discount e.g. net cash stocks, net-nets, low P/B stocks, sum-of-the-parts discounts) and wide moat stocks (i.e. buying earnings power at a discount in great companies like "Magic Formula" stocks, high-quality businesses, hidden champions and wide moat compounders). Sign up here to get started today!