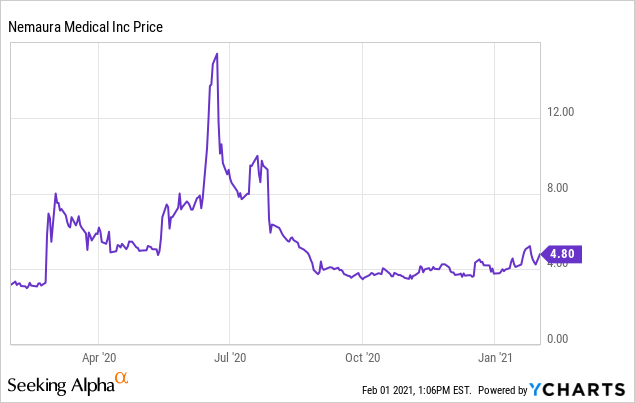

The 2020 stock chart of Nemaura Medical (OTCPK:NMRD), a medical device company with a continuous glucose monitoring (CGM) system, looks like the blood sugar chart of a diabetic patient who went on a sugar binge in June and crashed back down thereafter when their disease got the best of them. Put differently, shares of NMRD rallied big-time in June, reaching an intra-day high of $16.50/share before coming back to earth and settling in around the current share price range of $3.50-$5.00/share.

In this article, I will argue that the share price of NMRD now deserves a valuation much closer to that $16.50/share than its current price of ~$4.75/share. After about a decade of R&D to develop their CGM product, sugarBEAT, and prepare it for commercialization, the company is now prepared for rapid revenue growth in 2021 and beyond. In fact, in December 2020, NMRD launched its product under the name of the BEATdiabetes program in the United States.

Based on my research, I believe NMRD is on the cusp of signing a major deal with at least one large insurance provider, and possibly some large corporations as well. Below I will give background about the company, their products and programs, as well as details about my own research and why I believe NMRD’s efforts to lower diabetic patients’ glucose levels will lead to a sharp rise in their share price.

Company Background

About a decade ago, Nemaura Medical spun off of the privately-held company Nemaura Pharma. Nemaura Pharma had developed a platform technology to put pharmaceutical drugs into the human body through the skin. The company realized through the development of this method that not only could you put stuff into the body through the skin using their methods, but you could also remove things from the body as well. Thus was born Nemaura Medical.

Although NMRD is an independent, publicly-held company, they use the same platform as Nemaura Pharma to draw biological materials from the body in order to determine, for example, a device user's glucose levels. By using NMRD’s device, a user is able to continuously monitor her glucose levels. NMRD’s device and platform has established, through clinical trials, that its technology accurately measures, in a non-invasive way, a user’s glucose levels.

A product such as this takes time to develop. For the first six years of NMRD’s existence, they were able to produce and clinically test a device that was purely functional in the clinical setting. But after that, NMRD took a few years, and roughly $50M, to prepare a device and program ready for wide distribution and commercialization. As noted in the introduction, in December 2020 NMRD launched their BEATdiabetes program for commercialization in the US.

NMRD's Business Plan

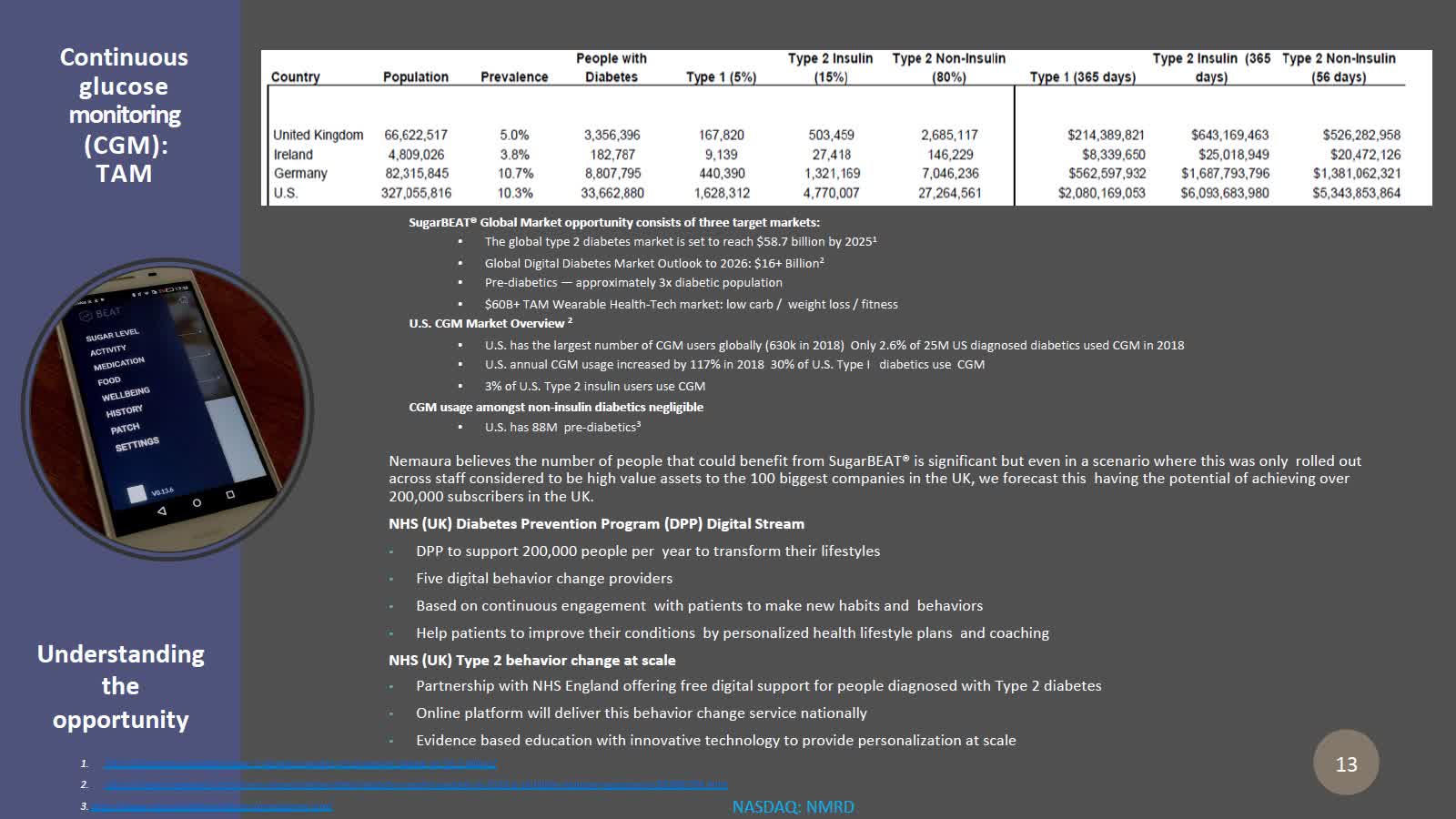

The BEATdiabetes program works by putting NMRD’s device on the user’s arm for several days per month, with one disposable product used each of those days. Rather than pricking a finger several times to draw and test blood, the user only has to draw blood at the beginning of each day the device is used, in order to calibrate the device for that day. While wearing the device, the user’s glucose level is checked every five minutes, with the information gleaned by the device being sent to an app that will provide readings and feedback about their glucose levels. It is important to note that NMRD’s program is not just valuable for the 34+ million type 2 diabetics in the United States alone, but also for the 88 million with pre-diabetes. Accordingly, NMRD’s product and program is relevant to well over one-third of the US adult population alone.

Source NMRD Investor Presentation

Source NMRD Investor Presentation

Of course, having a large possible total addressable market (TAM) is one thing; actually winning some of that TAM and translating it to revenue and EPS is another. In this respect, I believe NMRD’s disciplined approach over the past several years will begin to pay off enormously in 2021 and beyond. According to people familiar with the company, NMRD has been in discussions with large, potential strategic partners prior to their US launch. But NMRD was actually the one “pumping the brakes” on finalizing any of these deals as they were disciplined enough to ensure they were fully prepared to go to market before entering into these types of arrangements.

Now that NMRD is prepared for commercialization, their strategy is to approach large healthcare insurers and corporations. This targeted approach means that NMRD will not need to build and train-up a large salesforce to begin winning customers. In fact, the people familiar with the company to whom I spoke indicate that NMRD is in active discussions with several companies. They believe it is probable that NMRD will sign an agreement with a large insurer and/or a large employer in the first half or early second half of calendar year 2021. This same source believes the company is actually in serious talks with United Healthcare, which would obviously be a huge win for NMRD. Finally, it is believed that by signing one large insurer and/or one large corporation, NMRD could operate going forward on a breakeven basis. Whatever the case, I do believe the company will have plenty of positive news surrounding their US launch and other developments that they will be presenting to investors throughout the first half of this calendar year.

As stated, NMRD will initially focus their US launch around large insurers or employers. The idea, which has been used by other, comparable companies in this or similar spaces, is that the insurer/employer would adopt NMRD’s product and program and encourage its clients/employees to use it for free. The incentive of the insurer/employer is that this approach to dealing with diabetes and pre-diabetes will save them future healthcare expenses, as well as increasing the productivity and reducing time off work for employees. Again, for NMRD, this approach is beneficial not only from a revenue side - obviously a large insurer or employer could help them to quickly ramp revenue - but also from an expense side since the strategy does not require them to invest heavily in marketing and sales.

In the risk section below, I will address some of NMRD’s competition, but will also discuss why I believe their program is better and will be better received by their target market.

Upcoming Catalysts

I expect NMRD to have multiple upcoming catalysts in 2021. As discussed, I believe the biggest announcement is likely to be a large partnership win with an insurer and/or large employer—perhaps both, or multiple wins in each category. In addition to that, I expect by the fall or earlier NMRD will launch internationally through programs in the United Kingdom and, perhaps, Germany.

Source: NMRD's "BEATdiabetes" website

Source: NMRD's "BEATdiabetes" website

In addition to the expansion internationally, I have heard that sometime in 1H 2021, NMRD is likely to launch a direct-to-consumer (DTC) device and program. This approach would be applicable to a broader audience, and would require a different strategy than their main goal of winning large businesses. People familiar with the company believe NMRD’s plans would not at all disrupt or distract from their main goal, nor would they require large sales & marketing dollars. Rather, NMRD would allocate a small budget to promote via social media and through influencer networks. While I initially was skeptical of NMRD possibly entering the DTC market, my contact noted the success of the popular Noom diet app with their large subscriber base and annual revenue. So while NMRD’s primary focus will be winning large employers/insurers, they do want their product to be available DTC as well.

The final catalyst worth mentioning now is NMRD’s expected expansion by the end of 2021 from measuring glucose to also measuring a user’s build-up of lactate and their levels of the stress hormone, cortisol. Measures of lactate are especially helpful to athletes to determine and objectively measure their endurance and stamina. This product could potentially take off with the endorsement of a major athlete. As for cortisol monitoring, the stress hormone levels are considered to be a key indicator of chronic disease. Identifying activities or situations that significantly increase your cortisol levels, and learning to control or avoid them, could be extremely helpful in warding off chronic health problems.

By the end of 2021, and with these added measurements as part of their device and program, NMRD will be able to provide users with a fuller metabolic panel to help them manage their health than any comparable product of which I am aware on the market.

Insider Ownership and Dilution

NMRD is tightly-held by insiders. As of their last 10K filed with the SEC, the Officers and Directors of the company owned 57% of outstanding shares. In addition, holders of 5% or more of the common stock account for another 11% of shares, meaning that a total of 68% of shares are in strong hands, and that management is aligned with shareholder interests.

To that end, I should note that a source I spoke with who I believe is familiar with the company’s thinking indicated that now that NMRD has launched BEATdiabetes in the United States, they will not even consider any additional equity raises (the primary way their R&D has been funded to this point) unless their shares reach around $15/share, more than triple the current price. In fact, according to NMRD’s most recent 10Q filed with the SEC, they have an $8 million unsecured senior credit facility made available from “certain major stockholders” on August 1, 2019. The credit facility is non-dilutive carrying 8% interest with quarterly interest payments only and the principal being due on maturity in 5 years. Importantly, no drawdown has been made to date (although the company does have one $6M loan outstanding from another source). It appears that NMRD management, now on the cusp of winning some strategic partnerships, would like to avoid further dilution.

Speaking of dilution, the last time NMRD raised money through equity, they were able to sell over 1.5M shares for $7.25/share with half-warrants available at $8.00/share. That means that in addition to the $8M credit facility mentioned above, NMRD will have access to another $6M+from warrant exercise if their share price exceeds $8/share. More encouraging, however, is the fact that 1.5M shares were able to be placed at a significant premium to current prices. In short, I believe current investors should not be worried about any additional capital raises unless shares triple or more. With a cash burn of $1.5M per quarter without any revenue, and with some revenue likely coming in the back half of the year and more beyond, NMRD seems well positioned to fill its one to two-year operational needs through their cash, warrants, and credit facility.

Valuation

Valuing NMRD at this time is a difficult task since the company historically has had no revenue. However, a company should be valued on its expected future potential, so we can examine a few things to give us a rough estimate. When I do that, I cannot provide a precise “price target,” but I do conclude that a share price in the $4.75 range is significantly undervaluing NMRD’s potential.

As noted in the “Upcoming Catalysts” section above, the popular Noom diet app has exploded to well over $200M in revenue. That app is only DTC. With NMRD, not only will they eventually have a DTC program, but they will have a “captive audience” with the customers/employees of insurers/corporations with whom they partner. Furthermore, NMRD’s program is much more extensive than the Noom app, with the ability to give not only CGM readings, but also soon a fuller metabolic panel.

I noted earlier that a source familiar with the company believes NMRD can operate at breakeven with only one large insurer/corporation win. So any more than that, or with any breakout from the DTC launch, and NMRD could begin to show some nice EPS. The company’s earnings leverage should be substantial as sales & marketing and R&D expenses should not significantly increase from current levels, and with a razor/blade model with their device and disposables, the company should enjoy nice margins.

Taking all of this into consideration, as well as the company’s tightly-held float and low trading volume, I believe some large wins could send the stock soaring back or beyond all-time highs in the $15/share range, more than triple current prices.

Risks

Clearly, NMRD is not without risk. They are, after all, currently a zero revenue company. So the clearest risk is that NMRD could fail to win any significant insurer/employer. In that case, NMRD’s revenues would continue to lag and they would more quickly burn through their cash and credit line. Based on current expectations, I do not believe this scenario will play out. But failure to win significant business in 2021 could put NMRD in a position where they need to raise extra cash.

Another risk is that NMRD may decide to complete a capital raise at a lower share price than in my assumptions above (around $15/share minimum). Since NMRD is targeting large companies to win their business, these companies will want to see sufficient cash on the balance sheet to ensure NMRD will not be going away anytime soon, putting them in a bind after adopting and promoting the BEATdiabetes program.

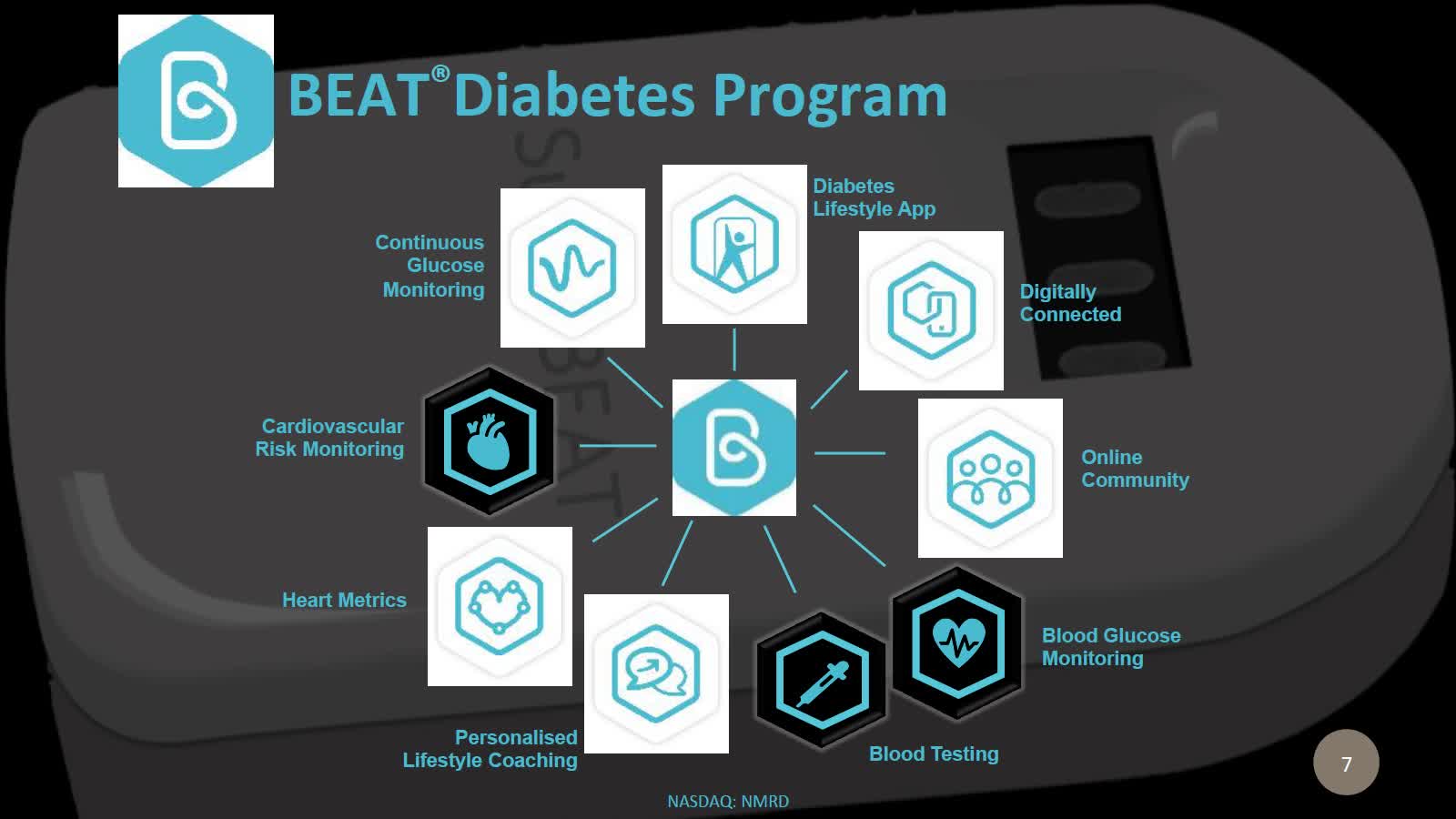

Yet another risk for NMRD is competition. The list of diet apps and fads is too long to consider listing! But the BEATdiabetes program is anything but a fad, nor is it simply a diet plan. Rather, BEATdiabetes is a program scientifically developed to help avoid or reverse type 2 diabetes. In addition, the program comes with the availability for 1-on-1 coaching. And unlike competitors such as Livongo (LVGO), Omada, and Virta, NMRD offers a longer-term, more cost-effective approach. Furthermore, NMRD will stay with their partner companies for as long as they operate the BEATdiabetes program. Many of its competitors set up companies with a 3-4 month initial assessment, but NMRD will be partnering with their customers for as long as the partner uses their programs.

Source: NMRD Investor Presentation

Finally, some investors express concern over the rumors of Apple (AAPL) and Samsung (OTCPK:SSNLF) adding blood sugar monitoring to their next generation of smartwatches. To me, this simply validates the market opportunity and the significant TAM. Apple and Samsung will not be direct competitors with NMRD, except perhaps in the DTC space. And even there, Apple and Samsung will not be incorporating all the capabilities NMRD will have by the end of the year. For example, Apple and Samsung are not also measuring cortisol and lactate. Moreover, Apple and Samsung will not be seeking out large corporations with whom they can partner on a full health improvement program. But Apple and Samsung’s moves indicate the marketplace is seeing demand for the type of product NMRD offers. There will be plenty of space for NMRD, Apple, and Samsung, each serving their target market.

Conclusion

NMRD shares have fallen significantly since their 2020 highs. But the company has never been in a better position to begin succeeding in the marketplace and to ramp revenues. The company has multiple catalysts expected this year and is unlikely to tap back into the capital market for funding absent a tripling or more in share price. With a float that is tightly-held by insiders and a stock that is thinly-traded, NMRD shares could rocket on the announcement of a major win, which would not only mean the company could possibly operate at breakeven, but would validate their business plan. In my opinion, investors would be wise to take a position in the stock now, at a steep discount from the price investors paid during the last capital raise, to ensure they are ahead of any major announcement.