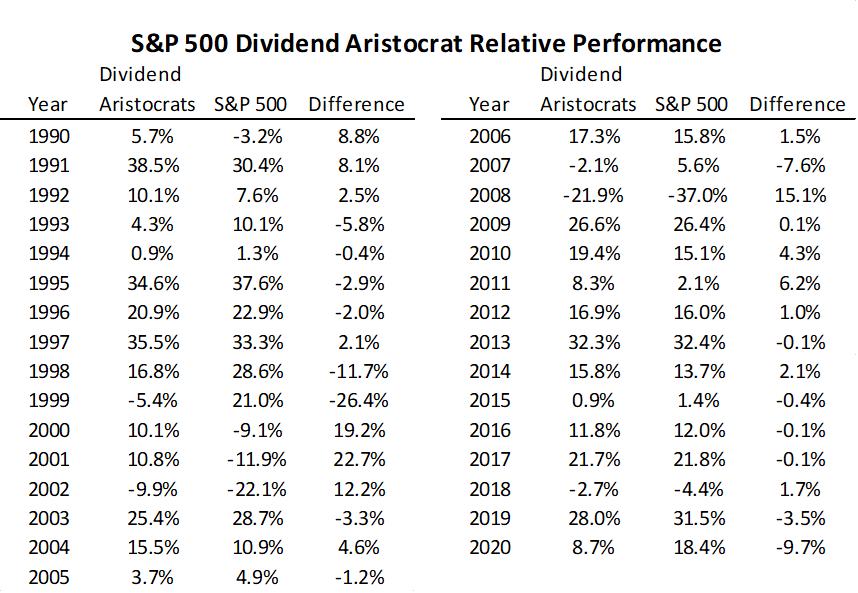

Over the past three-plus decades, the Dividend Aristocrats (BATS:NOBL) have outperformed the broader S&P 500 (SPY) from which they are drawn by 1.68% per year. The strategy has outperformed in the past six down years for the broad market - 2018, 2008, 2000-2002, 1991. In 2020, the dividend growth strategy returned 8.7%, meaningfully lagging the 18.4% for the S&P 500. That was the worst relative return for the strategy since 1998 and 1999 when Tech drove the capitalization-weighted market index towards its bubble heights, leaving dividend growth stocks behind.

The table below shows the key driver of the underperformance of the Dividend Aristocrats in 2020. Like the 1998-1999 episode, the driver of the performance differential in 2020 was the tech weighting. The dividend growth strategy was meaningfully underweight Tech, and did not have exposure to high-flying Amazon (AMZN), the largest Consumer Discretionary company in the S&P 500 Index. Away from tech and Amazon, the average Dividend Aristocrat stock did better (8.7% vs. 5.1%) than the average non-tech, non-Amazon S&P 500 constituent. Unfortunately for dividend growth investors, this outperformance was overwhelmed by the underweight to high-flying tech.

With the Dividend Aristocrats lagging the tech-fueled gains of the broad market, there could be relative opportunities as we look forward into 2021. A cooling of the tech-fueled gains could lead to relative outperformance of dividend growth stocks. While the dividend growth strategy only outperformed by 5bp in February, its underweight to Tech contributed positively to performance (+44bp). Similarly the exclusion of Tesla (TSLA) +19bp, and exclusion of Amazon (AMZN) +14bp in the dividend growth index boosted performance as these recent megacap market leaders lagged on the month.

In the table below, the list of the current Dividend Aristocrat constituents is sorted descending by indicated dividend yield, and lists total returns, including reinvested dividends, over trailing 1-, 3-, 6-, and 12-month