As SPACs fall out of favor, an attractive business combination such as the deal for FTAC Olympus Acquisition (FTOC, FTOCU) to combine with Payoneer is even more appealing now. The global payments market has decades of growth ahead as more companies move to digital payments and the existing companies grow. My investment thesis is even more bullish as investors can acquire the digital payments leader for the same price as major institutions.

Big 2021 Ahead

Payoneer provides a payments platform for more than 5 million marketplaces, enterprise and SMBs in over 190 countries. The company reported 2020 payments volume of $44.4 billion for reported volume growth of 53% and adjusted volume growth of 67%. Due to low international travel, revenue only grew 9% for the year and transaction profit was up just 11%.

The digital payments company connects emerging markets to developed countries allowing investors to fully participate in global e-commerce growth. The global payments market is currently listed at an estimated size of $26 trillion with ~$8 trillion of the volume outside the top 7 economies such as the U.S., Japan and Germany.

Source: Payoneer deal presentation

The company provides a full suite of payment options for marketplace ecosystems allowing for money to be deposited into a Payoneer account, mobile wallet, and even physical and virtual cards or sent via bank wires and paper checks. The full suite of payment options makes the payments platform attractive to marketplace participants.

Without COVID-19 impacts on international travel, Payoneer saw payment volume surge 67% last year with adjusted revenues growing 31%. The digital payments platform reaffirmed strong 2021 financial guidance as follows:

- Payment volume of $64 billion.

- Revenue of $432 million.

- Transaction profit of $311 million.

The company is targeting payments volumes to surge nearly 50% for the year with revenues growing nearly 25%. The long-term model has revenues and adjusted EBITDA growing at a 20% annual clip similar to how other payments volumes provide consistent growth.

With the stock down to only $10, the market might be focusing too much on the reported Q4 revenue increase of only 11% and the annual growth of just 9%. As mentioned, the drop in international travel reduced payment volumes and the higher take rates on these payments impacted the revenue growth despite still strong payment volume growth.

The company saw the total take rate collapse during the year from 1.1% in 2019 to only 0.78% in 2020. The take rate is forecast to only fall to 0.68% this year providing a closer connection with the payment volumes growth.

Cheaper Now

Since my original article on the Payoneer SPAC deal, the stock has only gotten cheaper. FTOC initially popped above $14 on news of forming a business deal in the digital payments area and now the stock is only worth slightly north of the $10 PIPE price. A new investor here gets to invest at the same price as the $300 million PIPE, which includes existing investor Wellington Management, as well as Dragoneer Investment Group, Fidelity Management & Research Company LLC, Franklin Templeton, certain funds managed by Millennium Management.

With 372 million shares outstanding, Payoneer is only valued at the $3.7 billion deal value with an EV of just $3.3 billion based on a net cash position of $525 million on the deal closing.

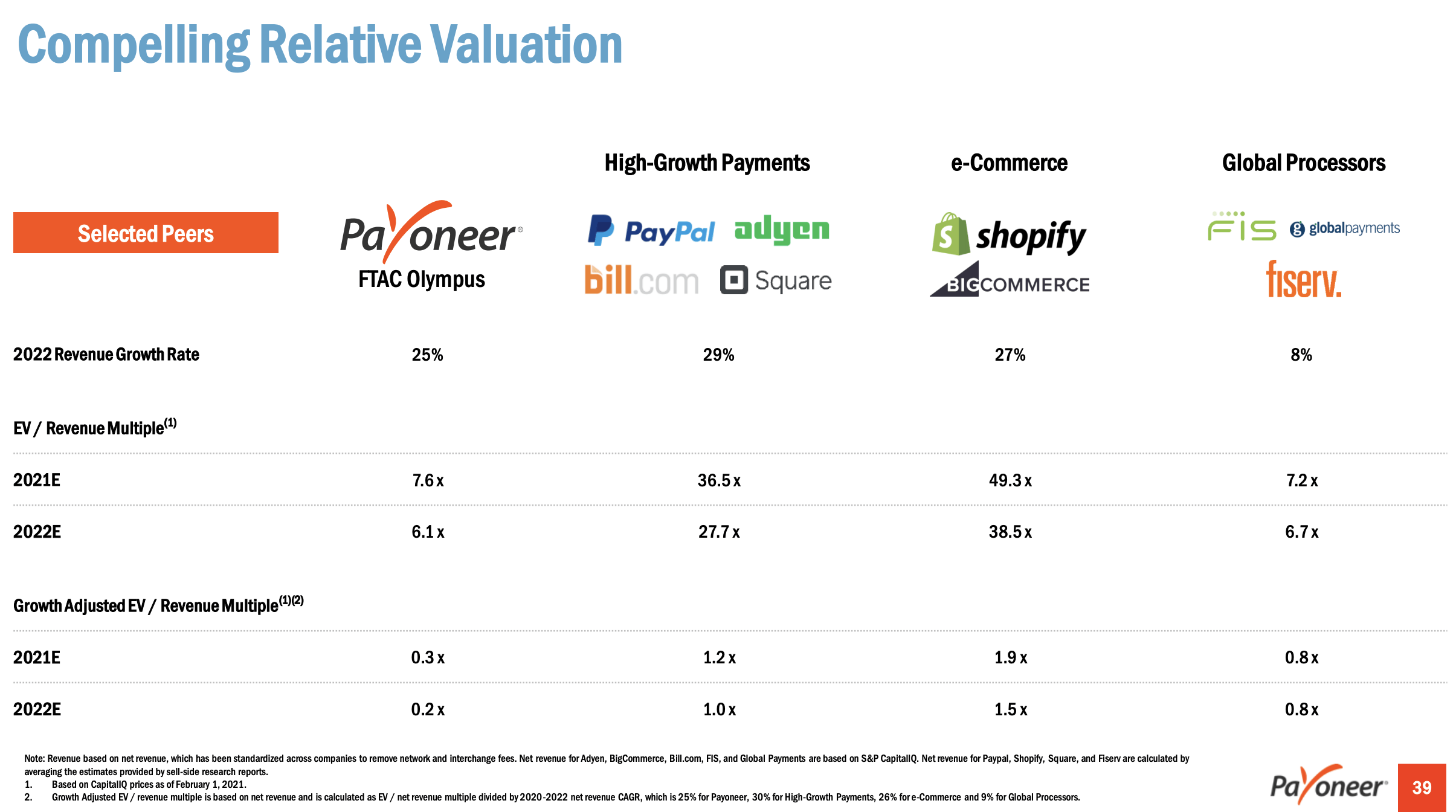

The stock only trades at 7.6x the current EV. Compared to other payment companies, this SPAC trades at similar valuations to slow growth, global payment processors. The company has the same growth rates of PayPal (PYPL), but trades much more like Fiserv (FISV).

Source: Payoneer deal presentation

As an example of the valuation disconnect, Bill.com (BILL) trades with a $13 billion market valuation and the company only has a FY21 revenue target of $212 million. The company only had $35 billion in payments volume last year in comparison to the $44 billion achieved by Payoneer.

Of course, Bill.com went public back at the end of 2019 trading around $35 following an IPO pricing at only $22. The stock hit nearly $200 earlier this year and now trades for around $163. The point being that these payment stocks tend to start slow before taking off once the stock market fully understands their growth potential.

Payoneer is definitely not guaranteed to follow the growth trajectory of these other payment stocks. The company has to hit their financial targets after closing the SPAC deal and the valuation assigned to stocks like Bill.com aren't logical in normal markets.

Takeaway

The key investor takeaway is that Payoneer is a cheap stock ignored by the market with the flood of SPACs. The digital payments company has a strong future and payment stocks tend to start off slow before the market becomes familiar with the consistent growth trajectory offered by the platform. Investors should use the current weakness to load up on FTOC.

If you'd like to learn more about how to best position yourself in undervalued stocks mispriced by the market, consider joining Out Fox The Street.

The service offers model portfolios, daily updates, trade alerts and real-time chat. Sign up now for a risk-free, 2-week trial to start finding the next stock with the potential to double and triple in the next few years without taking on excessive risk.