This article was amended on 4/28/2021 to reflect clarifying remarks in the 'Personal Opinion' section.

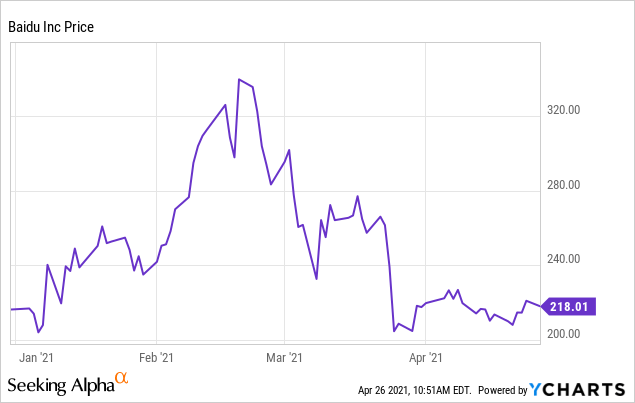

A Non-Fundamental Driven Sell-Off

In my previous articles on Alibaba, I received some comments from readers to research on Baidu (NASDAQ:BIDU), another seemingly undervalued Chinese tech giant. As a result of the Archegos sell-off, which was driven by a series of margin calls, Baidu's share price plummeted more than 30%, drawing my attention to the company once more. In this article, I will explain why Baidu is a great way to gain exposure into the rising autonomous driving industry as it allows you to benefit from the growth potential, while the company's strong cash generating core businesses provides downside protection.

Business Segments

Baidu is a Chinese technology company which specialises in artificial intelligence (AI) and internet services. They are most well known for being the "Google Of China" as a result of their legacy search engine business. Today, the company

operates in two main segments: Baidu Core and iQIYI. Baidu Core includes businesses which relies on Baidu's leading AI technology engine while iQIYI is a digital streaming platform which Baidu owns a majority stake in.

Based on the company's reports and personal judgement, I have grouped Baidu's main business segments as follows:

Source: Authors compilations from Baidu's 2020 10-K

Breakdown of Revenue & Income

Source: Author's compilations, blue parts denote Baidu Core business segments while green denotes iQIYI

The majority of Baidu's revenue is derived from its "Baidu Core" business, with online marketing services constituting the bulk. Cloud services is Baidu's fastest growing segment while the company is slowly attempting to reduce its reliance on its legacy online marketing revenue.

In terms of net income, only the online marketing segment is currently profitable for Baidu.

Area For Growth

Growth In Digital Advertising Spend

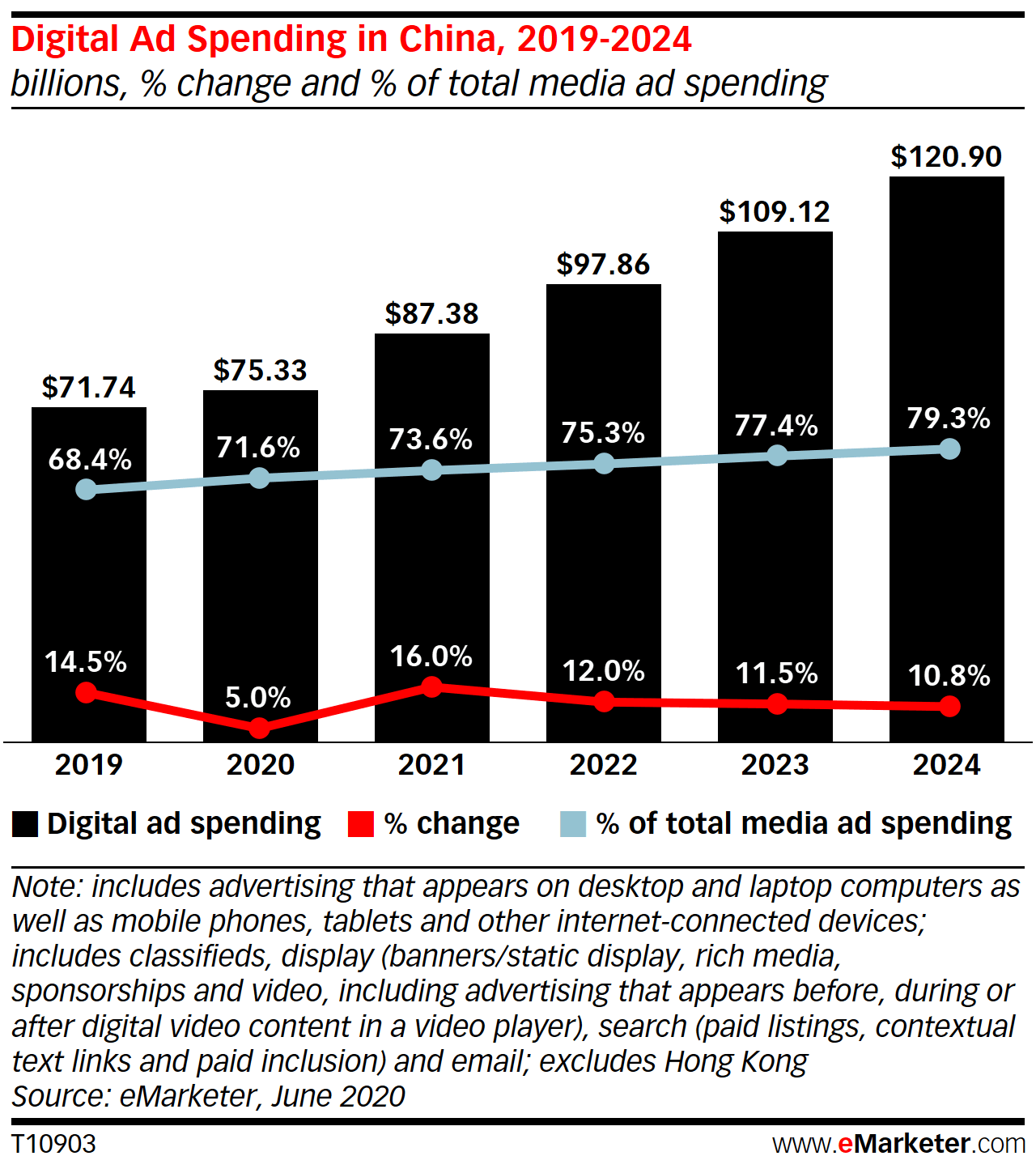

Digital advertising is currently Baidu's main revenue generator. Over the next few years, digital ad spending in China is expected to continue growing at a stable ~10% annually. While these figures are not exceptional due to the fact that China's digital economy is already well developed, it is still positive news for Baidu as this allows its cash generating core business to continue growing to fund the company's other ventures.

Source: Emarketer

Growth In Cloud Computing

Baidu's fastest growing business is its AI Cloud Service as it seeks to ride on China's rapidly increasing cloud adaptation. I quote from my article on Alibaba's growth prospects: "The cloud computing market is a rising industry in China as cloud services is part of the nation's drive to upgrade its economy by incorporating a range of new technologies such as big data and AI. This is reflective in the "Made In China 2025" Plan which places a key emphasis on IT development and independence."

The cloud industry in China is expected to be worth 300 billion yuan by 2023, up from 96 billion in 2018. With its AI Cloud, Baidu will likely be able to capitalize on this growth as it is one of the top four cloud providers and tech giants in China. The cloud business segment should be able to grow its revenue by mid to high double digits annually.

For more information on China's developing cloud industry, you can read my other article here.

Autonomous Driving

This is the part where things start to get interesting.

Baidu is the leading player in China for autonomous driving technologies. The company has been researching and developing the technology for autonomous vehicles since 2013.

Currently, Baidu's Apollo fleet has nearly 500 autonomous driving vehicles with a solid track record. As of 31 December 2020, Baidu reported that Apollo had accumulated 4.3 million test miles and 199 autonomous driving licenses in China, while the second place competitor only had 20 licenses. Out of the millions of test miles conducted, Baidu's fleet transported over 210,000 passengers and logged an astonishing zero accidents.

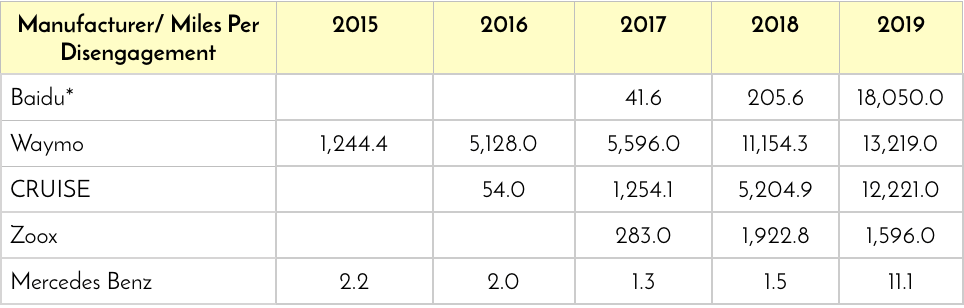

For skeptics who may doubt Apollo's track record given that it is a Chinese company, Baidu also conducted tests in California in 2019 where its feels drove 108,300 with only six disengagements and no accidents. The following table depicts how Baidu fares when compared to its peers during the California tests of 2019.

Source: Author's compilations from TheLastDriverLicenseHolder.com, manufactures denoted by * are based in China

Baidu leads both national and international peers in terms of miles per disengagement - a key metric for autonomous vehicles. However, I will note that Baidu has clocked much fewer miles than Alphabet backed Waymo and GM backed CRUISE. Compared to its local Chinese competitors, Baidu has the second most mileage and longest miles per disengagement by far.

The following table shows the changes in miles per disengagement over the past five years of testing. From 2018 to 2019, Baidu saw an astonishing jump by a factor of >800 times. Although this may be difficult to believe, it still does show that Baidu has made huge improvements in the past year. It is also unlikely that the actual results deviate by much since the tests were conducted in California (not China) and under the watchful eyes of other competitors.

Source: Author's compilations from TheLastDriverLicenseHolder.com, selected reputable manufactures with data across at least three years are included

From this data, we can see that Baidu is the leading autonomous vehicle manufacturer in China and among the top companies in the world, although it still trails a long way in terms of test miles when compared to Waymo and CRUISE.

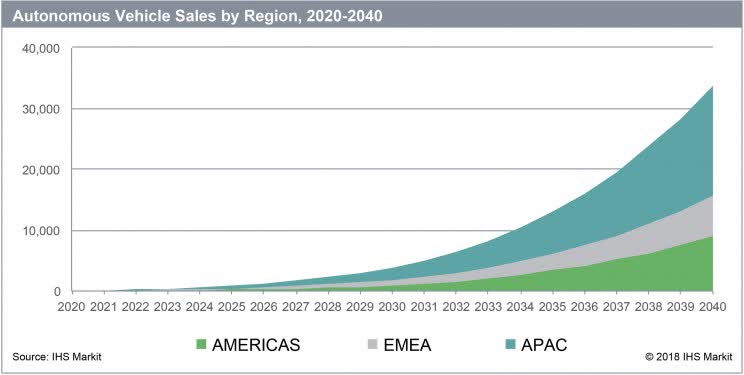

According to research firm IHS Markit, China will sell ~14.5 million autonomous cars by 2040, while global volume will be about 33 million. In the same report, we can see that the development of autonomous vehicles is still a long way from being part of everyday life but will start to take off around 2030. From there on, the industry will experience exponential growth.

Source: IHS Markit Research Adapted From InterestingEngineering.com

Considering that Baidu's main market is in China, where it currently has a significant advantage in terms of track record and autonomous-driving related patents, Baidu should be able to capture a large portion of this growth. If the company can accelerate its AI developments and test mileages, it could also fight for a chunk of the worldwide market, especially in Asia where Chinese companies have a strong presence.

Robo-Taxi Services

Apollo Go's Robotaxi fleet, Source: medium.com

Building on its autonomous vehicles, Baidu is also planning to commercialize robo-taxi services, Apollo Go, in future. The company currently has three robo-taxi pilot programs in Changsha, Cangzhou and most recently, Beijing from October 2020 onwards.

The launch in Beijing, China's capital city is a key milestone for the company's push for autonomous driving as the capital has the most "stringent safety regulations for autonomous driving testing in China". In order to operate in Beijing, Baidu also requires T4 licenses, which allows for road testing in complex, urban road conditions. Baidu acquired this license in July 2019 and is currently the only company with this license.

Through its pilot program, Apollo Go has been well received. In Beijing, Apollo Go's 40 vehicle fleet received >2000 orders on some days. The ride can be easily hailed using the Apollo Go app, Baidu Maps or the Apollo Go Smart mini program in the Baidu app.

According to Baidu's Chairman, we can expect full commercialization of the robo-taxi fleet in around 2025. Baidu appears to be on track to this aim as in March 2021, the company received licenses allowing it to charge for robo-taxi services in Cangzhou. In a statement, Baidu said that "35 of its robo-taxis have been granted licenses by the local Cangzhou government to begin commercial operations"

We expect the autonomous driving industry to enter the stage of full commercialization in 2025," says Robin Li, Chairman and CEO of Baidu.

Mobility-as-a-Service Program

Apart from robo-taxis, Baidu is developing numerous other transportation and mobility autonomous solutions. They include:

- Apolong Shuttles

- Robo-Buses

- Public Safety Robots

- "New Special Vehicles" that can perform a variety of functions such as sweeping and disinfecting the streets as well as dispensing snacks and drinks

Baidu is also progressing well in this area, as the company is said to have received rights to roll out a commercial autonomous bus program in the west of China in April 2021.

Electric Vehicle (EV) Partnership

In early January 2021, Baidu announced that "it would establish an intelligent car company in partnership with the automaker Geely." Both companies will work closely to produce intelligent, electric vehicles by leveraging on Baidu's Apollo autonomous driving systems and Baidu's technologies (e.g. Baidu Map, Baidu IOV OS), as well as Geely's electric vehicle expertise.

This seems to be a logical extension to Baidu's autonomous driving program as a strong intelligent driving software requires a high quality car to complement it, which is something this partnership can provide. With this, Baidu will be able to tap on both autonomous vehicles and EV growth trends.

Electric cars have received policy and market support. Baidu has advantages in its massive volume of user data, which may be applied in self-driving technologies. For Geely, it has what I think is China's best electric vehicle manufacturing platform, which will help them launch intelligent cars," Independent tech analyst Liu Dingding told Global Times

Other Innovation Projects

Apart from autonomous driving, Baidu's AI capabilities and developments also allows the company to be able to create a large range of "intelligent" and "smart" solutions. One rising product line would be the company's Xiaodu smart devices and services.

These include smart speakers, AI voice assistant (similar to Alexa), smart learning devices and smart home devices. The products are powered by Baidu's OS and adopt Baidu's technology such as Baidu Maps and search engine.

Source: Tmall

Source: Tmall

Evaluation On Growth Prospects

Overall, while Baidu should benefit from stable growth in its advertising business and cloud services, the company's main growth driver is undoubtedly its autonomous vehicle programs. Should the company continue to maintain its market leading position in China, it would be able to capture a huge portion of the estimated 14.5 autonomous vehicle sales in 2040. Furthermore, Baidu will also be commercializing autonomous vehicle fleets in the form of robo-taxis, robo-buses and more which will provide the company with even more revenue streams.

Of course, we are still about a decade away from the autonomous vehicle industry fully taking off, but Baidu has the highest chance to succeed in this market in China due to its leading position in developments, test miles, licenses and patents. Once the market develops, the upside and growth for Baidu could be extremely large. In the meantime, Baidu should still be able to log some growth in advertising, cloud services and possibly smart devices.

Competitive Advantage (AI Patents)

Apart from its strong growth trends, Baidu has a key competitive advantage that allows the company to maintain a market-leading position in technology related fields - patents.

Baidu is one of the world's leading company in terms of AI development. The company has been investing in AI since 2010, initially to improve search and monetization. Over the years, Baidu has expanded its AI capabilities and used "Baidu Brain", the company's core AI technology engine in the development of new businesses.

According to Baidu, they are one of the few companies in the world which offers "full AI stack, encompassing an infrastructure consists of AI chips, deep learning framework, core AI capabilities, such as natural language processing, knowledge graph, speech recognition, computer vision and augmented reality, as well as an open AI platform to facilitate wide application and use."

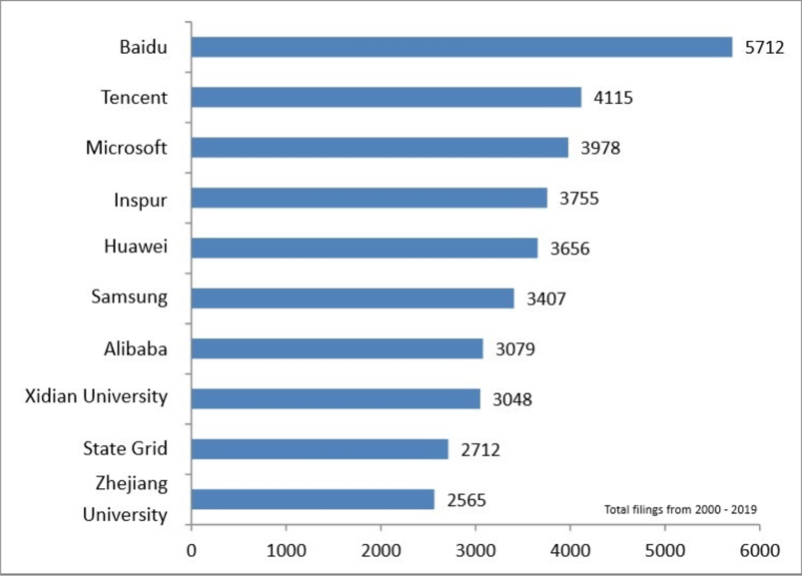

To support the company's assertions, Baidu has the greatest number of AI patents in China among both international and local companies.

Source: GlobeNewsWire (2019 Figures)

As of October 2020, the number of AI related patent applications filed by Baidu almost doubled to 9,346 while the company has been granted 2,682 AI-related patents. Baidu remains the leader in AI patent applications, both filed and held. Key patents include deep learning (438 held), natural language processing (377 held), intelligent speech (330 held), autonomous driving (283 held), knowledge graph (242 held), intelligent recommendations (540 held) and big data for transportation (384 held).

Baidu's market leadership in patents gives the company a strong competitive advantage as it allows for product differentiation and prevents competitors from copying their technology. This means that the company has exclusive rights for a large number of AI related technology which will help to improve the company's core businesses as they rely on AI.

Other Areas Of Strength

Apart from its advantage in terms of patents, Baidu's business has a few other notable strengths that make it a good business.

Dominant Search Engine Market Position

Baidu is considered a monopoly in among pure search engine providers. The company has consistently remained the number one by a large margin in the past decade. As of March 2021, Baidu has a market share of 75%.

Source: statcounter.com

Although Baidu seems to be a monopoly in the Chinese search engine market, I will not consider it a competitive advantage due to a rise in alternative search platforms in China.

In recent years, search in China has been moving away from traditional search providers due to the extensive ecosystems that Chinese tech giants have created. For example, customers can easily search for a product on e-commerce platforms like Tmall, read through community reviews on Xiaohongshu, check out news on Weibo and Toutiao or search for local services on Alipay and WeChat. More will be explained in the section on risks.

Therefore, until we can access the impact of alternative search platforms on Baidu, I will classify Baidu's market leading position as an area of strength instead of a business moat.

Mobile Ecosystem

Baidu has constructed a portfolio of over a dozen apps such as Baidu App, Haokan, Baidu Post which provides "a platform for people to discover and consume information through search and feed, interact and engage with creators, publishers, service providers and merchants". The entire mobile ecosystem is centered around the main Baidu App which has 544 MAUs.

Baidu's ecosystem of apps include:

- Knowledge based apps for news, search, feed and content creation

- Entertainment apps including short form and long form video streaming

- Utility apps such as maps and translators

Source: Screenshot from a Baidu produced Youtube Video

Source: Screenshot from a Baidu produced Youtube Video

Within the Baidu App itself, there are hundreds of thousands of smart mini programs which covers e-commerce, entertainment, education and more. With the roll out of Baidu's smart devices, the company should be able to further enhance this ecosystem of apps and mini programs as more people will be actively using the apps.

Source: Screenshot from a Baidu produced Youtube Video

As Baidu brings more smart devices and products into the market such as driverless vehicles, Baidu's ecosystem could be further expanded and create a network effect for the company. A swath of products ran on Baidu's OS, enhanced by Baidu's AI and all connected using Baidu Apps and smart mini programs, could potentially become an extremely strong ecosystem.

Government Support

In recent months, the Chinese government has ramped up pressure on tech firms to comply to its regulations or face punishment. Notable companies such as Alibaba and recently Meituan have been investigated for monopolistic practices.

As Baidu is also a leading tech company in China, the company will definitely face similar pressures as its peers. However, I believe that Baidu will also be on the receiving end of greater government support as compared to other firms.

The Chinese government has ambitious plans for its automobile industry, with the country aiming to have "vehicles with partial self-driving technology account for 50% of all new-auto sales by 2025". By 2030, this number is expected to rise to 70%. For fully autonomous vehicles, China has set a 2025 target for commercialization and expects level 4 autonomous vehicles to contribute 20% of total vehicle sales by 2030. The government is also looking at adopting top level self-driving technology nationwide by 2035 in their push for smart cities.

This is where Baidu fits in perfectly for the country's plan. Baidu is by far the market leader in autonomous vehicle, with second place Pony.AI a rather distant second. Furthermore, Baidu is a pure local Chinese company while Pony.AI is backed by Toyota, a Japanese company. In order for China to achieve their goals, the government would provide the necessary support Baidu requires to expedite its development process. This is already evident by the fact that Baidu is able to quickly acquire patents and licenses for testing even though the country traditionally has strict laws regarding autonomous vehicle and road safety.

Given China's track record of achieving its ambitious goals (such as eradicating extreme poverty and push to technology), I am confident that the country will be able to do so again with its autonomous vehicle plans. For this to happen, I believe that Baidu will be given the political help they require which is extremely important in state-capitalist nations

Management

With the company's strength and growth prospects, I believe that Baidu's management is capable enough to bring the company forward. At 20 years of age, Baidu is still a founder-led company, with co-founder Robin Li as the CEO and Chairman. The rest of the senior management are also vastly experienced and most have been with the company for over a decade, climbing through the ranks.

This means that Baidu's management is well experienced, has a good understanding on the grounds and the insights to the products and services that Baidu develops.

Risks/Limitations To Growth

In this segment, I will highlight some key risks to Baidu's current and potential businesses that investors should take note of.

Alternative Search Platforms

As mentioned, Baidu's moat in search engine dominance is being challenged in recent years due to alternative platforms to search for different things. However, alternative platforms like Tmall, Toutiao and Weibo do not entirely replace the utility of traditional search engines like Baidu.

A bigger threat to Baidu's search engine would be WeChat. In recent years, WeChat, China's leading social media and messaging platform, has also launched WeChat Search which can screen through content in WeChat as well as web articles, images, videos and more. According to China Internet Watch, WeChat Search has reached 500 million MAUs.

WeChat Search could potentially be dangerous to Baidu as WeChat has 1.2 billion MAUs which the company can leverage on to use their search engine. Furthermore, WeChat Search allows users to search the web too, although the search results are still not as comprehensive as Baidu. I would be interested to see how Baidu reacts to this development.

Over the past five years, Baidu's revenue from online marketing services has also somewhat stagnated, which may suggest that the company is indeed feeling the pressure from alternative platforms. It would be important to keep tabs on Baidu's 2021 online marketing revenue to see if the company manages to bounce back from 2020 which was adversely affected by the pandemic.

Source: Author's compilations

One positive point would be that the DAUs for Baidu App has been increasing over the years, from 161 million in 2018 to 202 million in 2020, suggesting that Baidu still remains an attractive search platform and application for consumers despite the competition.

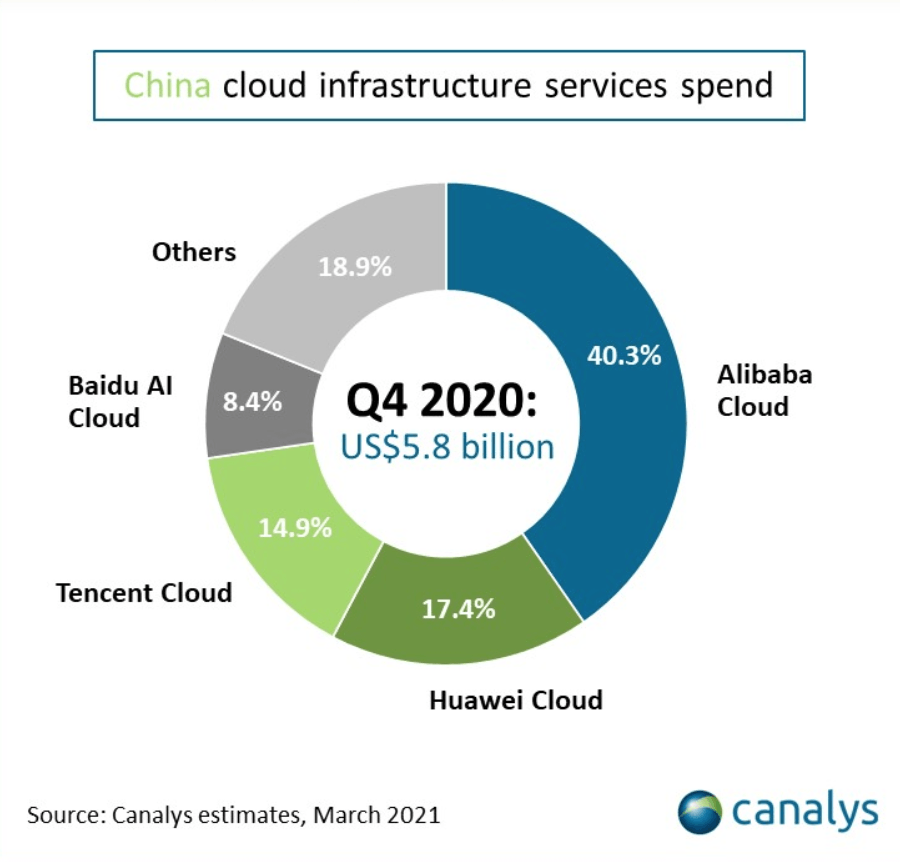

Unprofitability Of Cloud

Cloud services is currently Baidu's fastest growing business segment. However, Baidu AI Cloud is not a market leader in this industry. The company has the smallest market share among the top four tech companies in China (Alibaba, Tencent, Huawei, Baidu) of around 8%.

Source: Canalys

Although Baidu does not report income from individual business segments, its cloud business is likely unprofitable, similar to all other competitors. Baidu may have a difficulty turning a profit in this segment if the company is unable to gain enough market share or scale. For example, Alibaba Cloud, with a dominant market share, only recently managed to turn a non-GAAP profit for 4Q20.

Failure Of Autonomous Vehicle Industry

The autonomous vehicle market is Baidu's largest potential growth segment. However, as with all new technologies, there is huge uncertainty about the future of autonomous vehicles.

First, Baidu may not be able to successfully develop vehicles which are "smart" enough to drive on the busy and crowded urban streets. Second, even if Baidu manages to do so, a strong public buy in will be required in order for the commercialization of driverless vehicles to yield meaning results for the company. As of 2019, around ~35% of Chinese still think that fully autonomous vehicles will not be safe on public roads.

While I believe that there is a high chance of this industry succeeding, it will definitely take quite some time as the technology and public trust both still need to be developed.

Financials

As this article is already rather long and I do not wish to bore readers with more dry information, I will highlight some key financial information and metrics of Baidu:

1. The company's net and operating income has been slightly decreasing since 2018, due to stagnating advertising revenue and increase in costs attributed to the company's new business segments

2. FY21's online advertising revenue will be a key figure to watch to see if Baidu can bounce back from the pandemic infused dip in 2020.

3. Company's margins are still high so there is some leeway for further contraction in margins to accommodate innovation

4. Baidu's financial health is very strong with the company having more cash & short term investments than liabilities

5. Investors should still keep an eye on spending and margins and ensure that Baidu is not spending more than they can potentially earn. Personally, I will be alright if net margins fall to the low double digits as long as I can see tangible developments in both cloud and autonomous driving.

Valuation

Sum Of The Parts (SOTP)

For this SOTP, the values are derived as follows:

P/S multiple for online marketing service was derived using the ten year average P/S of Alphabet (GOOGL) and five year average of Yahoo before it was acquired. The resultant average was 6.8. I have used a slight discount for Baidu's base case to be conservative.

For cloud services, the multiple is adapted from an article titled "Cloud Companies And 10x Revenue Multiples." In 2020, Amazon's AWS traded at around a 12x multiple.

Bear case valuation for iQIYI (IQ) takes the share price at current levels which there is a very strong support, while the bull case valuation is Baidu's own valuation of iQIYI.

Source: Authors calculations

This SOTP valuation is very conservative as it excludes all of Baidu's "future" businesses including autonomous vehicles and smart devices. Therefore, just by valuing Baidu's existing established business segments alone, the company is already trading below its intrinsic value range of $237 to $335. At a current market price of ~$220, Baidu is 23% undervalued from a conservative base case scenario.

Therefore, at today's price, you can buy Baidu's existing businesses at a discounted price and also get the company's up and coming autonomous vehicle and smart devices businesses FOR FREE!

Investment Thesis

The autonomous vehicle industry is still at its infancy and is very complicated. I believe that most investors (including me) do not have an in-depth, technical understanding of this industry. Therefore, it would be very risky to cherry pick companies that we expect to be successful in future. Baidu is a true value investment in this aspect, as it gives investors exposure to the huge upside of the autonomous vehicle market while a protected downside due to the company's cash generating core business. By buying the entire autonomous driving business for free, we also have a huge margin of safety to compensate for the lack of expertise in this field. In the worst case that all new ventures fail, Baidu's legacy businesses are still worth more than what it is priced at today!

It will take a long time to build the public's trust in autonomous vehicles and adopt it as a mode of transportation. Another benefit of Baidu is that investors can afford to hold the company long term for the entire industry to mature, for the company to further develop its AI capabilities and for trust and acceptance to be cultivated. Through all of these, Baidu will still be generating strong revenue from its search engine business and cloud services. In the worst case scenario that autonomous vehicles fail or fail to be implemented on a wide scale (more likely downside), we would still be owning a good business that now owns a huge amount of AI patents which it can re-deploy to other technological developments!

Personal Opinion

In my opinion, I will classify Baidu as a "Good" but not yet a "Great" business due to the upcoming business risks that the company will have to address. Baidu has a moat, but it still does not help the company generate significant revenues as the autonomous driving business is still in its early innings. Therefore, while the moat will likely give Baidu a sustainable competitive advantage in the long run, I cannot say that about the present.

However, I still believe that Baidu is priced below its fair value today and has a strong core business to supplement its exciting growth prospects. Personally, I will not be adding Baidu into my portfolio (as of the time of writing) as I am already overweight in Chinese equities. I would however, be tempted to strike if Baidu's price continues falling (e.g. below $166 which I consider a bargain price) or the company shows that it is successfully able to navigate the risks it is facing (e.g. continually increasing Baidu App MAU and recovering online advertising income despite the threat of alternative search engines).

Some readers might interpret my final paragraph as a contrast to my bullish article. I would like to add that the purpose of adding my own views in is to provide a more rounded perspective on Baidu and to remind investors that the company's key growth driver is still not developed. My own investing decision is also based on other factors such as my portfolio management and risk appetite, therefore it may differ from my rating of the company.