Elevator Pitch

I continue to have a Neutral rating assigned to Woori Financial Group (NYSE:WF) [316140:KS]. Woori Financial's stock price has increased by +11% from KRW9,640 as of January 21, 2021 to KRW10,750 as of April 29, 2021, following my earlier update published on January 22, 2021.

I have a mixed view of the stock.

On one hand, Woori Financial recorded its highest quarterly net profit in almost three years, thanks to robust loan growth, net interest margin expansion, and low cost-to-income & credit cost ratios. On the other hand, Woori Financial's 1Q 2021 CET1 (Common Equity Tier 1) ratio and FY 2020 dividend payout ratio were the lowest among the four major Korean financial services companies, which justifies the company's valuation discount to peers to a large extent. Woori Financial trades at 4.3 times consensus forward FY 2021 P/E and 0.39 times trailing P/B, and it boasts a consensus forward FY 2021 dividend yield of 5.9%.

Considering that Woori Financial's undemanding valuations have priced in most of the negatives associated with its low CET1 ratio and dividend payout ratio, I choose to maintain my Neutral rating on the stock.

Woori Financial's shares are traded on both the New York Stock Exchange and the Korea Exchange. The company's Korea-listed shares are very liquid with a three-month average daily trading value of close to $25 million, while the average daily trading value for its ADRs in the last three months is much lower at around $500,000. OCBC Securities and Monex Boom Securities headquartered in Singapore and Hong Kong, respectively are brokerages that investors can use to trade in stocks listed on the Korea Exchange.

Market Responds Favorably To 1Q 2021 Results

Woori Financial announced the company's 1Q 2021 financial results on last Wednesday April 21, 2021. The company's share price rose by +6% in the past six trading days post results from KRW10,150 as of April 21, 2021 to KRW10,750 as of April 29, 2021. This suggests that investors in general are positive on Woori Financial's financial performance in the first quarter of this year.

The company achieved a net profit attributable to shareholders of KRW672 billion in 1Q 2021, which was equivalent to a +30% YoY increase and a +302% QoQ growth. More importantly, this was Woori Financial's highest quarterly earnings since 2Q 2018. Woori Financial's best performance in almost three years was driven by a number of factors.

Firstly, Woori Financial's total loans at the group grew by +10% YoY from KRW243.4 trillion to KRW268.5 trillion in 1Q 2021. The company's total loans at the bank level (Woori Bank) increased +3% QoQ and +8% YoY to KRW271.1 trillion. Apart from a general economic recovery in Korea boosting loan demand, Woori Financial's strong loan growth was helped by the completion of the acquisition of a 74% equity stake in leasing company Aju Capital in December 2020.

Secondly, Woori Financial's group and bank net interest margin expanded by +7 basis points QoQ and +6 basis points QoQ to 1.60% and 1.35%, respectively in 1Q 2021. The company benefited from a +4% QoQ and +21% YoY increase in low cost deposits. Low cost deposits as a percentage of KRW-denominated deposits were 45.4% as of end-1Q 2021 for Woori Financial. This represented a significant improvement from Woori Financial's ratio of low cost deposits to KRW-denominated deposits of 41.4% as of end-1Q 2020.

Thirdly, the company's cost management has proven to be very effective in the most recent quarter. Woori Financial's cost-to-income ratio decreased from 55.0% in 4Q 2020 and 50.2% in 1Q 2020 to 46.2% in 1Q 2021.

Notably, Woori Financial's 1Q 2021 cost-to-income ratio was also much lower than most of its peers. The cost-to-income ratios of KB Financial Group Inc (NYSE:KB) [105560:KS] and Hana Financial Group [086790:KS] were relatively higher at 50.4% and 46.5%, respectively in the first quarter of 2021. Among the four major Korean financial institutions, Shinhan Financial Group Co., Ltd (NYSE:SHG) [055550:KS] stood out with the lowest cost-to-income ratio by a mile at 40.6% in 1Q 2021.

Lastly, Woori Financial's credit cost ratio contracted by -10 percentage points from 0.28% in 4Q 2020 to 0.18% in 1Q 2021. As a comparison, the 1Q 2021 credit cost ratios for Shinhan Financial, KB Financial, and Hana Financial were 0.22%, 0.20%, and 0.12%, respectively. In other words, Woori Financial's credit cost ratio was the second lowest among peers in the first quarter of this year.

Low CET1 Ratio And Disappointing Dividend Payout Ratio Draw Attention

Woori Financial's 1Q 2021 results were good, but its CET1 ratio and dividend payout ratio were the lowest among its peers.

Woori Financial's CET1 ratio was 10.0% as of end-1Q 2021. In contrast, the CET1 ratios for Hana Financial, KB Financial and Shinhan Financial were much higher at 14.1%, 13.8%, 13.0%, respectively as of March 31, 2021. Woori Financial's lack of capital buffer (on a relative basis) has also affected the company's dividend payout.

The Korean financial services companies typically pay out dividends once a year. Woori Financial's full-year dividend payout was cut from 27.0% in FY 2019 to 19.9% in FY 2020. While it is understandable that Korean banks reduced their dividend payout ratios last year given challenging market conditions as a result of COVID-19 and regulatory pressures, it is noteworthy that Woori Financial's dividend payout ratio was also the lowest among its peers. The FY 2020 dividend payout ratios of Shinhan Financial, Hana Financial and KB Financial were 23.5%, 20.5% and 20.0%, respectively.

On the positive side of things, Woori Financial has already applied to the Korean financial regulatory authorities for approval to allow the company to use the internal ratings-based or IRB approach (as opposed to the standardized approach which translates into lower capital adequacy ratios) for its subsidiaries in calculating its capital adequacy ratios. The other major Korean banks don't have such issues, as Woori Financial only recently reorganized itself as a financial holding company in 2019, which warranted increased regulatory scrutiny.

The company has guided in its 1Q 2021 results presentation slides that it expects "capital improvement" and wishes to "actively pursue to enhance shareholder return post COVID" after such approval is obtained. Sell-side analysts from Shinhan Investment are forecasting a +100 basis points improvement in Woori Financial's CET1 ratio once the Korean financial regulatory authorities grant approval to use the IRB approach for subsidiaries. This will likely narrow the gap in CET1-ratio between Woori Financial and its peers, but Woori Financial is still very likely to have the lowest CET-1 ratio (assuming adjusted CET1 ratio of 11.0%) of the four major Korean financial institutions.

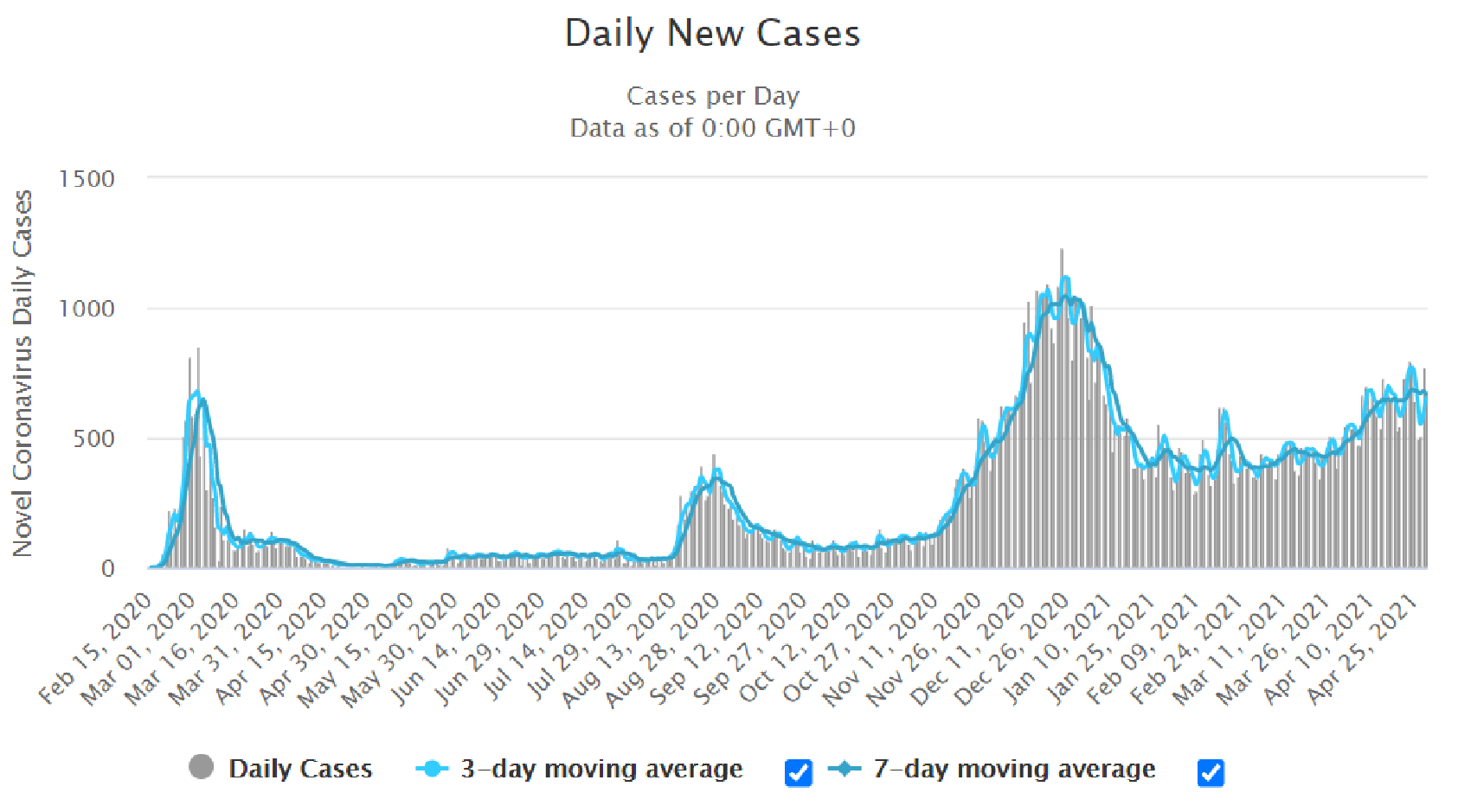

Also, market consensus expects Woori Financial's dividend payout ratio to increase to 25.4% in FY 2021, but this will be dependent on the company's continued earnings growth momentum (as per 1Q 2021 results) and the approval from Korean financial regulatory authorities on the usage of the internal ratings-based or IRB approach. A resurgence of COVID-19 in Korea in the past 1-2 months could pose downside risks to Woori Financial's future earnings for the rest of 2021.

Daily Confirmed Cases Of COVID-19 In South Korea

Source: Worldometer

Source: Worldometer

Valuation And Risk Factors

Woori Financial is valued by the market at consensus forward FY 2021 and FY 2022 P/E multiples of 4.3 times and 4.1 times, respectively, according to its last traded price of KRW10,750 as of April 29, 2021. It also trades at 0.39 times trailing P/B. The stock boasts consensus forward dividend yields of 5.9% and 6.4% for the current fiscal year and the next fiscal year, respectively.

Woori Financial is the cheapest among the four major Korean banks as per the peer valuation comparison table below. The stock has the lowest forward P/E and trailing P/B multiples, and it offers the highest forward dividend yields. Woori Financial's under-valuation relative to peers is justified to a certain extent, given that it has the lowest CET1 ratio and dividend payout ratio among the four major Korean financial services companies as highlighted above.

Peer Valuation Comparison For Woori Financial

| Stock | Consensus Current Year P/E Ratio | Consensus Forward One-Year P/E Ratio | Trailing P/B Ratio | Consensus Current Year Dividend Yield | Consensus Forward One-Year Dividend Yield |

| Hana Financial | 4.5 | 4.4 | 0.43 | 5.5% | 5.9% |

| Shinhan Financial | 5.2 | 5.0 | 0.47 | 5.1% | 5.4% |

| KB Financial | 5.3 | 5.1 | 0.49 | 5.0% | 5.4% |

Source: S&P Capital IQ

The key risk factors for Woori Financial include weaker-than-expected loan growth, lower-than-expected net interest margin, higher-than-expected cost-to-income & credit cost ratios, and a lower-than-expected dividend payout ratio going forward.

Asia Value & Moat Stocks is a research service for value investors seeking value stocks with a huge gap between price and intrinsic value, leaning towards deep value balance sheet bargains (i.e. buying assets at a discount e.g. net cash stocks, net-nets, low P/B stocks, sum-of-the-parts discounts) and wide moat stocks (i.e. buying earnings power at a discount in great companies like "Magic Formula" stocks, high-quality businesses, hidden champions and wide moat compounders). Sign up here to get started today!