Introduction

When the Covid-19 pandemic struck the global economy in early 2020 CVR Energy (NYSE:CVI) found themselves completely suspending their dividends by the middle of the year. Now with the middle of 2021 fast approaching, thankfully their shareholders have been pleasantly surprised with them announcing a massive special dividend. Whilst the prospects to receive such a large one-off dividend is certainly exciting, even better a 10% yield may follow in the future.

Executive Summary & Ratings

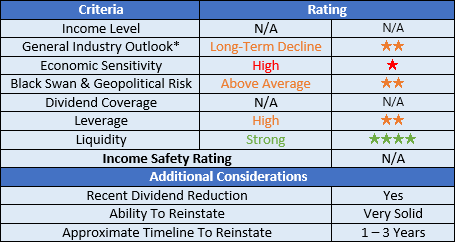

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Image Source: Author.

*There are significant short and medium-term uncertainties for the broader oil and gas industry, however, in the long-term they will certainly face a decline as the world moves away from fossil fuels.

Detailed Analysis

![]()

Image Source: Author.

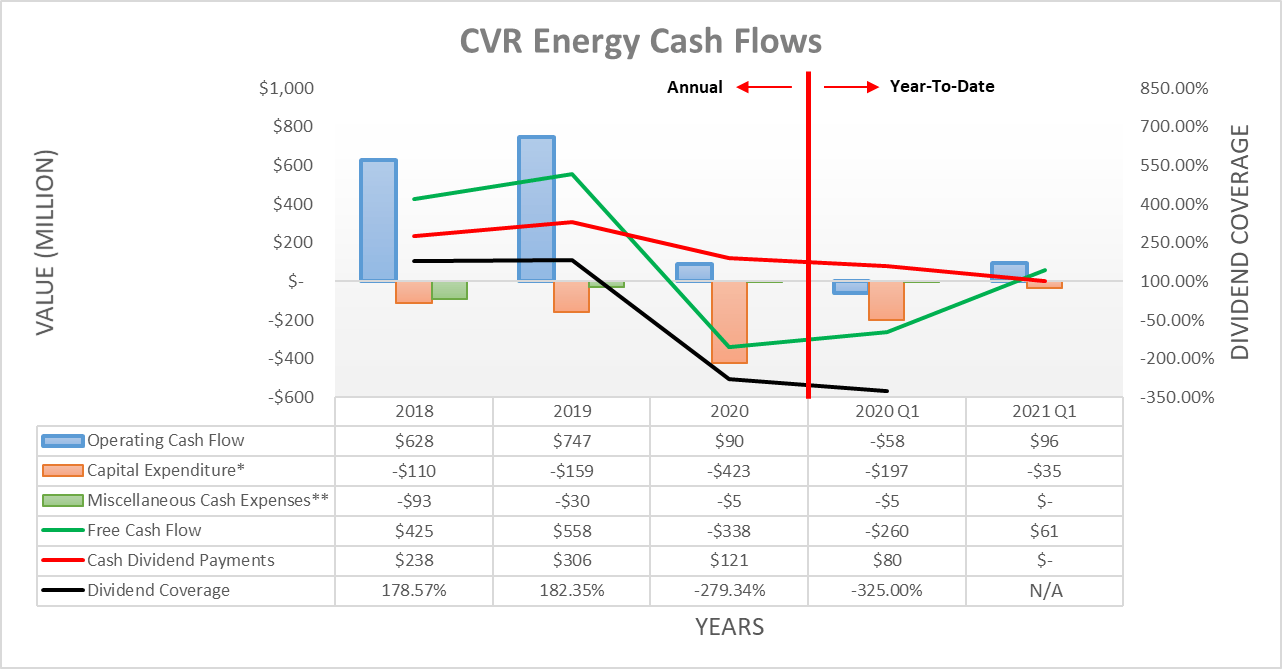

Instead of simply assessing dividend coverage through earnings per share, I prefer to utilize free cash flow since it provides the toughest criteria and best captures the true impact on their financial position. The extent that these two results differ will depend upon the company in question and often comes down to the spread between their depreciation and amortization to capital expenditure.

It was surprising to see such a large special dividend given their challenged cash flow performance during the previous twelve months, which during 2020 saw their operating cash flow nearly wiped out by a massive 87.95% plunge year on year to $90m versus $747m during 2019. Whilst their operating cash flow during the first quarter of 2021 has seen a material improvement versus the same time during 2020 with operating cash flow of $96m versus negative $58m respectively, on an annualized basis this would only be $384m and thus far short of their 2019 performance of $747m.

The headline value of this special dividend is $492m, which is massive compared to their current market capitalization as of the time of writing that stands at only $2.11b and thus represents a one-off 23.32% payment. There is one slight caveat to consider, they are making this payment with a combination of cash and shares of Delek US Holdings (DK), which they claim to have amassed an impressive $116m unrealized capital gain against their initial investment, as per their related news announcement. The exact split between the cash and share portion will be determined based on the difference between the total $492m dividend and the value of the portion of shares on the distribution date of 10th June 2021. They are currently holding a total of 10,539,880 shares as of May 10th 2021, which at the time had a share price of $21.87 and thus as things stand right now the share portion of this special dividend would equal a total of $231m or 46.95% with the remaining $261m paid through cash.

When looking ahead this special dividend stands to be followed by consistent dividends once operating conditions improve, as this clearly demonstrates that management remains committed to returning cash to their shareholders. Whilst no one knows exactly what the future holds, the continued distribution of Covid-19 vaccines should help keep the trend of new cases in the United State pointing down and thus progressively allow life to normalize, along with their operating conditions and by extension, their earnings.

Until their financial performance was ravished by the Covid-19 inspired economic downturn they paid a quarterly dividend of $0.80 per share, which if reinstated would provide a massive yield on current cost of over 15%. Thankfully their prospects to reinstate these former dividends appear very solid, as they were easily covered by free cash flow before the downturn with 2019 sporting very strong coverage of 182.35%. This means that shareholders could be set to begin receiving a consistent and very high dividend within one to three years once operating conditions have likely further improved.

Even if they were to take a more conservative approach than previously or possibly do not see their cash flow performance fully recover to its level during 2019, this still nevertheless highlights how they could realistically provide a dividend yield on current cost upwards of 10%. Given their continued challenged cash flow performance since the start of 2020, it will be important to assess their financial position to not only ascertain the impact of this special dividend but also their ability to reinstate consistent dividends in the future.

Image Source: Author.

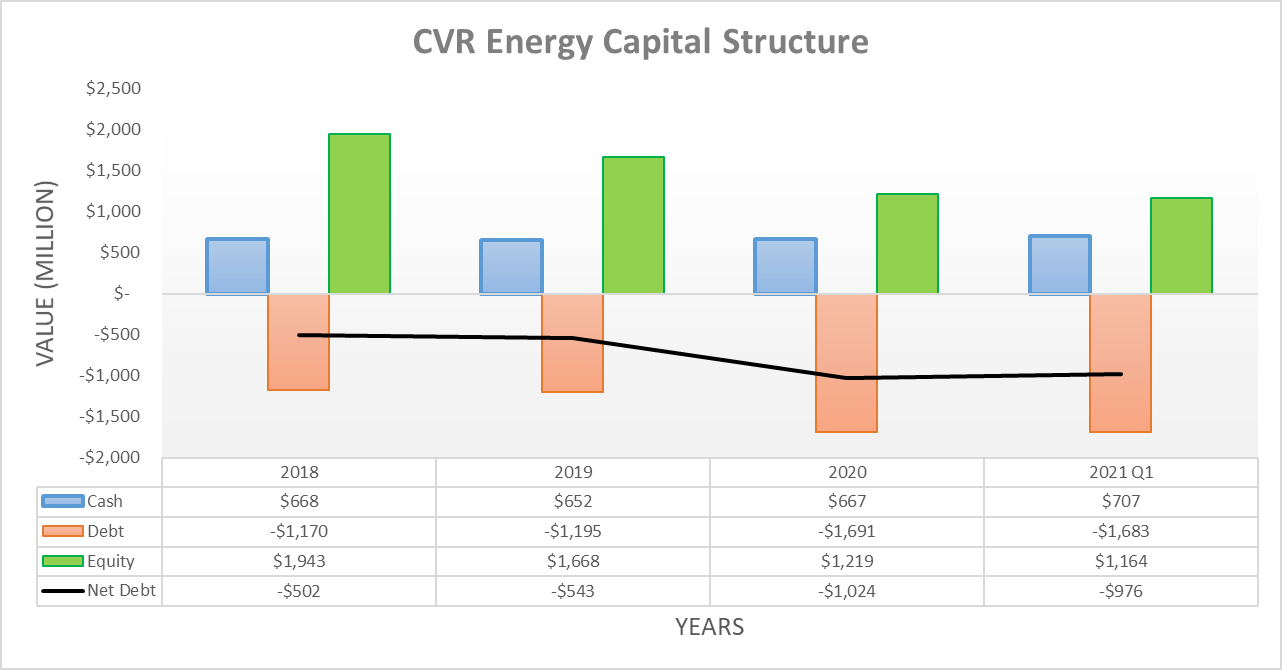

When reviewing their capital structure, it can be seen that their net debt increased by a significant 88.58% during 2020 to $1.024b versus only $543m at the end of 2019. Whilst it has edged lower during the first quarter of 2021 to $976m, it still remains elevated and holding everything else constant, it will increase to a record $1.237b after paying the previously estimated cash portion of their special dividend. Whilst this right now may not sound ideal, in reality this will ultimately be determined by their broader leverage and liquidity but thankfully, they currently have a very large $707m cash balance and thus they will not need to access debt markets.

Image Source: Author.

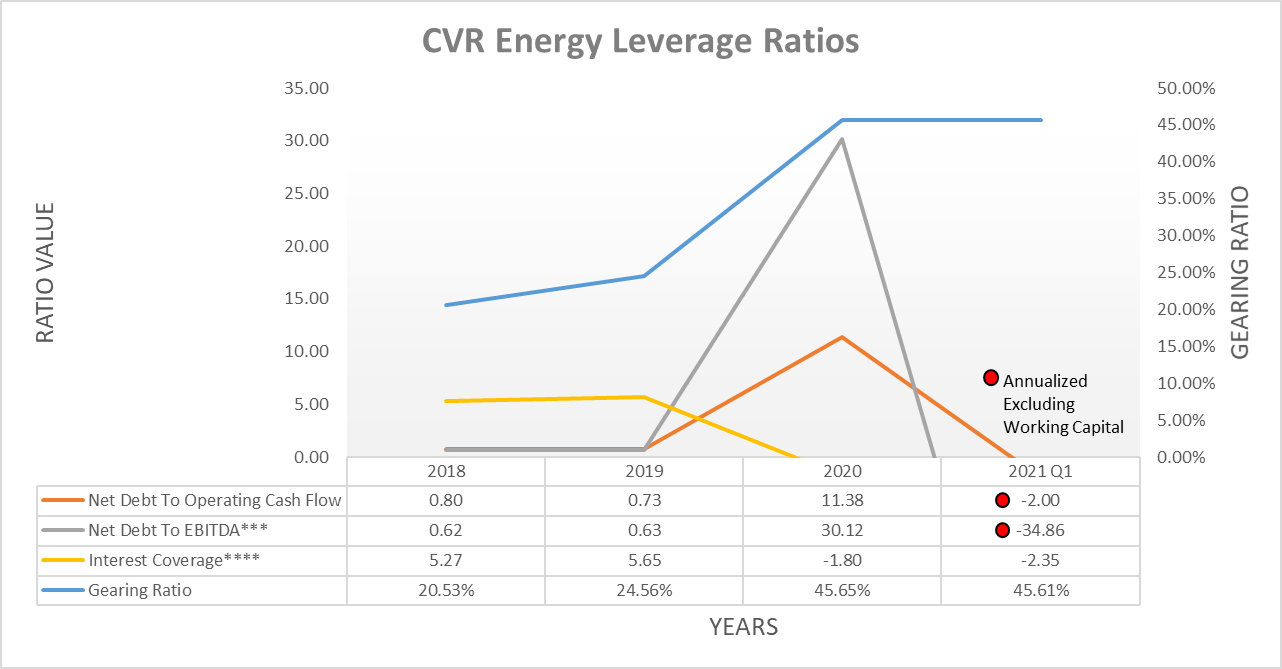

It can be rather tricky ascertaining judgments regarding their leverage when reviewing these financial metrics because of the downturn-related volatility within their earnings. This is evident with their net debt-to-EBITDA swinging around between 30.12 and negative 34.86 between the end of 2020 and the first quarter of 2021, which is similarly mirrored by their net debt-to-operating cash flow. Until such time as this downturn is fully in the past and thus their earnings have stabilized, it seems reasonable to judge their leverage by their gearing ratio of 45.61%, which sits within the high territory of 30.01% and 50.00%.

Whilst their high leverage is not necessarily ideal in isolation, as this results from a downturn it should improve quickly once their earnings recover. If their earnings were to rebound back to their levels from 2019 when their EBITDA as per my calculations was $863m, their net debt-to-EBITDA would only be a low 1.43 even after seeing their net debt jump to the record $1.237b following their special dividend. This means that their financial position can easily handle paying their special dividend and reinstating consistent dividends in the future, providing that their liquidity is at least adequate.

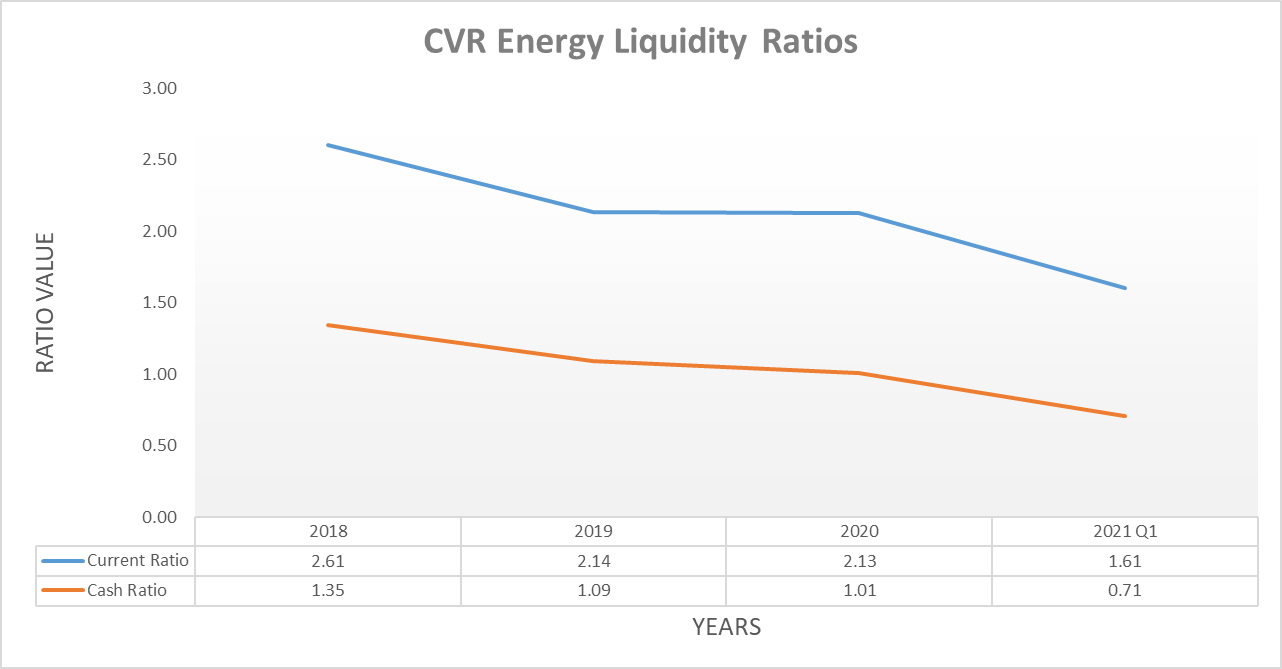

Image Source: Author.

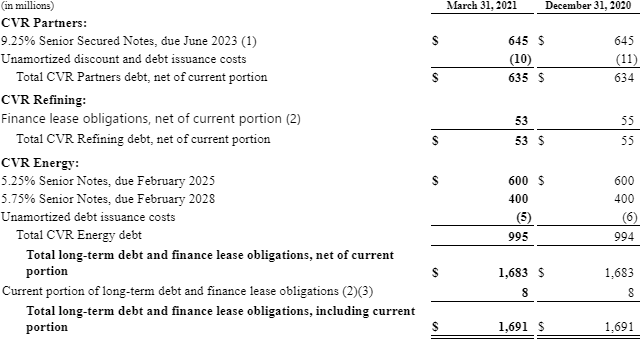

Thankfully their previously mentioned relatively very large cash balance has easily provided them with strong liquidity with current and cash ratios of 1.61 and 0.71 respectively. Even after making the estimated $261m cash portion of their special divided, their current and cash ratios would still be strong at 1.34 and 0.45 respectively. This naturally provides ample liquidity, especially since they have a further $389m available through their two credit facilities. Whilst they have a range of debt maturities thankfully the nearest one is not until June 2023 and thus provides them ample time to arrange repayment and refinancing if necessary, as the table included below displays.

Image Source: CVR Energy Q1 2021 10-Q.

Conclusion

Quite possibly even more exciting than this one-off special dividend is that management remains committed to return cash to shareholders and thus this bodes very well for their future income prospects. Since they could realistically afford to provide a 10% dividend yield on current cost once operating conditions finish recovering and stabilize, I believe that a bullish rating to be appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from CVR Energy's Q1 2021 10-Q (previously linked), 2020 10-K, and 2018 10-K SEC Filings, all calculated figures were performed by the author.