Article Thesis

Alibaba (NYSE:BABA) is a leading tech mega-cap that combines a range of positives, such as offering exposure to the high-growth Chinese consumer industry, digitalization tailwinds, and a dominant market position. Shares are inexpensive, and based on management's guidance, the current year should be a highly successful one for the company. Capital allocation seems somewhat objectionable in some cases, and there are risks that investors should consider, but from a risk-reward perspective Alibaba looks attractive - in absolute terms, and relative to other tech mega-caps.

Alibaba's Most Recent Quarterly Results Showcase Growth Exposure And Market Dominance

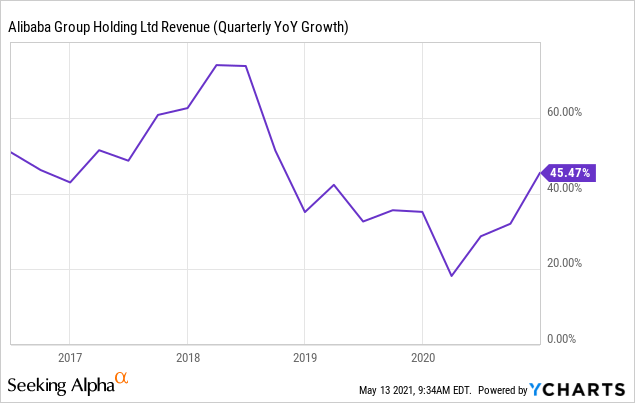

Alibaba's fiscal year ends on March 31, thus the most recent quarterly update was for its fiscal fourth quarter. During the period, Alibaba grew its revenues by a massive 64% year over year, although we have to adjust that number for one-time items, including the consolidation of Sun Art. Adjusted for that, and looking at revenues on a like-for-like basis, Alibaba still delivered attractive growth during the quarter, however, as revenues were up by 40% organically.

A 40% growth rate is more or less in line with the historical average, and ahead of the growth that the company delivered over the last year. Base effects, such as a relatively easy comparison to the pandemic-impacted quarter in the previous year, may explain what Alibaba was able to deliver strong growth that easily beat the analyst consensus estimate. Looking at how Amazon (AMZN), Alibaba's closest peer in the US, fared over the last year, we see a quite similar performance, as Amazon grew its revenues by 44% during the most recent quarter.

Alibaba's revenue growth rests on several pillars:

- User growth, as its platforms continue to grow the number of active accounts regularly.

- Consumer spending growth, as a fast-growing Chinese middle class allows more people to spend more money.

- Digitalization, as a growing portion of overall consumer spending is spent online.

The latter two factors are long-term megatrends that will, we believe, remain in place for years, and that are, generally speaking, advantageous for all e-commerce businesses that are active in China. The first factor, Alibaba's user growth, is a company-specific factor that has played a major role in Alibaba's success in the past, and that will likely be important in the future, too. The dominance of Alibaba's platforms, which results in a wide selection of products and vendors, explains why Alibaba's offerings are so attractive for consumers. Since this will likely not change in the foreseeable future, as Alibaba's dominance seems to be well-cemented in China, it can be expected that additional users will flock to Alibaba's platforms in the future. User growth will thus, we believe, continue to remain a tailwind as well, although the base effect of an already large user count will likely result in a lower relative growth rate in coming years, compared to the user growth that Alibaba has delivered in the past. Still, Alibaba has added 23 million new MAUs during the most recent quarter alone, for an annualized growth rate of more than 10%, thus this is not at all a negligible growth driver. When we look at the company's performance during fiscal 2021, which ended on March 31, we see that the Q4 growth record wasn't an outlier. During the year, revenues grew by 41% versus fiscal 2020.

Profit Growth - Healthy, But No Operating Leverage

When we shift our focus from Alibaba's top line to its bottom line, we see that profitability grew at an attractive pace in both the last quarter and the last year. Adjusted EBITDA totaled $30 billion for the year, up 17% versus 2020. High-teens EBITDA growth is highly compelling in a vacuum, but it should be noted that EBITDA clearly underperformed revenue growth during this period. This is somewhat underwhelming, as ideally, we would like to see EBITDA and profits grow at a faster pace than the company's top line. That is what has happened at Amazon and many other major tech companies, as they are usually able to benefit from operating leverage. Proportional expenses to support one additional customer are low, which means that each dollar in additional gross profit that companies like Amazon create can contribute to their bottom line over proportionally. This is why Amazon was able to more than double its operating income during Q1 on a year-over-year basis on the back of a 44% revenue growth rate.

In Alibaba's case, profits have not grown as fast as revenues, although this can, to some extent, be explained by growth investments. Alibaba does, for example, invest heavily in its cloud business, which hasn't been profitable during the last year yet. This could make sense strategically, as with growing size, the cloud business could eventually become a major profit center - the same has happened with Amazon's AWS. On top of that, Alibaba also keeps investing in the rollout of its offerings in international markets. If everything goes according to plan there, profits could see meaningful long-term tailwinds eventually, which is why the current below-average profit growth rate is not necessarily a cause for concern. Still, it seems noteworthy that Alibaba has, unlike many other tech companies, not seen tailwinds from operating leverage in the recent past. Alibaba sees its revenues grow by 30%+ this year, to at least 930 billion RMB, which underlines my belief that the growth story has not at all come to an end yet. Based on that, analyst estimates for this year and beyond may be too conservative, as single-digit earnings per share growth is forecasted for the current year.

Alibaba's Stock Is Priced For Disaster

Alibaba's shares went from a high of $320 that was hit in 2020 to as low as $210 at the time of writing, for a drop of more than 30% from the stock's all-time high. Alibaba is not the only growth stock or tech stock that has experienced a decline in recent months, of course, but Alibaba still seems like a noteworthy outlier due to the fact that its valuation was never especially high, and has gotten outright inexpensive by now.

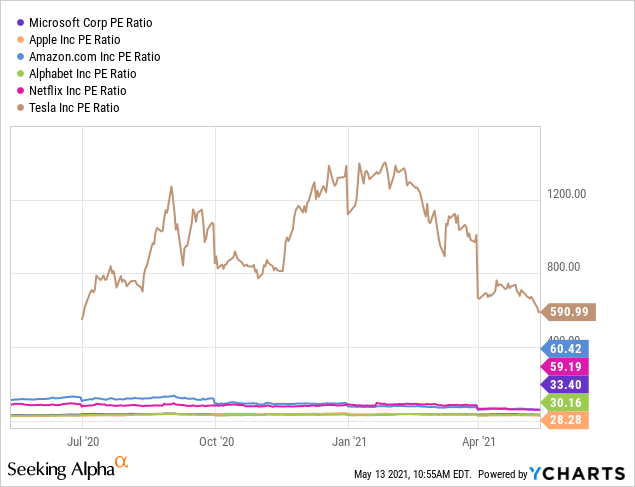

Based on adjusted earnings per share of $9.94 that Alibaba generated in its last fiscal year, shares are valued at 21 times trailing earnings. This compares very favorably to both the broad market and to other large-cap tech companies, which oftentimes trade at 30+ times trailing earnings, as can be seen in the following chart:

Apple (AAPL), Amazon, Alphabet (GOOG)(GOOGL), Microsoft (MSFT), Netflix (NFLX), and Tesla (TSLA) all trade at significantly higher valuations than Alibaba right now. One can argue that Alibaba's massive exposure to China and unforeseeable actions by Chinese regulators warrant a discount versus US-based tech companies, but I believe that the current discount is overblown.

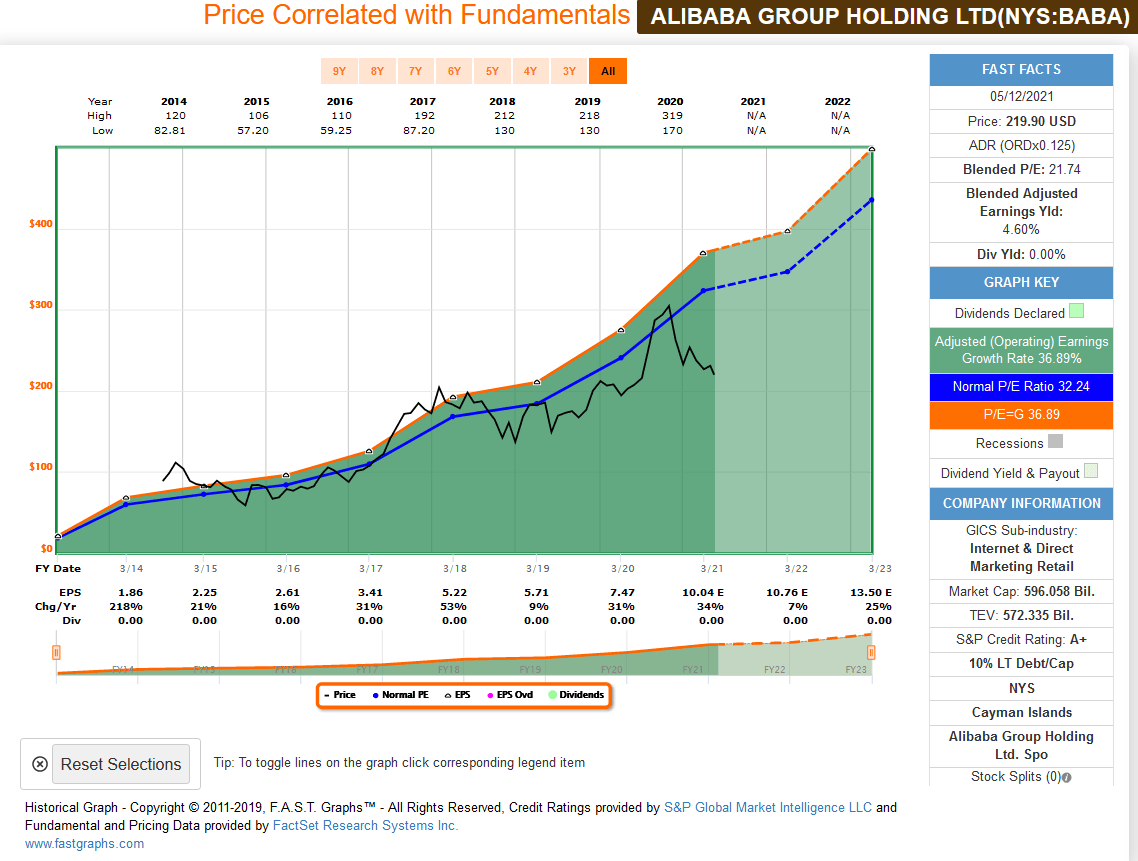

Source: fastgraphs.com

We see that Alibaba does clearly trade below its normal/average earnings multiple right now, following its move back towards $200. Looking at earnings estimates for Alibaba over the next couple of years, it doesn't seem unreasonable to assume that Alibaba will be a rewarding investment:

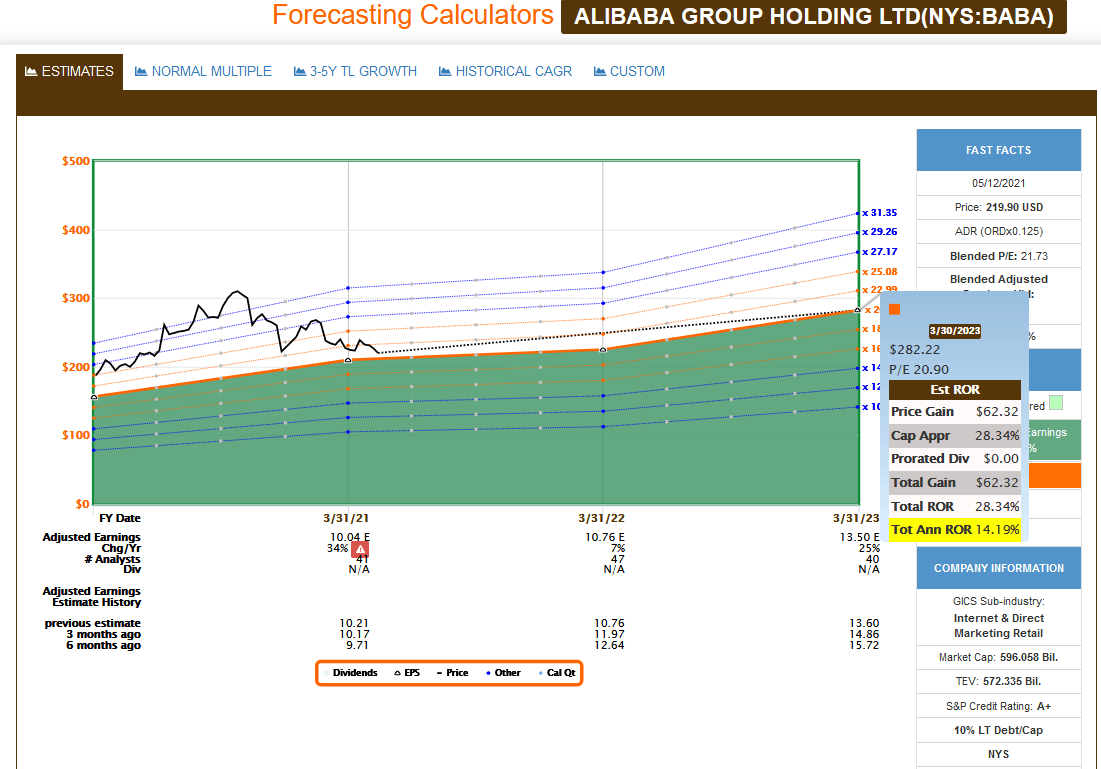

Source: fastgraphs.com

Even if Alibaba trades at just 21 times net earnings in 2023 - and due to the company's expected growth and its market dominance, a higher valuation may be warranted - shares could deliver a mid-teens return annually through the next 2.5 years. Have Alibaba's shares trade at 23 times earnings at the end of 2023, and annual returns will average ~20%. All in all, the combination of growth and a rather low valuation makes Alibaba look like an attractive pick at today's price, I believe, which is why I have just added to my investment in Alibaba.

Risks To Consider When Investing In BABA

With every investment, risks should be considered, of course. In Alibaba's case, those are mostly political/regulatory risks in China, and potential macroeconomic issues in the country. Right now, the Chinese economy is growing fast, and rising consumer spending is a major factor for that. Should that ever change, Alibaba would likely be impacted a lot, as its fate, for now, seems to be tied to ongoing strong consumption by the growing Chinese middle class.

Regulators have been pressuring Alibaba and Ant Financial on monopoly concerns. Recently, Alibaba was fined a little less than $3 billion, which has, for now, ended regulatory pressures. The fine alone isn't a major issue for Alibaba, as this equates to just a couple of weeks' worth of cash flows. Still, it is of course possible that there will be more investigations and more fines in the future, although I don't see this as overly likely. I believe that Chinese regulators won't be interested in hurting one of the country's largest and most successful companies, but future potential lawsuits are still a looming risk factor that investors should keep an eye on.

Is Alibaba Stock A Buy Or Sell?

Alibaba isn't risk-free, but the current valuation more than accounts for potential risks, I believe. Alibaba is delivering attractive growth, keeps investing in high-growth ventures such as cloud computing, is highly profitable, and at a massive discount versus US-based peers and the broad market, the stock looks attractive to me.

With shares recently dropping to just above $200, I decided to increase my investment in Alibaba, and I believe that buying in the low $200s could be a highly rewarding choice for those that are willing to hold onto shares for a couple of years at least.

I personally would like to see Alibaba's management scale back on some of their non-profitable business ventures and return cash to its owners via buybacks, which would also help stabilize the share price, but even without that, the stock looks like a solid pick to me.

Is This an Income Stream Which Induces Fear?

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% - 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio's price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!

The primary goal of the Cash Flow Kingdom Income Portfolio is to produce an overall yield in the 7% - 10% range. We accomplish this by combining several different income streams to form an attractive, steady portfolio payout. The portfolio's price can fluctuate, but the income stream remains consistent. Start your free two-week trial today!