Q1/21 results

The below analysis of Tencent's (OTCPK:TCEHY) earnings is based on the following materials:

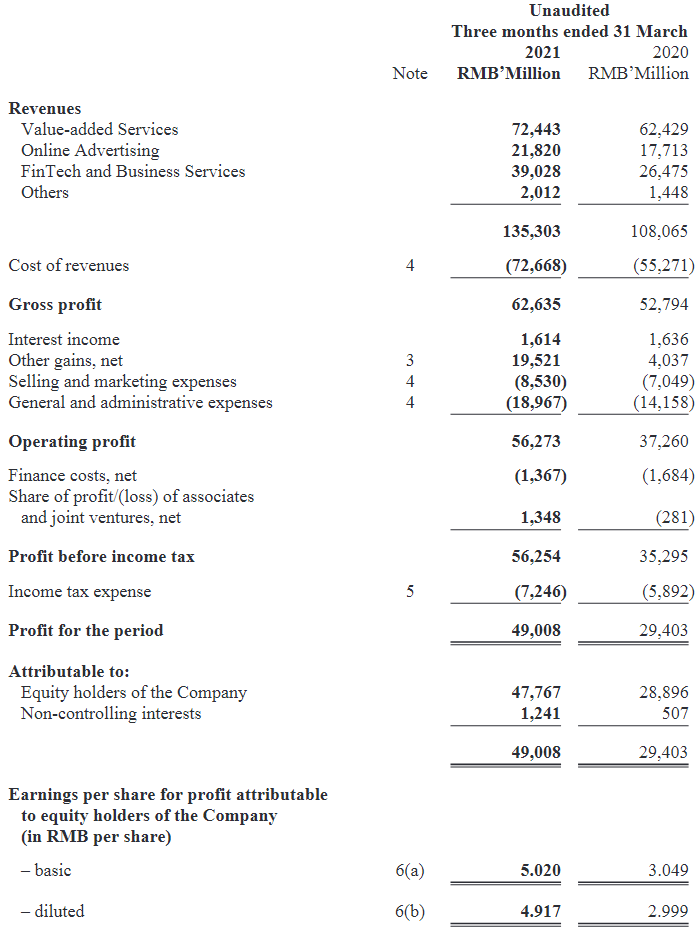

Consensus had expected somewhat lower revenues of RMB 134B and a bit higher non-IFRS profit, but as usual the really massive beat was in IFRS earnings (which include profits and fair value adjustments from investee companies): Tencent posted a staggering 66% increase YoY.

However, YoY growth was excellent even for non-IFRS earnings which increased 22%.

Profits from investee companies decreased from RMB 37B in the prior year quarter to a still massive RMB 22B in Q1/21. These profits are obviously highly volatile by nature. In this quarter, Chinese tech assets suffered from the regulatory pressure and a stock market sell-off in the tech sector, which makes the strong earnings contribution even more impressive. Over the past nine quarters, the average profit contribution was RMB 12.5B. And these quarters include the pandemic.

The fair value of Tencent's over 700 stakes in listed investee companies more than tripled YoY to RMB 1,362B ($207B - 28% of Tencent's market cap) and increased massively even compared to Q4, when it stood at $185B. And this was a bad quarter for tech in China.

Operationally, Q1 obviously faced tough comps, as Q1/20 was the lockdown quarter in China, so this year's consumers were out of lockdowns and back to their offices, with consequences on time spent online. Yet Tencent's business seems to have not suffered much from this development:

Non-IFRS net margin was stable, and IFRS margin increased from 27% to 36%.

VAS revenues were up 16% and game revenues were up 17% YoY. Even Social networks revenues grew 15%, despite the tough comp in Q1/20, as users massively bought online subscriptions. Online advertising revenues were up 23% and Fintech was up 47%, benefiting from an easy comp, as lockdowns reduced offline consumption in Q1/20.

Higher investments

Just like Alibaba (BABA), Tencent announced a year of partial incremental profit reinvestments, but provided greater detail on the scope of these investments:

"Business Services: We will make further investments in areas such as headcount and infrastructure to support the rapid growth of our business. We will strengthen our productivity SaaS products and security software as well as partnerships with and investments in SaaS providers and Independent Software Vendors, supporting our clients' digital needs. Through enhancing our upsell and cross-sell capabilities in key verticals such as healthcare, retail, education and transportation, we will provide smart solutions for enterprises and consumer-facing products for users.

Games: We are stepping up our investments in game development, and in particular focusing on large-scale and high-production-value games that can appeal to users globally. We are also investing further in new types of games serving more targeted audiences, building up IP franchises and developing them across media, and investing in advanced technologies for next generation game experiences such as cloud games.

Short-Form Video Content: We are now incubating the content ecosystem for Video Accounts which connect users with real-life content and bridge high-quality content creators with their customers. We will provide production and monetization tools to content creators, optimize social-driven recommendation, enrich knowledge-based content as well as add servers and bandwidth to support Video Accounts' solid growth. We are strengthening the synergies between our long-form and short-form video services. Through the merger of Tencent Video and WeiShi, we will empower long-form video leveraging our short-form capabilities. We will escalate self-commissioned production to further expand our IP content library, and provide video clips that can be adapted by our creator network."

This sounds very good, actually more like growth investments. And in fact the company expects very high returns on them, as noted on the call. The CCP clearly wants its giants to work for the overall social progress and not for the rapid maximization of profits, while squeezing consumers thanks to their monopoly power. Over time, this approach is likely to benefit these giants themselves, as nothing helps profits as much as boosting consumers' own productivity.

On the call, Tencent explained that investments will mainly concern business services (i.e. improve competitivity for Chinese enterprises). This is in stark contrast to the predominant representation of these investments in the press, which always seems to infer competitive pressures, especially from TikTok, as a key reason for greater investment needs. This doesn't seem to be the case, actually, as video has the lowest priority of investment:

"In terms of the areas of investment, you know, I would say, you know, mostly as James talked about, it's on the operating side. So, a big part of it is actually sort of people right, you know? So, these are engineers that we're going to hire additionally to create the products, perfect the products, and develop better services. And some of these new employees are higher-paid because, you know, they are essentially experts and professionals in their respective areas. And, you know, to a lesser extent, it will be bandwidth and infrastructure costs, and to some extent, maybe delayed monetization on the videos app, for example, right, you know? And so, these are sort, you know, the investments that we're talking about, which are actually are having a bottom-line impact.

And in terms of the magnitude, I would say business services, games, and video in that pecking order. And the nature is slightly different. Business services would actually take a longer time and it's a, you know, larger strategy of building scale first. And then over time, monetizing games, basically, you know, can monetize relatively quickly once you can launch the game and achieve success.

But the investment was actually in the development phase in which there is no revenue, but then you have incurred cost. Versus video as I said, right, you know? There's a continuous increase in terms of number of people in order for us to improve the product, improve the operations, improve the tools. And at the same time, in some cases, as some extent of delayed monetization on the advertising front."

The company also highlighted that there is no planned trajectory. Investment is part of business and if you look only at timely returns, you probably miss lots of opportunities. However, the largest hit will come right at the start:

"I have to disappoint you in saying there's no specific quantitative metrics. I think, you know, a lot of times in our industry, you actually sort of look at the trend, you look at the right things you do, and then you put in the resources. And over time, if you actually sort of, you know, are right and you - if you do it well, you know, the return is usually so much greater than what you can anticipate. But if you do all the calculations and say, "Oh, this is actually the rate of investment," and you invest according to that calculative mode, then usually, you won't be able to deliver over and beyond what the users want, and you will not be able to be a leader at the trend.

And usually, that means you're not going to even reap that return. So I think that's sort of, you know, essentially what it is. I think, you know, what we are saying is like this year, we are stepping up the investment. That's a strategic move.

And that increase in investment will actually continue. We will start to see some benefits over time. Now exactly what's the timing, I think, you know, it's hard to predict. But I think, you know, the - it's fair to say, at least at this point in time, right, the financial impact will probably be biggest as we start stepping into the investment."

Analysis of Q1 results

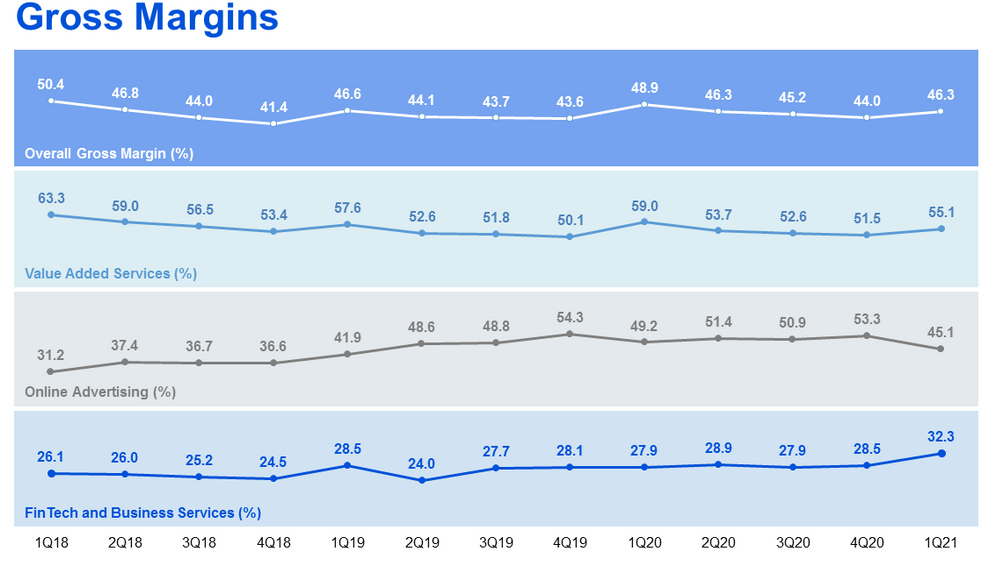

While VAS gross margins were down 3.9% YoY, this is actually an excellent result, as it compares to the Q1/20 record quarter, were much of China was subject to stay-at-home orders and heavily engaged in video gaming.

Gross margin for Online Advertising was 45.1%, down 4.1% YoY. The year-on-year decrease was mainly due to higher revenue contributions from mobile and network businesses, which carries lower margins.

Gross margin for fintech and business services was 32.3%, up 4.4% YoY. The improvement was mainly due to a favorable revenue mix shift towards merchant payment and wealth management services, which carry relatively higher profit margins.

Lumped together with gaming in the VAS segment are also video subscriptions and music subscriptions. The former grew 12% to 125 million subs, while the latter grew 43% YoY to 61 million subs. The overall number of paid subscriptions of 226 million (+14% YoY) also includes other subscription services, but compares well to Netflix's (NFLX) 204 million paid memberships as of Q1/21. (Netflix's market cap is about 30% of Tencent's.)

Overall, margins continue their slight multi-year downward trajectory. Whether this is due to competition or regulatory pressure, or due to heavy growth investments is hard to decide, given the tiny tilt of the curve. It should also be mentioned that, once we include investment gains and look at IFRS net profit margins, there is no margin pressure at all: 36% is record level. While investment gains are volatile, some estimate of average investment contributions to earnings should be included in our valuation, since Tencent's investments now account for 28% of its market cap.

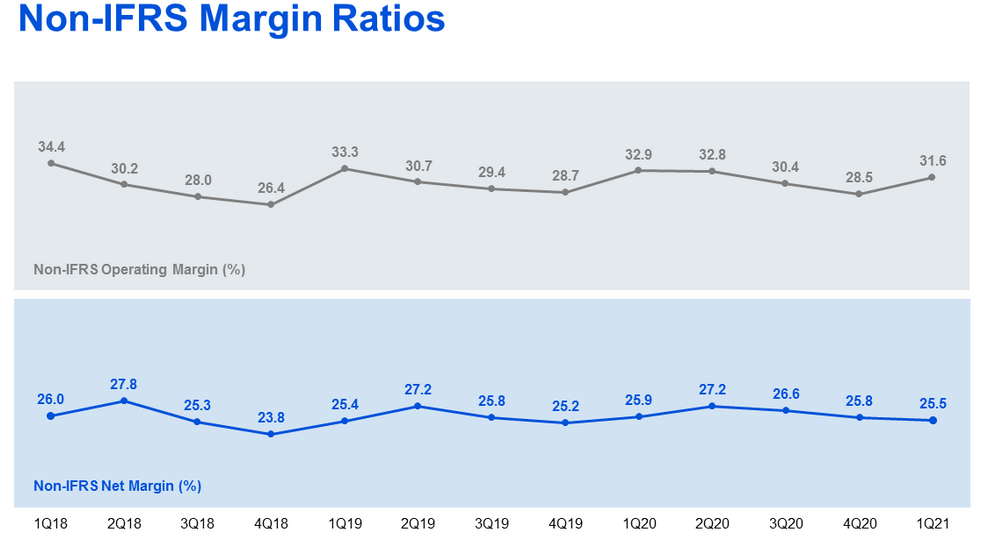

Finally, non-IFRS profits were also burdened by losses. Tencent noted on the call that its top five loss-making associates reduced non-IFRS net profit by 7% in the first quarter, i.e. the company could probably increase its earnings by 10% or more by simply cutting investments. And this actually means that some hits from the industry-wide investment increments are already in these Q1 results.

As far as gaming is concerned, the clear focus is on global expansion, and multiple large, new games have already been in the works for years and are close to launch:

"Lifelong game experiences requires many years of game development. But this is a trend that we've identified many years ago and we have a number of products that have indeed already been in development for many years and some of those are games that we're creating in China in our big internal studios like TiMi and Quantum and more fun in Aurora and some of those games that we're creating outside China or at studios, which we invest in and around the world. And you know, over the coming quarters and years, we hope to bring some of those big budget-long production cycle games to market. Now, as to why we're focused on this now and what changes now versus the past, we are indeed seeing that the global audience for games has grown both before, during, and after COVID.

And we're seeing particular growth in emerging markets such as the ones you highlight but also in developed markets, and we're also seeing that game players are increasingly willing to form long term relationships with games that they particularly enjoy such as the League of Legends or Fortnite or in Honour of Kings, which have very high retention rates and gamers, even if they churn, they come back to and enjoy again. You know, on our side, while historically our focus was primarily on the China market, as you know, in recent quarters we've had some hits globally that were developed in China including PUBG Mobile, including Call of Duty Mobile, all of which gives us more confidence to step up our rate of investment. And step up our rate of investment means fund bigger, better games, if necessary, for longer periods of time. It also means fund more experimental games.

It also means investing more in game marketing and game publishing capabilities. And then finally, it means investing in frontier technologies such as cloud-based gaming that will further grow the game industry in the future."

On the regulatory front management noted that everything is quite manageable, but did not provide precise guidance on how much of incremental profits will be invested. It only made clear that it will be more than in Q1:

"In terms of the incremental investment plan, I would not say the first quarter is the right benchmark. I think our investment plans actually stepping up from the first-quarter level. So if you look at the first-quarter results, I would say the benchmark is that our non-IFRS profit grew by 22% year on year. And what we're seeing is that we're going to be investing a portion of the incremental profit into new areas.

And so, that means it's somewhere between 0% and 22% from a quantitative basis. I think, you know, so, that's the quantification. Now, in terms of the regulatory news, well, I think, you know, the most significant way is, basically, after the first-quarter results, there was a meeting in which the financial regulator asked 15 fintech companies to have a meeting, and also announced certain principles as well as the fintech companies to have an internal review of their own business and practices. And I think, you know, the principle was largely public, right, you know, and they're largely focused on all businesses have to have to be conducted through licensed entities, and they asked for transparency.

And at the same time, I think, you know, there's quite a bit of focus on making sure that there's not going to be a systemic risk. And my understanding is it's quite focused on the size of the lending business and making sure that there's no overlending or overborrowing by consumers, right, you know. And toward that front, I would say as we have emphasized in our last conference call, we are very focused and compliant, we're very focused on risk management, we're very self-restraint in terms of the size of our non-payment financial products, especially on the lending side. So, when we look into, you know, the internal review and when we're looking to what are the things that need to be done in order to make sure that we are compliant with the spirit of the regulators, right, you know.

I think, you know, it's actually relatively manageable."

On China's digital currency tests, Tencent remains positive, as it simply considers digital currencies as a substitute of cash. It should therefore favor the adoption of digital payment, banking and fintech services, of which the company is a market-leading provider.

Valuation

While this quarter delivered solid results - and maybe even surprisingly solid ones, I still don't expect a massive boost to sell-side estimates, given the regulatory buzz. The YoY comps in Q2/21 will remain tough, as the 2020 pandemic benefited Tencent. In addition, in the short term there will certainly be margin pressure due to reinvestments of profits.

In my opinion, the right way to look at this year requires a long-term perspective: It is a year of investment, after which Tencent will be an even stronger company. IFRS profit growth might be slower for some quarters, but afterwards growth is likely to pick up again. So it doesn't make a lot of sense to apply a multiple to 2021 earnings estimates, without factoring in the likely subsequently improved growth trajectory. Yet this is what the market is currently not doing, as it fears a permanent margin impairment and cannot (yet) figure out the future growth trajectory. However, a permanent margin impairment is not what management is signaling, and Tencent management is not known for pumping and promotion, it has earned high credibility.

The company trades for about 26 times annualized Q1 earnings, which looks quite cheap, given its excellent market position, the strong balance sheet (net cash position since Q3/20) the long growth runway ahead and the many businesses where it is currently under-earning. Assuming somewhat slower average profit growth of ~20% for the next 5 years and a terminal multiple of 20x, Tencent should return ~15% annually including dividends.

While this seems to be very cheap, I guess that only if the current regulatory concerns dissolved themselves without much harm, a somewhat higher multiple might be in the cards. However, these concerns will likely dissipate only slowly over time, so the market will continue to apply an extra dose of caution for some quarters at least.