Never promote someone who hasn’t made some bad mistakes, because if you do, you are promoting someone who has never done anything. - Phillip Fisher (Warren Buffett's mentor)

It's a thing of beauty when you discover a bio-stock delivering a breakthrough therapy. Such growth equity usually appreciates multiple folds in a few years. After its most robust growth phase, the stock becomes a stalwart. Here, the share price appreciation would slow down for less than 50% upside.

That being said, I want to share with you another stalwart dubbed NovoCure (NASDAQ:NVCR). In the past year, NovoCure rallied by 209% as its market capitalization reached $20.9B. Due to a flurry of catalysts, I believe this stock has more room to run. In this research, I'll feature a fundamental analysis of NovoCure and provide my expectation on this intriguing grower.

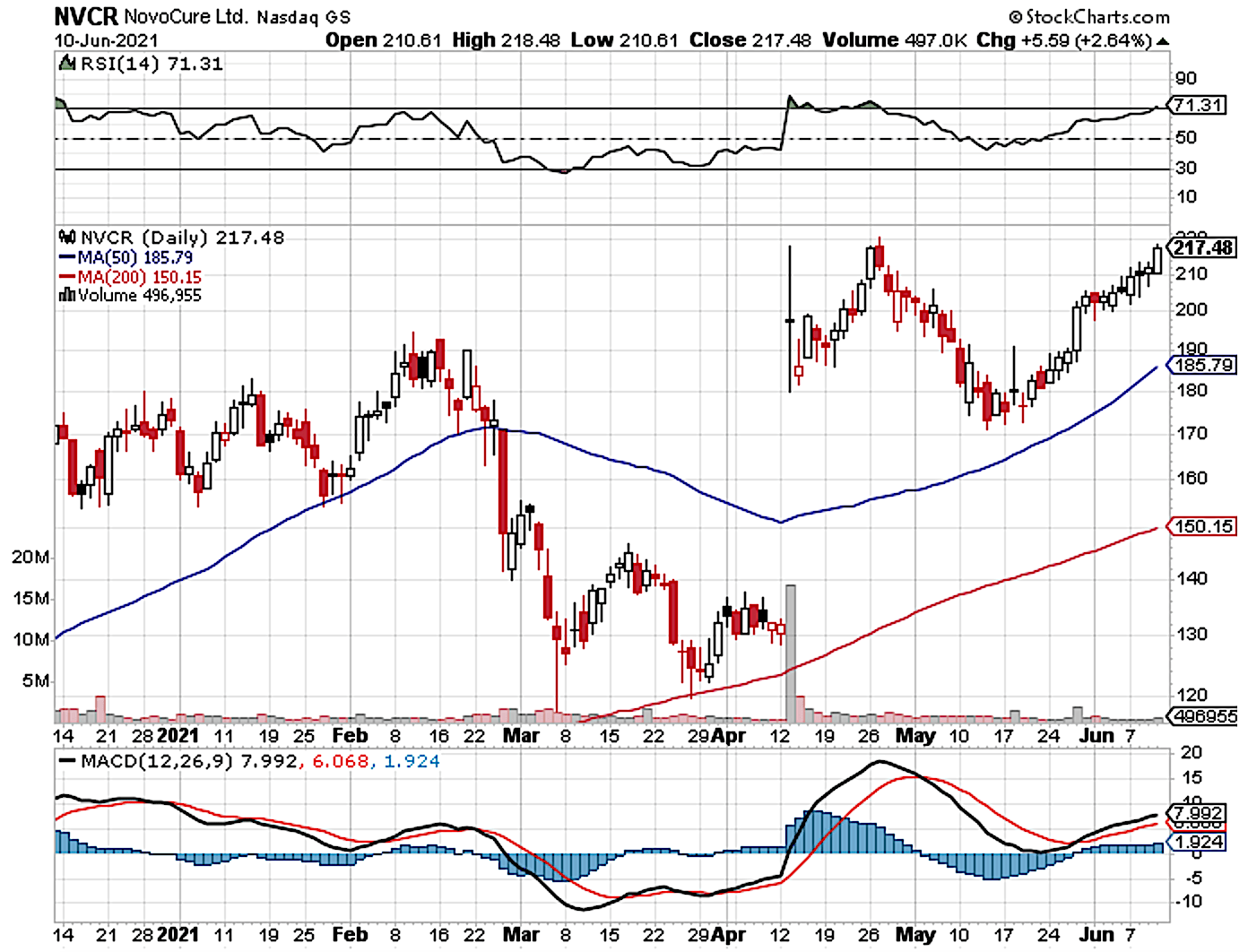

Figure 1: NovoCure chart (Source: StockCharts)

About The Company

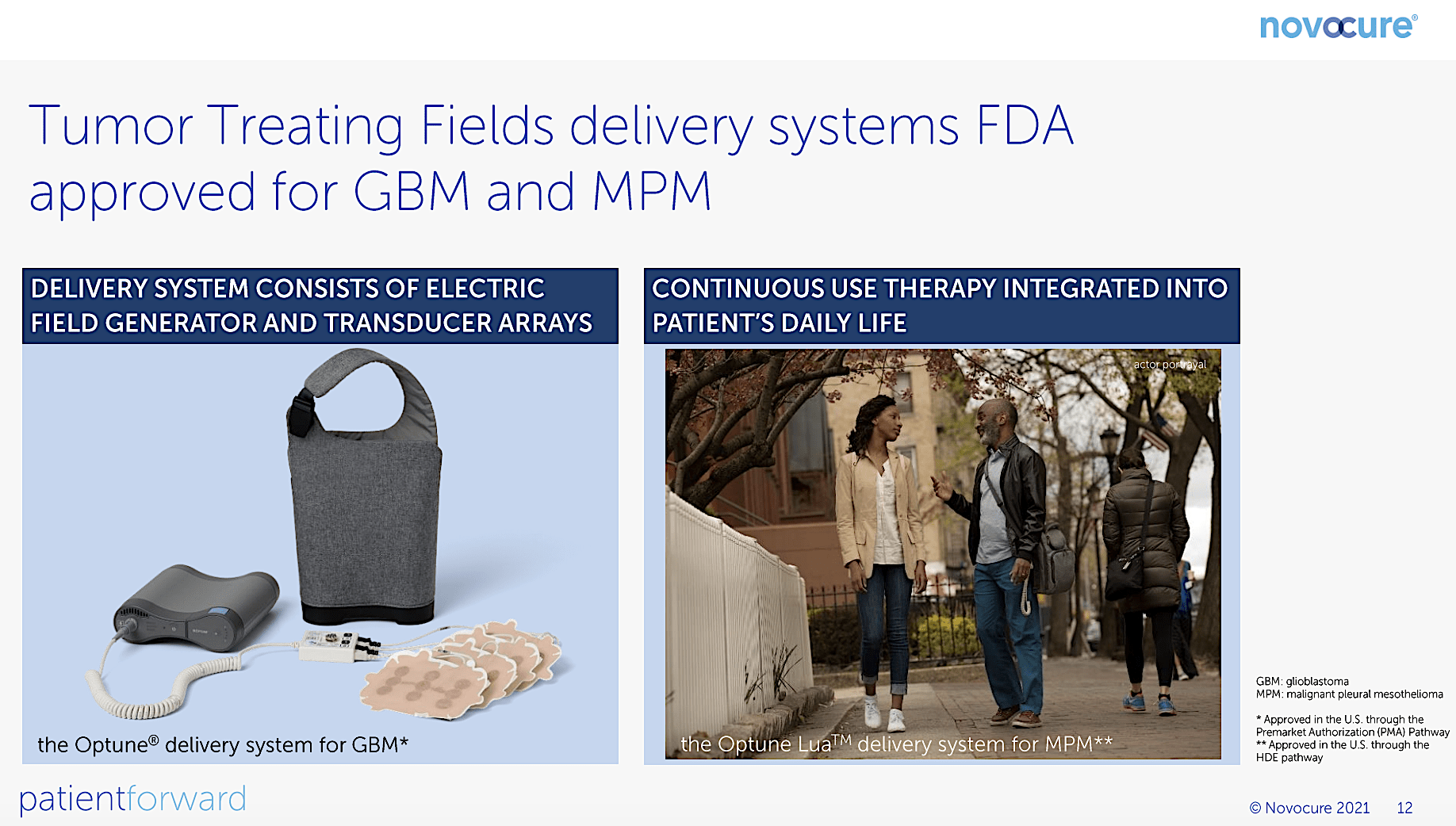

As usual, I'll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in St. Helier, Jersey, NovoCure is a global oncology leader in the novel cancer treatment known as Tumor Treating Fields (i.e., TTFields).

Figure 2: TTFields delivery system (Source: NovoCure)

The company is a risk-deleveraged investment because it has both approved and developing therapeutics. Looking at the pipeline, NovoCure already launched TTFields for both newly diagnosed and recurrent glioblastoma multiforme (i.e., GBM) as well as mesothelioma.

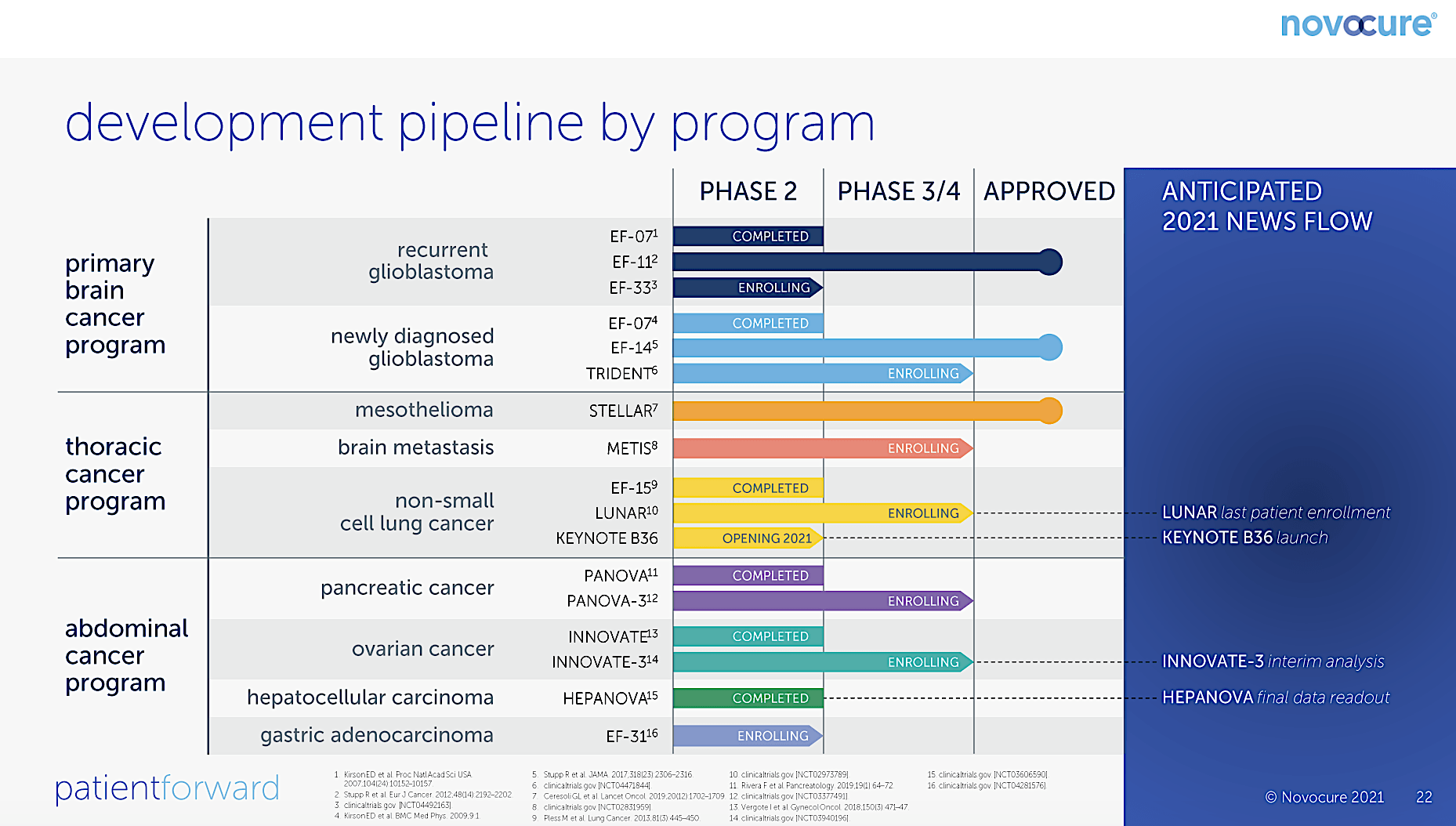

That aside, NovoCure is investigating TTFields' efficacy for a variety of cancer indications such as non-small cell lung cancer (NSCLC), brain metastases, pancreatic cancer, ovarian cancer, liver cancer, and gastric cancer. Furthermore, the company has other pre-clinical development for many cancer indications.

Figure 3: Therapeutic pipeline (Source: NovoCure)

Tumor Treating Fields

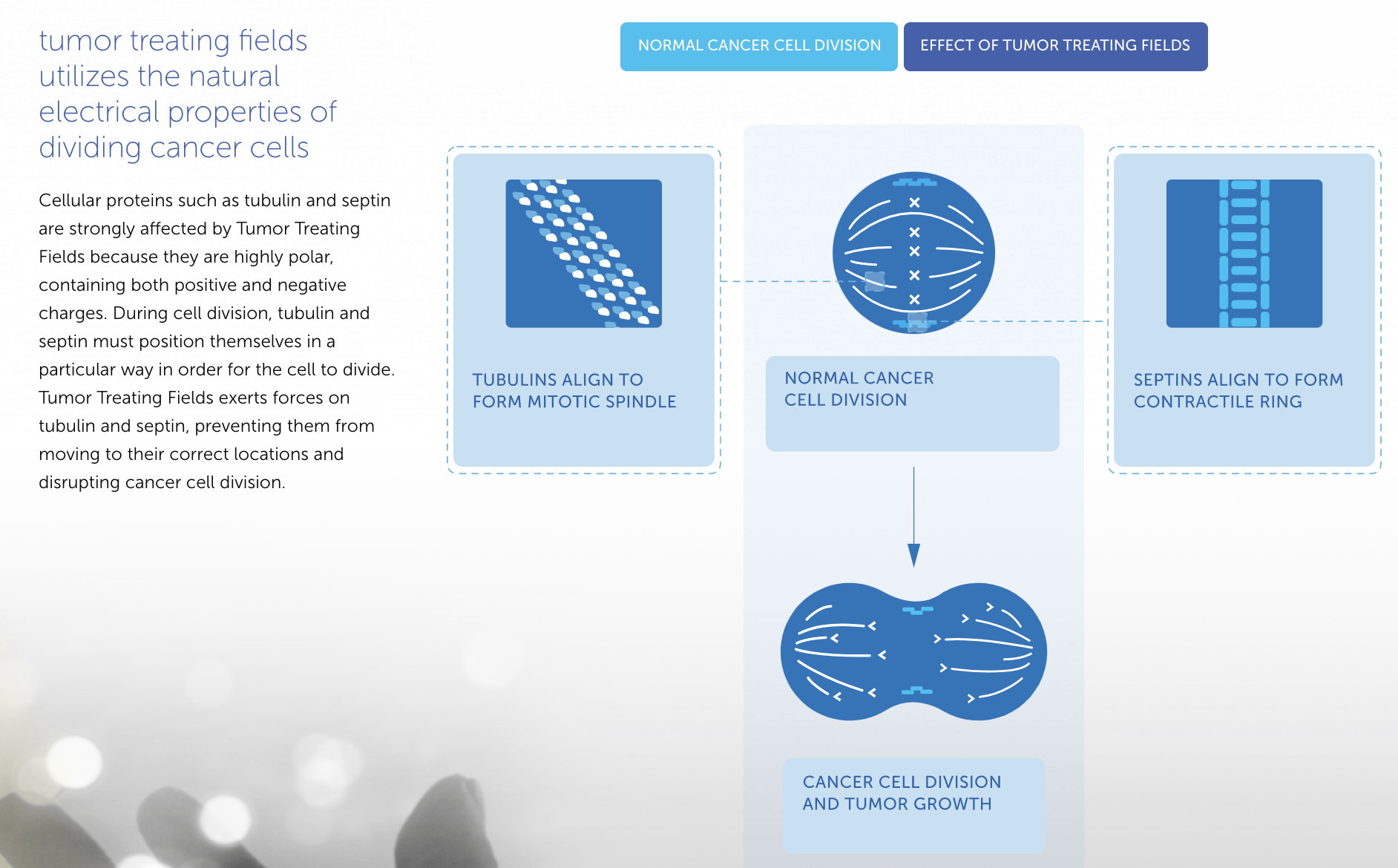

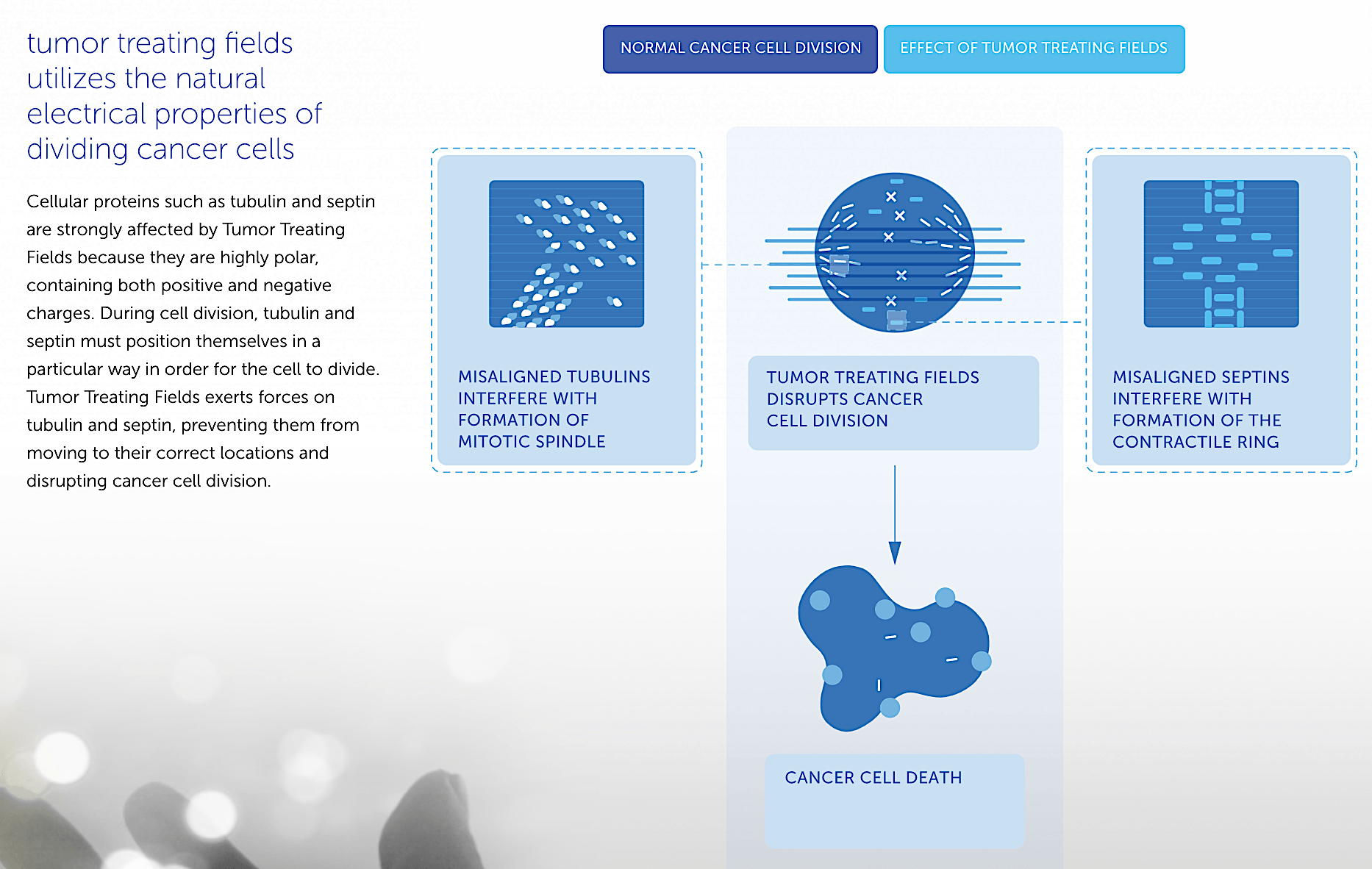

Shifting gears, let us assess the therapeutic prowess of TTFields. Now, the stellar efficacy of TTFields relates to its ingenious mechanism of action. But to appreciate its mechanism of action, you should first go over normal cellular division. After all, cancer cells need to divide for the tumor to expand.

In its life cycle, the cell undergoes various phases that ultimately lead to a division, i.e., splitting into more cells. When the cell divides, the genetic elements of the cells (i.e., chromosomes) have to line up in the middle. As the alignment is occurring, protein filaments (i.e., tubulins and septin) come into formation to properly form the mitotic spindle. As a result, these microscopic strings would literally pull the chromosome apart for division.

Figure 4: Cellular division (Source: NovoCure)

As you can see, TTFields leverages the electrical property of dividing cancer cells to stop their replications. They do this by displacing the tubulin and septin from their normal position. Consequently, that disrupts the ability of these rogue cells to divide.

In my view, this is an ingenious approach that galvanizes efficacy while limiting toxicity. More importantly, you can employ TTFields in combinations with other treatments like an immune checkpoint inhibitor to ramp up efficacy. With combination therapy being the cornerstone of prudent cancer management, you can expect great utility for TTFields.

Figure 5: Tumor treating field mechanism of action (Source: NovoCure)

Commercialization Progress

All the sound underlying science is meaningless unless the drug can generate strong market traction. Per the figure below, global net revenues for TTFields are increasing every single year. In other words, it increased from $248M for FY2018 to $494M for FY2020. At this pace, you can anticipate that TTFields would reach more than $540M for this year (i.e., more than halfway toward blockbuster).

Figure 6: Increasing sales traction (Source: NovoCure)

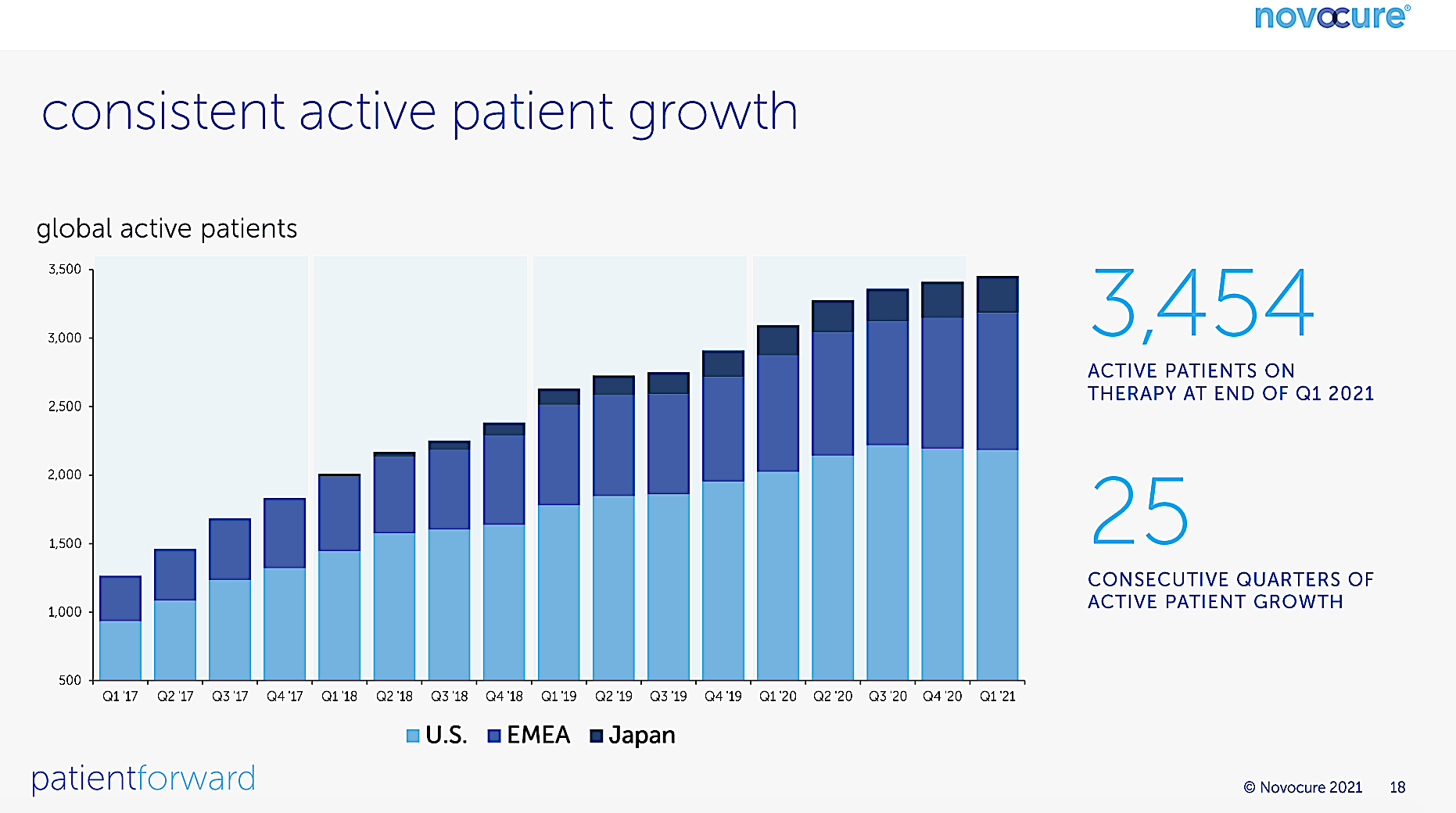

Alternatively, you can gauge future growth is by looking at the increasing number of patients being on TTFields therapy. From 1Q 2017 to 1Q 2021, there is continued growth in active patients for 25 consecutive quarters. As of Q1 this year, there are 3,454 active patients. Of note, the growth trajectory slightly cooled down last year due to commercialization constraints relating to COVID. Commenting on recent developments, the Executive Chairman (William Doyle) remarked:

Over the last several months, we have made progress across multiple clinical development programs intended to determine Tumor Treating Fields’ optimal use. We continued to increase our understanding of the potential benefits of Tumor Treating Fields when used together with immunotherapies and continued to enroll patients in five late-stage clinical trials in multiple solid tumor types. The accelerated interim analysis of the LUNAR trial and the upcoming HEPANOVA data presentation represents the beginning of what we expect to be an exciting few years of data readouts from our pipeline.

Figure 7: Active patient growth (Source: NovoCure)

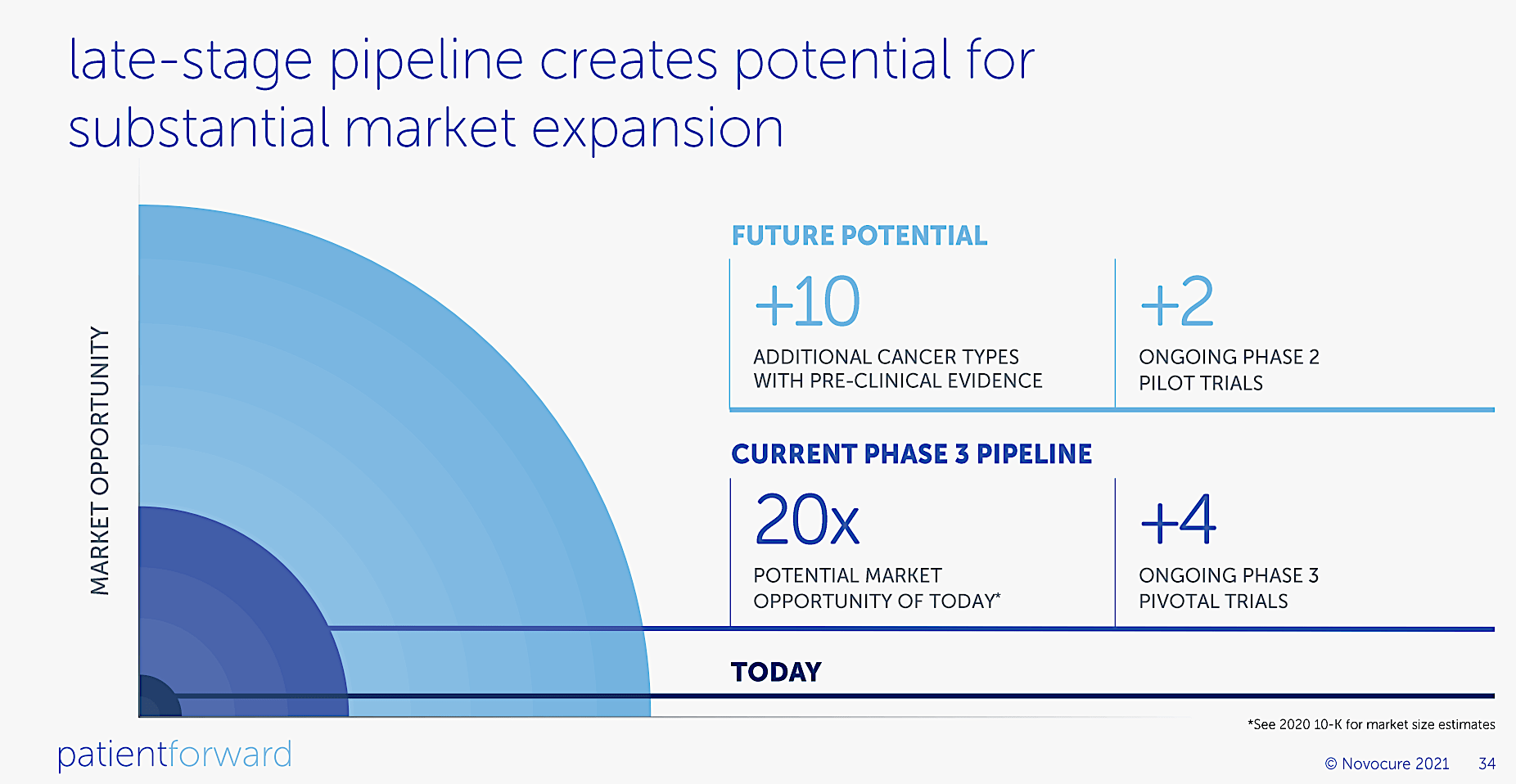

Now, there is a vast number of pre-clinical and clinical development for TTFields. For instance, the late-stage (i.e., Phase 3) development will mostly ramp up market share by over 20 folds. With the robust efficacy and excellent safety profile, I believe that the majority of these clinical investigations will bear fruits. Based on my integrated system of forecasting, I ascribed the overall 65% (i.e., more than favorable) chances of clinical for all clinical franchises.

Figure 8: Active patient growth (Source: NovoCure)

Financial Assessment

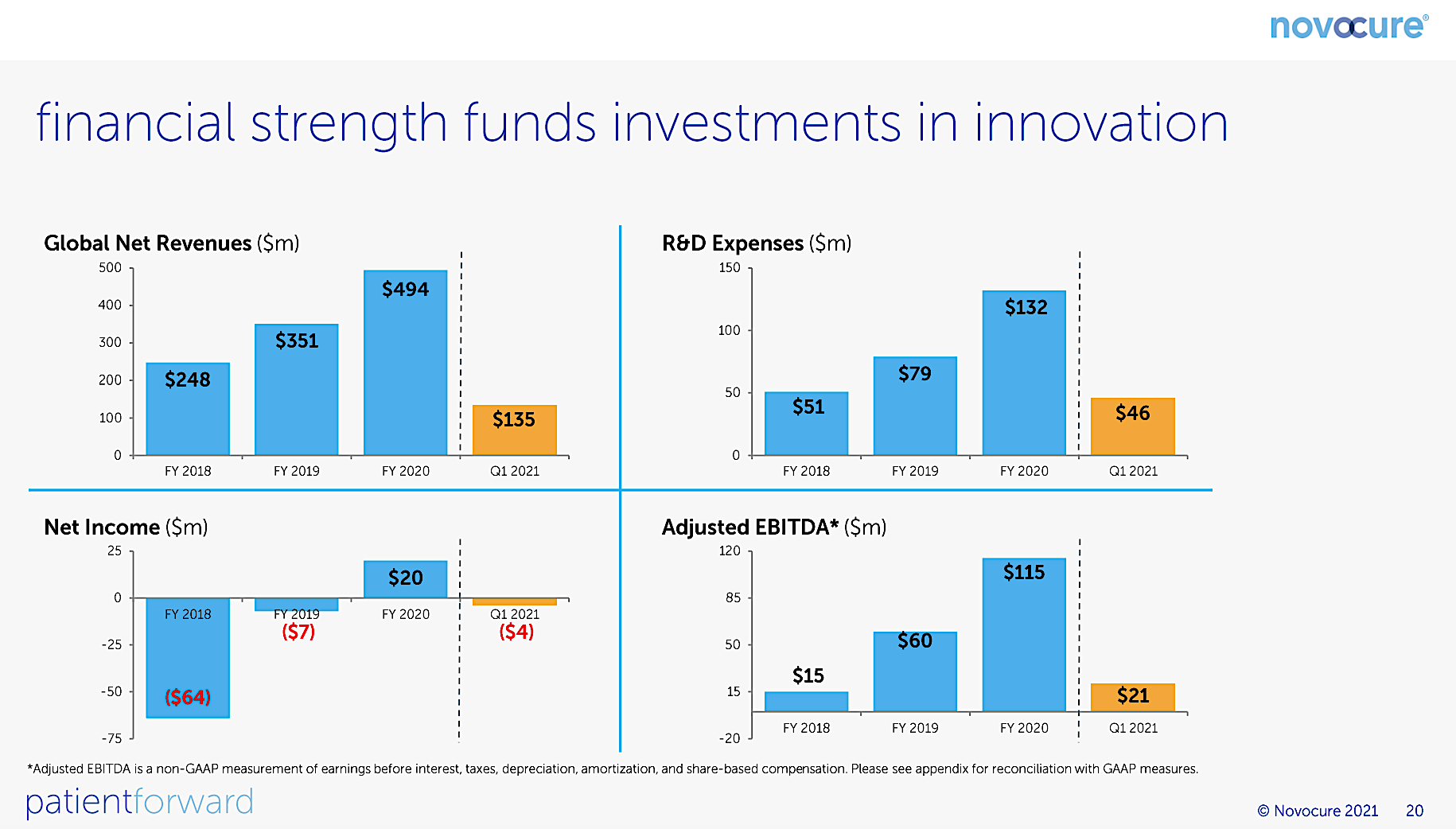

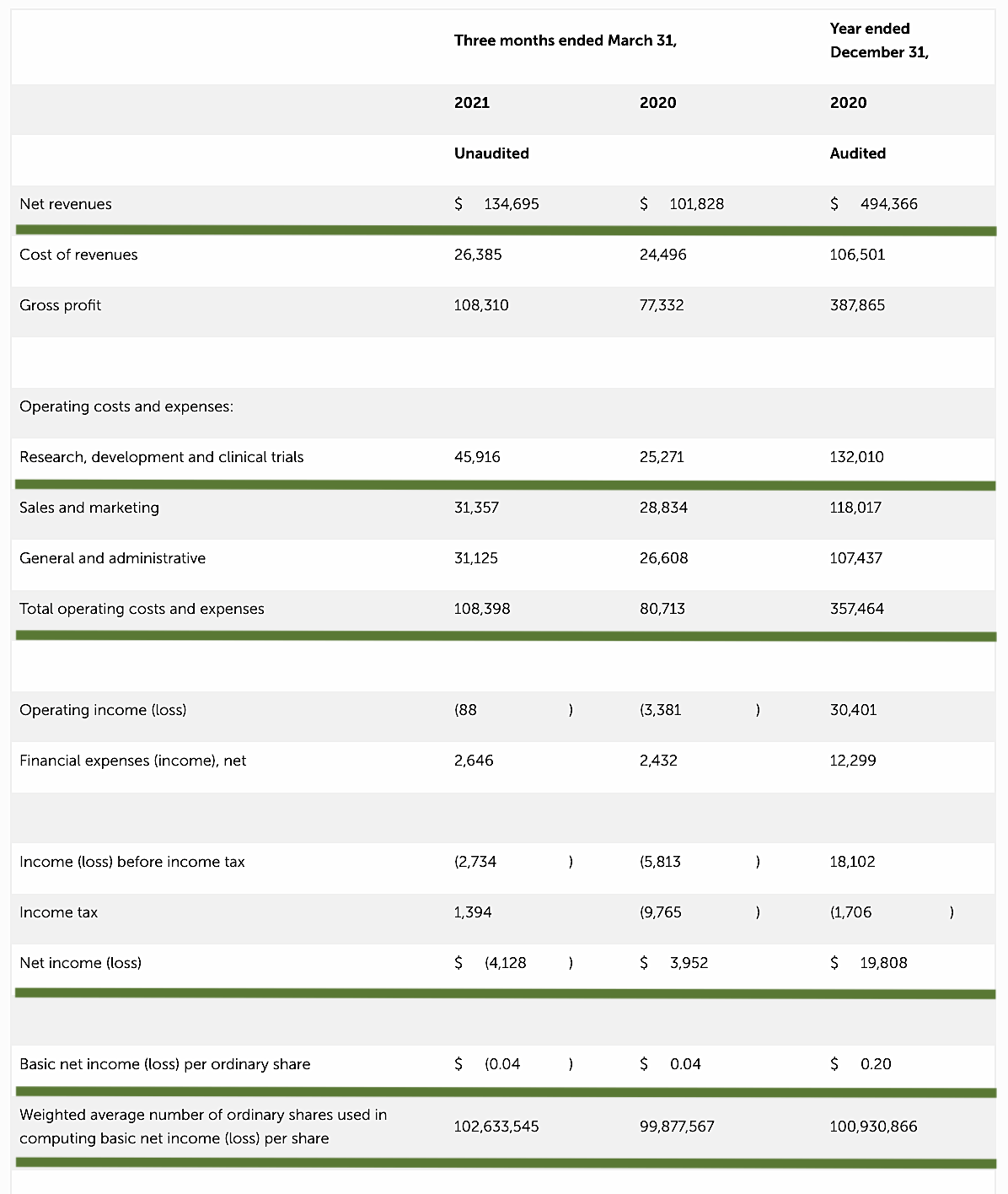

Just as you would get an annual physical for your well-being, it's important to check the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll assess the 1Q 2021 earnings report for the period that ended on March 31.

As follows, NovoCure procured $134.6M in revenue compared to $101.8M for the same period a year prior. As such, the revenue grew by 32.2% year-over-year (YOY). With COVID abating while there is increasing clinical advancement, I expect the sales growth to be multiple folds higher in the coming years.

That aside, the research and development (R&D) for the respective periods registered at $45.9M and $25.2M. I view the 82.1% R&D increase positively because the money invested today can turn into blockbuster profits in the future. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $4.1M ($0.04 per share) net loss compared to $3.9M ($0.04 per share) net gain for the same comparison. The bottom line depreciation makes sense, as the company is boosting R&D investment and commercialization ramp-up.

Figure 9: Key financial metrics (Source: NovoCure)

Figure 9: Key financial metrics (Source: NovoCure)

About the balance sheet, there were $864.4M in cash, equivalents, and investments. Against the $108.3M quarterly OpEx, there should be adequate capital to fund operations into 1Q 2023. Simply put, the cash position is robust.

While on the balance sheet, you should check to see if NovoCure is a "serial diluter." After all, a company that is serially diluted will render your investment essentially worthless. Given that the shares outstanding increased from 99.8M to 102.6M, my math revealed a 2.8% annual dilution. At this rate, NovoCure cleared my 30% cutoff for a profitable investment.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are "growth-cycle dependent." At this point in its life cycle, the main concern for NovoCure is whether the company can boost its revenues further.

The other risk is if NovoCure can generate positive cash flows in the coming years. I believe that investors will sell off the stock if there is no net profit in the next three years. There is also a 35% chance that the various clinical investigations won't generate positive results.

Conclusion

In all, I recommend NovoCure a buy with a five out of five stars rating. Riding the stellar science of TTFields, Novocure is making big waves in the therapeutic innovation space. After TTFields approval for GBM and mesothelioma, NovoCure is enjoying strong sales trading. Net revenues have reached beyond halfway toward blockbuster. Nevertheless, I strongly believe that sales will continue to ramp up aggressively due to the abatement of COVID. More importantly, there is a flurry of clinical catalysts for this year and beyond. Ultimately, I believe various ongoing development will translate into robust share price appreciation. Though NovoCure is a stalwart, you can expect this stock to see roughly 50% share price appreciation.

Thanks for reading! To read the full article, CLICK HERE. To get the latest articles, please hit the orange “Follow” button on top.

Be sure to check out our private investment research community, Integrated BioSci Investing.

Dr. Tran's analyses are the best in the biotech sphere, well worth the price of subscription.

Very professional, extremely knowledgeable and very honest … I would highly recommend this service and his stock picks have been very profitable.

Simply put, this is worth every penny. Just earlier today, one of the companies recommended by Dr. Tran got acquired for a nice 50% premium.

Click here for a FREE TRIAL.