This is an update on insider buying in the gold mining (NYSEARCA:GDX) sector over the past month. I've been publishing these updates monthly to give readers a pulse on insider trading activity to spot potential buying opportunities.

I track insider buying closely to see which insiders are bullish on their company and buying shares. Over time, I have noticed that insiders tend to time purchases wisely.

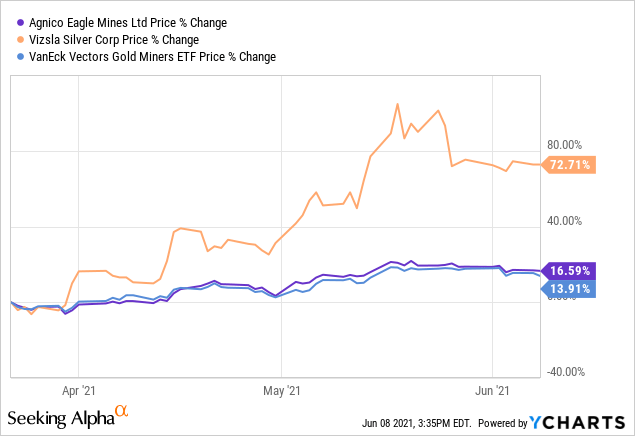

Back in March, I noticed insiders were loading up on Agnico Eagle Mines (NYSE:AEM) and Vizsla Silver (OTCQB:VIZSF), and shares are up substantially since then, outperforming the gold miners index.

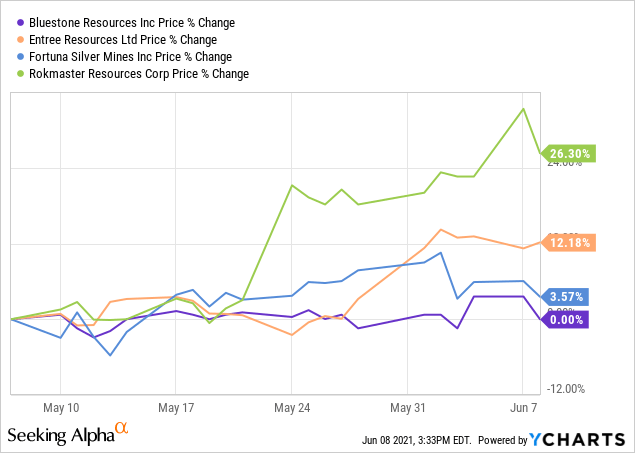

My last insider buying update came in May, when I highlighted insider purchases at Bluestone Resources (OTCQB:BBSRF), Entree Resources (OTCQB:ERLFF), Fortuna Silver Mines (NYSE:FSM), and Rokmaster Resources (OTCQB:RKMSF).

Three of the four stocks mentioned have outperformed the GDX since publication on May 9. Rokmaster Resources has advanced by 26.30%, while Entree Resources has continued its ascent, returning 12.18% over the past month as one of its largest shareholders, Sandstorm Gold (NYSE:SAND), continued to increase its position.

Here are four gold stocks with recent insider buying, an overview of each company, and my thoughts on each stock.

(Note: To track insider trading, I follow MarketBeat's website, as well as SEDAR and CanadianInsider.com. Figures are priced in US dollars, unless stated otherwise.)

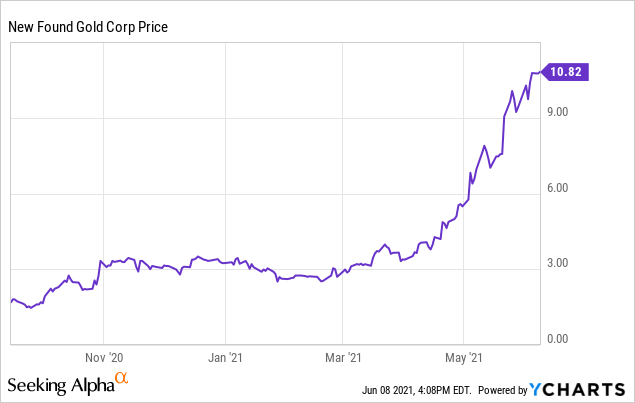

1. New Found Gold (OTCPK:NFGFF)

New Found Gold is the largest landholder in Newfoundland, claiming over 1,500 square kilometers of land prospective for gold mineralization. This is a top tier gold explorer which started the present-day Newfoundland gold rush when it released its first drill hole as a private company a few years ago, reporting a stellar 92.86 g/t gold over a 19-meter intercept.

Since then, it has been off to the races, with the explorer consistently reporting grades of 15 g/t and higher, starting at surface, most recently reporting its best assay yet (146 g/t gold over 25.6 meters.) The project has drawn comparisons to Kirkland Lake Gold's (NYSE:KL) Fosterville mine due to the epizonal-style mineralization and comparable features in mineralogy.

New Found Gold is a well-financed company and has strong support from insiders, which includes its largest shareholder, Palisades Goldcorp, which owns 31%, precious metals investor Eric Sprott (18%), Novo Resources (10%), Rob McEwen (7%), and management & insiders (6%).

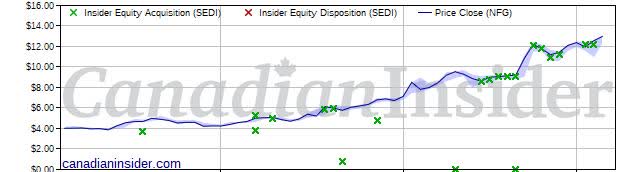

Sprott has not only been holding onto his shares tightly, but he has also been adding to his position:

- Sprott acquired 200,000 shares at prices ranging from $12.210 to $12.227 between June 2-3, 2021, which represents a C$2.44 million investment, according to insider filings.

(Sprott's insider purchases are marked with a green X. Source: CanadianInsider.com)

- Sprott previously invested C$15 million in the company back in April, purchasing 2.857 million shares at C$5.25 per share, via a non-brokered private placement (the financing was at a premium to New Found Gold's stock price at the time of the announcement.)

Sprott's latest investment in New Found Gold is a major show of support in the gold explorer because despite sitting on 100%+ gains, he is still adding to his position. It's clear that Sprott is investing for much larger returns and believes the stock has further room to run.

Despite my enthusiasm for New Found Gold and the recent insider buying from Sprott - which I view as a very positive sign - I am hesitant to be adding to my position here as I sit on 478% unrealized gains. Instead, I am going to be patient and wait to see if we get a dip below US$10, at which point I may re-consider a purchase.

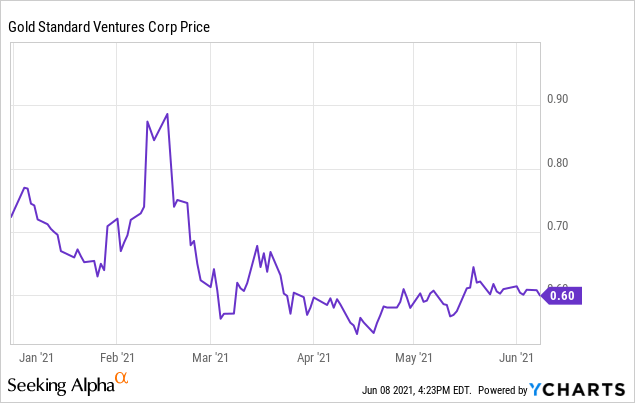

2. Gold Standard Ventures (NYSE:GSV)

Gold Standard Ventures is developing the South Railroad project, which is an open pit, heap leach gold project located in Elko County, Nevada. The company is actually the second-largest landholder on the Carlin Trend of Nevada, with a more than 20,000 hectare land package; the majority of the Carlin Trend is controlled by senior miners Barrick (NYSE:GOLD) and Newmont (NYSE:NEM) through a joint-venture.

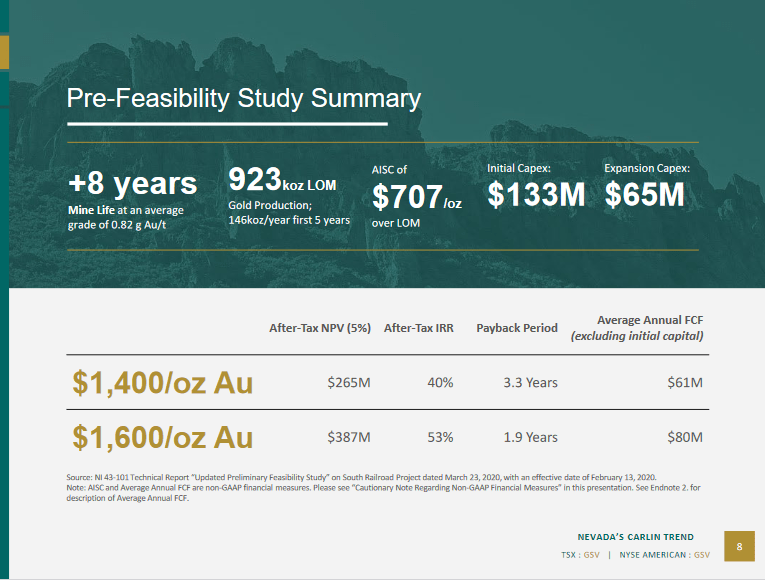

Gold Standard has released a pre-feasibility study, which outlines potential production of 146,000ozAu per year over the first five years at US$707/oz all-in sustaining costs, and which estimates a net present value of US$387 million (post-tax, 5% discount rate) with a low upfront capex estimate of US$133 million. Gold Standard has a market cap of US$214 million, as of writing, and so it appears to trade at a reasonable valuation.

(Source: Gold Standard Ventures presentation)

Currently, Gold Standard is focused on growing its ounces at the Pinion and Dark Star deposits, with a goal of adding at least 300,000 ounces of gold to mineral reserves to be included in its mine plan. In May, it announced plans to drill close to 8,000 meters over 46 holes at Pinion, Dark Star and LT.

Recently, a few insiders bought shares of Gold Standard in the public market:

- On May 13, Alexander Morrison, Director, bought 100,000 shares at a price of US$.564.

- On May 13, Jason Mark Attew, President, CEO and director of the company, bought 7,500 shares at C$.69.

- Management and the board of directors own approximately 4% of the fully diluted shares outstanding, according to Gold Standard's most recent corporate presentation. That doesn't sound like much, but it equates to a value of approximately $8.56 million.

- Readers should also note that Gold Standard raised C$34.5 million in a private placement back in February, issuing 39.2 million shares at a price of C$.88, while the stock trades at C$.73, as of writing on June 8.

The stock has certainly been a disappointment, with shares down 12.3% over the past year compared to a 17.4% gain in the GDX. The share structure is quite bloated with 378 million shares fully diluted. That is high even for a gold explorer like Gold Standard.

Despite the underperformance, I believe Gold Standard presents a decent risk vs. reward for new investors at the present moment.

This is a well-funded company that has released a positive technical study with a high net present value and very low upfront capex requirements. Its current market cap is almost half the project's NPV. And it has a drill program underway which should lead to resource growth and potentially improve the mine's economics in the upcoming feasibility study. It's also exploring gold in the top tier mining jurisdiction of Nevada. All of this makes it attractive for a potential acquirer.

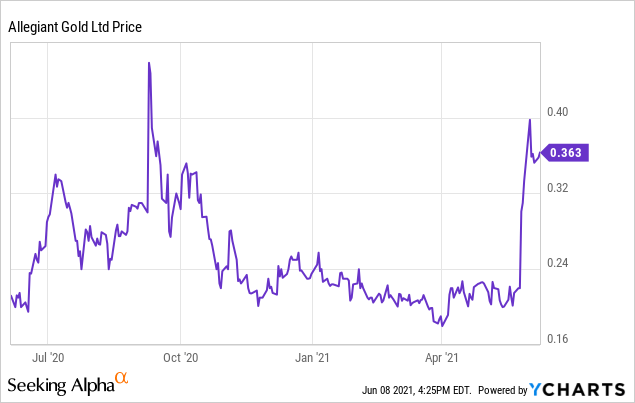

3. Allegiant Gold (OTCQX:AUXXF)

Allegiant Gold is a gold explorer which holds 10 drill-ready projects in the southwest U.S., including seven in the state of Nevada. Its flagship project is Eastside, where it has defined a 1.1 million gold equivalent ounce resource (made up of 996,000 ounces of gold and 7.8 million ounces of silver.) One of its goals is to grow that resource to 2 million ounces through aggressive exploration.

Allegiant is a particularly interesting explorer because four of its projects are farmed out to other explorers, and those option agreements provide annual cash payments to the company. These payments have helped fund its exploration efforts and kept its share structure quite lean with just 88 million fully diluted shares outstanding.

On May 26, Allegiant reported bonanza gold and silver grades from drilling at Eastside. The results were its best to date and included 147.8 meters of 2.55 g/t gold, which was a 100-meter step-out drill from the closest hole in the original pit at Eastside (this means the resource is very likely to expand in a future update.) This hole included an intersection grading 21.9 g/t gold over 14 meters and 173.8 g/t silver over 20 meters; grades were well above the .54 g/t reported in its resource estimate.

Silver bulls will also be pleased to read that Allegiant reported significant silver intercepts, which included 6.1 meters of 113.35 g/t silver and 44.2 meters of 93.3 g/t silver.

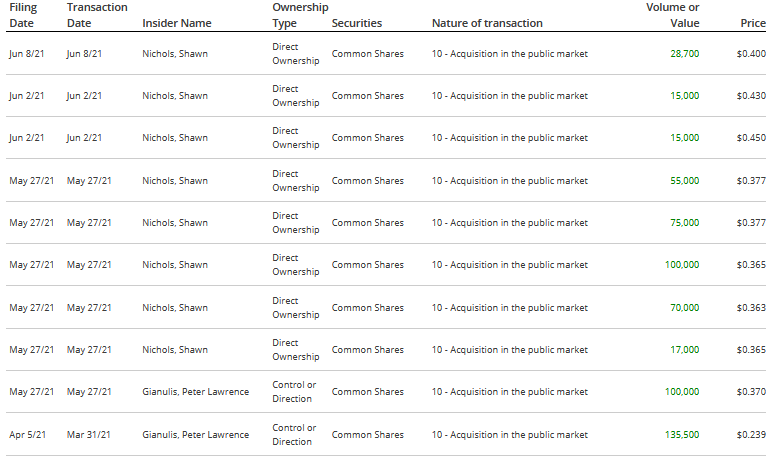

Insiders appear very bullish on Allegiant, as it has witnessed the most insider buying of any stock in this article.

Here's a summary of recent transactions:

(Source: CanadianInsider)

- Shawn Nichols, Director, has been the most active buyer of shares recently, purchasing 58,700 shares in June at prices of C$.40, C$.43 and C$.45.

- Peter Gianulis, CEO of Allegiant, bought 100,000 shares at C$.37 back on May 27 and also bought 135,500 shares at C$.239 on March 31.

- Readers should note that management and insiders have bought approximately 9 million shares in the public market since September 2019. Insiders hold more than 16% of the outstanding shares, according to its corporate presentation.

Out of the stocks mentioned in this article, I am most bullish on Allegiant Gold. The recent bonanza grades at Eastside appear to be a turning point for the stock, with renewed investor interest.

4. i-80 Gold (OTCPK:IAUCF)

i-80 Gold is a spin-out company from Premier Gold Mines via its takeover by Equinox Gold (NYSE:EQX). This is a new Nevada-focused gold producer which boasts more than 5 million ounces of gold in reserves and resources, through its three development-stage projects. The company's goal is to produce at least 200,000ozAu per year at sub-$1,000/oz AISC, while growing its resources to at least 10 million ounces.

The company owns 40% of the producing South Arturo mine, 100% of the advanced exploration-stage Getchell project (PEA study to be released shortly), and 100% of the advanced exploration-stage McCoy-Cove project.

i-80 Gold has some strong potential catalysts ahead this year, including an underground drill program at South Arturo, the release of a PEA study at the 1.275 million ounces Getchell project, and the advancement towards a feasibility study at McCoy-Cove.

Insiders have actively been buying shares in the public market over the past few weeks:

- The most notable purchases came from Ewan Downie, who is the company's CEO and director. He's purchased over 90,000 shares since May 25th at prices ranging from C$2.57 - C$2.65.

- On May 27, Equinox Gold, a mid-tier gold miner which is a major shareholder owning 30.3% of the company on a fully diluted basis, subscribed for 5,479,536 new common shares of the Company at a price of C$2.60 per common share, for proceeds of C$14.2 million.

According to Downie this was a positive move:

The exercise of Equinox's anti-dilution right further strengthens our balance sheet and I believe demonstrates Equinox's commitment to the work with i-80 as we aggressively grow our business in Nevada.

i-80 Gold is an organic growth story, and it appears to carry a pretty low valuation of US$454 million, compared to its three assets which carry production potential of 200,000+ ounces of gold per year at sub-$1,000/oz AISC. Ultimately, I believe the stock could be a takeover target for a mid-tier miner seeking to diversify into the mining-friendly jurisdiction of Nevada.

I'm keeping an eye on i-80 Gold for now and will analyze its coming drill results and PEA study before making an investment decision.

If you want more gold mining stock analysis, subscribe now to The Gold Bull Portfolio. I help my subscribers find the best money-making opportunities in the gold & silver sector.

Receive frequent updates on gold mining stocks, access to all of my top gold and silver stock picks and my real-life gold portfolio. I offer a 37% discount on annual subscriptions vs. monthly, with a 30-day money back guarantee!