Introduction

When looking back at my library of analysis, it has been approximately eight months since last covering Höegh LNG Partners (HMLP) and as my previous article discussed, their distribution yield still sits at a very high 10% yield was unfortunately risky. Since quite a length of time has now passed, this article provides a follow-up analysis that reviews their subsequently released financial results and most importantly, assesses the resulting outlook for their all-important distributions.

Executive Summary & Ratings

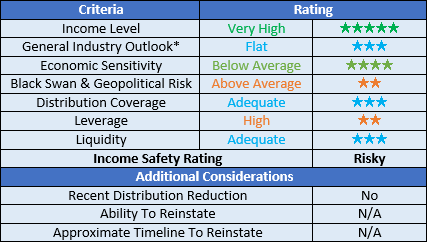

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Image Source: Author.

*Even though LNG is often considered to see further growth in demand, this has to be balanced against the long-term threat from the world moving away from fossil fuels and thus the general industry outlook was deemed to be flat.

Detailed Analysis

Image Source: Author.

Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and best captures the true impact on their financial position. The main difference between the two is that the former ignores the capital expenditure that relates to growth projects, which given the very high capital intensity of their industry can create a material difference.

It should be easily agreeable that the most desired and thus important aspect for their partnership is their very high distribution yield since after all, the primary purpose of any Master Limited Partnership is providing a relatively high income to their unitholders. When it comes to the world of income investing, a general rule of thumb is that lower risks equal lower yields and thus by extension, buying units in a partnership with a risky yield can be very well rewarded with higher unit prices as the risks subside. The two most important fundamental considerations that sit at the core of distribution risk are their coverage and the health of their financial position.

Since conducting my previously linked analysis, they have released their results for the second half of 2020 and despite the turmoil caused by the Covid-19 pandemic, their operating cash flow remained essentially unchanged for the full-year versus 2019 at $85.8m. Following this resilient performance and their essentially non-existent capital expenditure, they saw adequate distribution coverage of 114.60% and thus remained broadly in line with the previous analysis.

When looking at their more recent first quarter of 2021 result their operating cash flow was 15.28% higher year-on-year at $16.2m versus their $14m during 2020, their distribution coverage was less than adequate at only 89.52%. Thankfully it partly stemmed from a working capital build of $4.7m and if removed, their underlying operating cash flow of $20.9m would have seen their distribution coverage remain an adequate 110.07%.

It should also be mentioned that their results for the first quarter of 2020 saw a far larger working capital build of $9.3m, thereby pushing up their underlying operating cash flow to $23.3m. Since this means that their results for 2021 sit 10.62% lower year-on-year, they clearly had a soft start to 2021. Whilst not necessarily ideal, one quarter alone does not call for concern since quarter-to-quarter variations are natural but given their continued very thin margin of safety to absorb any possible lengthier impacts, it will be especially important to consider how their financial position has evolved since the previous analysis.

Image Source: Author.

Despite there being nine months of financial performance subsequently released since my previous analysis, there have only been minimal changes to their capital structure but at least they were positive. When last reviewing their net debt it stood at $414.9m, which subsequently decreased to $401.3m by the end of 2020 and is now down to $395.1m following the first quarter of 2021 for a total change of only 4.79% and whilst this helps, it only just barely moves the needle. It should also be mentioned that the only reason that their net debt decreased during the first quarter of 2021 was due to them issuing $8.3m of preferred units, which is not ideal since it slightly boosts their future cash outflows.

Image Source: Author.

Following their rather soft start to 2021 during the first quarter and their net debt decreasing only slightly, it was quite surprising to see their net debt-to-EBITDA drop significantly down to only a moderate 2.67 from its previous high result of 4.01 when conducting the previous analysis. This rather odd situation arises from their accrual-based earnings during the first quarter of 2021 being boosted materially by their equity earnings of joint ventures, which came in at $11.1m versus only $6.4m for the entirety of 2020.

Since the beginning of 2018 their equity earnings of joint ventures have not once translated into their cash-based financial performance, which is evident with their accrual-based net debt-to-EBITDA always being lower than their cash-based net debt-to-operating cash flow. Whilst technically correct under accrual-based accounting standards, it remains debatable the extent that they benefit their unitholders. Until such time these translate into tangible cash flow performance, it seems reasonable to continue judging their leverage as high given their net debt-to-operating cash flow of 4.73 sitting within the applicable territory of between 3.51 and 5.00. This means that despite the small progress seen through their lower net debt, they still only have a very little financial safety net to provide support to their barely adequate distribution coverage.

Image Source: Author.

Similar to their capital structure and leverage, their liquidity has not materially changed with their respective current and cash ratios of 0.72 and 0.35 being quite similar to their respective results with the previous analysis of 0.77 and 0.40. Whilst this does not pose any new risks, it nevertheless still cannot completely mitigate the risks from their high leverage and considering they need to refinance their debt maturities for 2021 it would not be wise to count upon their credit facility to bridge any gaps, as the table included below displays.

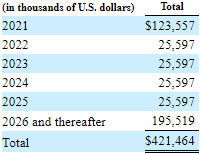

Image Source: Höegh LNG Partners 2012 20-F.

It can be seen that they face a large $123.6m of debt maturities before 2021 ends, which given their current cash balance of $27m and only thin free cash flow after distribution payments, they cannot possibly repay. This means that they are reliant on financial markets to provide refinancing options and thankfully they have already started this process with it seemingly progressing well, as per the commentary included below. Once this refinancing has been completed, it will almost certainly see their liquidity improve and will likely warrant a strong rating given their already desirable cash ratio.

“To address the liquidity needs, the Partnership has commenced this refinancing process and is at an advanced stage to completing the refinancing of the Lampung facility. The loan documentation has been finalized and is now subject to satisfaction of closing conditions before drawdown. For the joint venture, the refinancing is in the planning stage.”

-Höegh LNG Partners Q1 2021 Conference Call.

Conclusion

Overall it seems that they are still making progress towards strengthening their financial position and thus reducing the risks surrounding their very high distribution yield, but they are still not quite there and thus their all-important 10% yield remains risky. Following this analysis and the only minimal underlying fundamental changes, I still believe that a neutral rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Höegh LNG Partners’ SEC filings, all calculated figures were performed by the author.