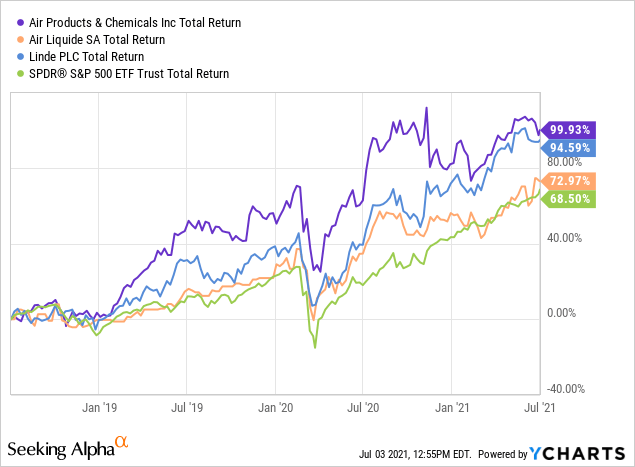

Over the last three years, Air Products and Chemicals (NYSE:APD) has delivered a return that doubled value for shareholders, ~100%. Linde (LIN) also generated a similar return while L'Air Liquide (OTCPK:AIQUY) and the S&P 500 delivered a total return of ~65%. In light of this outperformance, investors are naturally asking themselves whether the GDP-based stock still has room to further yield strong gains, especially after it missed EPS by $0.08 at $2.12 in 1Q21 and by $0.02 at $2.12 in 4Q20. While it is true that the stock has actually underperformed its peers over the last year, the stock is still trading well above its historical EBITDA multiple of 12x at 17.5x currently. This is also a notable premium to the 14.1x EBITDA multiple for Air Liquide, though slightly below Linde's 18.5x.

According to Seeking Alpha data, the Street is roughly split on the stock. Just slightly more than 50% of the 27 analysts are "bullish" or "very bullish" on the stock, with the rest being "neutral". This is a sentiment that has largely stayed the same since 2020, as the stock continued to do well despite bumpy performance. To the company's credit, ROIC has improved materially in the recent years from the high single-digits in the early 2010's to 11.3% currently as EBITDA margins have expanded from 25.8% in 2011 to 40.5% over the twelve trailing months. In other words, the company has dramatically improved its efficiency. At the same time, the company has massive upside exposure on the renewables front and is building a world-scale net-zero hydrogen energy complex for ~C$1.3 billion that provides a strong foundation for the future. This facility will produce net-zero pipeline hydrogen and liquid hydrogen, oxygen, and nitrogen for various end markets, and will come online in 2024. With an aggressive $18 billion capital budget and a leadership position post the Shell/GE gasification acquisition, the company is positioned for further momentum even as the cash flow becomes more de-risked. Fundamentally, the business looks good; but, the question is whether it's worth the price.

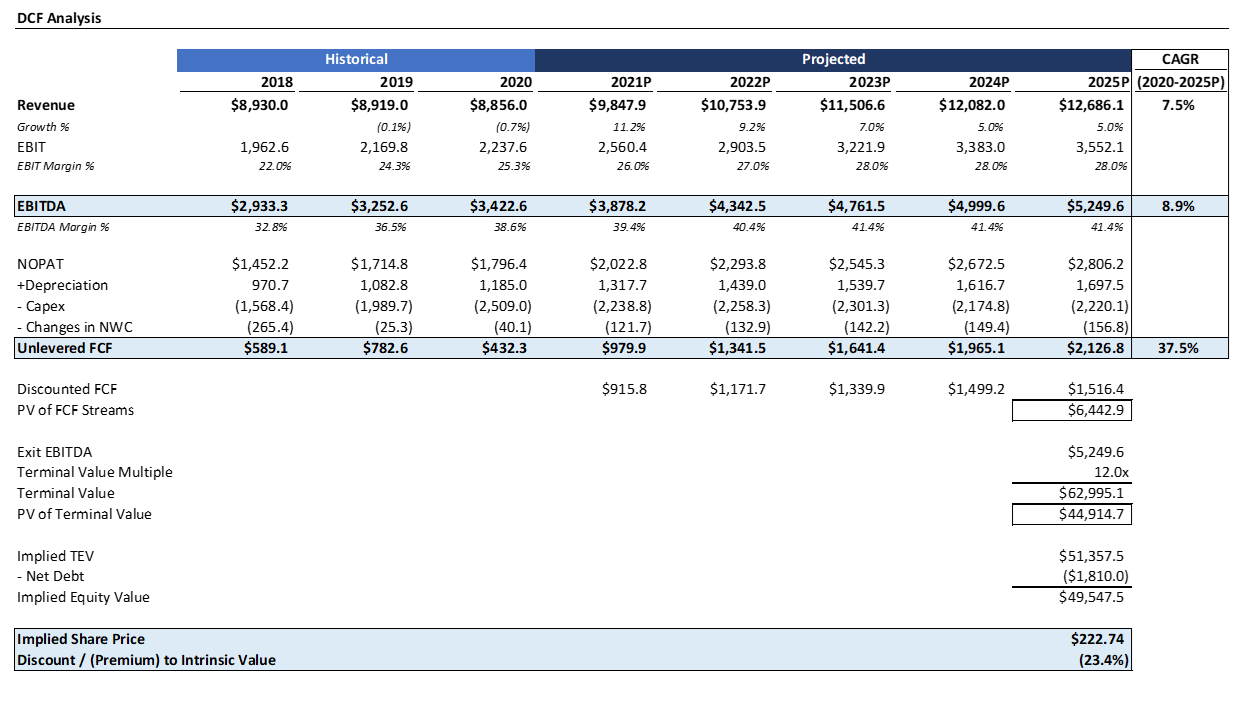

DCF Analysis Indicates 25% Downside

As strong of a performer as Air Products have been, I believe the upside has been more than captured. To prove out this point, I ran a DCF analysis. No DCF analysis can provide a perfect picture of future returns for shareholders; however, they can provide an illustrative "story" of the likelihood of different scenarios. In my DCF analysis, I assumed consensus revenue and EBITDA estimates through 2023 (when they usually run out to) and then forecasted 5% growth thereafter. I also assumed EBIT margins continuing to expand from 25.3% in 2020 to 28.0% in 2025. To be generous, I dropped capex % by the end of my projection period to the low-end of the three-year historicals of 17.5% versus 28.3% most recently. I also flat-lined depreciation and changes in net working capital.

Source: Created by author using data from Yahoo! Finance

Assuming an EBITDA exit multiple of 12x and a 7% discount rate, I find the stock to have 25% downside. Importantly, this exit multiple may have further contraction potential. Currently, the EBITDA multiple is 17.5x, but, going back to the early 2010's, it was more in the 7.5-12.0x range. Either way, from 2015-2019, pre-COVID, the stock was trading at the 12.0x range, so my assumption isn't far off.

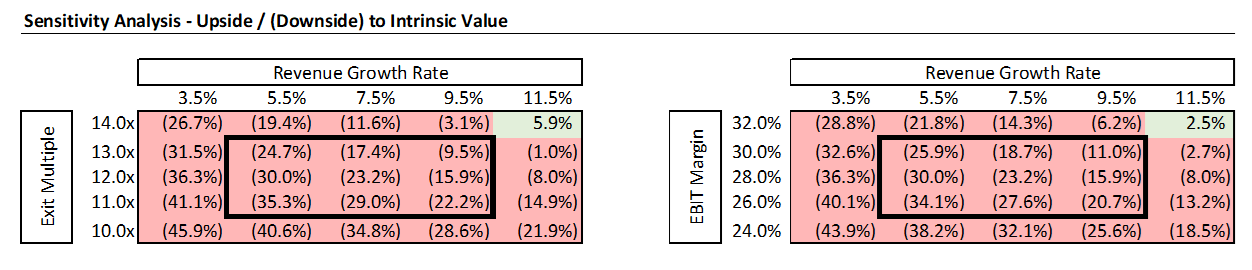

Even if you were to be generous and go with a 14x multiple, the stock would still have 12% downside! And this is also still assuming the company is able to grow revenue by a CAGR of 7.5% when it has been declining for several years. Tellingly, my DCF analysis indicates only (minimal) potential upside under 2 of the 50 scenarios: if the multiple is 14x and revenue grows by a 11.5% clip or EBIT margins expand 700 bps to 32% and revenue grows by a 11.5% clip. None of those scenarios are particularly realistic given past performance.

Source: Created by author using data from Yahoo! Finance

Downside Catalysts

There are several catalysts that could cause Air Products to contract. Firstly, the company faces increased competition from innovative players. Air Liquide's acquisition of Airgas and Linde's merger with Praxair has pushed Air Products behind the curve in the gas business. At the same time, contracts are becoming increasingly tougher to win out in China and India, which are also the big growth opportunities for the business. Any indication that the company is struggling there would detract from the margin expansion story, which has buoyed the stock for so long. Since Ghasemi took over in 2014, EBITDA margins expanded by 1,500 bps due to operating efficiency improvements and divestments of lower-profitability non-core assets that enabled Air Products to focus on emerging markets. In the first quarter, however, Asia volumes were down 2% from reduced Lu'An gasification project contribution. Currently, there is a high degree of uncertainty around the Lu'An and Jazan gasification projects, and, regarding the latter, management hasn't provided much clarity other than there are ongoing conversations with Saudi Aramco.

With an $18 billion capital allocation plan in place, all eyes are on the returns of future initiatives. You can always clean a company of its costs, but it's harder to do so and make sure that you're keeping the underlying operations strong. With Air Products failing to so far deliver on EPS consensus while other businesses are off to a good start, there's not much room for further misses. Weak industrial production is eroding merchant volumes, and the company has not yet returned to pre-pandemic growth. Debt/EBITDA is now also at a historic high of 4.2x versus the 1.5-2.5x historical range.

Upside Risks

While I am very bearish on the stock, the market has a way of making fools out of anyone, and it's important to stay humble. With that in mind, it's important to also consider how the stock could continue to do well. In addition to the hydrogen hype that's benefiting from secular tailwinds in green energy, the company still has strong runway for synergies to continue to reduce costs and for M&A to provide leading footholds into new markets, as it did in Latin America via Indura. With a dividend payout of 66% and a beta of 0.77, investors may also simply rotate to the stock as a means of, ironically, getting downside protection. At the end of the day, Air Products is still a GDP-based business and thus will always be capable of continuing to deliver gains for shareholders so long as the story of economic growth since the Agricultural Revolution continues to occur. After all, Air Products has a history of producing strong free cash flow across economic cycles. Further, materials exposure also offers investors an opportunity to hedge against inflation, which is still a big story as employment ramps back up and businesses start firing on all cylinders again.

Conclusion

Although Air Products has been an excellent cash cow even during the pandemic, the fundamentals do not justify the price at this point. The stock now trades at 26.9x forward earnings vs. 26.4x for Linde despite recent misses, increasing competition, and generally a smaller economic moat. Even if the multiple continues to remain above the ten-year historical level, there will still be downside. And while the GDP-based nature of the business means Air Products will never go away, it also means that there's not much the company can do to really disrupt its sector and justify the price (it's just a commodity producer), especially when it fell behind the curve following Linde's merger. Accordingly, I strongly recommend investors avoid the stock for now.