Plenty of great articles have been written about what Etsy Inc (NASDAQ:ETSY) does and what catalysts can drive its growth, as well as the risks that are associated with the company.

For a great analysis of Etsy's business model, you can check out the article titled "Etsy: Underappreciated Growth Story" by Andres Cardenal, CFA where Andres talks about why Etsy is more than just a "stay at home" stock. For some good points about potential risks, check out the article titled: "Etsy: Why I'm taking A Wait And See Approach With This Pandemic Winner" by Kennan Mell.

In this article, we want to focus more on the deep potential value hidden in Etsy from a purely fundamental point of view, rather than talk about things that have already been talked about.

Valuation

To value Etsy, we will use a discounted cash flow model. Forecasting is not easy and it's difficult to be precise. However, the point of forecasting is not to be right but to be reasonable. Our projections are not based on hype or an unrealistic extrapolation of the success witnessed in 2020. Instead, projections are based on the company's fundamentals. We try to determine what growth rates the company can fundamentally sustain up until 2025 and then transition the company to a "mature phase".

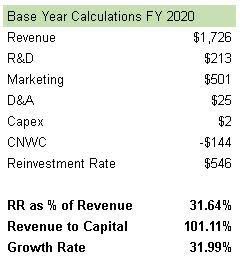

We will begin with the growth rate we expect for fiscal year 2021. The first thing we need is to determine what will constitute as reinvestment. For Etsy, it will be research and development, marketing, capital expenditures, and change in net working capital. Please note that depreciation and amortization is subtracted from the reinvestment rate as it is used as a proxy for maintenance capex that does not contribute to growth. The next step is to find the revenue-to-capital ratio. This measures how much revenue a company generates for each dollar in capital. Once we have both numbers, we multiply them to calculate the fundamental growth rate.

Source: Author

In the picture above, we see that the reinvestment rate was 31.64% of revenue. For revenue to capital, we used a 3-year average to smooth out the boost from COVID-19, which equaled 101.11%. Therefore, the fundamental growth rate for fiscal year 2021 equals 31.99%, slightly below analysts' expectations.

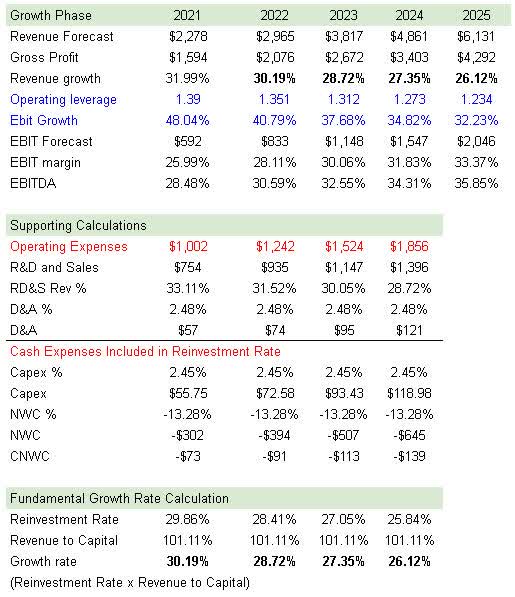

The next step is to determine the degree of operating leverage which is a multiple that measures how much the operating income of a company will change in response to a change in sales. Fiscal year 2020 is a bad starting point so we will use the average of 2019 and 2018 to get a more accurate representation. This resulted in an operating leverage of 1.39 which we decrease in a straight line in the forecast period to bring it close to 1 in year 10.

As the EBIT margin increases, the reinvestment rate decreases because R&D and marketing expenses become a smaller percentage of revenue, resulting in a slow down of growth. We measure this slowdown by setting R&D and marketing to 75.24% (the 5-year average) of total operating expenses. We then calculate the future fundamental growth rates with the projected numbers as follows for the growth phase:

Source: Author

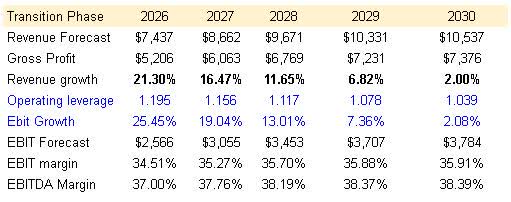

We used the average capital expenditure and D&A margins of the last three years. In addition, we used a gross margin of 70% which is actually below the company's current 74.4% gross margin to be a little more conservative. In the transition phase, we simply reduced growth in a straight line until it reached 2% which is what we used as the perpetual growth rate. We believe the EBIT and EBITDA margins are reasonable as they are comparable to those of eBay (EBAY).

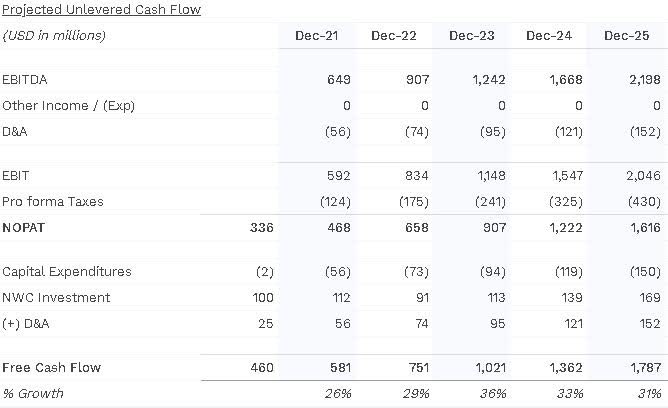

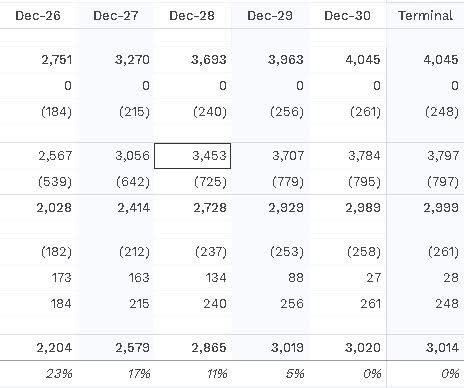

Now we will input these numbers into a DCF using the company's weighted average cost of capital of 6.02% based on current market conditions.

Source: Author using Finbox tools

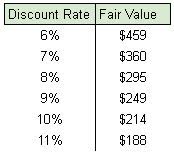

As you can see, with a 6.02% discount rate, 21% tax rate, and a forecast based on fundamentals, the company has the potential for 135.5% upside. Of course, discount rates are always changing and not everyone likes to use current discount rates. Therefore, we made the chart below to demonstrate the fair value at each discount rate:

Source: Author

As you can see, Etsy is undervalued up until a discount rate of almost 11%. We believe this provides a good margin of safety for modest downside variances from our forecast. It also makes us less worried about increases in the discount rate.

Final Thoughts, a Very Important Note

Now, before bears spam our comments section with doomsday predictions and before bulls run out to dump more money into Etsy, we want to make clear how to interpret our valuation.

To both the bulls and the bears, we don't disagree that stocks are inflated because of low interest rates. In addition, we don't rule out the possibility of high inflation for longer than expected which would lead to a rise in rates. However, we don't rule out the possibility of deflation that would be driven by technology. None of that really matters to us because interest rates move the market and we find that it is better to listen to the market than market commentators.

Currently, the risk-free rate has dropped considerably which has increased the valuations of stocks. Rates can remain stubbornly low for an extended period of time. Therefore, we personally prefer to react quickly to market conditions than to try and anticipate them. We're not saying buy and hold no matter what happens in the market. We are simply saying listen to what the market as a whole is saying by looking at the discount rates.

In addition, we are not saying that an investor needs to wait 10 years for the price of Etsy to hit fair value. We simply want to illustrate at what points future growth is fully priced in (at least by our estimates) so investors have some sort of guideline on when to take some profits if they choose.

With that being said, we believe Etsy has a strong enough margin of safety for us to initiate a position.