Thesis and Background

As a conservative investor who focuses on capital preservation in the long-term, the consumer staple sector is a great place to look for investment opportunities. The Coca-Cola Company (NYSE:KO) is a quintessential example of a dividend king, with 59 years of consecutive dividend increases behind it. Despite the current seemingly rich valuation, the stock is actually not that overvalued upon close examination. An analysis based on yield spread relative to the risk-free rate also suggests it is a good substitute for Treasury bonds under today's low rate environment.

Overview of the businesses

If there is a business that needs no introduction, it is probably KO. Not only because of its scale and presence, but also because its simplicity. The business has been the quintessential example of a perpetual compounder, and has achieved an impressive 59 years of consecutive dividend increases.

In recent years, the business has been facing some headwinds as consumer tastes and preferences shift. Soda consumption continues to decline in the U.S. The decline soda consumption certainly slowed KO's growth. But thanks to its diversified product line, lead position, scale, and global reach, despite of the headwinds, KO still enjoys superior profitability both relative to other peers in the same sector, as illustrated by the following chart. At the same time, KO is taking active steps to further diversify its portfolio with teas, coffee, fruit juices, sports drinks, bottled water, and even alcoholic beverages.

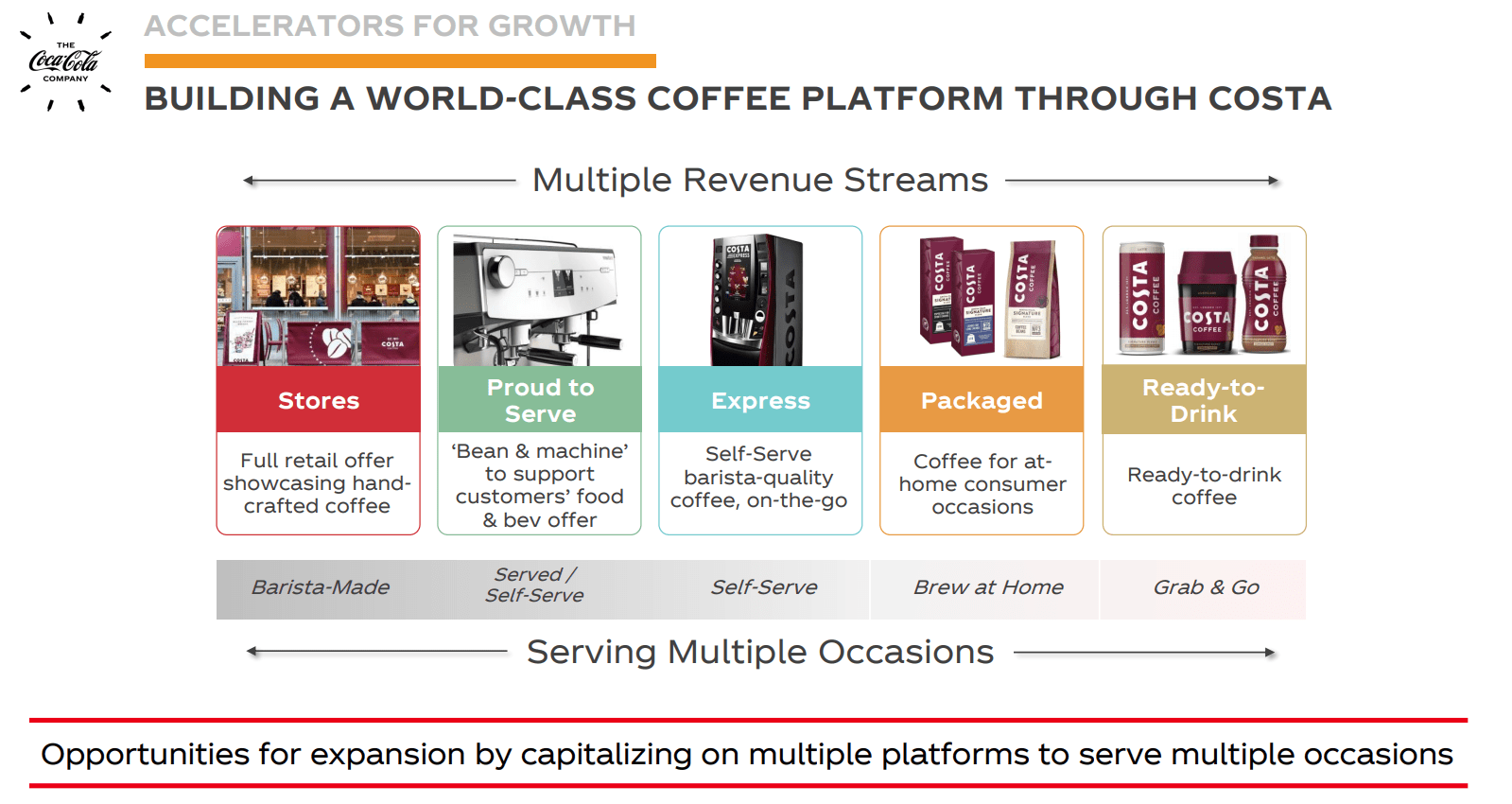

For me, at the end of the day, I do not view KO as a drink company, I view it as a marketing company. Actually, they are a world-class marketing company. With their marking expertise, scale, and reach, they have plenty of opportunities for expansion by capitalizing on multiple platforms to serve on multiple occasions.

I am not expecting KO to become a growth stock in any means, but I have a high degree of confidence that KO would be at least able to maintain its current profitability with its marketing expertise.

Source: KO investor presentation

Source: Seeking Alpha

The valuation

As can be seen from the following numbers in the table, at its current price levels, KO is about fairly valued or slightly overvalued depending on which valuation metric you use based on its historical valuations. In terms of absolute valuation, its current valuations (PE ratio around 26x) is on the expensive side, but not in any bubble regime for a scale leader with good quality like KO. In terms of dividend yield, the business is actually close to fair valuation.

Also, the business has been increasing its leverage in recent years. As seen from chart below, the business essentially has been debt free till 2020 - the interest coverage (defined as EBIT divided by interest expenses) has been more than 35x. The current interest coverage is about 10x. This cannot be considered debt free any more for sure. But 10x debt cover is a very safe and sustainable level for a business like KO who has such reliable profitability.

Source: author and Seeking Alpha

Source: author and Seeking Alpha

Based on the above analysis of the business fundamental, growth potential, and valuation metrics, it is relatively straightforward to project the return in the next a few years. Here let's consider the following "normal" scenario. This scenario considers the following return drivers:

1. 4.5% growth in the earning based on consensus forecast.

2. Share dilution at 1% per year based on its historical track record.

3. Dividend on the 3% level (assuming dividend increase would keep the dividend yield approximately at the current level).

4. A valuation revision to the mean due to market mood swing. If this occurs, it will cause a -3% CAGR in the next 3~5 years.

Based on the above return drivers, the annual return should be around 3.5% a year as shown below, with a total return of about 10~15% in 3~5 years.

Source: author and Seeking Alpha

Essentially buying a bond

For stocks like KO who enjoys stable income and pay a regular dividend, it is really a good substitute for bond, especially under today's ultra low interest rate environment. At least for two reasons - the return driver and the yield spread, as elaborated below.

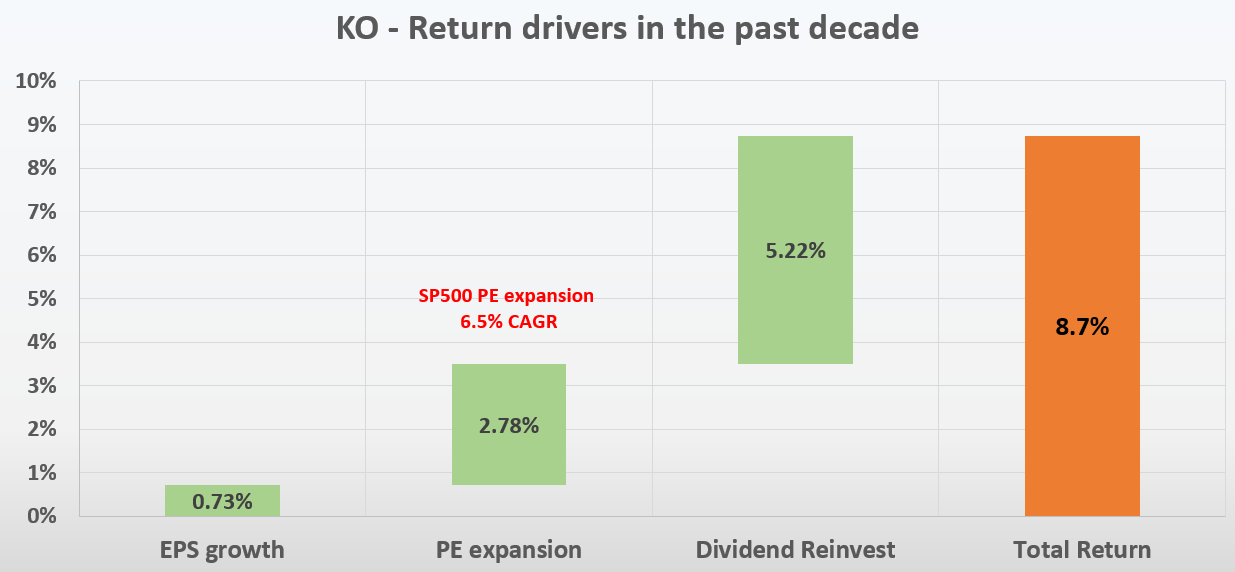

First, the return driver for KO is primarily dividend. As seen from the next chart, returns from KO has been largely driven by dividend - just like coupon payments are the major return driver for bonds. In the past decade, KO stock delivered 131% of total return (assuming dividend reinvestment), translated into CAGR of 8.7%. This return was driven by three factors as illustrated in the chart. Over the past decade, KO was able to grow the EPS at 0.73% CAGR. Second, thanks to a long bull market, PE expansion is the second driver as seen in the second chart, contributing 2.78% CAGR into the total return. Lastly, dividend reinvestment contributed the remaining 5.22%, making it the largest contributor by far. Besides illustrating the bond -like behavior of KO, this chart really highlights the power of dividend reinvesting for a dividend growth stock.

Source: author and Seeking Alpha data.

Second, the yield spread relative to Treasury bond is in favor of owning KO. For bond like equities like KO who enjoys stable income and pay a regular dividend, another useful indicator I rely on (and fortunately with good success so far) to gauge their valuation has been the yield spread, as illustrated in the following chart. This chart shows the yield spread between KO and the 10 year Treasury since its inception. The yield spread is defined as the TTM dividend yield of KO minus the 10 year Treasury bond rate. As can be seen, the spread is bounded and tractable. The spread has been in the range between about 0% and 1.5% the majority of the time. Suggesting that when the spread is near or above 1.5%, KO is significantly undervalued relative to 10 year Treasury bond (i.e., I would sell Treasury bond and buy KO). In another word, sellers of KO are willing to sell it (essentially an equity bond) to me at the same yield as a risk free bond. So it is a good bargain for me.

And when the yield spread is near or below 0%, it means the opposite. Now sellers are demanding such a high price that drives yield to be the same as risk free yield - which begins makes less sense to me as a buyer. No matter how good KO stock is, it does not have the ability to print money after all to pay dividend like a Treasury bond.

As of this writing, the yield spread is 1.66%, closer to the historical high end of the yield spread, suggesting a manageable risk profile relative to owning Treasury bonds even when the current valuation is slightly overvalued.

Source: author based on Seeking Alpha data

Conclusion and final thoughts

At its current price levels, Coca-Cola Company represents a quality business that has reached its full valuation at this moment. Under the current conditions, KO is really a good substitute for bond at least for several good reasons (that is, for investors who can manage to ignore the market price fluctuations). Analysis based on yield spread relative to the risk-free Treasury rate suggests it is currently in favor of owning KO than Treasury bond. KO provides 3% of coupon payment (in the form of dividend), and the dividend is very likely to keep increasing in the future. While 10 year Treasury bond currently provides 1.2% of coupon payment that does not change.

Thx for reading! And look forward to hearing your thoughts and comments.