People who succeed in the stock market also accept periodic losses, setbacks, and unexpected occurrences. Calamitous drops do not scare them out of the game. - Peter Lynch

In biotech investing, there will be periodic losses and unexpected occurrences that are outside of your control. For instance, the current FDA environment is unpredictable due to the recent controversial FDA approval of Aduhelm. Amid a catastrophe, you should reassess your investment thesis to see if you should cut your losses and move on.

That being said, Sesen Bio (SESN) is an intriguing investing story because the shares have rallied multiple folds before the recent debacle. As part of several companies recently impacted by the FDA scrutinized environment, Sesen's investment thesis is changed. In this research, I'll share with you a fundamental analysis of Sesen and provide my expectation on this biotech.

Figure 1: Sesen chart (Source: StockCharts)

About The Company

As usual, I'll present a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Operating out of the heart of medical innovation (Cambridge Massachusetts), Sesen is focused on the innovation and commercialization of stellar cancer treatments. The company leverages the therapeutic prowess of a technology dubbed targeted protein therapeutic, which is essentially an antibody-drug conjugate. I noted in the prior article:

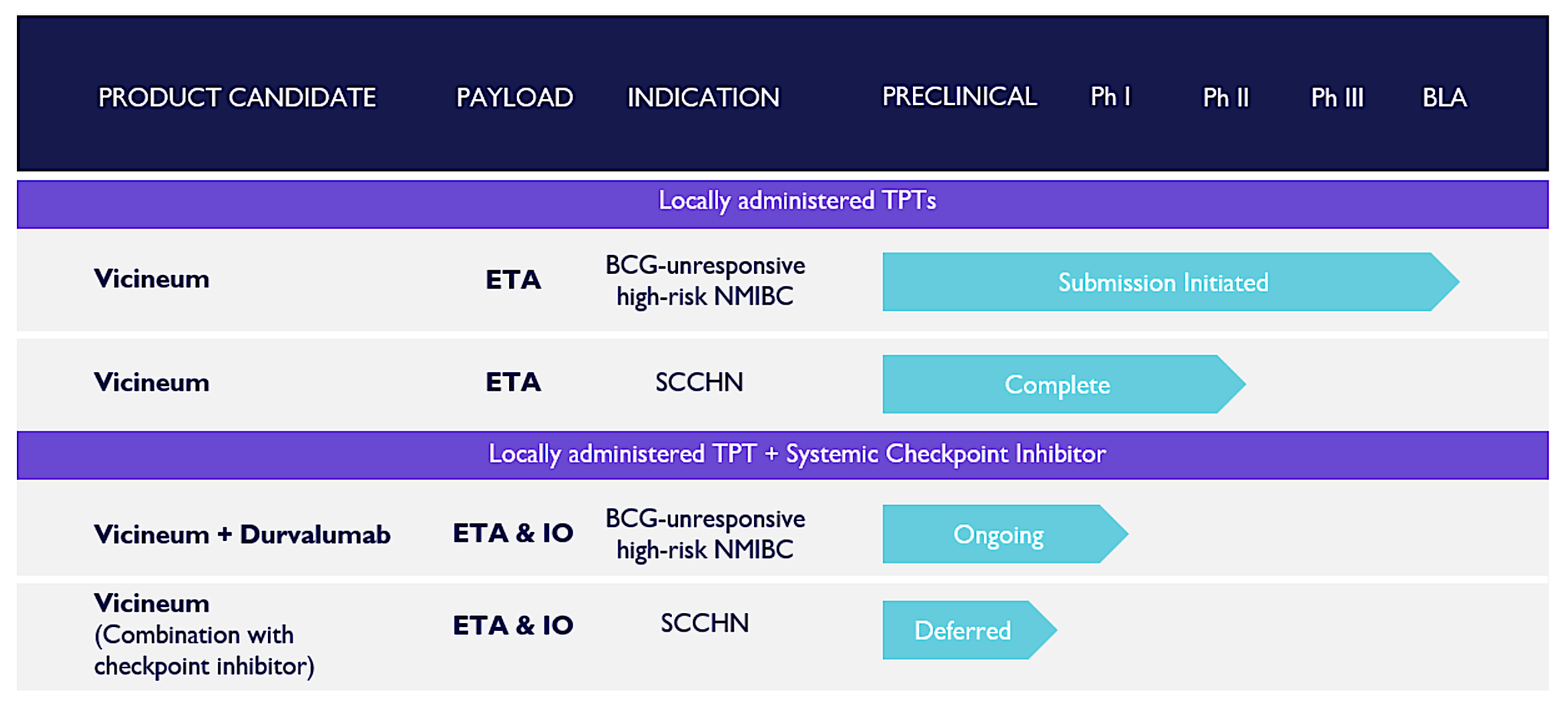

Viewing the pipeline below, you can see that the lead medicine (Vicineum) already cleared its Phase 3 VISTA trial. The potential next stop for Vicineum is to be crowned as the new standard of care for Bacillus Calmette-Guérin ("BCG") vaccine refractory high-grade non-muscle invasive bladder cancer ("NMIBC"). To boost long-term growth prospects, Sesen is expanding Vicineum's indication for squamous cell carcinoma of the head and neck (SCCHN) through a Phase 2 clinical investigation. Interestingly, there are combination studies of Vicineum with other immune checkpoint inhibitors like durvalumab (Imfinzi) of AstraZeneca (AZN).

Figure 2: Therapeutic pipeline (Source: Sesen)

Vicineum Complete Response Letter

Like a dagger thrusting at the heart of bio-innovation, Sesen announced that the US FDA issued a complete response letter (i.e., CRL) to Vicineum BLA for NMIBC. That is to say, Sesen mentioned that the FDA cannot approve in its current form and "has provided recommendations specific to additional clinical/statistical data and analyses in addition to Chemistry, Manufacturing, and Controls (i.e., CMC) issues pertaining to a recent pre-approval inspection and product quality." According to the President and CEO (Dr. Thomas Cannell):

We are deeply disappointed by this unexpected result, and it is an unfortunate day for patients suffering from BCG-unresponsive NMIBC. We remain dedicated to our mission to save and improve the lives of patients by bringing new treatment options to patients, and we intend to work closely with the FDA to understand the next steps.

As you can see, Sesen provided in the business call update that the company is requesting a Type A meeting with the FDA. This is a meeting that is immediately necessary for an otherwise stalled drug development program to proceed. And, it's usually being held after a CRL.

Though we don't know the specific outcome of the meeting yet, I believe that Sesen would need to run a new clinical trial. As such, this would extend the Vicineum approval by at least 12 months and an additional 6 months. Altogether, you can expect the delay to push the approval timeline to roughly 1Q2023.

Facing the aforesaid debacle, the key question you should ask is whether Sesen has adequate capital to fund Vicineum to approval. For a small company like Sesen, running an additional trial might put tremendous cash flow constraints on the balance sheet. On the investor's call, Dr. Cannell elucidated:

I will remind you that as of June 30, 2021, the Company had $151.1M in cash, cash equivalents and restricted cash. We believe we have the capital to do what is necessary to resubmit the BLA, and gain approval of a product that has the potential to save and improve the lives of patients.

The Uncertainty

Like all the bad news that seems to occur simultaneously, a Twitter source mentioned that Sesen's trial is marked by many violations and toxicity that has not been disclosed to the public. Specifically, the source referenced a STAT reporter who found through Sesen's internal documents over 2,000 trial violations, 215 classified as major. There was also one patient death in 2016 due to liver injury.

I tend to lean toward the veracity of a major news article. However, whether those are valid claims remains to be verified. Similar to how you feel, I'm intrigued by how the STAT author is able to garner the company's internal document. That is to say, did Sesen management leaked it, or was it the FDA? Simply put, it's an overhanging uncertainty. As you know, the market despises uncertainty which explicates the heavy selling pressure that Sesen has been experiencing.

That aside, there's a BMJ study demonstrating that most companies do not reveal the complete information in the CRL. Perhaps, investors have not been getting a complete picture of Vicineum's prospect. In that study, the author concluded,

FDA generally issued complete response letters to sponsors for multiple substantive reasons, most commonly related to safety and/or efficacy deficiencies. In many cases, press releases were not issued in response to those letters and, when they were, omitted most of the statements in the complete response letters. Press releases are incomplete substitutes for the detailed information contained in complete response letters.

Altogether, the new developments created many unknowns in the investing equation for Sesen. In the coming months, you can anticipate that Sesen management will provide an answer, i.e., after the Type A meeting. Thereafter, you can have clearer expectations of where this company is heading.

Financial Assessment

Just as you would get an annual physical for your well-being, it's important to check the financial health of your stock. For instance, your health is affected by "blood flow" as your stock's viability is dependent on the "cash flow." With that in mind, I'll analyze the 2Q2021 earnings report for the period that ended on June 30.

As follows, Sesen procured $2.2M in revenue compared to none for the same period a year prior. With the company being pre-commercialized stage, it's more meaningful for us to assess other metrics. That being said, the research and development (R&D) for the respective periods registered at $7.2M and $4.5M. I view the 60% R&D increase favorably because the capital invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits.

Additionally, there was $25.4M ($0.15 per share) net loss compared to $26.3M ($0.24 per share) decline for the same comparison. On a per-share basis, the bottom line improved by 60%. This suggests that Sesen is doing a good job with cost reduction.

Figure 3: Key financial metrics (Source: Sesen)

About the balance sheet, there were $151.1M in cash and equivalents. Against the $27.6M quarterly OpEx, there should be adequate capital to fund operations into 3Q2022. Simply put, the cash position is strong. While on the balance sheet, you should check to see if Sesen is a "serial diluter." A company that is serially diluted will render your investment essentially worthless.

Given that the shares outstanding increased from 112M to 175M, my math reveals a 56.2% annual dilution. At this rate, Sesen failed to clear my 30% cutoff for a profitable investment. However, this is not a hard-and-fast rule. As a small company, Sesen would need to raise tremendous capital to fund its therapeutic innovation.

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are "growth-cycle dependent." At this point in its life cycle, the main concern for Sesen is whether the Type A meeting with the FDA would reveal fruitful outcomes. In other words, the risk is extremely high that the FDA would require Sesen to conduct a new clinical investigation.

Obviously, a new trial would be highly time-consuming and capital intensive. Consequently, that can potentially put Sesen out of business. Dr. Cannell's prior company, Orexigen (OREX) went out of business in the past. The other concern is that Sesen would need to do more public offerings to continue funding its drug development. Therefore, that would dilute the value of your stocks.

Concluding Remarks

In all, I downgrade Sesen Bio to a sell with a 3.4 out of five stars rating. Despite the stellar prospects for its medicine (Vicineum), Sesen is facing great uncertainty regarding both its management as well as approval prospect. We are not sure whether the STAT claims on Sesen will prove valid. Concurrently, we do not know the depth of the requirement in running a new clinical trial. The current FDA environment since Aduhelm's controversial approval added many concerns to the investing equations. What is certain is that, with the new trial using Vicineum supply from its partners (i.e., Fuji and Baxter (BAX)), the CMC concerns would be abated.

As you know, I'm a mix between a realist and an optimist. On my optimistic side, I believe you can expect Sesen to garner much better outcomes with the upcoming European approval in 2022. Thereafter, Vicineum should be able to enjoy better results in the Far East with the potential China approval. Now, provided that there are no significant trial violations to render the results non-meaningful.

Thanks for reading! To read the full article, CLICK HERE. To get the latest articles, please hit the orange “Follow” button on top.

Be sure to check out our private investment research community, Integrated BioSci Investing.

Dr. Tran's analyses are the best in the biotech sphere, well worth the price of subscription.

Very professional, extremely knowledgeable and very honest … I would highly recommend this service and his stock picks have been very profitable.

Simply put, this is worth every penny. Just earlier today, one of the companies recommended by Dr. Tran got acquired for a nice 50% premium.

Click here for a FREE TRIAL.