When I wrote my article on Orange (NYSE:ORAN), many investors expressed doubts about the call, calling the company uninvestable or not a safe investment. While it's true that the company is on the higher tier in terms of shorter-term risk when it comes to things such as volatility, my firm stance is that the underlying assets and the company make for a solid investment both on the basis of what they do, and also what they have.

It's a stance I continue to hold. In this article, I'll show you why.

![]()

Orange - How has the company been doing?

A company such as Orange has some similarities with a business such as AT&T (NYSE:T) as well as some Scandinavian businesses in similar situations. It doesn't really matter if the company performs well in the short term, as it has during 2Q21/1H21, the company still doesn't go up significantly. Investors view the risks as being far more material here.

When it comes to Orange, what I mean by "perform well", is:

- Overall superb commercial performance, combining excellent equipment sales due to reopenings and 5G, as well as good B2B performance.

- Increased revenue numbers in growth areas as well as legacy areas.

- Moving forward on TowerCo.

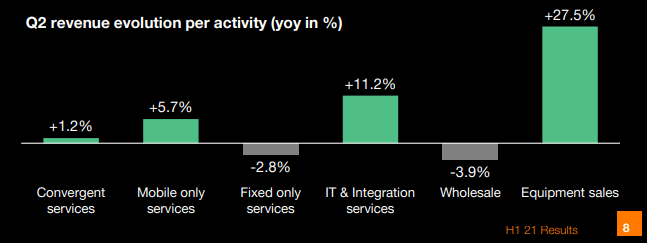

The company saw net adds in Enterprise, France, revenue growth in problem areas such as Spain, double-digit equipment sale increases, 5G launches in 6 European countries, and already almost 1 million 5G customers across the company's base.

Orange managed a 1.5% YoY revenue increase for the 1H21 period, a more or less flat EBITDAaL, increase in CapEx due to investments, organic cash flow of almost €850M, and combines this with a net debt/EBITDAaL of less than 2x, which compared to most telcos isn't just "good", it's in fact market-leading.

The revenue acceleration came primarily from non-France Europe, MEA, and Enterprise, with sales of new handsets, IT/integration, and mobile sales contributing to numbers.

(Source: Orange)

That doesn't mean that there isn't cause for some negativity, of course. The company recorded €3.7B worth of Spain impairment due to worse competition, continued headwinds from the pandemic, and some FX hedging. It's likely this negative net income, including this impairment, is impacting the company's share price.

However, on the flip side, the company once again shows that it's capable of generating over €800M in operational cash flow per half-year, meaning a capacity of over €1.5B per year. The company continues to be BBB+ rated, and a large part of that is its excessively strong liquidity position, having nearly €15B worth of cash or equivalents. The company's average cost of debt is less than 2.95% and the company has an average maturity on its bonds of nearly 9 years.

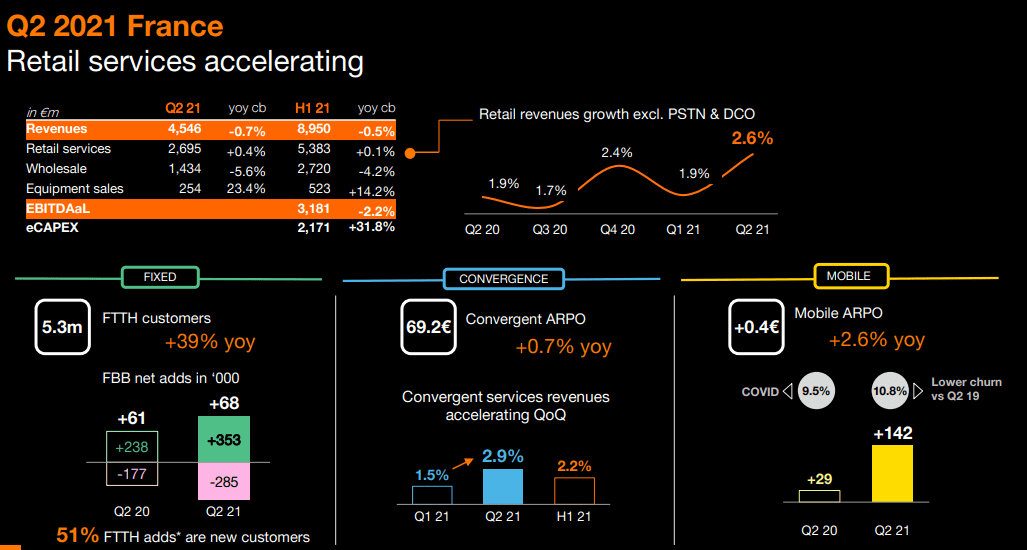

If we exclude the impairments in Spain, Orange's operations are showing impressive growth across the entire board. France is accelerating...

(Source: Orange)

...and remaining Europe is showing EBITDAaL growth of 4.7% YoY. The company added nearly 90,000 contract net adds during the second quarter, as well as 100,000 fixed broadband net adds. Spain, while impaired, is recording double-digit increases in Equipment sales, and the company has had success in its voluntary departure plan, which has been fully subscribed by employees. The company's Spain-based customer segment is stabilizing, and Orange is no longer losing customers, but adding them in both broadband, mobile and convergence.

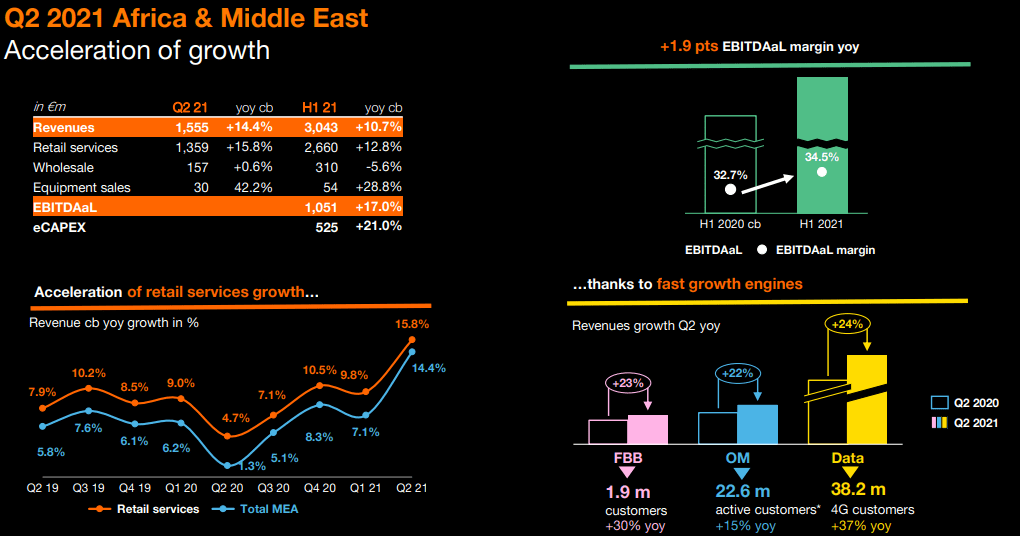

Then there are the company's growth areas in Africa and the Middle east, which are seeing massive growth.

(Source: Orange)

These positive results are echoed further by B2B, where IT services and mobile are causing growth - double-digit growth in terms of cybersecurity, cloud and digital & data. The B2B segment is contributing larger and larger portions of revenues to the company's overall sales and earnings.

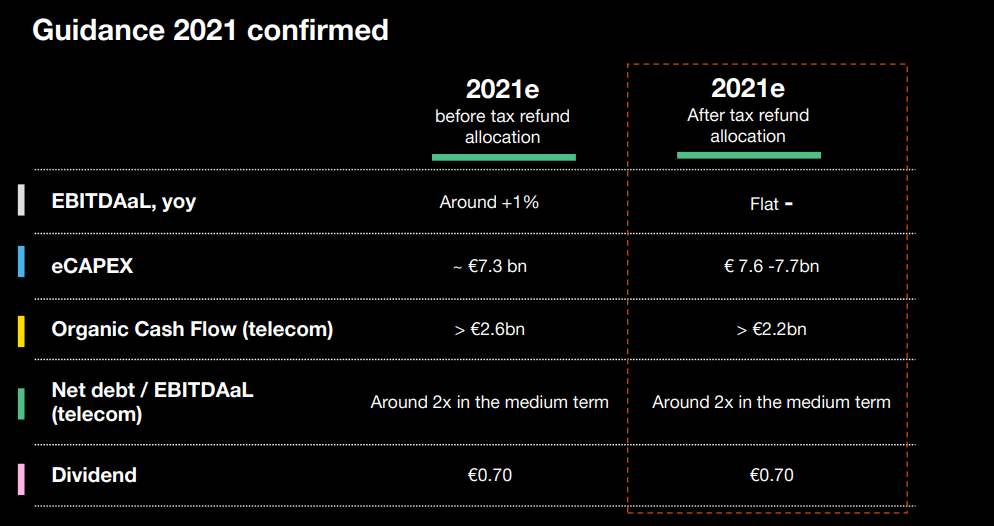

Orange has also given us guidance for 2021 - 2 different ones, where one includes a tax refund.

(Source: Orange)

While some may say this is not good enough, I consider this guidance and the numbers therein to be an important stepping stone to moving forward here. The company has clear growth plans to growing future EBITDAaL, growing Europe, growing IT and Cyberdefense, and Orange has a solid plan for its future infrastructure development.

(Source: Orange)

If it wasn't for the impairment, the company's results wouldn't have been solid only on the basis of certain key metrics, but most. The post-COVID acceleration of sales is confirmed, and the B2B appeal is also confirmed.

Let's look at valuation here, the key to the thesis.

Orange - What is the valuation?

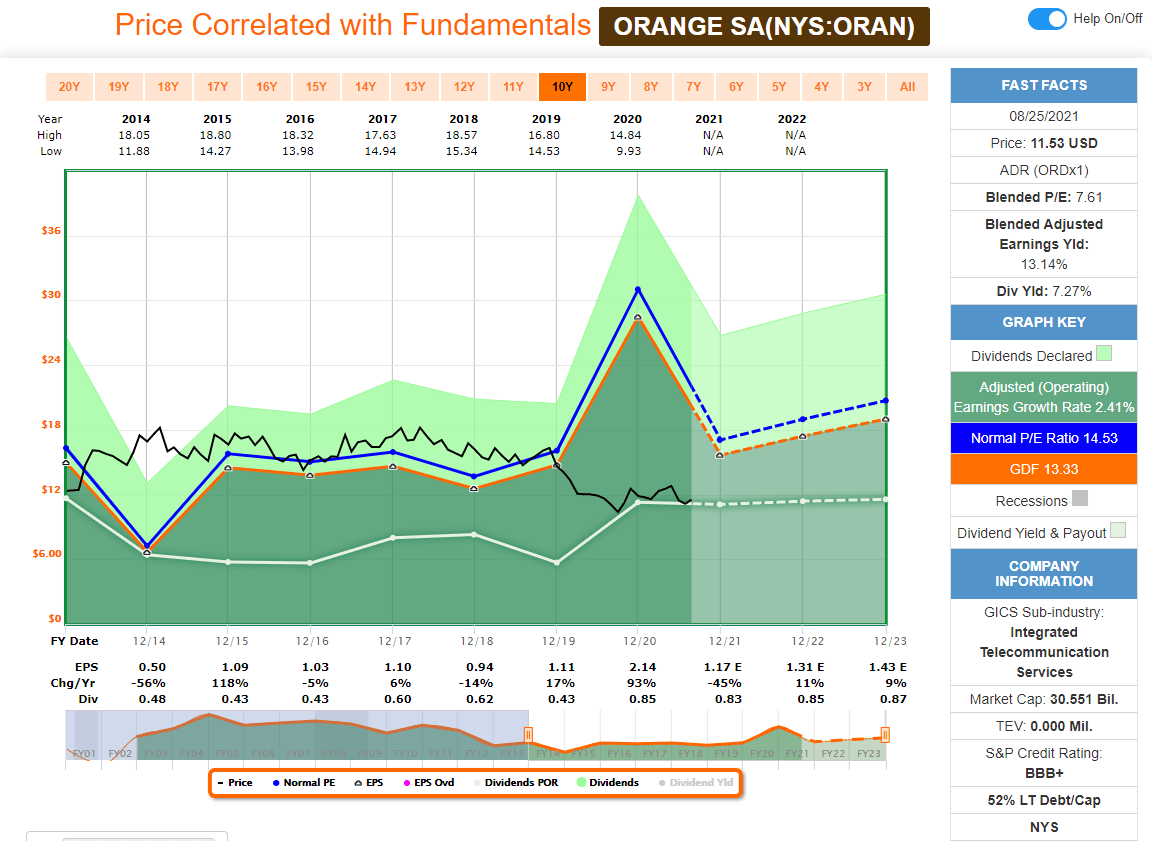

When I wrote about Orange I made it clear that the reason I thought it appealing was that the market is pricing what the company owns and operates at far too cheap a mark. I still hold this stance, perhaps more than before.

(Source: F.A.S.T. Graphs)

While it's true that the company is likely to see continued challenges for years, there are a few things, that to my mind, are not in question. The company's dividend is one of those things. I view Orange very similar to an appealing bond, a set-and-forget sort of investment that will generate around 8% to me per year. The difference is that this investment has the very real potential of generating triple-digit returns in a relatively short time frame based on a valuation reversal when things return to relative normalcy.

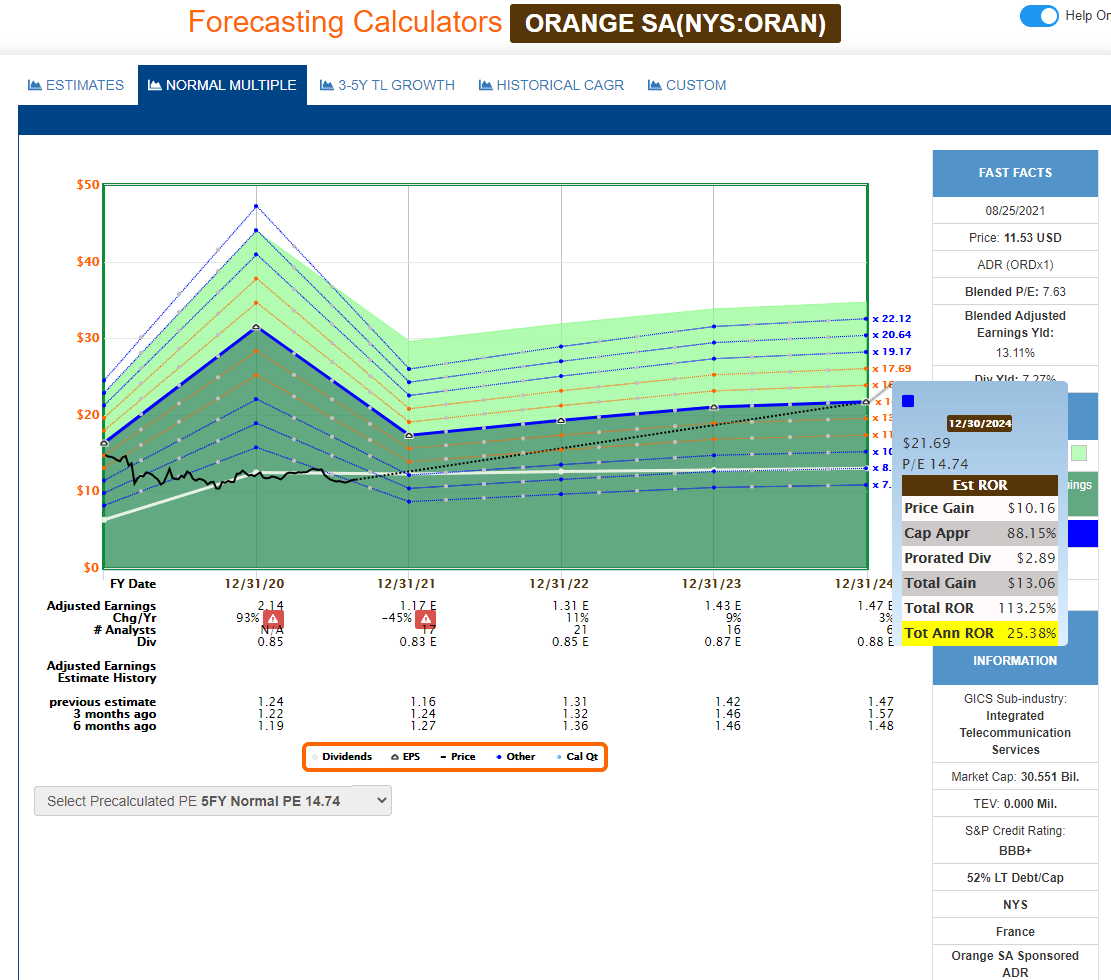

(Source: F.A.S.T. Graphs)

I will be the first to tell you that these estimates aren't worth much, given the near-zero percentage of accuracy these forecasts have historically held. It's almost better if FactSet analysts did not bother doing forecasts here, given how off the mark they usually are.

However, what's clear to me is that this company will continue to pay out dividends and retain its fundamental appeal - its customer base and network - even during times of trouble such as now.

Telecommunication investments to me are investments focused on a higher sort of yield and relatively low rates of growth - similar to utility investments. Over the course of years, these investments are responsible for nearly 13% of my annual dividends, and that is at a significantly higher Yield on invested capital than the overall average YoC of my portfolio. It's a conscious decision to aim a part of my portfolio at higher relative yields with less capital, in order for me to allow low-yielding high-growth stocks to do "their" thing, yielding less than 2-3% but growing that dividend in double-digits. To me, both investments have their place.

In very few places on the market can you buy an undervalued, well-covered 7-8% yield that's based on telecommunication revenues, an area which barring a societal breakdown will neither slow down nor collapse. That is the basis for my investment here, and fully acknowledging the associated volatility we're seeing in the company here. Over the course of years, it's entirely possible that the company will go far lower - as well as going far higher. In the end, I believe the changes the company is making will eventually push things back to normal. I remind you that less than 2 years ago, the price for this company was a 15x P/E, which seems almost inconceivable at this time.

However, that's the way valuation works. When companies are beaten down, we cannot even fathom them rising, and when they're riding high, we cannot fathom them falling. When it comes to this, I try to be as contrarian as an investor as I possibly can.

Analyst targets for this company that aren't FactSet would agree.

(Source: S&P Global)

While I wouldn't necessarily put much stock in the degree of undervaluation, I would argue that the overall direction is correct - that the company is, at this point, in fact, undervalued. This is the stance I would argue that investors overall need to take when looking at this company. Do not try to focus too much on where you think the company will be in 1-2 years - but rather focus on the well-covered yield, covered by extremely conservative and fundamental cash flows, as well as what you're paying for what you get.

Eventually, things will reverse - but there's little telling exactly how long that may take.

Thesis

My current stance on Orange is:

- This is one of the safer Telcos that you can currently buy and at an amazing discount. I view it actually better than AT&T.

- There's no telling then the company will revert to a more standard level of valuation - it could take 1 year, it could take 10.

- Until such time, your returns are well-covered with the high dividend, and there are plenty of growth ambitions and projects that look as though they have the potential to generate a further return for the company.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

This process has allowed me to triple my net worth in less than 7 years - and that is all I intend to continue doing (even if I don't expect the same rates of return for the next few years).

If you're interested in significantly higher returns, then I'm probably not for you. If you're interested in 10% yields, I'm not for you either.

If you however want to grow your money conservatively, safely, and harvest well-covered dividends while doing so, and your timeframe is 5-30 years, then I might be for you.

Orange S.A. is currently in a position where #1 is possible in my process, through #3 and #4. It's a "BUY".

Thank you for reading.