As mortgage banking income currently makes up more than half of Meridian Corporation's (NASDAQ:MRBK) total revenues, the eventual normalization will deal a significant blow to the bottom line. On the other hand, continued loan growth will likely support earnings. Overall, I'm expecting Meridian to report earnings of $1.81 per share in the second half of 2021, taking full-year earnings to $4.79 per share. The December 2022 target price suggests a limited upside from the current market price. As a result, I'm adopting a neutral rating on Meridian Corporation.

Mortgage Banking Normalization Pivotal in Determining Earnings Outlook

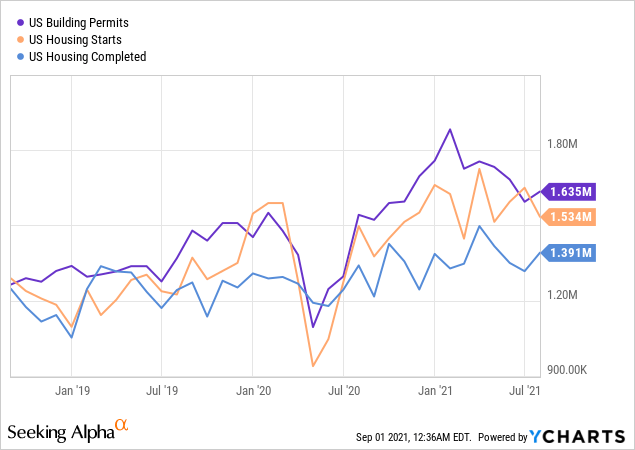

Meridian's jump in earnings last year was largely attributable to heightened mortgage banking activity. Over the next few quarters, mortgage refinancing activity will decline towards a normal rate because stable interest rates will diminish the benefit of refinancing. Further, new residential construction is already showing signs of losing steam. As shown below, permits, starts, and completions were all down after peaking earlier this year.

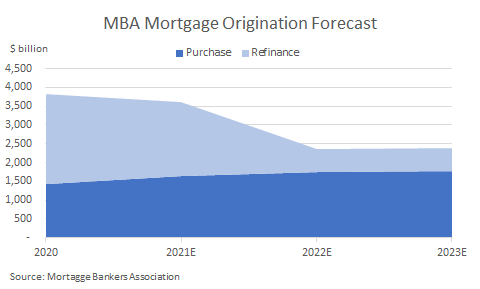

Mortgage banking income made up more than half the total revenues for the second quarter of 2021. As a result, the eventual normalization will have a significant impact on Meridian's bottom line. The Mortgage Bankers Association ("MBA") expects the refinance activity to normalize by next year, as shown in the chart below.

Considering the current economic environment and MBA's expectations, I'm assuming Meridian's mortgage banking income will trend downwards linearly to a normal level through the end of 2022.

Growth of Loans Held for Investment to Ease Pressure on the Bottom Line

As mentioned in the second quarter's investor presentation, loan growth for the June-ending quarter was an impressive 4%, excluding the impact of Paycheck Protection Program ("PPP") loans forgiveness. The loan growth trend has remained positive through a large part of the pandemic, which is encouraging. Further, I'm optimistic about future loan growth because of the anticipated economic recovery in Meridian's markets in Pennsylvania, New Jersey, Delaware, and Maryland.

However, the upcoming forgiveness of PPP loans presents a considerable threat to loan growth. According to details given in the presentation, PPP loans made up a massive 13.8% of total loans at the end of the last quarter. I'm expecting most of these loans to get forgiven before the end of this year, which will limit loan growth. At the time of forgiveness, Meridian will book the remaining unamortized fees, which will support net interest income. Therefore, the impact of loan decline on net interest income will become apparent in the quarters following the forgiveness.

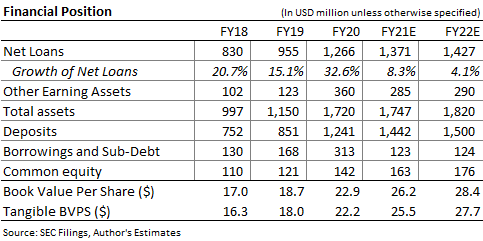

Considering the factors mentioned above, I'm expecting the loan portfolio to increase by 2.0% by the end of December 2021 from the end of March 2021. For 2022, I'm expecting loans to grow at a below-normal rate due to the remaining PPP forgiveness and impact of the pandemic. Meanwhile, I'm expecting deposits to grow in tandem with loans through the end of 2022. The following table shows my balance sheet estimates.

Pressure on the average portfolio yield from low reinvestment rates will likely counter the impact of loan growth on the net interest income. Further, the funding cost will likely remain sticky. Meridian does have some certificates of deposits ("CD") totaling $54 million that will mature in the third quarter, as mentioned in the presentation. However, these CDs carried rates of only 0.41% as of the second quarter. Even if the company replaces the maturing CDs with deposits that are carrying rates around 20 basis points lower, it will be able to reduce the average total deposit cost by only one basis point, according to my calculations.

Considering these factors, I'm expecting the net interest margin to decline by four basis points in the second half of 2021 from 3.75% in the second quarter. Based on the outlook for loan growth and margin compression, I'm expecting the net interest income to increase by 25% year-over-year in 2021 and 3% year-over-year in 2022.

Expecting Full-Year Earnings of $4.79 per Share

The anticipated decline of mortgage banking income will lead earnings downwards in the second half of the year. On the other hand, the anticipated loan growth will likely support the bottom line. Further, the provision expense will likely remain subdued as the existing allowances for loan losses are at an excessively high level relative to non-performing loans. Allowances made up 1.58% of total loans at the end of June 2021 while non-accrual loans made up just 0.55% of total loans. Nevertheless, I'm not expecting any significant reserve releases because active covid-19 related modifications are greater than allowances. Modifications made up 2.2% of total loans at the end of the last quarter.

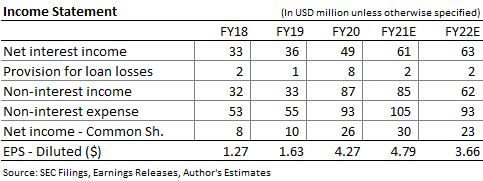

Overall, I'm expecting the company to report earnings of $1.81 per share in the second half of 2021, taking full-year earnings to $4.79 per share, up 12% year-over-year. For 2022, I'm expecting the earnings to decline by around 24% year-over-year because of the mortgage banking income normalization. The following table shows my income statement estimates.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to the COVID-19 pandemic, especially the Delta variant.

Current Market is Close to Next Year's Target Price

Meridian Corporation is offering a low dividend yield of 1.7% based on the current market price and the current quarterly dividend of $0.125 per share. The company also gave a special dividend of $1.0 per share earlier this year. If we include the special dividend, then Meridian is offering a high dividend yield of 5.1%. There is not enough historical data to tell whether or not the special dividend will be paid out every year. Therefore, I have excluded it from my investment thesis.

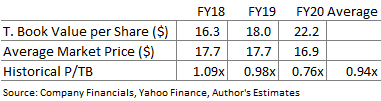

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Meridian. The stock has traded at an average P/TB ratio of 0.94 in the past, as shown below.

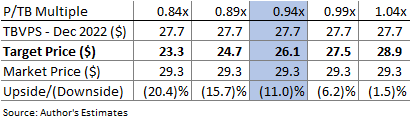

I usually use the earnings and book value estimates for 2021 to determine the stock's target price. However, in Meridian's case, I have decided to use next year's estimates because earnings will fall substantially in 2022. It doesn't make sense to give a higher target price for the end of 2021 when I know that next year's target price should be substantially lower. Multiplying the average P/TB multiple with the forecast tangible book value per share of $27.7 gives a target price of $26.1 for the end of 2022. This price target implies an 11.0% downside from the September 1 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

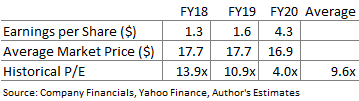

The stock has traded at an average P/E ratio of around 9.6x in the past, as shown below.

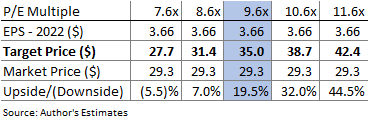

Multiplying the average P/E multiple with the forecast earnings per share of $3.66 gives a target price of $35.0 for the end of 2022. This price target implies a 19.5% upside from the September 1 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

Equally weighting the target prices from the two valuation methods gives a combined target price of $30.6, which implies a 4.3% upside from the current market price. Adding the forward dividend yield gives a total expected return of 6.0%. Hence, I'm adopting a neutral rating on Meridian Corporation.

The company's earnings are set to decline sharply next year because of the normalization of mortgage banking income. As the total revenue is heavily reliant on mortgage banking income, the normalization will have a significant impact. On the other hand, growth in loans held for investment will help the bottom line. As Meridian is currently trading near its target price, I would only consider investing in the stock if its price dipped by more than 10%.