Summary

Prometheus Biosciences (RXDX) is an early-stage drug development company bringing precision medicine to millions of patients with inflammatory bowel disease (“IBD”). The company is premised on the observation that moderate to severe IBD should be classified by disease severity (“which is often driven by genetics”) instead of disease activity (“the current standard”). Prometheus is taking a different approach based on its biobank and platform technologies to combine their therapeutics with companion diagnostics. The company went public in March 2021: Prometheus Biosciences Announces Closing of Initial Public Offering and Full Exercise of Underwriters' Option to Purchase Additional Shares

The company’s platform, Prometheus360, combines drug development with companion diagnostics to identify patients more likely to respond to their therapeutic candidates. With this technology, Prometheus has built a diverse pipeline focused on IBD. The company’s lead asset, PRA023 is a humanized monoclonal antibody (“mAb”) that inhibits tumor necrosis factor-like ligand 1A (“TL1A”) for ulcerative colitis (“UC”) and Crohn’s disease (“CD”). The drug candidate is currently entering Phase 2 clinical trials focusing on patients with increased TL1A expression.

Prometheus is building the category-leading company for precision medicine and gastrointestinal (“GI”) disease. The platform has the potential to grow the company’s pipeline and likely will provide partnering opportunities down the line. Combined with this, PRA023 is a compelling drug candidate pursuing two large markets with significant unmet patient need. In the United States, UC affects around 900K patients and there are around 1M CD patients. Moreover, the lead drug candidate already has past clinical validation by Pfizer (PFE) and has been established as safe so far in Phase 1 trials by Prometheus. However, the Phase 2 trial readouts for PRA023 are expected in late 2022; as a result, the company is a compelling opportunistic investment based on pipeline expansion and partnering opportunities.

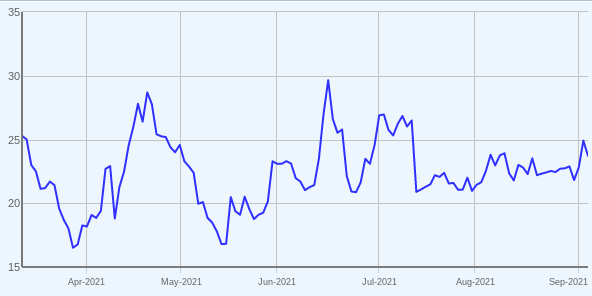

Figure 1: RXDX daily chart (Source: Capital IQ)

Opportunity

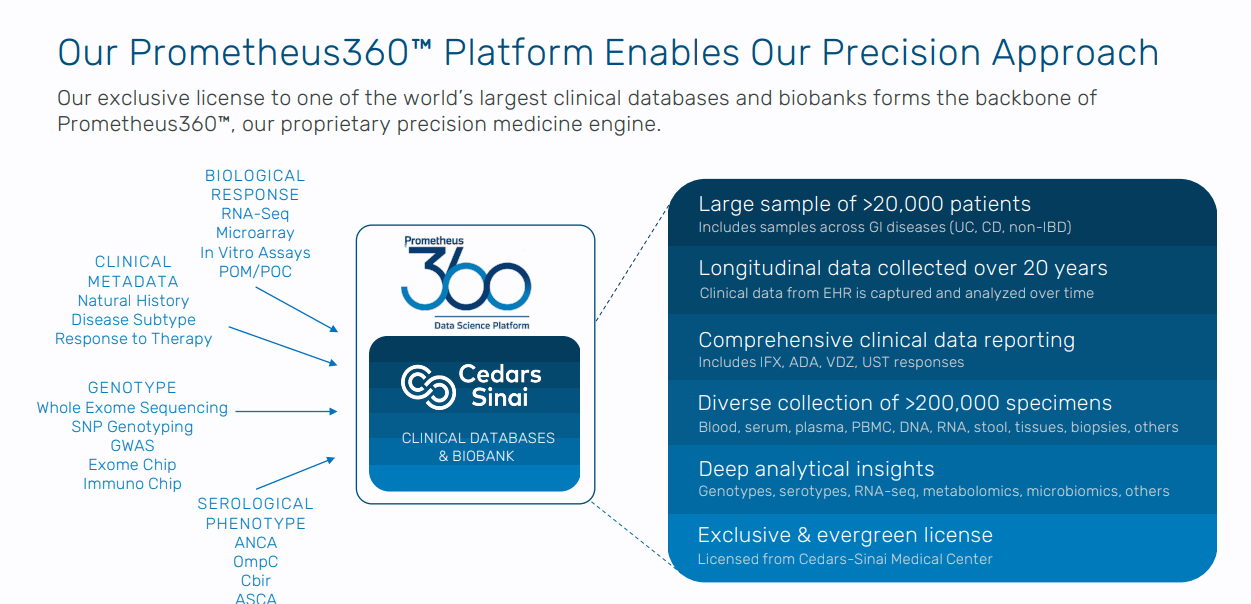

IBD affects around 2M people in the US and millions more around the world. As a complex disease, IBD has several contributing drivers from genetic to environmental that make the current standard-of-care treatments lacking. Typically, patients are given anti-TNF medicines as first line treatments. Then JAK inhibitors are the standard second line treatment for IBD patients. However, these drugs do not target fibrosis, which is a major part of IBD. Prometheus is a really unique business given the unprecedented scale of its biobank - over 200,000 samples exclusively licensed from Cedars-Sinai Medical Center from over 20,000 patients collected over the course of 2 decades or so. This is the largest biobank for GI disease. This positions the company to use this data to hone in on new mechanisms that drive IBD and develop new medicines pursuing them.

This data forms the basis of the company’s platform, Prometheus360. It is a discovery engine for new therapeutics and their corresponding companion diagnostics for IBD. In general, drug development for IBD can take more than a decade due to the difficulties of recruiting patients into trials based on undifferentiated mechanisms of action (“MoA”). Prometheus’ use of companion diagnostics allows the company to enroll a specific subset of IBD patients and accelerate clinical development with smaller trials. This creates a wide set of advantages for the company:

Increasing the likelihood of trial success by matching a drug to a patient more likely to respond to it.

Help Prometheus have a stronger position for label claims for reimbursement and use.

Accelerate development of the company’s pipeline.

As a result, Prometheus is building an IBD drug pipeline in an entirely new way when compared to incumbents. Rather than take a one size fits all approach, the company is working to improve decision making in the clinic and improve patient outcomes and responses. For the former, Prometheus can help gastroenterologists use their therapies based on individual factors like inflammation and genetic background. For the latter, the standard of care in IBD rarely exceeds a 15% remission rate versus the placebo and a good portion of these patients will lose their responsiveness over time. Prometheus’ use of precision medicine will drug the biological basis of IBD to work to improve patient response rates.

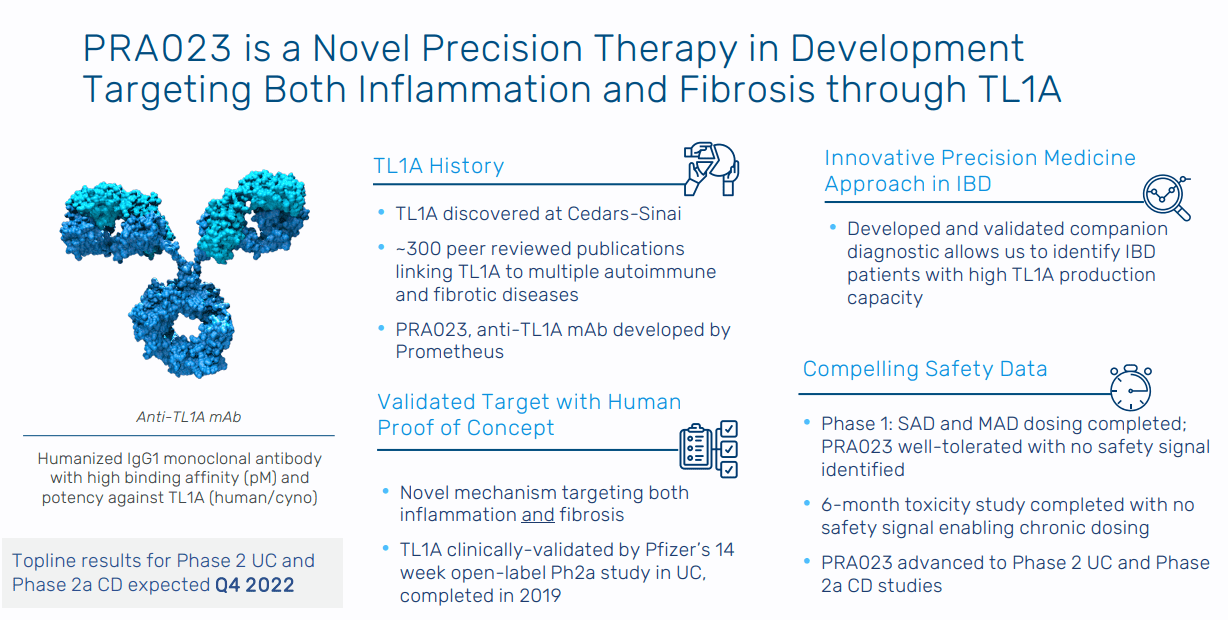

PRA023 is the company’s lead asset. It is an IgG1 humanized monoclonal antibody that inhibits TL1A, which is expressed in around 30% of IBD patients. In a Phase 2a trial conducted by Pfizer in 2021, TL1A was established as a viable target for UC. In the study, over 14 weeks, 38% of patients (“n=50”) with moderate to severe ulcerative colitis receiving an anti-TL1A antibody had an endoscopic improvement compared to 6% for the historic placebo rate with 24% of patients overall getting to clinical remission (“total Mayo score”):

This study clinically validates TL1A but leaves a lot of room for Prometheus to improve upon these results. The Pfizer study had 3 adverse events in patients; as a result, Prometheus has designed PRA023 with a new epitope that more potently binds TL1A to reduce off target effects. The company initiated a Phase 1 clinical trial for the drug candidate in UC and CD in December 2020: A Study of PRA023 in Healthy Volunteers - Full Text View - ClinicalTrials.gov

The clinical trial is expected to be completed in September 2021 with data announced thereafter. Depending on the safety readouts, Prometheus is expecting to start a Phase 2 trial this year with data expected in the second half of 2022. In conjunction with PRA023, the company is also developing a companion diagnostic test to identify patients who over-express TL1A and are more likely to respond to the treatment. Versus comparable medicines in UC and CD like Entyvio from Takeda (TAK) and Humira from AbbVie (ABBV), PRA023 addressed both inflammation and fibrosis.

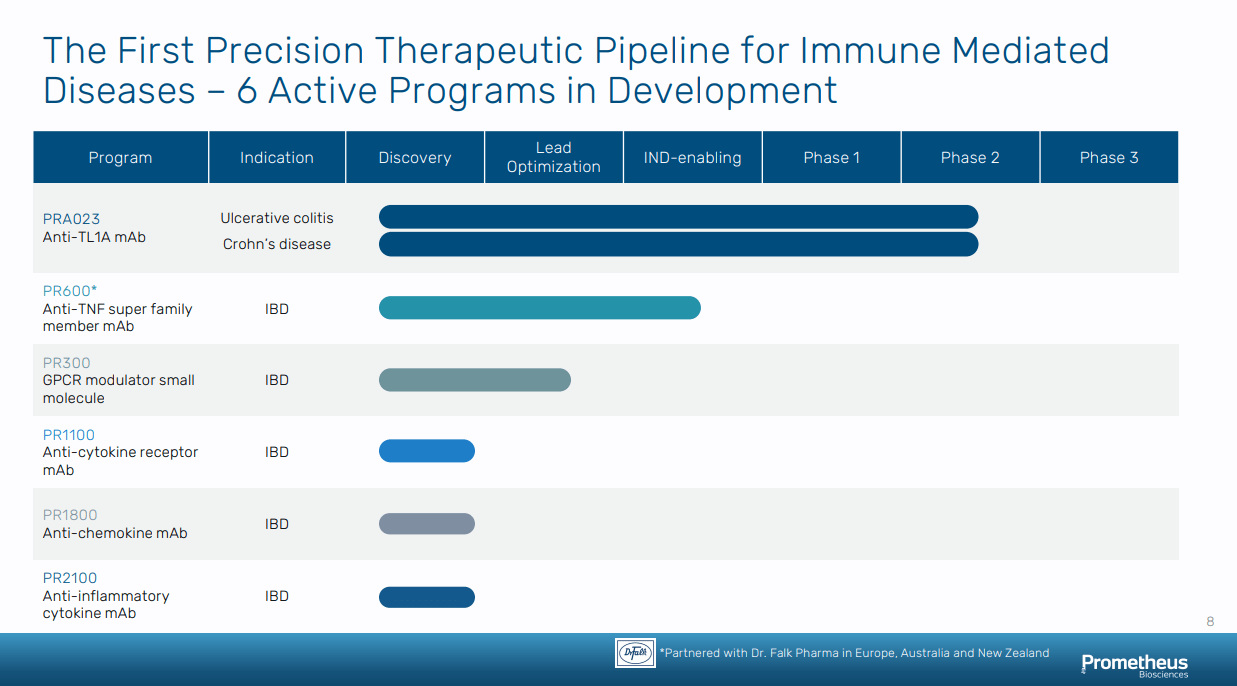

Beyond this lead asset, Prometheus has built a diverse pipeline pursuing several MoAs in IBD:

PR600: a monoclonal antibody that targets a member of the TNF superfamily that has been genetically linked to certain IBD subpopulations. With this candidate, Prometheus entered into a partnership with Falk Pharma giving exclusive commercialization rights in Europe, Australia, and New Zealand for their expertise in manufacturing and GI disease. PR600 is expected to reach an investigational new drug (“IND”) application in the second half of 2022.

PR300: a small molecule that targets an orphan G-protein coupled receptor (“GPCR”) overexpressed in the GI tract who has single nucleotide polymorphisms (“SNP”) linked to UC.

PR1800: a monoclonal antibody targeting a protein involved in chemo-attraction of inflammatory cells in the GI tract.

PR2100: also a monoclonal antibody that targets a cytokine connected to fibrosis in IBD.

This pipeline is enabled by the platform and gives Prometheus the optionality to engage in partnerships and other deals. For example, the company has a strategic collaboration with Takeda to develop a companion diagnostic for therapies in UC and CD that Takeda develops: Prometheus Biosciences, Inc., Enters Into Multi-Target Strategic Collaboration with Takeda to Develop Targeted Therapies for Inflammatory Bowel Disease

All in all, Prometheus has 3 main moats: its biobank, clinical data, and the ability to convert these discoveries into drugs. The company has the largest biobank of IBD samples in the world. On top of this, Prometheus has access to an unprecedented amount of clinical data from IBD patients from electronic medical records, imaging data, pathology slides, among others. In particular, having access to longitudinal data and well annotated patient samples is a powerful advantage.

Finally, the company can use this data to uncover new biological pathways that drive IBD, which sets up Prometheus360 to find new drug targets and develop the right therapeutic/diagnostic combinations for specific IBD subpopulations. Importantly, no drug in IBD has been approved with a companion diagnostic that can predict if the patient will respond to the therapeutic. Other companies could try to replicate this model with publicly available data that is not standardized enough to generate useful insights or create their own data, which is prohibitively costly.

This is what makes Prometheus’ exclusive access to patient data from Cedars-Sinai incredibly valuable. With this platform and pipeline, the company can develop IBD therapies with new targets, make these medicines more precise and reduce trial & developmental costs, and lower the barrier for payor adoption by increasing patient outcomes.

Figure 2: Prometheus’ pipeline (Source: Prometheus Biosciences’ corporate presentation)

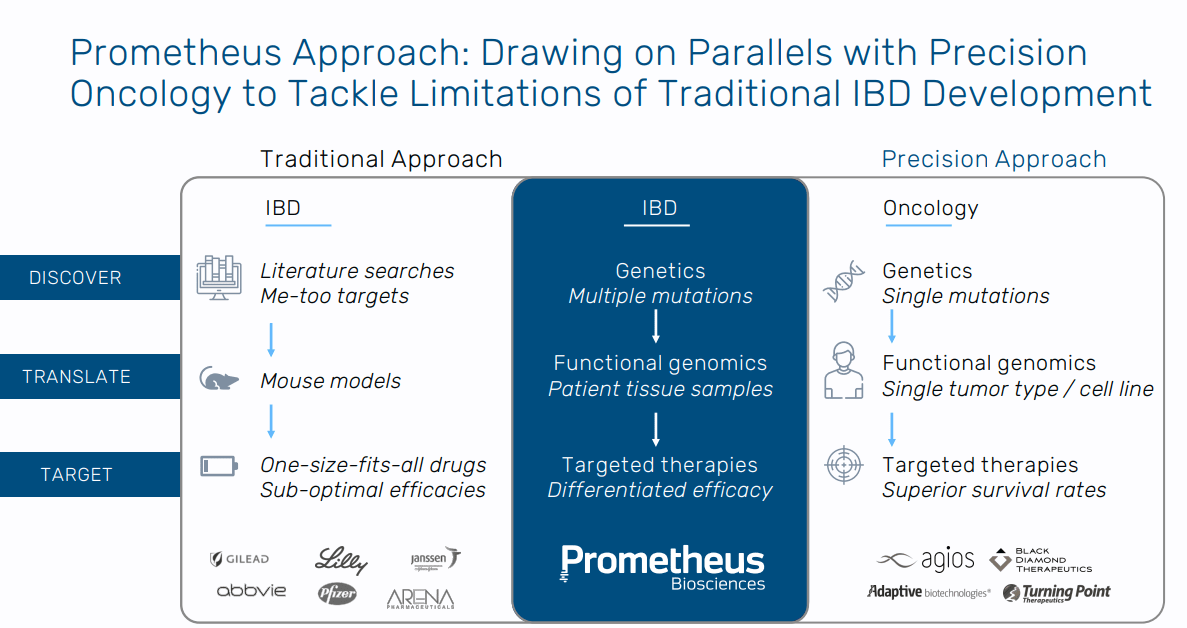

Figure 3: Taking inspiration from precision medicine in oncology for IBD (Source: Prometheus Biosciences’ corporate presentation)

Figure 4: Overview on the Prometheus360 platform (Source: Prometheus Biosciences’ corporate presentation)

Figure 5: Overview on Prometheus’ lead drug candidate (Source: Prometheus Biosciences’ corporate presentation)

IBD represents over a million patients in the US and millions more around the world. However, drug development in the field has not evolved over the last 1-2 decades. This is mainly due to the complexity of IBD - it is chronic, frequently relapses in patients, and has several contributing factors from genetic and environmental to immunologic. There are a little under 1M UC patients in the US and over 1M CD patients. The standard of care focuses on managing inflammation but not addressing genetic drivers or fibrosis. With the top 4 drugs in IBD accounting for more than 75% of sales, Prometheus has a very large opportunity to bring new technologies and targets to bear in this market and quickly scale.

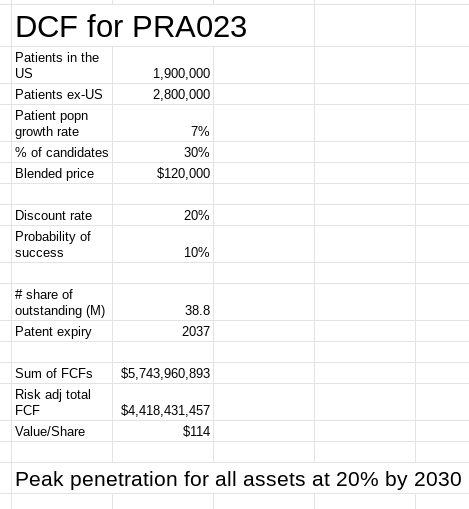

The valuation model for the company focused on PRA023, the lead asset, and assumed an FCF margin of 35%, discounting the company's ability to generate this cash flow from PRA023 over the lifetime of the product. The model also assumed a drug price of $120K. From this work, Prometheus Biosciences in my opinion is trading at a ~80% discount implied by the model.

Figure 6: Valuation of Prometheus Biosciences (Source: Author's valuation work, using base data from RXDX’s 10-K)

Ultimately, Prometheus is building a category-leading company in IBD. This disease lies on the interface of genetics, the environment, and the microenvironment in the human gut spanning bacteria, fungi, and viruses. The last real innovation in the field was in 1998 with the first approval of an anti-TNF therapy for CD. Overall, patients with IBD are categorized into 2 main treatment regimens: induction or maintenance.

For the former, the goal is to reduce inflammation and the latter, to maintain this reduction after ~3 months. But the current standard of care does nothing to attack the key drivers of IBD and potentially reverse scarring in the GI tract. This has led to a large portion of IBD patients, 15% in UC and 50% in CD, requiring some sort of surgery within a decade of their diagnosis. Prometheus has built a platform to ingest genetic and clinical data to move beyond the one size fits all paradigm and start taking into account biological variation in IBD patients when developing new medicines.

Figure 7: Opportunity to bring precision medicine to gastrointestinal disease (Source: Prometheus Biosciences’ corporate presentation)

Catalysts

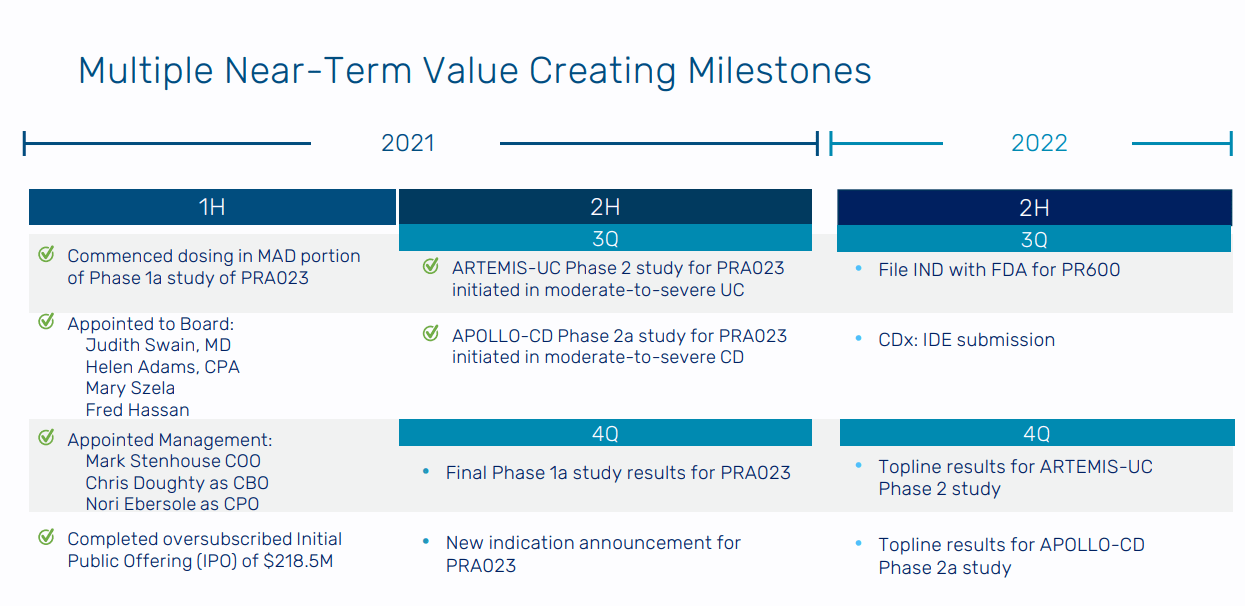

Prometheus is expected to start a Phase 2 study for PRA023 in UC and CD by the end of 2021. Over the next 3 months or so, this is the most important event for the company’s stock price. Prometheus is also expecting to report Phase 1 data for PRA023 later this year as well, and the Phase 2 trial is dependent on the success of the Phase 1 study. If there are any safety issues, which did come up in the Pfizer study but not in Prometheus’ pre-clinical models, the company’s stock price would face major headwinds. With around $300M, the company has several years of runway to grow their platform and business.

Moreover, in 2022, Prometheus is expecting to file an IND for PR600 and file for a clinical study of their companion diagnostic to put together with PRA023. Pending the Phase 2 trial being initiated, the company is expecting Phase 2 readouts for PRA023 by the end of 2022. Also, the company has a powerful platform so partnerships and other forms of business development would be a positive catalyst.

Figure 8: Prometheus’ catalysts (Source: Prometheus Biosciences’ corporate presentation)

Risks and Challenges

The main risk right now for Prometheus is the upcoming Phase 1 results for PRA023. If the drug candidate is established as safe, the company will meet a major milestone and have a clear path to start a Phase 2 trial. If adverse events are reported or early response rates come in below ~15%, Prometheus will likely have to go back to the drawing board and delay several important events by 2-3 years.

Moreover, there is a market risk for the company - given the focus on defined populations in IBD, the patient populations could be smaller than expected and reduce the total addressable market for Prometheus’ pipeline. Another risk could be competition - IBD is very crowded with several approved drugs and a lot more in development; however, Prometheus’ technology and focus on unique MoAs gives it a strong advantage in this type of environment.

Conclusions

Prometheus is a one of a kind biotechnology company in IBD. By combining precision medicine with a proprietary data set, the company has built a promising pipeline of drug candidates. The next 3 months with PRA023 will be exciting and a major point to either validate their technology or not. But there is so much need in IBD - the current treatments are like hammers looking for a nail, while the drugs Prometheus is developing are fitted for specific patients.

The company has a lot of work left to do but has built a compelling platform and business model that has a chance to transform the ~$10B IBD market. Overall, the company is also a case study of finding areas of drug development that have not been impacted by precision medicine. There are large opportunities to bring the toolkit to diseases in autoimmunity, kidney disease, fibrosis, aging, and dermatology.

The thesis to invest in Prometheus is premised on the following:

The company’s compelling platform and data that has enabled substantial partnerships, a diverse pipeline, and non-dilutive capital.

The magnitude of the IBD market opportunity, which has had little innovation over the last 2 decades.

Prometheus has an upcoming catalyst over the next few months with Phase 1 data coming out for its lead asset that can set up a Phase 2 clinical trial.