ClarkandCompany/E+ via Getty Images

Source: Company

Summary

Homology Medicines (FIXX) is a gene therapy and editing platform company centered around hematopoietic stem cells (“HSC”). The investment thesis for Homology builds on top of past analysis on Orchard Therapeutics (ORTX) to use HSCs to potentially cure immune-related disease - Orchard Therapeutics: For Immune-Related Disease (NASDAQ:ORTX)

Homology’s technology is based on adeno-associated virus (“AAV”) capsids from HSCs calling them AAVHSCs. Homology has a library of 15 novel AAVHSCs to build an advantage around gene correction: replacing entire, mutated genes with a functional copy while relying on natural DNA repair machinery. The biological premise is that AAVHSCs have tropism for several tissues from the muscle and liver to the retina. Importantly, these vectors can cross the blood-brain barrier (“BBB”) and deliver genetic cargo to the central nervous system (“CNS”). This allows AAVHSCs to act as a platform technology for in vivo delivery and gene editing across a wide range of diseases. One caveat is that Homology’s technology is probably only useful as a gene therapy. Homology has built a pipeline across several rare diseases with their lead asset focusing on phenylketonuria (PKU). However, the company has experienced COVID-related delays for their lead asset in phase 2 trials. There is an opportunity to buy Homology’s stock in preparation for the clinical trial coming back online. This is a similar thesis as Alector (ALEC) - Alector: Activating Microglia To Treat Neurodegeneration (NASDAQ:ALEC), which had a trial delay from COVID as well and experienced a significant gain in stock price after the company was able to get the trial back on track. Given the technology advantages for Homology and the promise of their lead asset, we recommend a core investment with a resumption of the clinical trials for the company’s lead drug candidate.

Figure 1: FIXX daily chart (Source: Capital IQ)

Opportunity

Homology’s use of AAVHSCs is focused on safer gene editing and therapies. The technology uses natural homologous recombination to edit genes rather than a nuclease itself. As a result, Homology’s pipeline of gene therapies is biologically possible whereas the gene editing data is less conclusive mainly because more evidence is needed on whether an AAV alone can mediate gene editing. The opportunity set for a gene therapy in PKU is large enough in combination with a stock price hit for COVID related trial delays and push back on the gene editing claims for Homology, to make the investment exciting with a margin of safety and obvious catalyst with the lead trial.

For HMI-102, Homology has reported initial data from the phase 1/2 trial in late 2019. The trial established safety so far; however, the results were not promising. In cohort 1, the two patients showed no efficacy signal from the therapy while one patient out of two that was reported in the second cohort had some weaker than expected response. The main catalyst for the investment is not more data from this trial but just a resumption of it. Homology’s lead asset is pursuing a large market opportunity with a strong comparable. HMI-102 is an AAVHSC15 that delivers a normal version of the phenylalanine hydroxylase gene along with a liver-specific promoter. And phenylketonuria (“PKU”) is a rare disease caused by mutations in the phenylalanine hydroxylase (“PAH”) gene. This leads to a buildup of phenylalanine (“Phe”) in patients leading to neurological damage and excess levels of tyrosine (“Tyr”). In pediatric patients, elevated Phe levels can lead to impaired brain development and long-term intellectual disabilities. The current standard of care for PKU patients do not treat the genetic cause rather rely on dietary restriction and lower production of Phe normalizing serum levels of the amino acid. BioMarin Pharmaceutical (BMRN) is the current leader in the field with two approved medicines: Kuvan (“can only treat ~10% of PKU patients”) and Palynziq. BioMarin has started a phase 1/2 trial for their AAV5 gene therapy in PKU, BMN 307 to replace the faulty PAH gene with a corrected version.

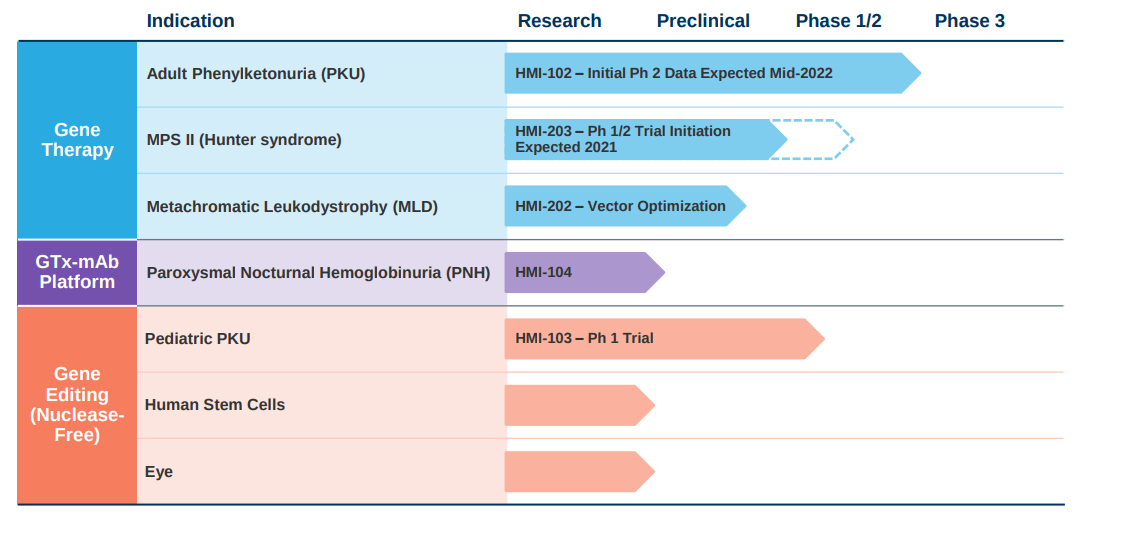

Beyond PKU, Homology has gene therapy programs in other rare diseases, Hunter’s syndrome and MLD, with the platform to develop candidates across a wide range of diseases and tissues. In preclinical research, the company has shown their library of AAVHSCs has biodistribution for the following tissues: central nervous system (“CNS”), bone marrow, eye, liver, lung, and muscle. This sets up Homology to build a pipeline and set of partnerships for their gene therapies for monogenic diseases across these tissue types. From a strategic perspective, Homology has communicated that they want to keep programs for intracellular, inborn errors of metabolism for gene therapy while using their gene editing technology, which in our opinion is still speculative, for CNS, liver, and bone marrow. From our perspective, depending on the readout of HMI-102, Homology could use their gene therapy technology to partner with larger companies and build a licensing business model similar to REGENXBIO (RGNX). However, the investment opportunity in Homology is premised on the lead trial coming back online.

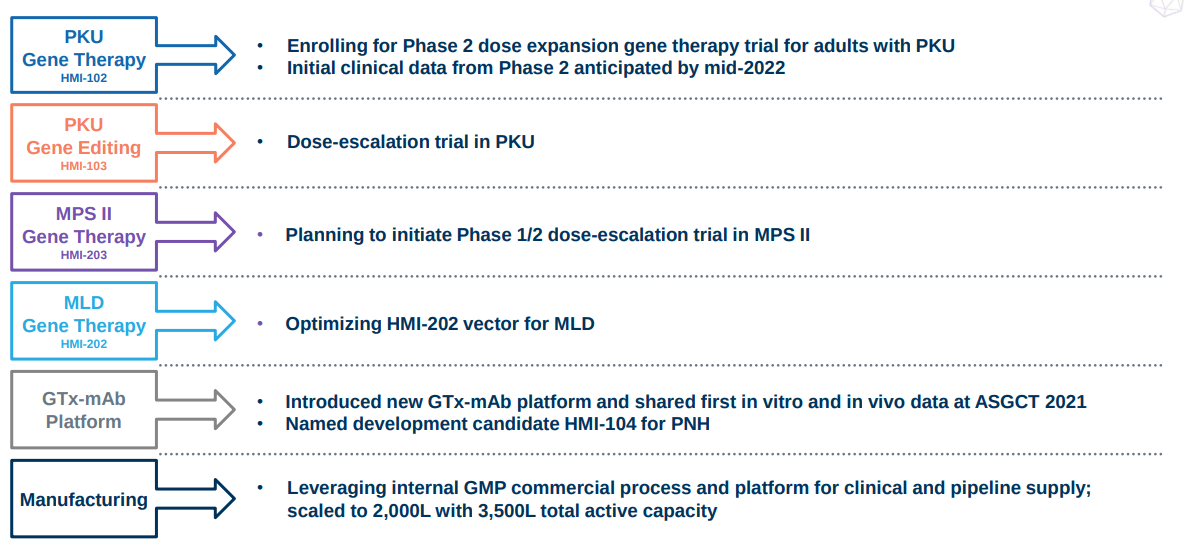

Figure 2: Homology’s pipeline (Source: Homology Medicines corporate presentation)

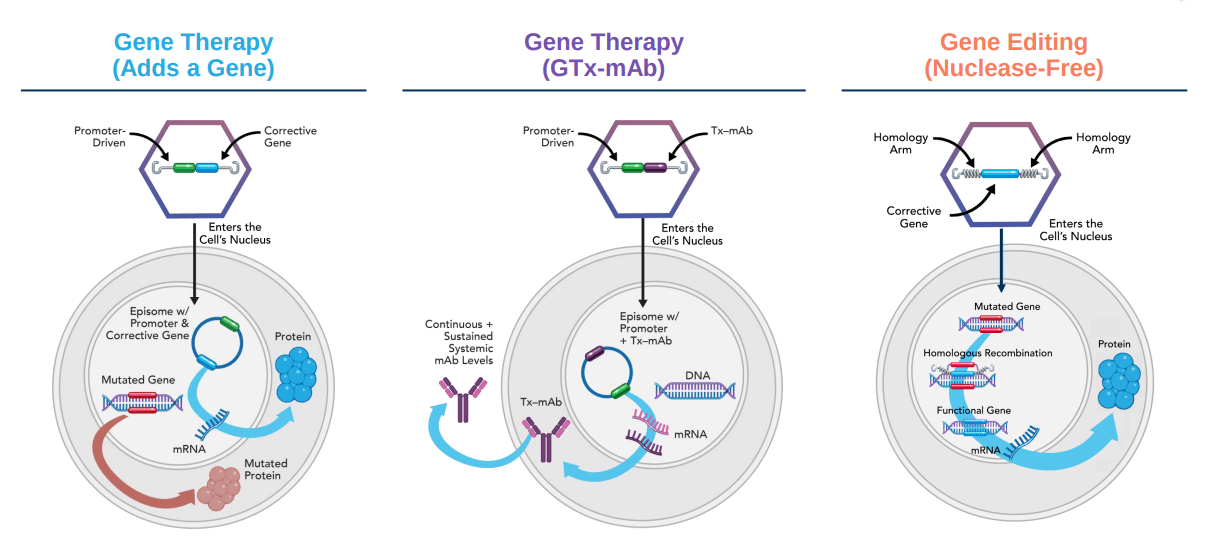

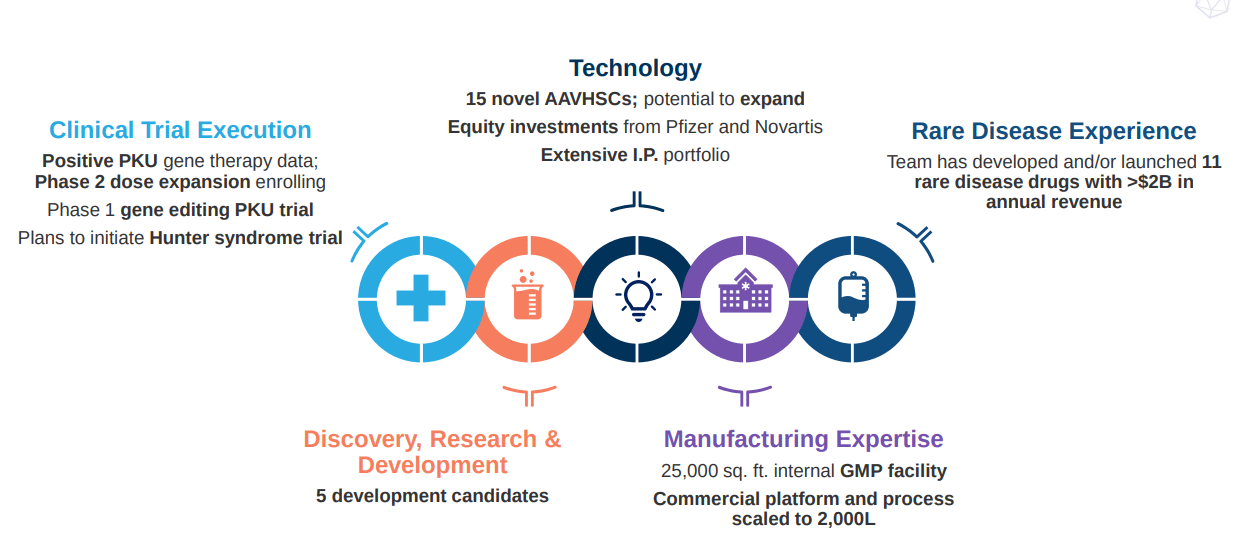

Figure 3: The three platform technologies underpinning Homology’s pipeline (Source: Homology Medicines corporate presentation)

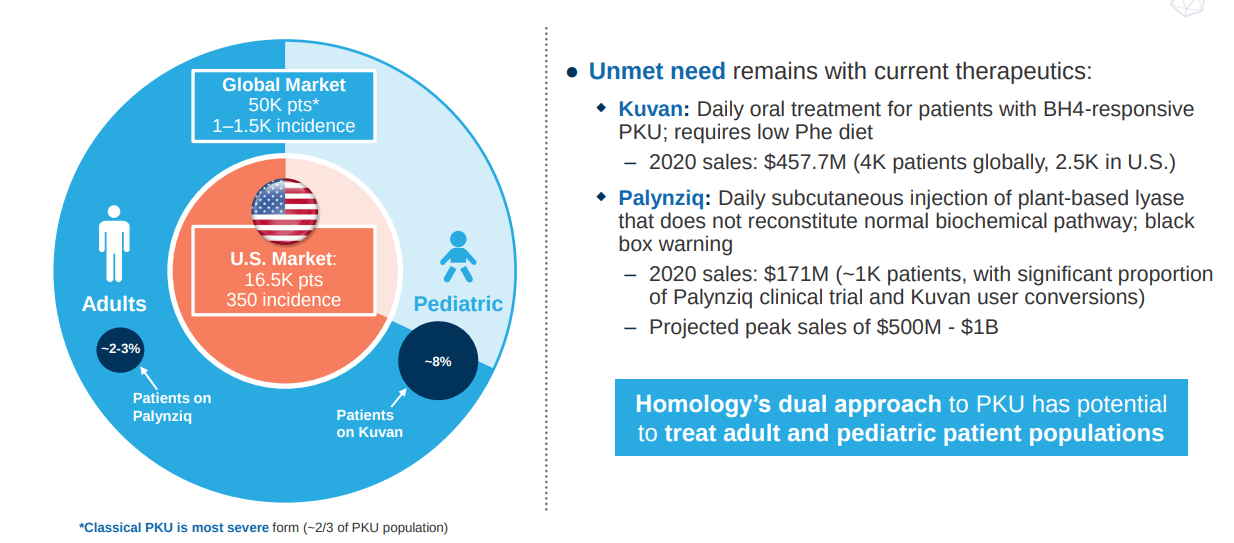

Figure 4: Market opportunity in PKU (Source: Homology Medicines corporate presentation)

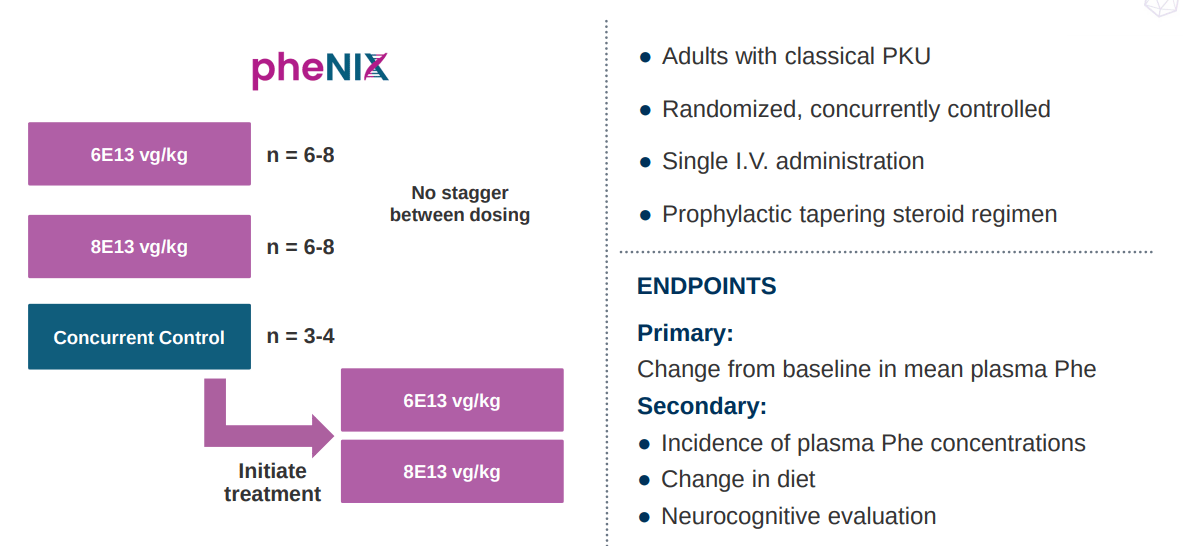

Figure 5: Clinical trial design for Homology’s lead drug candidate, HMI-102 (Source: Homology Medicines corporate presentation)

PKU is a genetic disease affecting around 16.5K patients in the US and over 70K patients around the world. Around the 1960s, newborn screening for the disease was started due to PKU’s massive negative effects on childhood development. Right now, the disease is managed with Phe-restricted diets powered by medical foods and approved medicines that reduce Phe production. So the opportunity for Homology, BioMarin, among others is to potentially cure this disease with a gene therapy and help patients a lifelong experience of restricted diets and chronic treatments.

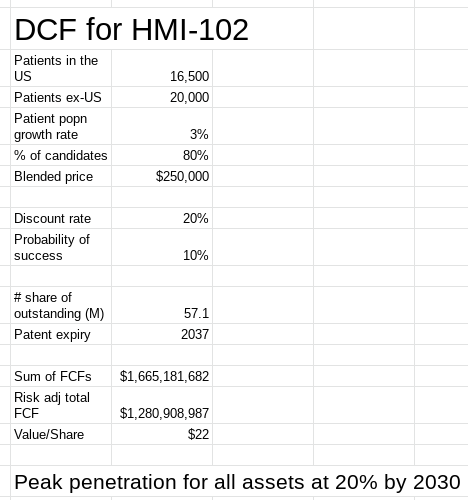

The valuation model assumes an FCF margin of 35%, discounting the company's ability to generate this cash flow from HMI-102 over the lifetime of the product. The model also assumed a drug price of $250K comparable to the annual price of Palynziq. From this work, Homology Medicines, in my opinion, is trading around a 3x discount to its current market value. The current investment thesis is premised on the HMI-102 trial completing its enrollment and no longer being delayed by COVID. This is the main catalyst to close the valuation gap but by no means is the opportunity right now focused on Homology reaching this estimated valuation. Instead, this valuation conveys a margin of safety given the market potential of Homology’s lead asset. As a result, the thesis for the stock has to be revisited once the lead trial is put back on track.

Figure 6: Valuation of Homology Medicines (Source: Author's valuation work, using base data from FIXX’s 10-K)

Homology has developed a unique set of gene therapies and gene editing tools, with their 15 AAVHSCs. The data in clinical trials still need to come out to validate this platform. In our opinion, the opportunity in gene therapies is large enough to warrant a compelling window to buy Homology’s stock. Once HMI-102’s trial is resumed, the company’s valuation is likely to close the gap with our internal valuation. If the PKU trial shows some level of success, Homology could execute non-dilutive partnerships for the AAVHSC platform and execute a rare to common drug development strategy to expand to diseases with larger patient populations.

Figure 7: Opportunity for Homology to use its gene editing technology in PKU and other rare diseases (Source: Homology Medicines corporate presentation)

Catalysts

The main catalyst for our thesis is the resumption of normal enrollment for the phase 2 clinical trial of HMI-102. Homology’s management has been communicating top line data from this trial; is expected sometime in 2022. As a result, we are expecting the trial to resume enrolling sometime between now and ~mid-2022. The opportunity is for this event to have a positive impact on Homology’s stock price in face of controversy over its gene editing technology claims and the lead trial delay. The data release for HMI-102’s phase 2 will come well after the thesis for this investment plays out.

Importantly, Homology is only initiating trials for other programs, which should not interfere with the thesis and potentially present negative data along the way. Moreover, the company might have announcements around new technologies and potential partnerships that would act as minor positive catalysts. Homology is also building out internal biomanufacturing capabilities, which will be important for the long-term value of the business: the process is the product for cell and gene therapies.

Figure 8: Homology’s catalysts across its pipeline and platform (Source: Homology Medicines corporate presentation)

Risks And Challenges

The main risk for the investment in Homology is a long-term delay for the lead phase trial well into 2022. The longer it takes for the phase 2 trial to enroll, the more time for Homology to announce data that could negatively impact its stock price or external events related to gene therapy and editing to bring down the whole sector. The company’s lead asset is competing head to head with BioMarin in PKU. The latter has a lot more resources than Homology. Given that BioMarin has 2 approved medicines that are the standard of care for the disease, Homology’s lead asset has a much higher bar to show non-inferiority to justify an equal or likely higher price for a potentially curative treatment. However, these risks will be assessed after the lead trial is resumed.

Conclusions

Homology has built out a unique gene therapy platform with a lead asset in PKU. The latter is entering phase 2 clinical trials after mediocre phase 1 results that at the very least established safety. The investment thesis is that COVID-related delays for the lead trial among other things have negatively impacted Homology’s stock price and a resumption of this clinical trial will act as a positive catalyst.

Homology’s platform of AAVHSCs is a unique series of viral vectors for in vivo treatments of monogenic diseases. For gene therapy applications, AAVHSCs are packaged with a copy of a functional gene along with a cell specific promoter to express the gene without integrating into a patient’s genome. Data still need to come out on the technology, particularly HMI-102, but the premise is that these vectors have advantages over other AAVs for their ability to target a wide range of tissues and treat more patients given the lower prevalence for AAVHSCs versus other vectors already in use. In our opinion, there is potential for Homology to bring gene therapy to larger indications and ideally pursue these programs with partners, given these advantages.

The lead asset’s, HMI-102, phase 1/2 data was well below expectations in terms of efficacy but showed safety in 4 patients. However, the market opportunity for PKU in combination with the poor standard of care still makes HMI-102 a compelling asset. With Homology’s asset and BioMarin’s program being the 2 lead gene therapies in clinical trials for the disease, our thesis is that enrollment for HMI-102 will close the valuation gap in the short term. Long-term success is more uncertain given if HMI-102 can show better efficacy in a larger trial or if BioMarin reports strong data that blows Homology out of the water in PKU. For the disease, Kuvan is a synthetic version of BH4, a cofactor important for PAH activity and the idea is that the drug increases the metabolism of Phe. This medicine generates $100M in annual sales but still requires patients to have a low Phe diet. The other therapy on the market is Palynziq; is a phenylalanine ammonia lyase that breaks down Phe and has similar limitations as Kuvan. Homology’s gene therapy can potentially be curative and help patients avoid current dietary and lifestyle restrictions and capture the market value of currently approved PKU treatments.

For the investment in Homology, if the clinical trial comes back online in the next few months, the risks become the data readouts for HMI-102’s phase 2 trial. If the trial doesn’t resume in short order, then we recommend taking a neutral position and waiting for new data releases on the lead program - for this scenario, Homology will likely have partnering opportunities with its platform and an ability to pivot. But the opportunity here is short term with enrollment for the phase 2 trial with the option to monitor for events with a longer-term impact.

The thesis to invest in Homology is premised on the following:

The resumption of HMI-102’s phase 2 trial and completing enrollment ought to have a positive catalyst on Homology’s stock price.

HMI-102’s potential to replace the standard of care in PKU combined with the high unmet need make positive news on the trial likely to help Homology close its current valuation gap.

Depending on the timing of the lead trial, Homology has built out a unique gene therapy platform with the potential to expand to CNS disorders, ophthalmological diseases, lung diseases, and more.