arturogi/E+ via Getty Images

Author's note: This article was released to CEF/ETF Income Laboratory members as part of the CEF Weekly Roundup on October 25, 2021.

MXE's offering concludes

The Mexico Equity and Income Fund (MXE) has announced the results of its rights offering, which expired on October 8, 2021. From the press release:

The Mexico Equity and Income Fund Announces Expiration of Rights Offering

October 12, 2021 03:17 PM Eastern Daylight Time

NEW YORK--(BUSINESS WIRE)--The Mexico Equity and Income Fund, Inc. (“the Fund”) (NYSE: MXE) announced today that its non-transferable rights offering to purchase additional shares of its common stock expired on October 8, 2021.

The Subscription Price was $8.90. The Fund has elected to fulfill all subscription requests by Rights Holders. Since the Subscription Price is greater than the Estimated Subscription Price of $11.13, refunds will be made to those Rights Holders that elected to receive a refund of such excess amount. All other subscribing Rights Holders will receive additional shares of the Fund for such excess amount.

The total number of shares to be issued to subscribing Rights Holders is 2,613,746.

This non-transferable offering, which was initially announced on August 16, 2021, had an ex-rights date of August 24, 2021. This was a 1-for-1 offering which had a subscription price of 92.5% of the volume-weighted average market price for three trading days ending on the trading day after the expiration date. There was also an oversubscription allotment of up to 200% of the primary subscription available, should there be sufficient requests.

Massive dilution at the NAV/share level

Because the subscription price would always have been at a discount to the market price, there was no floor to this offering. Moreover, a 1-for-1 offering means that full subscription would have doubled the share count, while fulfilling all oversubscription requests would have quadrupled (!) the share count. As a result, this was a massively dilutive rights offering.

We can see how disastrous this offering period was for existing shareholders. Since the offering announcement, MXE's market price has fallen by nearly -28.74% as the market anticipated the impending dilution. We can also see that dilution reflected in the NAV graph which shows the NAV dropping by -21% (!!!) in a single day (from $13.85 to $10.93) as the accounting adjustment for the newly issued shares was performed. The actual share count increase was +146%, greater than the +100% of shares in the primary offering but less than the +300% maximum possible with the oversubscription shares.

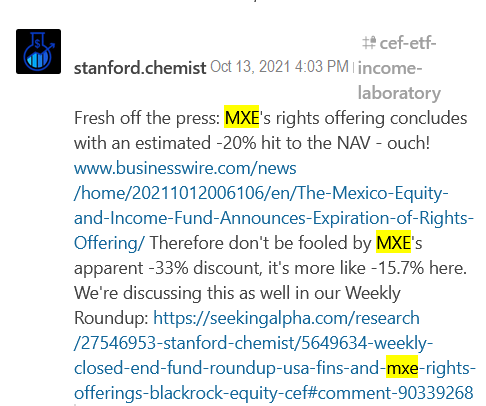

This is why I warned our members in the chat at the time that the rights offering results were announced to not be fooled by the -33% discount showing on CEFConnect, as that figure had not yet reflected the new shares.

Indeed, MXE's discount instantly contracted from -33.86% to -17.29% once those new shares were accounted for.

Outlook

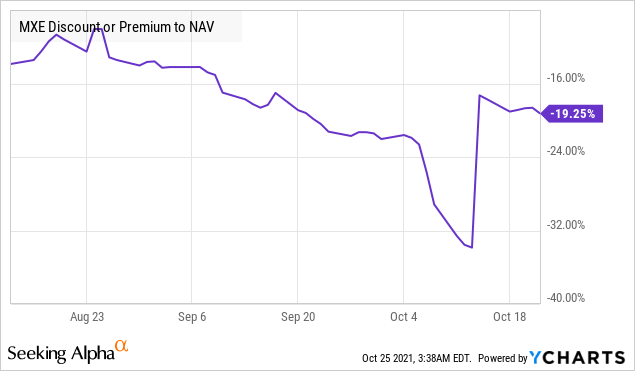

Despite the valuation drop, the fund's discount of -19.25% is still significantly below the fund's 1, 3, and 5-year average discounts of -16.40%, -11.33%, and -11.87% respectively, suggesting that it is undervalued relative to its own historical averages.

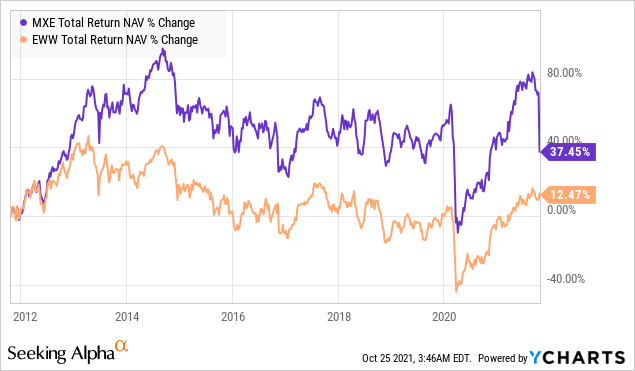

Moreover, MXE has actually been quite a decent equity CEF, even significantly besting its ETF counterpart, iShares MSCI Mexico ETF (EWW), by a substantial margin over the last 10 years. We can see that the outperformance was actually very impressive (+80% vs. +10% over 10 years), until the rights offering significantly damaged the NAV.

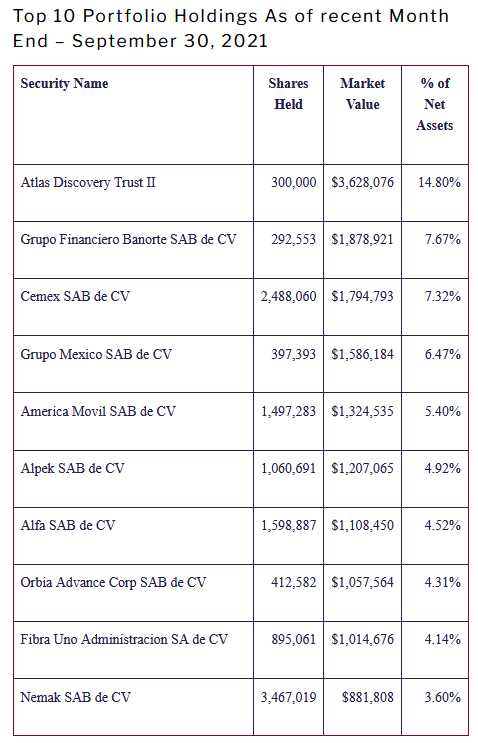

Hence, those looking for Mexican equity exposure could potentially take a look at MXE here. The fund's most recent holdings are shown below: (Source)

(Source)

The excellent performance of the fund (vs. its benchmark) aside, this highly dilutive rights offering is a negative that should be considered by potential investors. The fund successfully increased its share count by +146% (with total AUM increasing from $19.6m to $48.2m), but at the cost of significant harm to existing shareholders. Remember, with a dilutive offering like this, one must subscribe to avoid being negatively impacted by the NAV/share dilution. Hence, those MXE shareholders who were not aware that the rights offering was going on, and let their rights expire worthless, were harmed the most. Meanwhile, all shareholders suffered at the market price level as the discount of the fund widened. Therefore, if this rights offering were to become an annual event for MXE, then the long-term investor would probably give this one a pass as there would be a chance of getting stuck in the fund at a persistently wide discount, while paying fees to the shareholder-unfriendly managers.

Trading idea

But how about the trader? With the potential 200% oversubscription privileges, our member Patrick Irish had an interesting idea:

Last thought, next time I am buying 100 shares and subscribing for thousands.

The idea is that by initially buying only a small number of shares, one could avoid most of the pain caused by the discount widening and NAV dilution, while still having the ability to participate in the oversubscription requests and potentially gain many more discounted shares than one would normally be entitled to in offerings without oversubscription issuances.

With such a massive share count expansion like MXE's, it was unlikely that the maximum of +300% new shares would be issued (the actual was +146%). Hence, even 1 share of MXE purchased before the ex-rights date could potentially be used to subscribe for thousands or more of discounted shares, which would then be flipped for a profit once they were issued to the trader.

(However, in the event that there are too many oversubscription requests to be fulfilled, these would then be issued pro-rata to rightsholders so in that scenario, 1 share would not do much.)

But for the regular investor, the strategy of avoiding CEFs during rights offering periods holds true again. Here, selling MXE before the ex-rights date and then buying it back today would have allowed an investor to gain +40% "free shares" of MXE at no additional capital input, due to the massive share price depreciation caused by this highly dilutive offering.

Don't know what to do about CEF corporate actions?

Closed-end fund corporate actions such as rights offerings and tender offers present both significant opportunities and risks. We cover these regularly for members of CEF/ETF Income Laboratory, allowing them to profit or avoid losses.

Check out what our members have to say about our service.

To see all that our exclusive membership has to offer, sign up for a free trial by clicking on the button below!