RgStudio/E+ via Getty Images

Introduction & Thesis

I am extremely bullish on fuboTV (NYSE:FUBO). All my previous articles on fuboTV were bullish. I had two reasons for my positive view of fuboTV. One, the company was growing extremely fast at over 100% year-over-year while consistently reducing its loss ratio. Second, I believed the company's opportunity in the online live sports betting combined with the live sports streaming service was unique. fuboTV reported its 2021Q3 earnings, and I continue to be bullish. First, the company reported great earnings, showing strong momentum that is building up to be a powerful force. Second, the future opportunities fuboTV has in the streaming and the betting market became closer to reality. Finally, I believe the company's strategic acquisition will most likely result in even faster growth. Therefore, I continue to be extremely bullish on fuboTV.

Great Earnings

fuboTV reported another tremendous quarter showing strong business momentum. The company reported total revenue of $156.7 million with a year-over-year growth rate of 156% while the advertising revenue grew 147% year-over-year to $18.6 million. Further, total subscribers grew 108% year-over-year and 38% quarter-over-quarter to 944,605. Finally, the average revenue per user per month (ARPU) grew 10% year-over-year. As such, fuboTV reported another quarter of over 100% growth in every single metric. I believe these growth rates are a sign that the company's business is gaining momentum and that it is in a hyper-growth stage.

Guidance

Another great bullish catalyst reported in the earnings was the full-year guidance. The company increased its guidance and is expecting 2021Q4 revenue of $205-210 million and 1,060,000-1,070,000 subscribers, which represents about 32% and 10% growth sequentially. These numbers are great, but the company said that these numbers do not include any potential benefits from Fubo Sportsbook and its acquisition. Therefore, it can be reasonably assumed that the company's business, even without acquisition and expanding into new verticals, is strong. Further, with the addition of Fubo Sportsbook and the acquisition of a company can be beneficially shown in its 2022 guidance as the impact materializes, fuboTV can see a huge jump in revenue and valuations.

Future Opportunities

fuboTV's future opportunities are immense, and because of these opportunities, I think it has the potential to continue its strong growth momentum for the foreseeable future. For example, as growth in streaming services wanes down, Sportsbook and global expansion can continue the growth.

Sports Betting & Global Expansion

The sports betting market is enormous, and companies like DraftKings (DKNG) that are in the live online sports betting industry are receiving extremely high valuations in the financial market. The market is expected to explode in popularity amongst consumers seeking easier and accessible interactive activity as the states finally legalize live online sports betting. Compared to fuboTV's competitors, I believe it has unique advantages because it provides unmatched live sports streaming content. Betting customers can enjoy all sports-related content on fuboTV's platform while using the betting service. Also, it has an opportunity to convert its streaming-only customers to betting customers for further growth. As such, I think it is extremely likely for consumers to choose fuboTV's platform because it provides an all-in-one service.

During the earnings conference, fuboTV said that it will be acquiring two companies to aid its growth and global expansion as it is its ambition to dominate the global online sports streaming and interactive activity market. First, the company announced that Edisn.ai will be acquired to "enhance [the company's] AI-driven interactive experiences, personalization, and stability." I believe increasing fuboTV's AI capability is a reasonable move because it will increase the efficiencies of the entire operation. More importantly, the company announced the acquisition of Molotov SAS for $190 million, which will aid fuboTV to expand its services globally. Molotov SAS is a freemium online TV streaming platform with about 4 million monthly active users, and Molotov is the second-largest streaming service in France behind Netflix (NFLX). I believe this strategic acquisition is extremely beneficial for the company because fuboTV can dramatically increase its global expansion while increasing the platform to integrate its interactive activity.

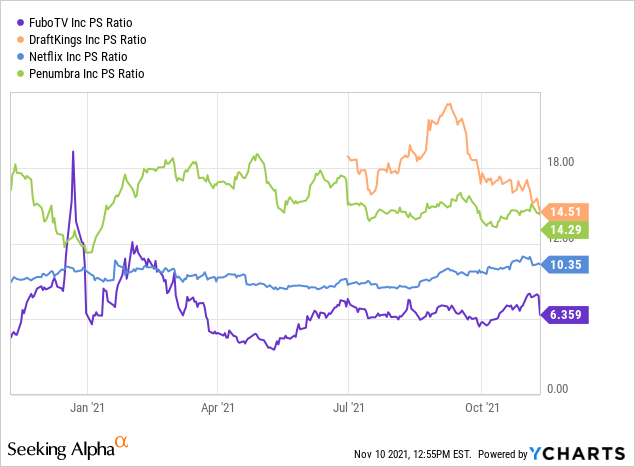

Valuation

After the earnings report, fuboTV's stock crashed. Because I thought the earnings, guidance, and acquisition were positive, I could not understand the rationale behind about a 20% decline. So, I acquired more shares. I believe the current valuation is an opportunity to acquire a company that is growing at over 100% yearly with immense opportunities in live streaming and betting markets. fuboTV today is worth about $3.8 billion with a price to sales ratio of 5.4, which I believe is a reasonable price to pay for extreme growth. Further, as the chart below shows, compared to its competitors in the streaming and betting industry, I think fuboTV is cheap.

[Chart created by author using YCharts in Seeking Alpha)

Risks

fuboTV is certainly not the safest asset to park investors' capital. There are numerous risks associated with investing in the company, including its financial risks due to continued net losses, dilution, and execution risks.

fuboTV has not reported any profitable quarters yet, and the company will not be profitable for the foreseeable future. During the 2021Q3, the company lost about $100 million. However, the company only has about $400 million in cash and cash equivalents with a total liability to asset ratio of about 49%. Thus, because of the continued losses due to fast expansion, future dilution may be inevitable. Further, the acquisition of Molotov SAS is expected to dilute about $190 million. Finally, execution risks are a concern for fuboTV because there are multiple business expansions concurrently occurring. The company is attempting to scale its online live sports betting services to the rest of the United States while attempting to grow its live sports streaming service in both the United States and internationally.

Summary

fuboTV is still a high-risk investment due to the competition, dilution, and profitability; however, I think an investment in it can potentially be a rewarding one. The company is growing extremely fast and firing on all cylinders, including advertisement revenue, subscriber growth, revenue growth, sports betting, and global expansions through acquisitions. Therefore, I believe fuboTV is a strong buy today after the post-earnings sell-off.