Kativ/E+ via Getty Images

Coupa Software (COUP) is not only recommended by Gartner. The company is also a partner of massive organizations in different industries. That's not all. With new partners, successful R&D, and new functionalities, I believe that the company's valuation could increase significantly. Using estimates from management and conservative assumptions, my financial model revealed that COUP could be worth $500. Yes, I am a buyer at the current market price.

Recommend By Experts, Coupa Software Already Serves Large Business Clients

Headquartered in San Mateo, California, Coupa Software was established to offer solutions for business expense management. In my view, the company follows exactly the words of Linus Torvalds when engineers conceive new software:

The function of good software is to make the complex appear to be simple. Source: Famous Quotes About Software Engineer Everyone Should Know

Software experts like Gartner, Forrester, and IDC noted that COUP is a leader in its current offering. With these experts recommending the software and large clients, we can expect significant business growth in the coming years:

Source: Presentation

Source: Presentation

Source: Presentation

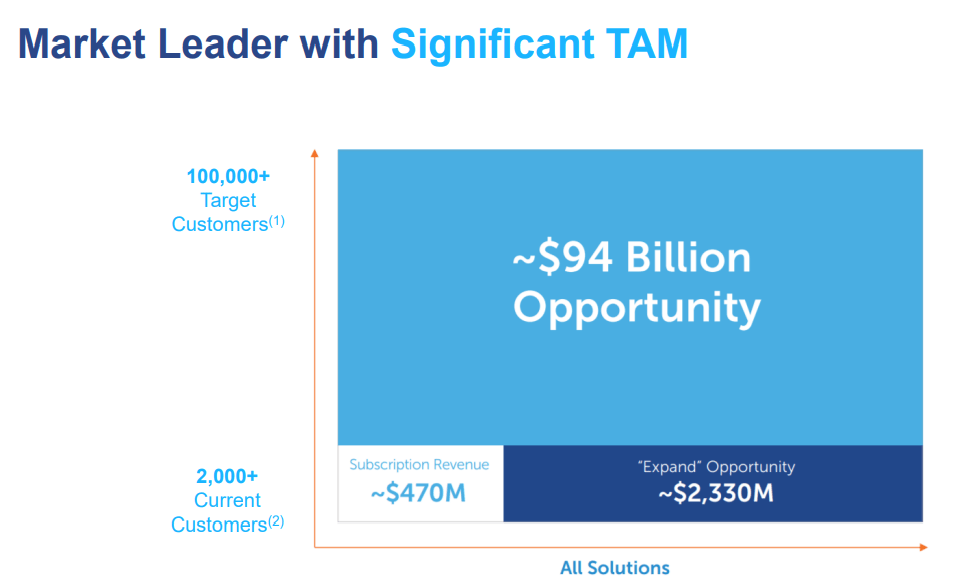

The company's cloud-based business expense management platform offers visibility and control over how companies spend money and manage liquidity. The target market for software offering similar solutions is said to be worth close to $94 billion. In 2021, I expect revenue to be close to $500 million, which means that COUP has many more potential customers to please:

Source: Presentation

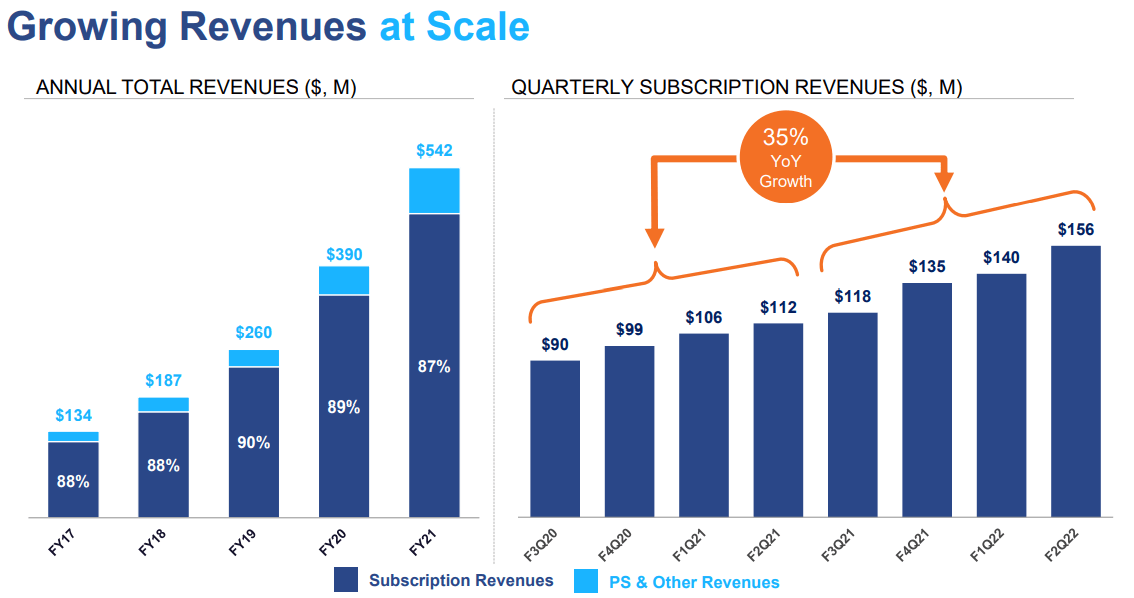

With the previous information, the company's revenue growth expected by management appears logical. The company envisions that quarterly subscription revenue could grow at a CAGR of 35% y/y. For the year 2021, management believes that revenue of $542 million is achievable:

Source: Presentation

A Conservative Scenario Implies A Fair Price Of $200

Under the base case scenario, I believe that COUP will successfully sign partnerships with other companies offering expense management software. COUP's partners will most likely bring clients, and the company, in return, will give them a small percentage when business is made.

The company knows well how to contact collaborators and partners. System integrators such as Accenture (ACN), Deloitte, and KPMG work with COUP. Besides, take into account that management signed agreements with leading hosting and infrastructure companies. They don't only bring clients but also help COUP scale its services:

With these partnerships, we are able to easily scale the service during peak load periods, allowing us to continuously add users and customers without significant downtime or lead-time to procure new capacity. Source: 10-k

There are other types of partners that are happy to work with COUP. Large conglomerates like Barclaycard, Citigroup (C), PayPal (PYPL), JPMorgan Chase (JPM) are among the list of partners. They help clients move money more rapidly. In my view, with more partners of this type, in the future, COUP's revenue growth would most likely increase. I am quite optimistic about the company's community collaboration capabilities. COUP appears to help connect industry practitioners, who can share experiences and know-how related to spending decisions. In my view, the network effect generated by these collaborations is immense. It will not only reinforce the connection of COUP with clients, but it could also bring more clients, and enhance sales growth:

These capabilities are embedded throughout our platform and include, for example: informative discussion forums surfaced in-context to users as they make spend decisions within Coupa; an exchange for companies to share and download forms and content from across the community; and a spend matchmaking capability that automatically recommends connections with community experts to provide input or work together on a sourcing event, among others. Source: 10-k

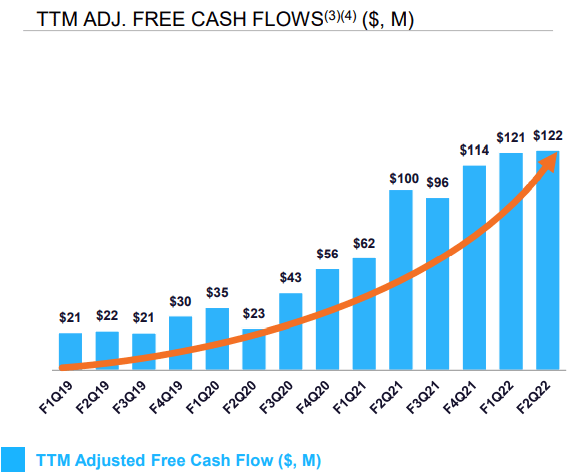

In this case scenario, I will be using the free cash flow forecasts made by management. They are expecting to report quarterly FCF around $122-$114 million, which could mean yearly revenue close to $450-$500 million:

Source: Presentation

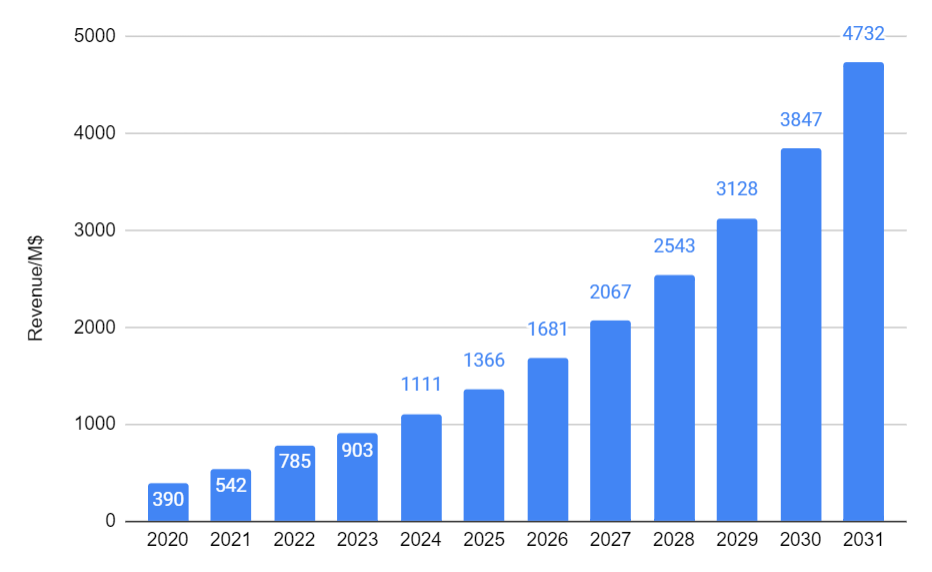

Note that I assumed sales growth around 23%, which I believe is conservative. With these numbers, revenue would increase from $542 million in 2021 to more than $4.700 billion in 2031:

Source: Hohaf

Source: Hohaf

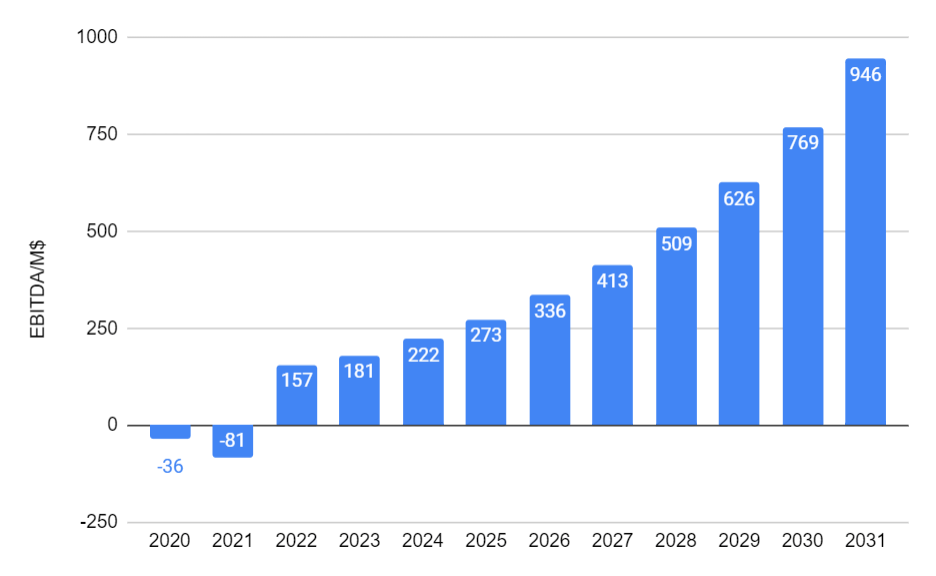

Like other investment analysts, from 2022 to 2031, I envision an EBITDA margin of 20%. It means that the EBITDA would grow from close to $150 million in 2022 to close to $950 million in 2031:

Source: Hohaf

Source: Hohaf

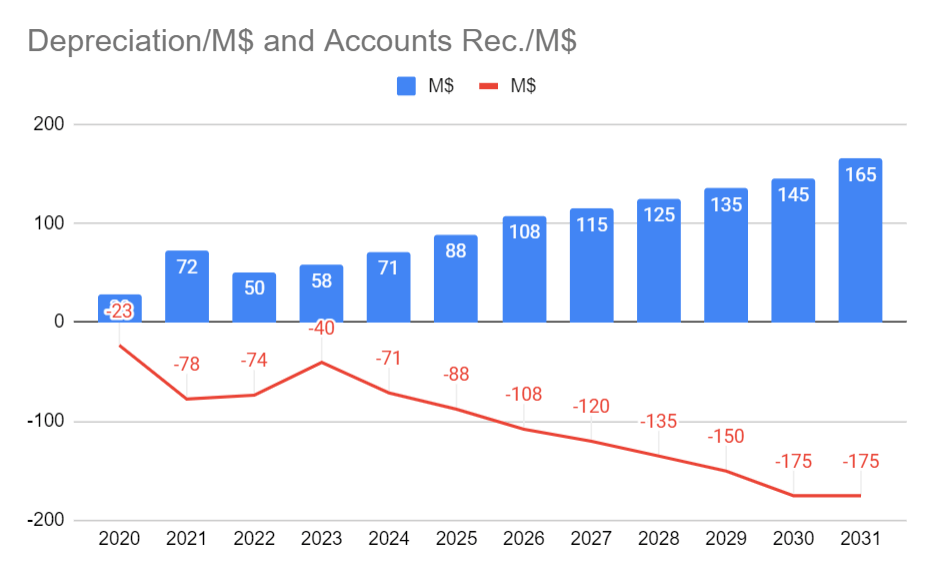

I also assumed that depreciation would increase from $50 million in 2022 to around $165 million. Besides, changes in accounts receivables would go from -$40 million to less than -$175 million in 2031. Note that my numbers are not far from previous figures reported by COUP:

Source: Hohaf

With the previous assumptions and capital expenditures worth between -$55 million and -$95 million, the FCF would stand at $600-$650 million in 2031:

Source: Hohaf

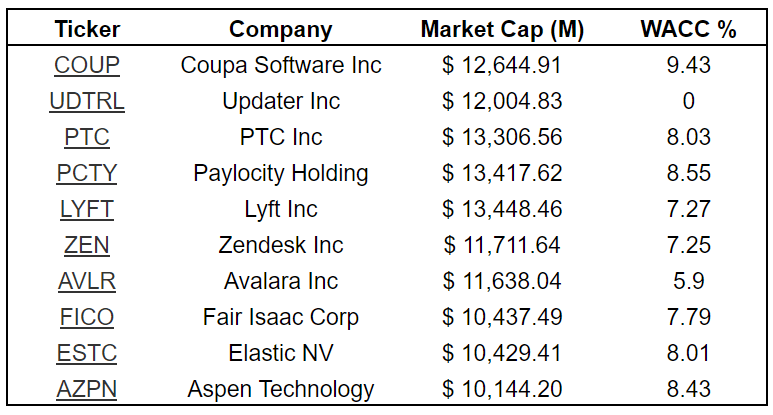

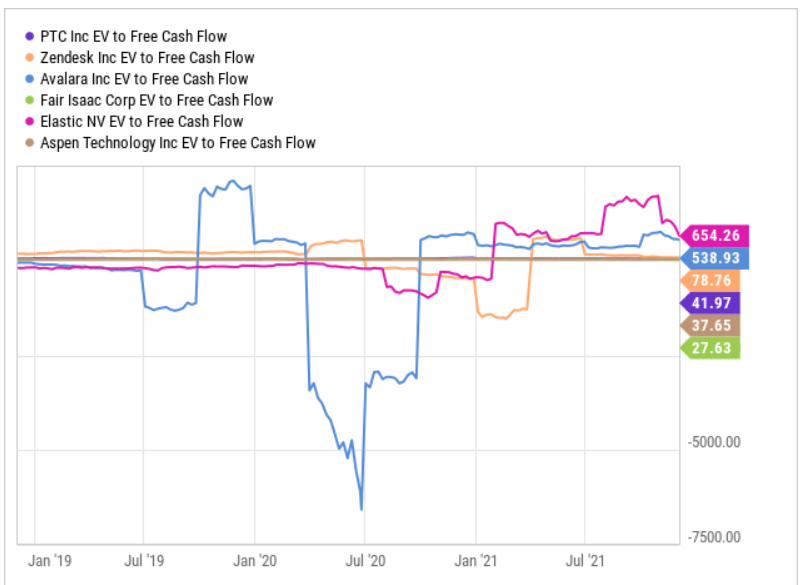

COUP's competitors have a WACC of around 7.27%-8.55%, and trade at 27x-654x FCF. With these figures in mind, I tried to come out with very conservative multiples. I used 8.25% FCF and an exit multiple of 55x:

Source: COUP WACC % | Coupa Software - GuruFocus.com

Source: Ycharts

The results include a net present value close to $1.25 billion, and an implied market capitalization close to $15 billion. Finally, the fair price would be close to $200:

Source: Hohaf

Successful R&D, Acquisitions, And Synergies Could Push The Stock Price Up

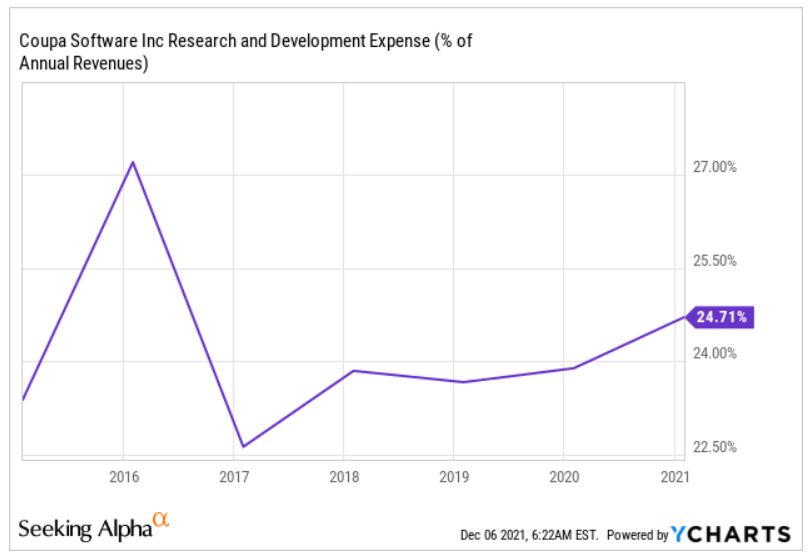

In my view, if the company's software continues to be reliable, and usability and functionality continue to improve, revenue growth would increase. In this regard, I would expect COUP's research and development efforts to be successful. Take into account that COUP's R&D/Sales ratio stands at 24%, which appears significant:

Source: Ycharts

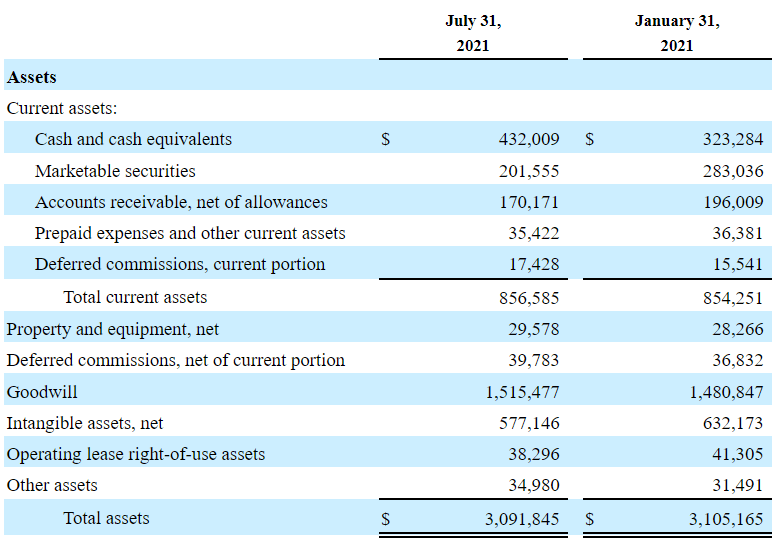

COUP has a significant amount of cash in hand. As of July 31, 2021, the company reported cash worth $432 million, and marketable securities worth $201 million. With this level of cash and goodwill worth $1.151 billion, I believe that we could see more inorganic growth in the coming years.

Source: 10-Q

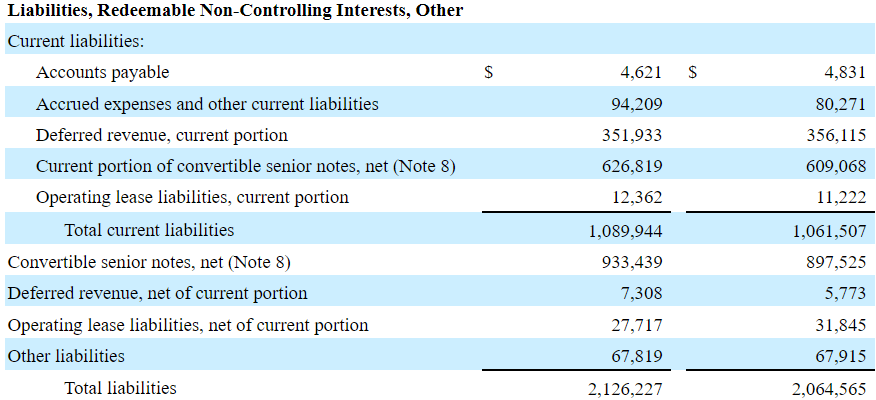

The company also reports some debt. I counted $1.559 billion in convertible senior notes. Under this case scenario, the company may achieve close to $1.5 billion, so I wouldn't worry much about COUP's financial debt.

Source: 10-Q

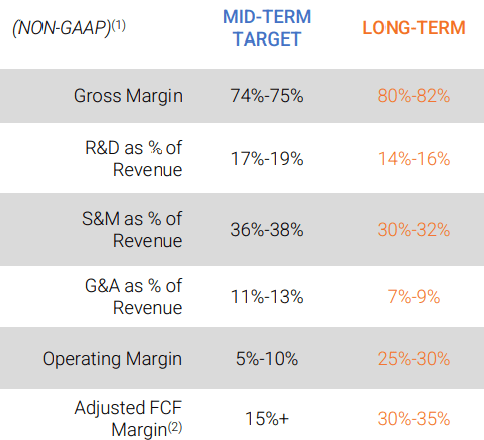

In the previous case scenario, I obtained 2031 FCF close to 10%-13%. Management gave an estimate of the margins in the future, which is better than my previous results. COUP believes that it could obtain a long-term FCF margin of 30-35%. Taking into account these figures, I designed another DCF model.

Source: Presentation

Under the assumptions of the best-case scenario, revenue growth would stand at 23%, and the company's EBITDA margin would be equal to 35%. Also note that the FCF margin stands at 25%-27%, which is close to the estimates given by management:

Source: Hohaf

Source: Hohaf

If we also assume that with a better FCF margin, the cost of debt could decline, the WACC could be 6.755%. Finally, the fair price would stand at $500:

Source: Hohaf

The Demand For The Software May Decline, Which May Lead To A Decrease In FCF Expectations

The company's previous revenue growth is quite impressive. However, investors don't usually expect further growth because they saw it in the past. COUP's annual report clearly notes that a reduction in the demand for software, more competition, and many other factors could make the revenue growth decline. As a result, market participants may sell their shares, which would lead to a reduction in COUP's valuation:

Revenue growth could slow or our revenues could decline for a number of reasons, including any reduction in demand for our platform, increased competition, contraction of our overall market, our inability to accurately forecast demand for our platform, or our failure, for any reason, to capitalize on growth opportunities. Source: 10-k

The Acquisitions Could Fail

The company acquired a significant number of businesses in the past. If management calculated an excessive amount of synergies, the goodwill accumulated may have to be impaired. As a result, expected free cash flow may decrease, which would lead to a decrease in the stock price:

For example, we acquired LLamasoft, Inc. in November 2020, Bellin Treasury International GmbH in June 2020, ConnXus, Inc. in May 2020, Yapta, Inc. in December 2019, and Exari Group, Inc. in May 2019. Acquisitions may disrupt our business, divert our resources, and require significant management attention that would otherwise be available for the development of our existing business. In the future, if our acquisitions do not yield expected returns, we may be required to take charges to our operating results based on this impairment assessment process, which could adversely affect our results of operations. Source: 10-k

Conclusion

COUP is a business leader according to Gartner. The company is targeting a massive market opportunity and expects double-digit sales growth. With sufficient acquisitions, partners, and research and development efforts, in the future, COUP could see its share price at $500. There are some risks from failures in M&A operations and a decrease in demand. However, I believe that the share price will most likely trend north in the medium term. I am buying.