BARTON/DigitalVision via Getty Images

Although some parts of the world are experiencing population declines, the planet as a whole is expected to see more people in it in the future than in the past. In the US alone, for instance, population is expected to expand by at least 100 million by the end of the century. And with that rise in population will come the requirement for more physical infrastructure. This includes residential properties and various non-residential ones as well. One interesting play to consider on this trend is a firm called Cornerstone Building Brands (CNR). In recent years, due to a combination of organic growth and growth by means of acquisition, the company has expanded its top line considerably. And while net profitability for the company has suffered as of late, its cash flow picture has been generally positive. This year is looking to be a bit mixed, but when you consider just how cheap shares are today, it seems to me that this enterprise could exhibit significant upside for shareholders who buy in now.

Cornerstone Building Brands - A provider of windows and more

At present, Cornerstone Building Brands operates as the largest manufacturer of exterior building products in North America. The company services both residential and commercial customers across the market, ranging from those focused on new construction to those dedicated to the repair and remodel markets. As of the end of its latest fiscal year, the company provided its services through the operation of 67 manufacturing facilities spread across the US and Canada. It also has a network of 40 distribution and branch office facilities.

The overall operations of Cornerstone Building Brands can best be described by looking at the individual segments the company operates. The first of these is called the Windows segment. Through this, the company provides windows and doors for their customer base. Products range from those made of vinyl to aluminum to wood and more. Their overall collection of brands includes names like Ply Gem, Simonton, Atrium, Great Lakes Window, and more. In its latest fiscal year, adjusting for the various asset sales and purchases the company made, sales under this segment accounted for 41% of the company's overall revenue.

The next key segment of the company is called the Siding segment. In this segment, the company provides a large selection of exterior cladding, fencing, and stone products. It also provides other accessories to its customer base including vinyl siding, composite siding, steel siding, fabricated aluminum gutter protection, PVC trim, and more. This particular segment accounted for 26% of the company's overall revenue in 2020. And the brand names that fall under it include Variform, Mitten Building Products, and ClipStone.

The final segment the company has is called its Commercial segment. The company provides a wide variety of products such as metal building systems, metal roofing and wall systems, insulated metal products, doors, and more to customers that are mostly in the low-rise non-residential construction market. Selling brands like ABC, Ceco Building Systems, and Centria, Cornerstone Building Brands generated 33% of its revenue from this segment in 2020.

In recent months, the management team at Cornerstone Building Brands has initiated a lot of asset sales and purchases aimed at refocusing the enterprise and cutting down debt. For instance, on December 3rd of this year, the company completed its acquisition of Union Corrugating Company at an undisclosed price. This particular purchase will bring in annual revenue for the company of $250 million. In August, it acquired Cascade Windows for $245 million and sold its Roll-up Sheet Door Business for $168 million. But the biggest deal completed this year was its sale of its Insulated Metal Panels assets for $1 billion. Naturally, the number of deals the company has completed does complicate the valuation process. But management has provided some data that factors in what financial performance would have looked like if the company had completed these various deals, excluding the most recent purchase, at the start of its 2020 fiscal year.

*Created by Author

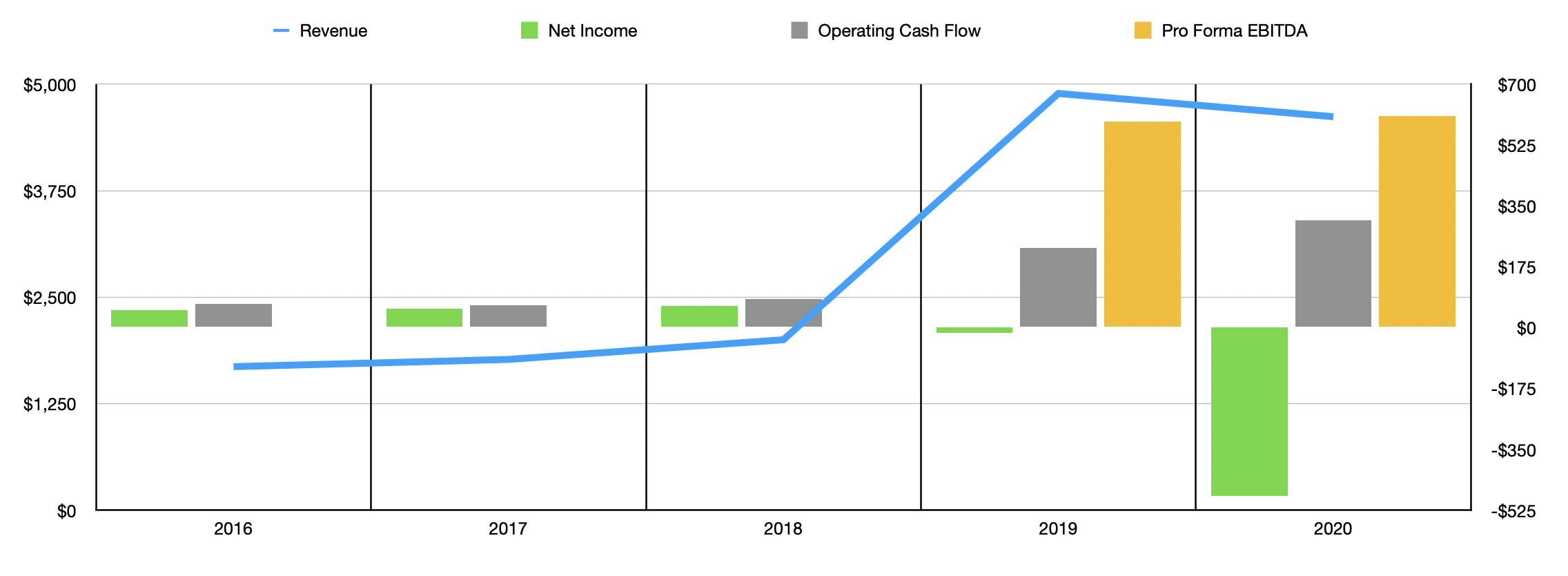

To see just how big an impact wheeling and dealing has had on the company, we need only look at revenue over the past few years. After seeing revenue climb from $1.69 billion in 2016 to $2 billion in 2018, it then jumped to $4.89 billion in 2019. Then, in 2020, due to the COVID-19 pandemic, revenue dipped slightly to $4.62 billion. For the current fiscal year, things are looking up. Revenue in the first nine months of its 2021 fiscal year totaled $4.11 billion. This compares to the $3.43 billion achieved the same time a year earlier. If instead of relying on these figures, we rely on the figures of how the company would look if its acquisitions and sales had been completed sooner, then revenue would have risen from $3.30 billion to $4.01 billion over the same window of time.

When it comes to profitability, things have been rather volatile. Between 2016 and 2018, for instance, the company saw its net income grow from $50.64 million to $62.69 million. But then, in 2019, the company generated a loss of $15.39 million. This loss then soared to $482.78 million in 2020. Operating cash flow, fortunately, has followed a different trajectory. After rising from $68.44 million in 2016 to $82.46 million in 2018, it then jumped to $229.61 million in 2019. In 2020, operating cash flow grew to $308.42 million. Management has not provided reliable EBITDA data for the years prior to 2019. But from 2019 to 2020, this metric increased from $593.18 million to $608.67 million.

*Created by Author

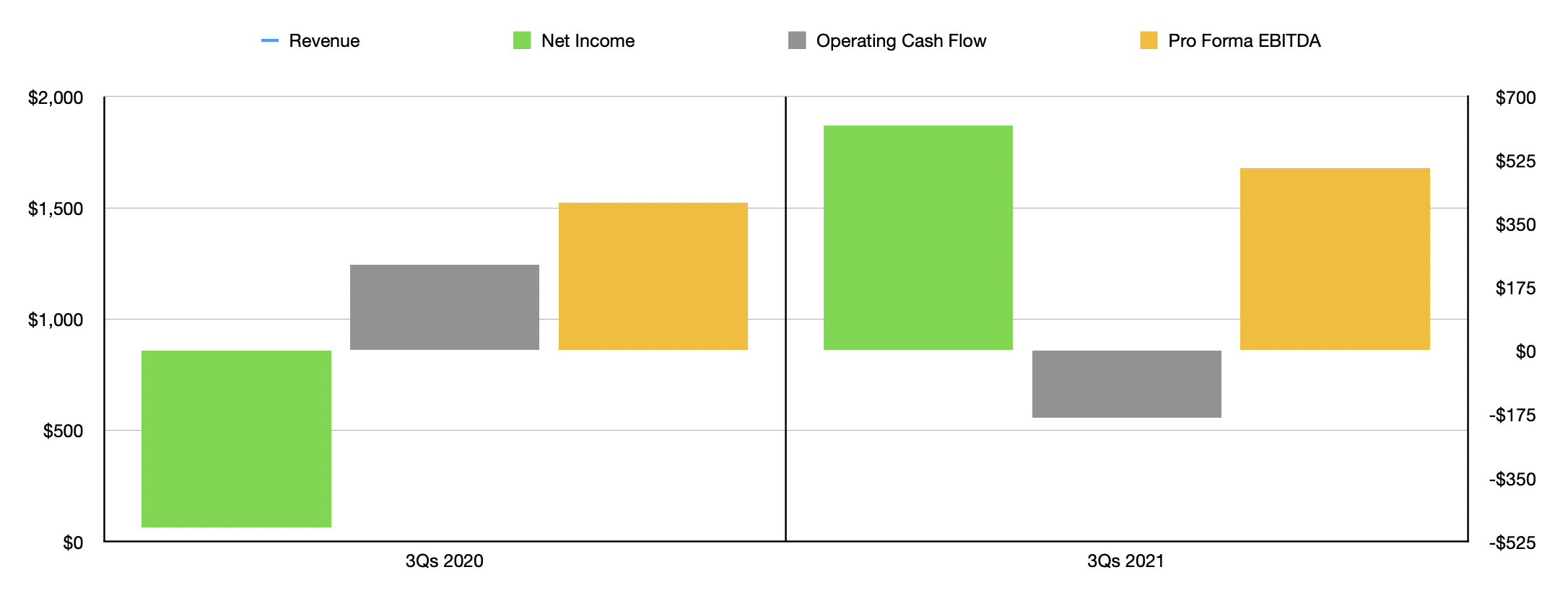

This current fiscal year is looking a bit mixed for the company. For instance, in the first nine months of the current fiscal year, the company generated a net profit of $619.97 million. This compares favorably to the $484.66 million loss achieved one year earlier. On the other hand, operating cash flow went from a positive $236.88 million to a negative $183.64 million. Even if you were to adjust for changes in working capital, it would have declined from $231.35 million to $75.49 million. EBITDA grew from $448.66 million to $511.75 million. And adjusted for its asset sales and purchases, this would have grown from $407.57 million to $503.80 million. Although operating cash flow is not looking great this year, the other profitability metrics are looking better. A good portion of this can probably be chalked up to the synergies and cost savings that the company has been working toward. For this fiscal year, for instance, management expects annualized synergies and savings associated with its 2018 merger to range between $325 million and $330 million. Of this, $250 million was achieved by the end of the firm's 2020 fiscal year.

Pricing CNR stock reveals a cheap prospect

Fortunately for investors, management has provided some guidance for the current fiscal year. At present, the company expects EBITDA to be around $681.30 million. If we apply that same year-over-year growth to other profitability metrics, then operating cash flow should be about $475.23 million. Taking these figures, we can effectively price the company. On a forward basis, the company is trading at a price to operating cash flow multiple of 4.5. This compares to the 6.9 reading if we use the data from 2020. Meanwhile, the EV to EBITDA multiple of the company is 6.6, down from the 7.4 if we use 2020 data.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Cornerstone Building Brands | 4.5 | 6.6 |

| Builders FirstSource (BLDR) | 14.5 | 7.1 |

| A. O. Smith Corporation (AOS) | 22.3 | 18.6 |

| Insteel Industries (IIIN) | 10.6 | 6.6 |

| UFP Industries (UFPI) | 12.6 | 7.9 |

| Johnson Controls International (JCI) | 22.9 | 17.2 |

To put this data into perspective, I decided to compare the company's results to five high rated peers identified from Seeking Alpha’s Quant platform. On a price to operating cash flow basis, these companies ranged from a low of 10.6 to a high of 22.9. Using both the 2020 and 2021 figures, our prospect was the cheapest of the group. I then did the same thing using the EV to EBITDA approach, ending up with a range of 6.6 to 18.6. Using the 2021 figures, our company was tied with one other as being the cheapest in the group. And if we use the 2020 figures, there were only two companies cheaper than Cornerstone Building Brands.

Takeaway

Based on the data provided, I must say that the volatility of Cornerstone Building Brands from a fundamental perspective makes valuing the firm a bit difficult and unreliable. But so long as recent performance can be indicative of the future, then shares look extremely cheap. This is true not only relative to the competition; it is true on an absolute basis. And because of this, I would urge any investor who likes this particular market to consider this firm at this time.

Crude Value Insights offers you an investing service and community focused on oil and natural gas. We focus on cash flow and the companies that generate it, leading to value and growth prospects with real potential.

Subscribers get to use a 50+ stock model account, in-depth cash flow analyses of E&P firms, and live chat discussion of the sector.

Sign up today for your two-week free trial and get a new lease on oil & gas!