luza studios/E+ via Getty Images

Editor's Note: This article was submitted for review on Sunday 27th, 2022

Investment thesis and background

We are initiating with CTI BioPharma (CTIC) with a buy rating with a TP of USD 6.3. CTI BioPharma is a US-based clinical-stage biotechnology company developing therapeutics for blood-related cancers.

Regarding clinical development, CTI BioPharma has finished its NDA submission for pacritinib, which is its lead candidate. In our view, pacritinib is going to get approved by the FDA in 2022-Feb-28 PDUFA. Pacritinib is a JAK2/IRAK4/FLT3/CSF1R inhibitor, that is differentiated, that targets myelofibrosis in patients with severe thrombocytopenia. We highlight that there are no approved therapies in the myelofibrosis space targeting this specific niche indication. We view the setup as similar to Sierra Oncology (SRRA). We think pacritinib has the potential to fill the unmet need in patients with severe thrombocytopenia which is defined by platelets sub 50k/µL. In this patient segment, the current standard of care Jakafi, JAK-2 focused therapeutics, from Incyte (INCY) is not indicated. One of the reasons for our enthusiasm is because pacritinib may offer a candidate with a cleaner adverse event profile compared to currently available JAK2-focused agents, which is problematic because it lowers platelet levels, limiting their usage in thrombocytopenic myelofibrosis patient population, particularly in patient groups with platelet counts sub 100k/µL, which represent approximately 2/3 of the ~20,000 US myelofibrosis patient population.

We like the clinical data, targeting a niche MF patient population where Jakafi can't be used

We emphasize that pacritinib is a unique oral JAK-2 inhibitor with specificity for JAK2/IRAK1/CSF1R, without inhibiting JAK1. Due to this differentiated mechanism of action, the drug has shown activity in patient populations with low platelet counts. During the PERSIST-2 trial, when studied on patients with MF with severe thrombocytopenia, 200mg BID pacritinib resulted in 29% of patients reaching spleen volume reduction (SVR) of +35% vs 3% with the BAT arm (best available therapy that included standard of care ruxolitinib)). We consider SVR to be more of an objective endpoint as it actually measures the volume of the spleen, unlike other endpoints that are based on the patient's subjective responses. Furthermore, 23% of the patient population who received pacritinib saw a decline in Total Symptom Scores (TSS) >50% versus 13% of those on best available therapy (BAT). On the safety front, the treatment-related adverse events associated with pacritinib were clean and low-grade. We highlight that these adverse events rarely lead to discontinuation of the therapy and most importantly platelet and hemoglobin levels also stabilized, which indicates its potential to be used in anemia and thrombocytopenia patient population.

FDA delay is likely a minor issue, and we expect the drug to receive the FDA's stamp of approval soon

Last December (December 1st, 2021), CTI Announced an FDA delay in the decision for pacritinib's NDA for myelofibrosis, and the stock dropped 45% right after, which was quickly bought up by investors. Based on the company's statement:

In the second quarter of 2021, the FDA granted priority review for CTI's NDA for patients with myelofibrosis with a PDUFA date of November 30, 2021. In the course of product labeling discussions, the FDA requested additional clinical data, which was submitted to the agency on November 24, 2021. Earlier today, the FDA informed the Company that it considers the data submission to constitute a "major amendment" to the NDA and therefore the PDUFA date has been extended by three months to provide additional time for a full review of the submission. At the current time, CTI is not aware of any major deficiencies in the application. Source

We highlight that the company wasn't aware of major deficiencies in the application, and this type of delay is common by the FDA. We see this type of event as a mechanism for buying more time for the FDA. As such, we are not too worried about it. In our view, CTIC's interaction with the FDA was smooth, and the company passed manufacturing inspections. If FDA had problems with its trial, we believe the company would have gotten more specific feedback or a request for a new trial. Furthermore, I do not think the FDA would have given a priority review in 2021 for this candidate if there were big issues that worried them. Also, the fact that pacritinib received a clinical hold by the FDA in 2017 and the FDA lifted it after makes us think the agency is confident about its safety.

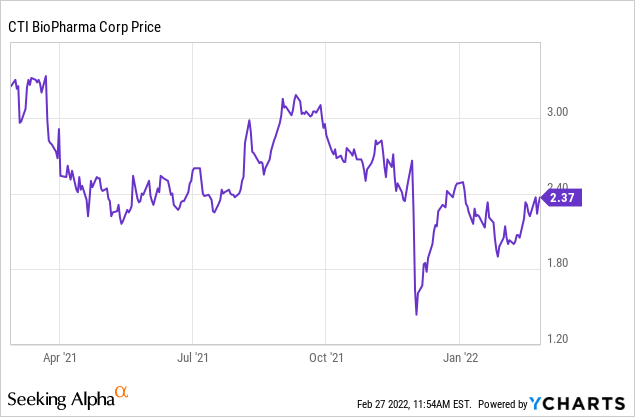

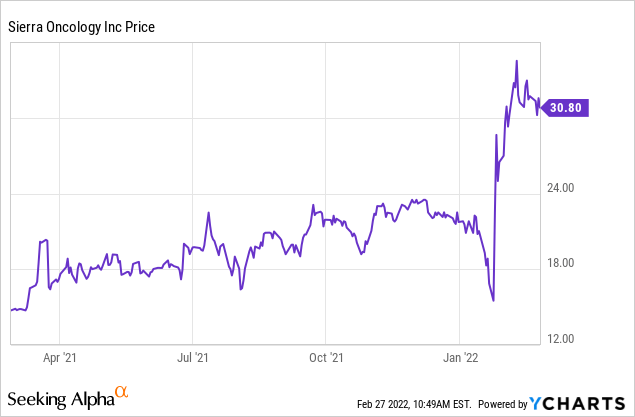

Setup similar to Sierra Oncology before phase III data

Seeking Alpha

Source: Seeking Alpha - SRRA valuation

Sierra Oncology's (SRRA) momelotinib targets MF patients who have severe anemia, where Jakafi can't be used. Even though it is a niche segment, after its phase III data, SRRA's share price skyrocketed close to 100% (even during the bear market that we have seen across the biotech sector (XBI) (IBB)). Considering that CTIC also targets a similar niche segment, targets thrombocytopenia patients particularly, and showed stronger efficacy data compared to momelotinib which showed decent/but not that great efficacy (that is why some of the trials were designed to look for non-inferiority), we think if approved, CTIC to follow a similar trajectory in share prices. Furthermore, we highlight that pacritinib has already filed a BLA, and its clinical development status is a couple of years faster than momelotinib (which is still in phase III), we think the current setup is more interesting.

Valuation

Seeking Alpha

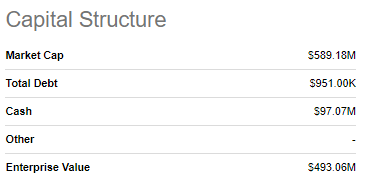

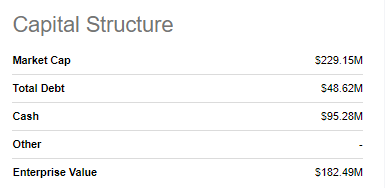

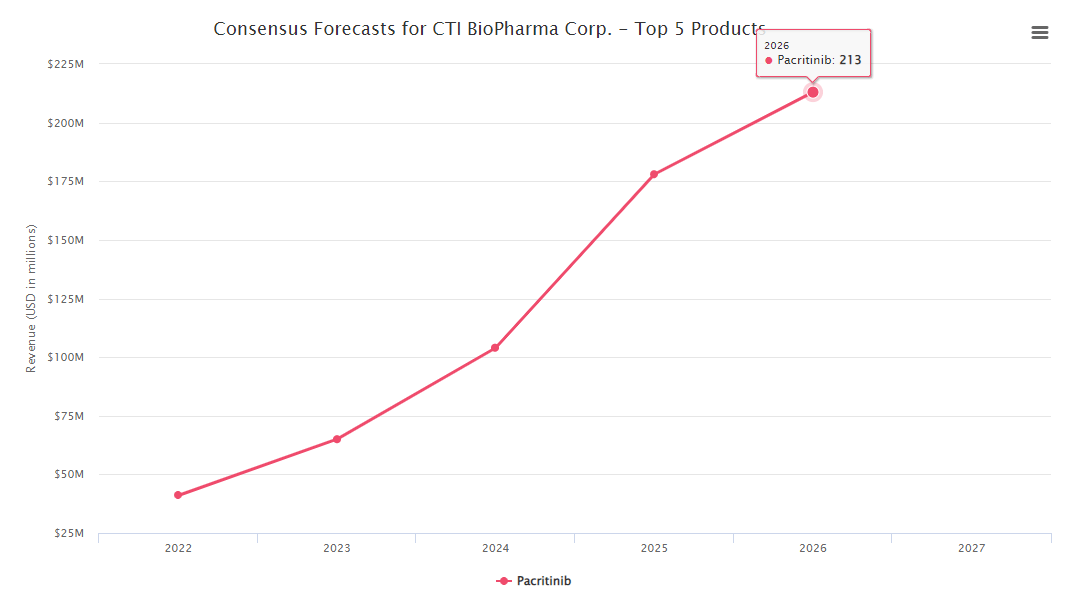

The company currently holds USD 95M cash and has an EV of around 182M which in our view is very cheap. According to the consensus forecast from Biomedtracker (accessed on Feb. 25th, 2022), the peak sales of the candidate is around USD 213M and if we risk-adjust the peak sales using the probability of success statistics 90.6% from Evaluate, we believe the pipeline valuation should be around USD 580M using conservative peak sales multiple of 3. As such, based on our valuation, this means that the company has room to go up another 320% from the current price of USD 2.37.

Biomedtracker database

Risks

1. FDA may reject the approval due to unforeseen reasons or the PDUFA date may be delayed again.

2. Macroeconomic factors - increased interest rate may reduce investors' appetite for the biotech sector.

3. Geopolitical events - Russia and Ukraine war may put negative pressure across the market dragging the CTIC's share price down.

Upcoming catalysts

- Q1 2022: Feb-28-2022: New FDA Action Date for pacritinib in myelofibrosis. We view this catalyst to be the pivotal data that we are focusing on.

- Q1 2022: launch of pacritinib for MF.

- 2022: Spleen volume reduction (SVR) data from the confirmatory Phase III PACIFICA trial for pacritinib.

- 2023-24:Total Symptom Score (TSS) data from the confirmatory Phase III PACIFICA trial for pacritinib.

Conclusion and valuation

We believe that pacritinib has the potential to be a lead therapeutic agent in the niche myelofibrosis indication and the current valuation, EV of 182M, is extremely attractive for a candidate with a conservative peak sales potential of USD 200M. Considering that pacritinib may be the first product for myelofibrosis targeting a patient population with severe thrombocytopenia, low valuation (discussed in detail in the valuation section), with a cash position of USD 95.28M (last of last reported Q3 earnings presentation), we envisage that CTI BioPharma's current set-up represents an attractive risk-reward scenario with 50% potential downside (around cash value of $1/share if trial completely fails) and ~320% potential upside (bull case of USD 7.6 if approved on the Feb 28th - valuation section). I have initiated an option-sized position to play the PDUFA that is planned for Feb 28th. If approved, I am planning to offload 50% of my position and keep the rest, if not approved and FDA rejects the candidate, I am planning to cut my losses and liquidate 100% of my position. If FDA delays (which we think is unlikely) without material reasons, I am planning to buy the dip and accumulate more shares.