Rob Kim/Getty Images Entertainment

Investment Thesis

BlackRock (NYSE:BLK) is the largest asset manager in the world, with over $10 trillion in AUM. Shares have sold off by more than 20% since peaking near $970 in November 2021. Investors might find that the valuation and dividend growth is attractive, but I don’t think it’s a bargain at current prices. The company has grown revenues at a solid clip and has a solid balance sheet. Investors focused on income can secure a 2.6% yield with a history of solid dividend growth.

However, owning a company like BlackRock that makes a fortune on the passive investing movement is anathema to active investors like myself. I won’t own it, but I have to appreciate the solid business model, as well as the potential opportunities created by the passive money flows and the ESG investing movement. In my opinion, we are going to see a renaissance for active investment over the next decade. I don’t know if it will lead to declining AUM and in turn revenue for BlackRock, but I think there are better opportunities out there.

BlackRock and ESG

Instead of jumping right into the business, I’m going to lead off today with a brief criticism of BlackRock and the ESG movement. One of the reasons I’m not interested in owning BlackRock is management and their philosophy. I’m not a huge fan of Larry Fink, BlackRock’s founder and CEO. Apart from his role with BlackRock, he is known for being a proponent of ESG and stakeholder capitalism. He also sits on the board of the World Economic Forum, another organization I’m not a huge fan of. He isn’t the only one responsible for the woke narrative being accepted in corporate America, but he has been a driving force behind ESG and other things that have negatively impacted wide swaths of the country.

I might be different than other people my age on this topic, but I want my oil companies to behave like oil companies instead of pandering to Wall Street. The fact that a hedge fund owning 0.02% of shares could get three of Exxon’s (XOM) board seats because they secured the backing of BlackRock, State Street (STT), Vanguard and several pension funds proves how out of control the ESG movement is.

Say what you want about ESG being a force for “good” or protecting the climate, what it really has become is a driving factor in the widespread malinvestment we have seen over the last decade, especially in the energy sector. As oil and natural gas prices spike, many ESG proponents take a naïve position: soaring energy prices prove that we need to transition to greener forms of energy. What they fail to mention is that ESG is a direct cause of the soaring energy prices. From higher interest rates on debt offerings to depressed equity valuations (especially from 2015-2020), ESG has created the structural undersupply in the energy market.

The Business

While investors are free to disagree with me on my takes on the ESG approach of BlackRock, we can all agree that BlackRock is a high-quality business with impressive margins and a solid balance sheet. The company had a net income margin over 32% in 2021, which is impressive for a company the size of BlackRock. They have a history of growing revenues and the bottom line at double digit rates, which is certainly something that investors look for.

Another piece that is attractive to investors is the solid balance sheet. At the end of 2021, the company had $7.5B in debt and over $9.3B in cash on the balance sheet. While it is highly unlikely that they would choose to repay billions of debt that has a negative real interest rate, investors can be comfortable with BlackRock’s liquidity position. The biggest driver for the performance of BlackRock’s business is going to be continued growth in AUM.

AUM Growth (10-K) (sec.gov)

This is the biggest question mark for investors in my mind. If you think the markets continue to march higher, then it stands to reason the BlackRock’s AUM will continue to grow at an impressive rate through a combination of appreciation and net inflows. The problem is that I think we are in for a turbulent stretch in the markets, which could have a negative impact on BlackRock’s AUM and bottom line. The current valuation is reasonable, but I don't think it is attractive enough to warrant buying for new investors.

Valuation

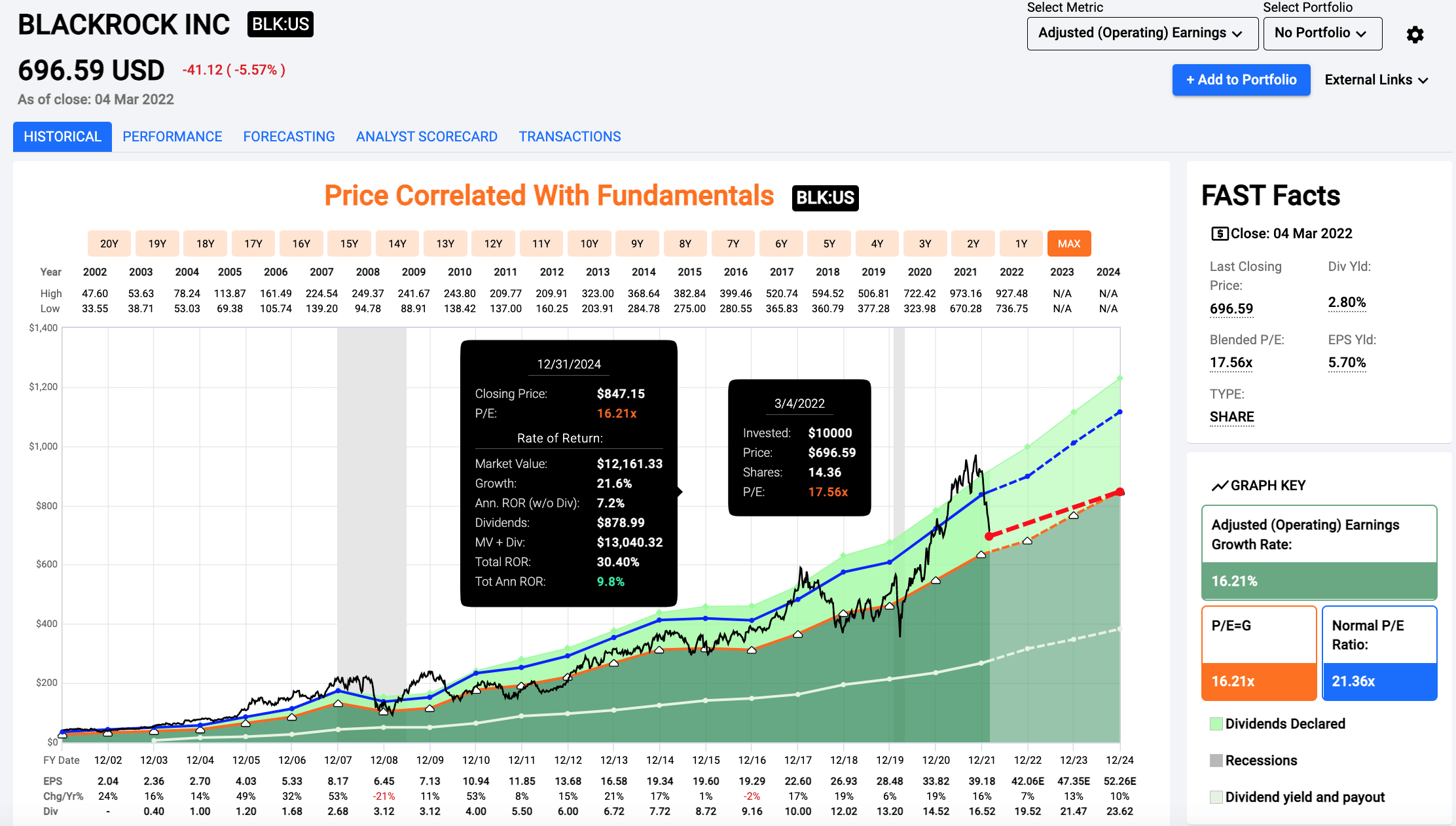

BlackRock currently trades at an earnings multiple of 17.6x. This is just under the normal multiple of 18.9x since coming out of the financial crisis in 2009. I think that shares would start to get attractive for interested investors around 15x earnings, especially considering the earnings and dividend growth.

Price/Earnings (fastgraphs.com)

If you think BlackRock deserves an 18x or a 20x multiple, investors are likely going to see double digit returns from here, barring a significant downturn in the markets. BlackRock is a solid business at a fair price for investors that want to own a piece of the passive investing pie. Another thing that might attract investors to BlackRock is the capital return program.

Dividends & Buybacks

BlackRock has an impressive history of dividend growth, with a dividend increase every year since 2009 (they didn't cut the dividend in the financial crisis either). Shares currently yield 2.6%. I think that as long as the market’s overall trend is up and to the right, BlackRock investors can expect continued dividend increases. They have also been buying back stock at a decent rate. The company repurchased 1.4M shares for $1.2B in 2021 and have 3.6M shares remaining on buyback authorization. I have mixed feelings about buybacks, especially with the valuation in 2021, but I think the buybacks are going to continue and might even accelerate if we see continued share price weakness.

Conclusion

If you think passive investing is going to continue to grow, owning shares of BlackRock is a great way to play it. Shares are starting to come into fair value after selling off by more than 20%, but I think T. Rowe Price (TROW) is more attractive today. I’m not a huge fan of passive investing, the ESG movement, or BlackRock, which have created distortions in the market that contrarian active investors can take advantage of. The company has a history of growing AUM, but weaker market conditions could lead to lower returns for BlackRock investors. I prefer T. Rowe Price (you can read my recent article here), but investors that prioritize dividend growth and think that the overall markets are going to march higher might choose BlackRock.

I would be fascinated to hear your thoughts. Feel free to leave a comment below.