BrianAJackson/iStock via Getty Images

Investment Thesis

VICI Properties (NYSE: NYSE:VICI) is a leading gaming and hospitality REIT that owns and acquires casinos and hotels around the U.S. They own premier casinos like Caesars Palace, Harrah's, and Venetian and collect rent from the operators based on a triple net lease. Since VICI's formation, it has grown at a rapid pace, and they now hold an investment volume of $29.5 B.

During the pandemic, the market sentiment soured on leisure and hospitality industry because people were traveling significantly less. However, VICI still had no problem collecting rents from their high quality tenants. Now, as we leave the pandemic, I expect VICI's stock price to return close to its pre-pandemic level, and investors should grab the stock now. I believe VICI is a great investment for a long-term dividend growth investor because:

- VICI owns a very strong portfolio that is well diversified on both a geographic and business basis.

- VICI has a favorable lease structure with built-in growth and inflation protection.

- They have a strong financials and stable cash flow from their portfolio.

Diversified Portfolio

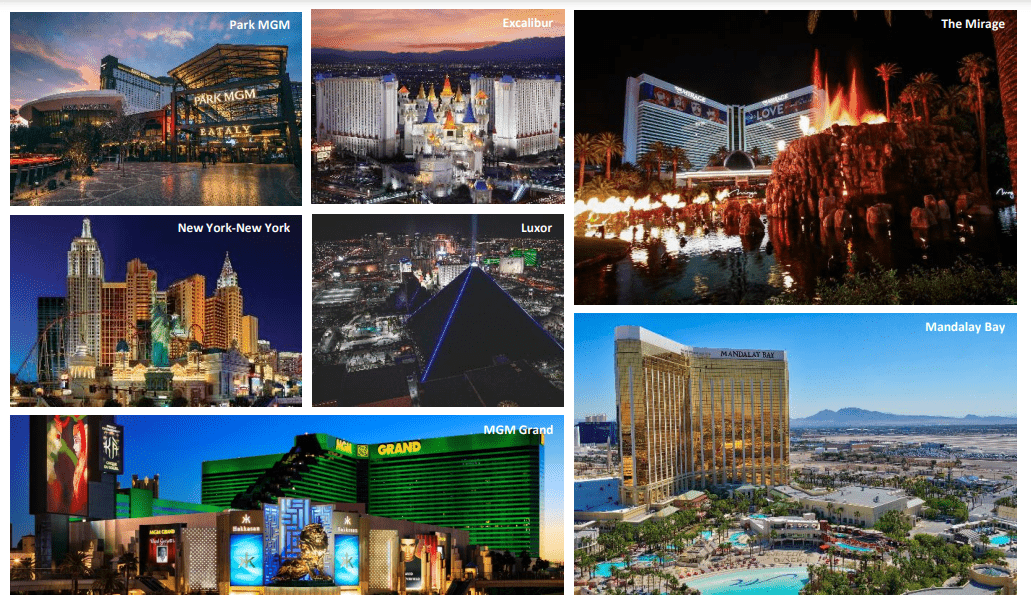

Investors in the real estate business say that there are three very important things to consider when you make an investment decision: location, location, location. In that regards, VICI is clearly making the right choices. Their portfolio includes the Venetian Resort, Harrah's, and Caesars Palace, and these hotels are often considered as the best in Vegas. They own the cream of the crop.

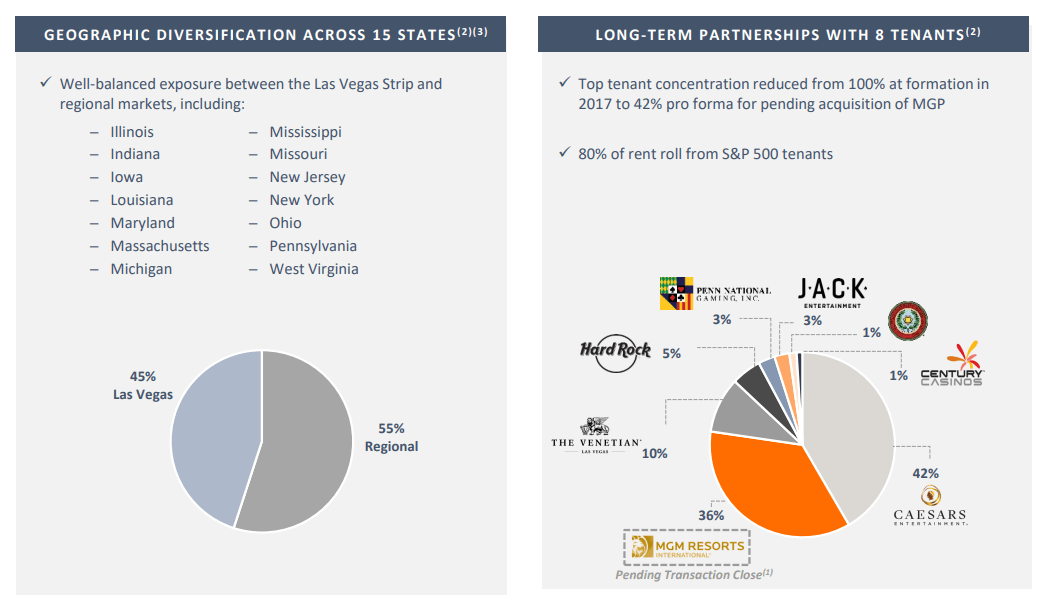

Not only that, they own many premier hotels spread across the U.S., covering 15 different states and multiple markets. Also, they have multiple revenue streams including gaming, food, beverage, and entertainment. They serve a wide range of customers with different needs and economic scales. This geographical and business diversification protects them from single market exposure and provides multiple income streams.

VICI Portfolio (VICI Investor Relations) Diversified Portfolio with Top Quality Tenants (VICI Investor Relations)

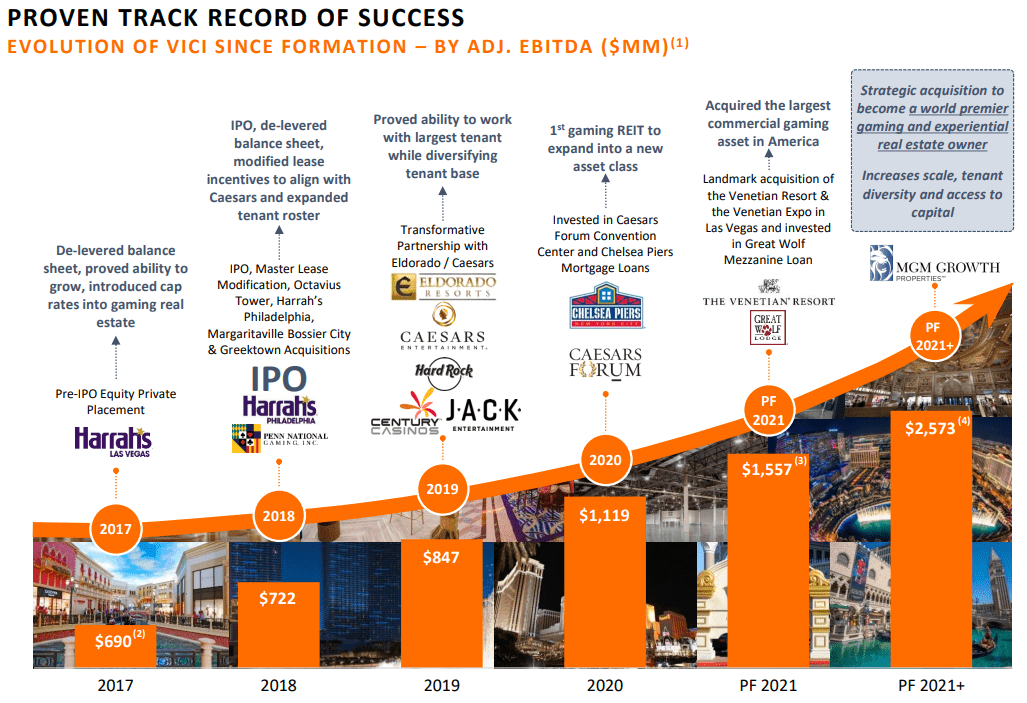

This impressive and diversified portfolio didn't happen by accident. Since formation, VICI consistently has managed to make key acquisitions to improve their portfolio. Some of the recent acquisitions include Venetian Resort (the largest commercial gaming asset in the U.S.) and MGM Growth. Based on their strong financials, I expect VICI to continue to grow their portfolio and increase their dominance in the leisure and hospitality industry.

VICI Growth Track (VICI Investor Relations)

Favorable Lease Structure

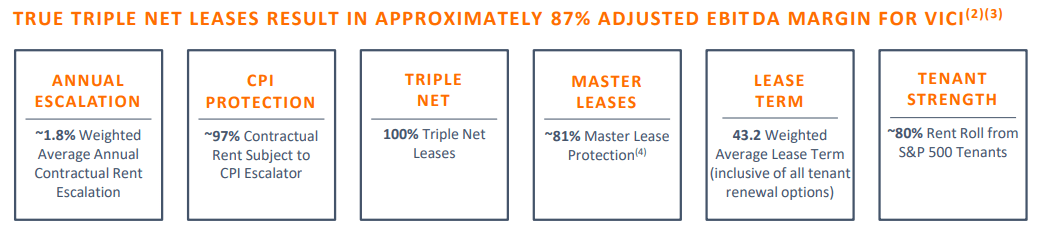

VICI has many favorable terms in their lease structure that ensure strong cash flow. First and foremost is the triple net and the master lease structure. These two terms require tenants to pay expenses related to operating the properties. The expenses include insurance premiums, repairs, maintenance, and utilities. Because of these, VICI doesn't really have to deal with any large unexpected outflows of cash.

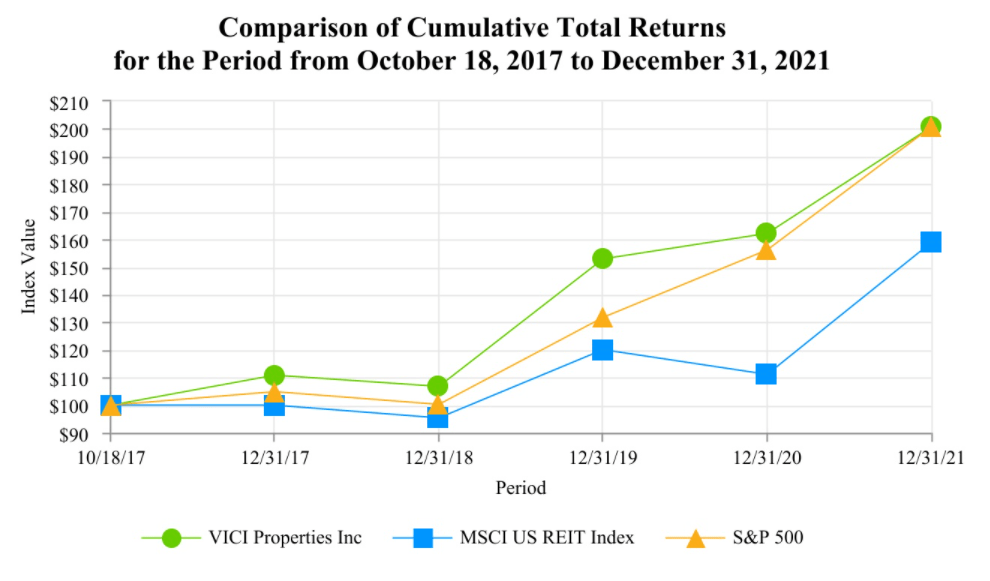

The next part is an annual escalator and CPI protection. Each year, the rent escalates automatically, and there is a further adjustment based on the inflation rate. These two terms are especially valuable during the current time of high inflation. Also, they have pretty strong tenants (Venetian, MGM, and Caesars) with long term leases. Combining these favorable lease terms with the prime locations of their properties, VICI has a strong and stable cash flow that is steadily increasing (AFFO growth 8.37%, 3 year average). Not surprisingly, they have been performing far better than the sector benchmark (U.S. REIT index), and I expect them to continue outperforming the sector for awhile.

VICI Lease Structure (VICI Investor Relations)

Comparison among VICI against benchmarks (SEC Filings)

Strong Financials and well managed debt

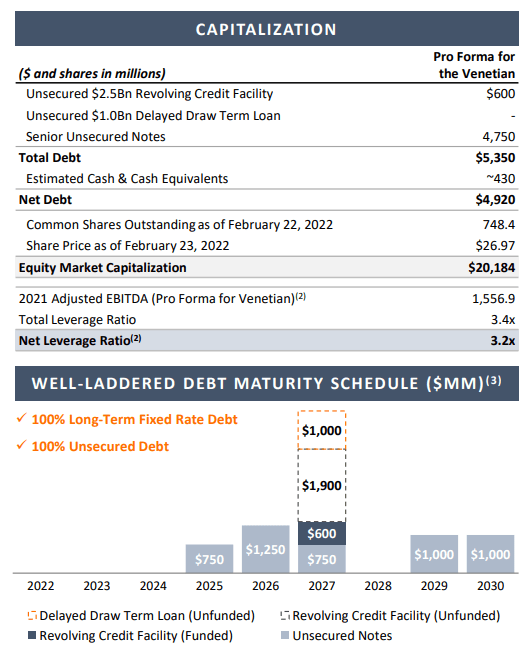

VICI has strong financials and well managed debt. Their adjusted EBITDA ($1,556.9 M) covers nearly a third of their total debt, and the debt is well distributed. They have no debt maturing until 2025, and the maturing debts are evenly spaced between 2025 to 2030. The debt is already well managed, and should further improve following the pending acquisition of MGM Growth. Management is targeting an investment grade rating from S&P, Fitch, and Moody's, which will allow them to access a larger financial pool for future acquisitions and improvements.

On top of this, their capitalization and balance sheet are heading in a promising direction. Since formation, they raised $12 B of common equity (more than any other REIT in the US over the period), and they lowered their leverage from 8.5x of adjusted EBITDA to 3.2x of adjusted EBITDA. Based on the strong cash flow (even during the pandemic) and management's commitment to improving their balance sheet to achieve investment grade, I expect their balance sheet will remain strong for the foreseeable future.

VICI Financials (VICI Investor Relations)

Fair Value Estimation

Looking at their valuation metric (P/AFFO and P/FFO), they are at the lower end of the sector. Their TTM P/AFFO is at 15.13x against the sector median of 19.96x, and their TTM P/FFO is at 15.65x against the sector median of 17.82x. I believe this weak valuation stems from the overall negative sentiment toward the leisure and hospitality industry during the pandemic, and VICI's stock price hasn't yet recovered.

As we come out of the pandemic, I believe that market sentiment toward leisure and hospitality businesses will improve. Also, based on their strong cash flow, premier portfolio, and solid balance sheet, I expect VICI will continue to perform better than the overall industry. Therefore, I expect the stock price to rise at least to match the sector median, which represents about 20% upside from the current level, along with a 5% dividend.

Risk

The Federal Reserves announced the interest rate hike schedule for the next couple of years: 6 times this year and 3 times next year. I think the hike schedule is a little too late and abrupt. The rapid increase of the interest rate could cause an economic downturn, which in turn would reduce travel and leisure spending. These factors may negatively impact VICI's business. Therefore, investors should monitor the macro economic indicators.

Also, rising interest rates will increase the financial cost, which will impact the funds available for the acquisition of a new property. Therefore, it may slow VICI's growth rate. Although, the high borrowing cost may lower property prices, so the effects could offset each other.

Conclusion

VICI owns several premier casinos in Las Vegas, and holds a diversified portfolio. Due to strong tenants and a favorable lease structure, they have a superb and steady ability to generate cash flow. Their strong cash flow and balance sheet has enabled them to acquire premier casinos and affiliated businesses to diversify their portfolio. An economic downturn and high interest rates may slow growth somewhat, but I see them as positioned well for the long term. I expect 20% upside with 5% dividend going forward.