Bill Pugliano/Getty Images News

Homebuilder PulteGroup (NYSE:PHM) is selling at a 3.8 P/E ratio as I write this. Stocks don’t sell at 3.8 P/Es without the assumption of impending disaster. One disastrous assumption could be an extended recession/depression. If that sounds right to you, stop reading this article now, pack up your canned goods and head for the hills. The other possible one is that the very sharp rise in mortgage rates this year will shut down a housing bubble the country has experienced the past two years.

As you could probably guess from my buy rating on Pulte, I disagree with the bubble thesis. A surge in asset prices like U.S. housing has experienced – a 34% rise over the past two years through February, according to the S&P/Case-Shiller National Home Price Index – can be due to either a supply shortage or excess demand. I will present evidence that it is the former, not the latter.

If you buy my evidence, then Pulte is a very cheap stock. I’ll review its strong Q1 and my EPS outlook to reinforce that view. Therefore, if the U.S. can dodge that depression, this stock should be up 50-100% in time.

The housing supply shortage

New housing is needed as the population grows. U.S. population growth has been slowing for several decades, which is clearly bad for new home demand. But following the end of a true housing bubble in 2007, home construction plummeted. Housing starts averaged 661,000 a year from 2008-2019, down 41% from the pre-bubble 1990s. As a result, housing got increasingly in short supply, as this chart shows:

Census Bureau

Source: U.S. Census Bureau

This chart clearly shows the excess housing supply created during the 2004-2007 housing bubble. The single-family home vacancy rate surged to 3%. And it shows that the dearth of new supply steadily used up the excess, to the point that the vacancy rate hit 0.8% during Q1 ’22, a more than 6 decades low.

To further illustrate this crucial point, here is my estimate of the numerical total housing (single family and apartment) excess/shortage, versus a 3.5% normal vacancy rate:

Census Bureau

Source: U.S. Census Bureau

As we stand today, the U.S. is short a record 1.6 million housing units! As a result, not only home prices soared. From Pulte’s Q1 earnings conference call: “According to John Burns Real Estate Consulting, their numbers indicate that…multifamily lease rates were up by approximately 13% over the prior year.”

Why housing is not in a demand bubble

Real estate, both residential and commercial, has had periods of excess demand in the past. Why? Because of too-liberal lending standards creating too much debt. That was certainly the case in the ’04-’07 housing bubble, but it is far from the case today. The evidence is very clear. First, here is an index of home mortgage lending standards; the higher the index the looser the lending:

The Urban Institute

Source: The Urban Institute

You can see the dramatic difference in lending practices today versus the bubble. And you can see that the recent home price surge was not driven by easier lending standards.

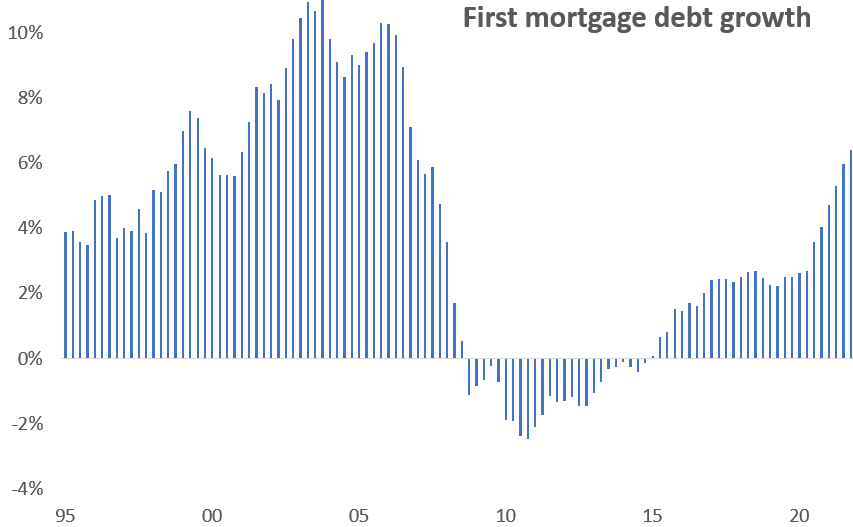

As a result, while mortgage debt growth certainly picked up to finance the sharp increase in home sales over the past two years, that growth rate is nowhere near the ’02-’07 debt bubble:

Federal Reserve

Source: Federal Reserve

The supply shortage means solid demand for new housing for a number of years

U.S. single family housing starts were 1.1 million last year, after three years averaging 0.9 million. That was far from enough – the housing shortage grew over the last four years by one million units. So, starts should at least average 1.1 million units a year going forward. Will they do so in every year? Probably not. Higher interest rates and a possible recession should push starts lower next year. But starts should recover in order to reduce the supply shortage. I therefore assume that homes sold for Pulte and its peers over the next four years will average about their ’21 levels.

What all this means for Pulte. We start with Q1

Here are the highlights:

- Pulte earned $1.83 in operating EPS, up by 43% from the prior year. You don’t expect that kind of growth in a 4 P/E stock, do you?

- Pulte’s gross margin was 29.0%, up by 3.5% from a year ago, and its widest margin since at least prior to the ’04-’07 bubble.

- It bought back a remarkable 4% of its stock during the quarter.

- Closings (deliveries of finished homes) were flat with last year, but the average price was up 18%.

- New orders fell by 19%, but the average price rose by 21%.

A lot of great numbers. But flat closings? A 19% decline in new orders? That doesn’t sound good. But these are unusual times, as Pulte noted on its earnings call:

“Our production time lines extended by about one week in the first quarter and now stand at 145 days to 150 days in most of our divisions [due to supply chain issues]. With our production cycles remaining extended, we continue to tightly control sales in most of our communities across the country. We appreciate these restrictions can be frustrating for consumers, but it is the right strategic decision given overall conditions. From both the customer experience and a business risk perspective, it doesn’t make sense to extend our backlog out a year or more just to record another sign up.”

“Between delays in municipal approvals and extended land development time lines, it is taking longer for some communities to open for sale.”

In other words, various roadblocks both made construction more time-consuming and Pulte less willing to sell homes. But:

“Consumer interest in purchasing a new home remained high throughout the quarter. With few exceptions, demand was strong across all the price points, buyer groups and markets that we serve.”

So, sales were not lost, they were just shifted to future quarters. That’s not so bad, is it?

My earnings forecasts

I expect Pulte to earn $11 a share this year and then $9 a share over the next three years. Wall Street analysts, as collated by Seeking Alpha, are even more optimistic. They agree with my ’22 number and expect the company to earn about $11.50 in both ’23 and ’24. My key forecasts are:

- Pulte closes 31,000 homes this year (the company forecast), 28,000 next year and then back to 31,000 for ’24 and ’25.

- The gross margin is 29.5% this year and steadily drops to 23.5% by ’25. This assumption is pretty conservative given that the bulk of land for the homes it will sell over the next four years were bought before the past two years’ run-up in home prices.

- Operating expenses average 9.5% of sales this year (company forecast) and then rise to 10.5%.

- Pulte continues to aggressively buy back its shares. This has been a long-term company policy. Pulte had 387 million shares in 2013. Now it has 245 million, a 37% decline. The combination of very strong cash flow and a low valuation will allow Pulte to further significantly reduce its share count by ’25. I expect 193 million, or another 21% decline. That means a 21% permanent increase in EPS.

Valuation. This stock is dirt cheap

Let’s take a look at price-to-book, a common valuation measure for homebuilders. This chart shows a 12-year history for Pulte, and a 31-year history for fellow homebuilder Toll Brothers (TOL), which makes this long-term data easy to calculate:

Pulte/Toll financial statements, Yahoo Finance

Sources: Pulte financial statements, Toll Brothers financial statements, Yahoo Finance for historical price data

First, the valuation changes for Toll and Pulte were similar over the past decade, so assuming it was so during the prior two decades seems reasonable. Second, the only time Toll’s price/book was at its current level was during the housing bust of ’07-’11. During those years Toll lost a cumulative $6 per share, or nearly 30% of its beginning book value. Pulte did even worse, losing a cumulative $22 per share, or 80% of its book value.

So, same prices-to-book as in ’07. But a very different earnings outlook. Seeking Alpha’s Wall Street analyst survey says that Pulte will make a cumulative $34 a share over the next three years, or more than 100% of its current book value. And Toll Brothers is expected to earn $33 per share over the next three years, or 75% of its current book.

Yes, I know. Wall Street analysts can be wrong. Even a lot wrong. But they are going to have to be dramatically wrong for Pulte to be worth only its current $42 a share. Pulte would basically have to break even over the next three years. Which will take one whopper of a recession.

The bottom line - Buy

If you aren’t already packing canned goods preparatory for heading to a mountain cabin to ride out the coming depression, I suggest you buy Pulte stock. Or pretty much any homebuilder stock. Their current prices will turn out to be exceedingly cheap.