Morsa Images/DigitalVision via Getty Images

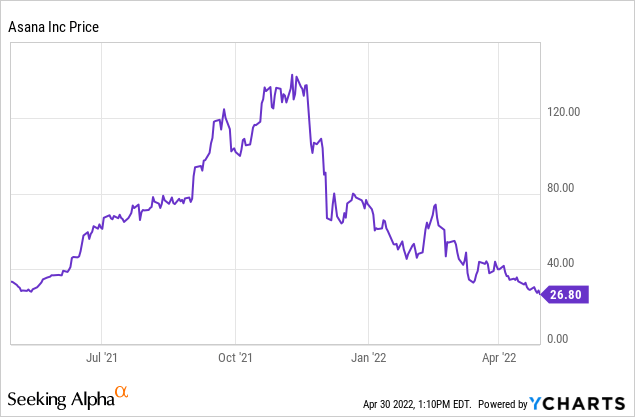

Today, the stock market is chock-full of really big losers in the tech space, but among them Asana (NYSE:ASAN) stands out as a poster child for former high-flying investors favorites that have been delivered a gut-wrenching reality check in 2022.

In 2021, Asana was riding a high. Its growth rates soared above 70% y/y, investors were buying the company for the remote-work story (as Delta and Omicron raged and school/office returns were delayed, pandemic stocks and remote-work enablers like Asana kept marching up to new highs, defying polite valuation multiples), and bulls kept breathlessly extolling the virtues of having a superstar founder/CEO like Dustin Moskovitz (who formerly co-founded Facebook) at its helm.

Today, however, those bulls are nowhere to be found. Asana has shed 60% of its market value this year, and is down more than 80% from all-time highs above $145. There comes a point in every correction when investors have to pause and rationally survey the damage, and I think that time has come now.

In January, when Asana was trading in the ~$60 range, I issued a cautionary note saying that despite recent losses, Asana's valuation was still rich and the stock still had more to lose. I held off on buying back then, and that call turned out to be prescient. Today, however, I believe Asana has found its permanent bottom in the mid-$20s, and I'm upgrading my view on Asana to bullish.

For investors who are unfamiliar with this stock, Asana is a work collaboration platform whose goal is to help information workers do their jobs more effectively. Asana's aim is to eliminate "work about work" and provide a systematic plan of record for teams to be able to effectively drive projects without wasting time. Asana's online tools allow teams to see "who is doing what, by when, and why."

Here, in my view, are the top reasons to be bullish on Asana:

- Asana's long-term demand will be bolstered by the ongoing shift to remote and distributed teams. More and more companies are embracing a distributed working model, if not a fully remote one. With fewer in-person touchpoints, software tools become critical to keeping teams together and in sync.

- Massive global TAM. Asana believes it has a $51 billion TAM by 2025, and is applicable to the global base of ~1.25 billion information workers. By that metric, Asana's current user base represents only <5% of the global eligible workforce.

- Land and expand. Asana adopts the classic software go-to-market playbook, which is to prove its concept and value with smaller teams at first, but eventually expand to entire organizations and companies. Dollar-based net retention rates are clocking in above 140% for companies spending more than $50,000 annually on Asana, a leading indicator that Asana's traction among larger enterprises is growing.

- Continuous innovation. The company added over 200 new product features in calendar year 2021, and in February 2022 unveiled a new workflow tool.

- Huge gross margin profile. Asana's pro forma gross margins hit 90%, making it one of the highest-margin software companies in the market. While the company isn't profitable today, that gross margin profile gives Asana plenty of leeway to scale profitably when it's larger, as nearly every dollar of incremental revenue flows through to the bottom line.

Asana's valuation has also never looked as modest as it does today. At current share prices near $27, Asana trades at a market cap of $5.07 billion. After we net off the $314.8 million of cash and $34.6 million of debt on Asana's most recent balance sheet, the company's resulting enterprise value is $4.79 billion.

Meanwhile, for the upcoming fiscal year, Asana has guided to a revenue range of $527-$531 million, representing 39-40% y/y growth. Considering Asana exited Q4 at a rapid 64% y/y growth rate, I do think there is a good deal of conservatism underlying this forecast:

Asana FY23 outlook (Asana Q4 earnings release)

Nevertheless, if we take the midpoint of this outlook at face value, Asana trades at 9.0x EV/FY23 revenue - which is quite cheap for a company expected to notch ~40% y/y growth, and which once commanded valuation multiples north of >20x forward revenue.

Don't let current pessimism cloud your rational judgment on Asana. I continue to view Asana as an attractive software product with secular remote-work tailwinds driving its growth, which benefits from a purely recurring-revenue profile on top of sky-high gross margins. I also take comfort in the fact that M&A activity in tech has continued to remain healthy, so if Asana continues sliding, there is almost certain to be a white-knight buyer who will be window-shopping to snap up Asana at low prices.

Buy the dip here, and buy it aggressively.

Q4 download

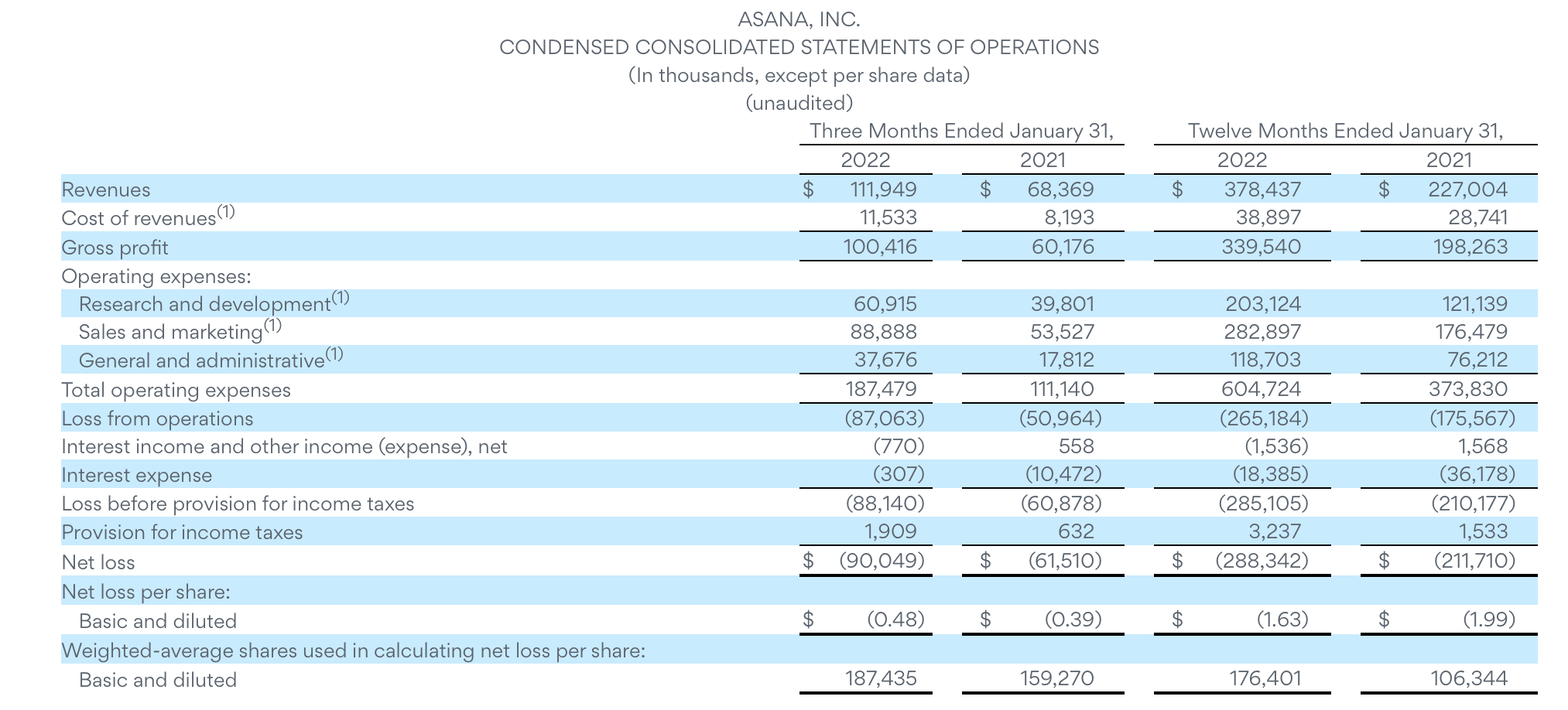

The slide in Asana has been a matter of pure sentiment, and not fundamentals - which have continued to soar above expectations. Let's now discuss Asana's Q4 results in greater detail. The Q4 earnings summary is shown below:

Asana Q4 results (Asana Q4 earnings release)

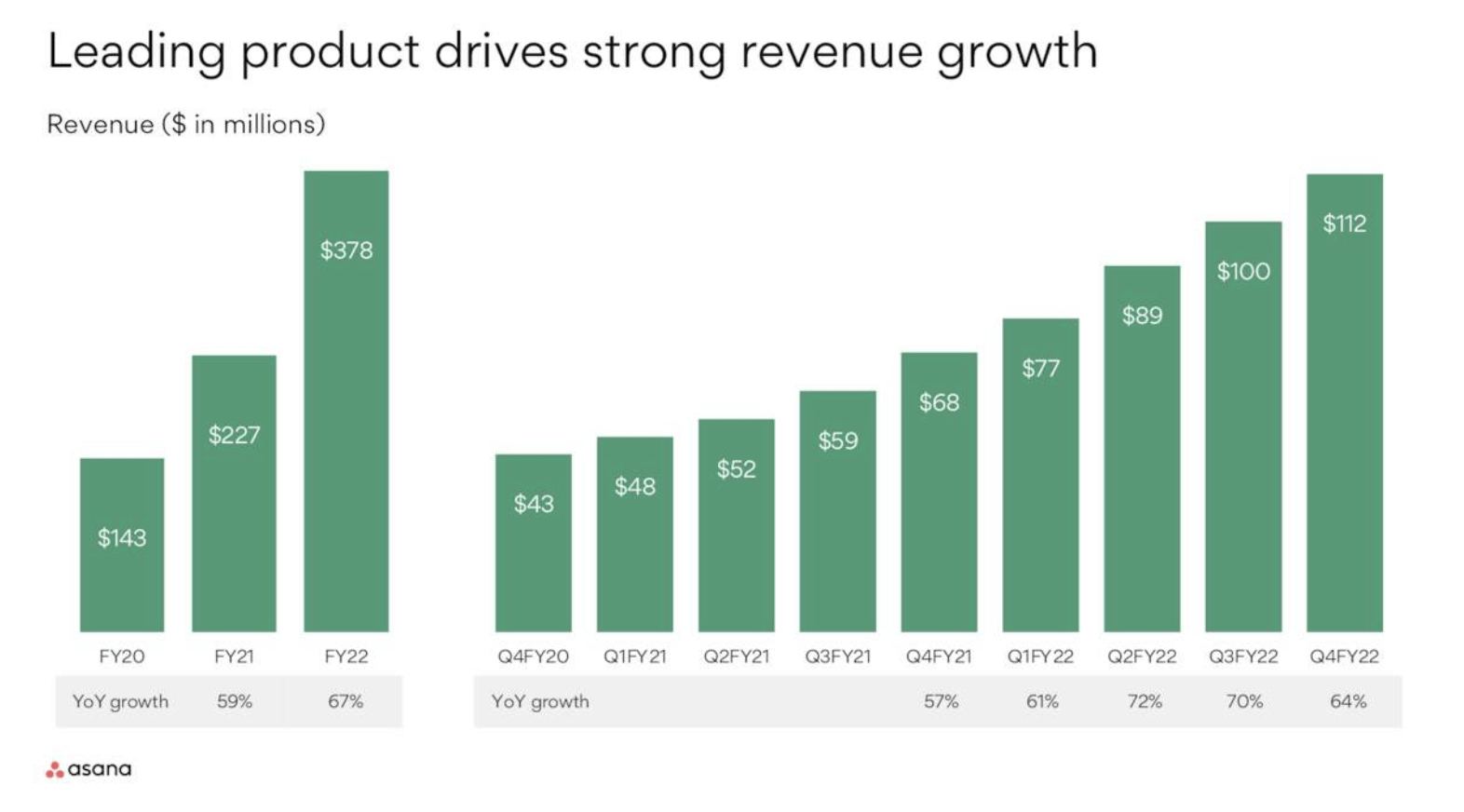

Asana's revenue grew at a 64% y/y pace to $111.9 million, beating Wall Street's expectations of $105.2 million (+54% y/y) by a major ten-point margin. Also, you can see in the chart below that Asana's recent pace of 60-70% y/y growth has seen barely any deceleration over the past several quarters:

Asana growth trajectory (Asana Q4 earnings deck)

I find it difficult to believe that Asana's growth rates will come down to 49-51% y/y growth next quarter as indicated in its Q1 guidance. For the current Q4 as well, Asana had only guided to 53-54% y/y growth back in Q3 - the company has adopted the tried-and-true playbook of setting expectations low and creating a nice "beat and raise" cadence throughout the year. The more likely scenario, in my view, is that Asana continues to outperform its guidance and Street expectations by ~10 points as it has done this quarter.

The expansion environment has also remained strong, proving the validity of Asana's land-and-expand sales model. Dollar-based net retention in the quarter hit 120%, and among customers spending more than >$50k annually, retention was 145%. The count of customers spending more than >$50k, meanwhile, grew 125% y/y to 894 customers, while the company ended Q4 with a total global base of 119k paying users.

Looking ahead to sales momentum next year, CFO Tim Wan noted that he expects a backend-loaded FY23, with more sales capacity ramping/maturing in the back half of the year. Per his prepared remarks on the Q4 earnings call:

In terms of the shape of the quarterly progression, we expect to see a more traditional enterprise sales seasonality with our sales capacity ramping towards the second half of the year as our mix continues to evolve towards a sales-led motion. Given the large untapped opportunity ahead and along with the success we've seen in fiscal year '22, with the Work Graph scaling to 25,000 and 50,000 seats and beyond, we are increasing our investments to expand the functionality required by large and complex enterprises and further investments in our go-to-market motion in the form of increasing our sales capacity and customer-facing teams to support adoption and expansion within many of our larger enterprise customers."

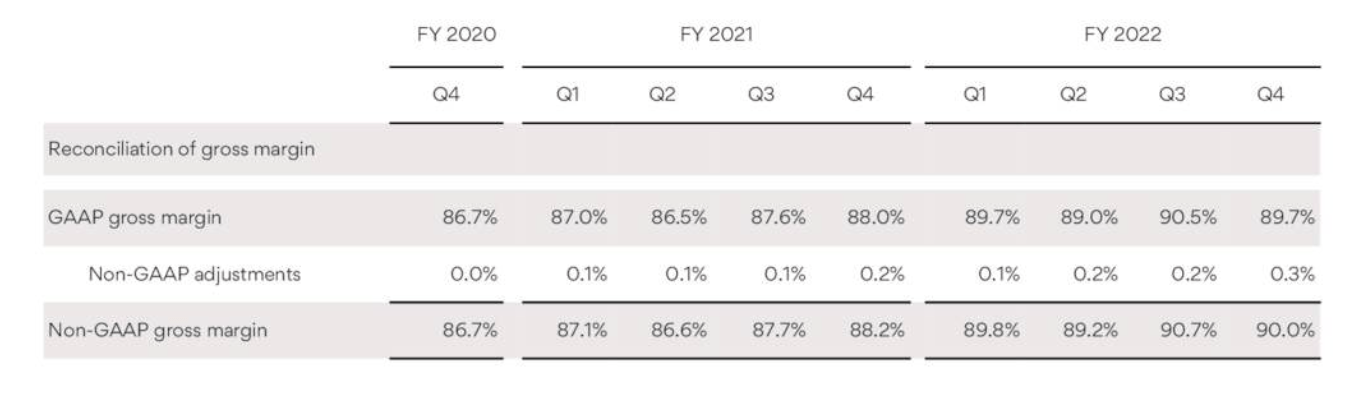

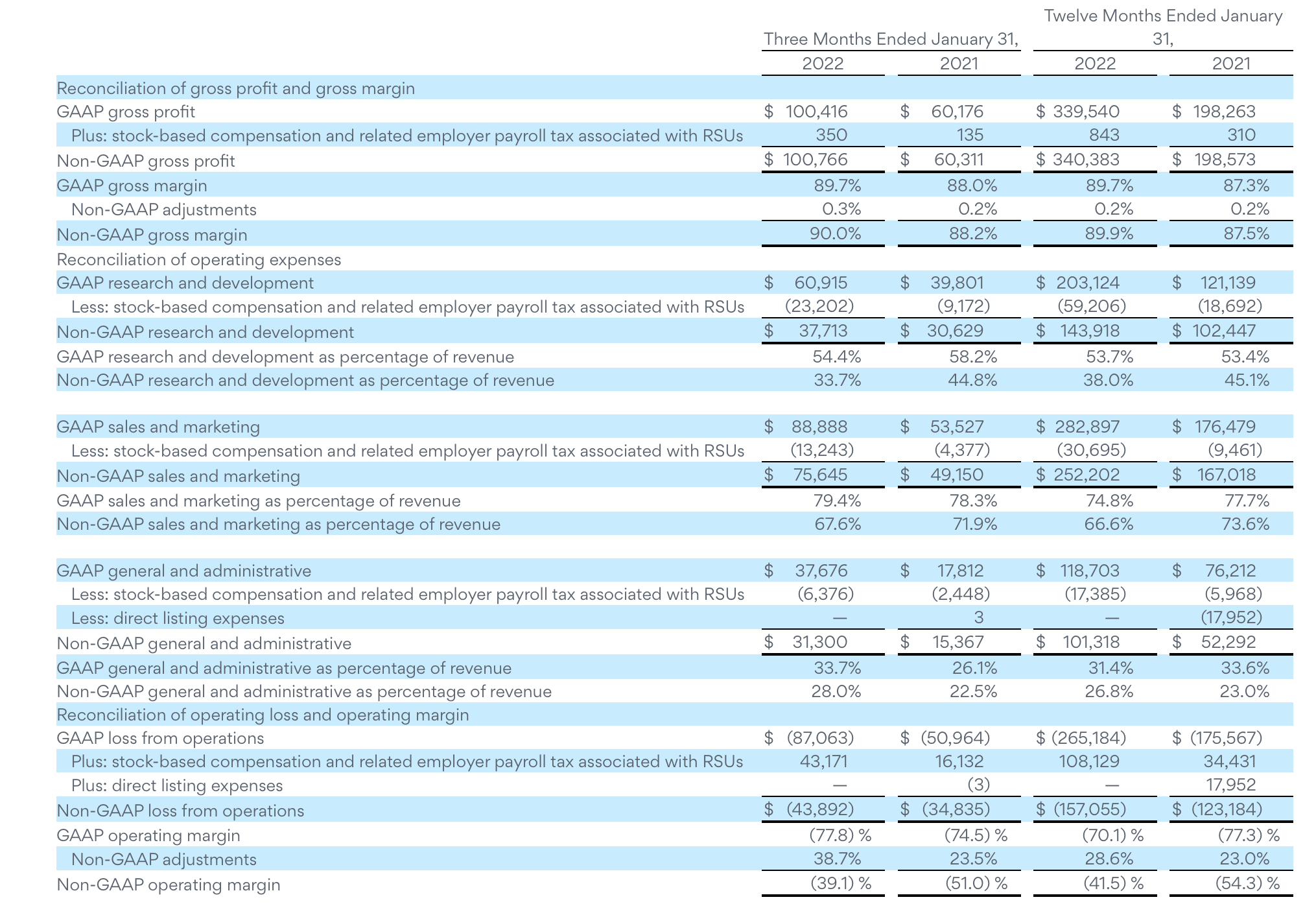

Gross margins in Q4 improved 180bps to 90.0%, as shown in the chart below. Again, I'll emphasize here that Asana is in a league of its own when it comes to gross margin - most SaaS peers have margin profiles closer to the mid/high 70s:

Asana gross margin trends (Asana Q4 earnings deck)

Now, admittedly, Asana's overall losses are still high, and a big reason why Asana shares have pulled back in this safety-oriented stock market. Pro forma operating margins in Q4 were a staggering loss of -39.1%, though that's twelve points better than -51.0% in the year-ago Q4.

Asana pro forma operating margins (Asana Q4 earnings deck)

I'm comforted on Asana's losses for two primary reasons. First, Asana's high gross margin profile means that at a larger scale, Asana will eventually be able to capture operating leverage on its fixed expenses and grow its bottom line. Second, Asana burned through "only" $88 million of cash in FY22, versus the $315 million of cash it has on its current balance sheet. Despite heavy losses here, at its current burn rate, Asana has sufficient liquidity to last for several years without needing to raise additional capital.

Key takeaways

Any time a stock is down ~80% from highs, it's worth at least a look. In Asana's case, while a steep valuation correction was certainly necessary after the stock's unsupportable rally last year, as usual investor sentiment took this correction way too far. Take advantage of the temporary dislocation to build up a well-timed position in this fantastic SaaS player.

For a live pulse of how tech stock valuations are moving, as well as exclusive in-depth ideas and direct access to Gary Alexander, subscribe to the Daily Tech Download. Highly curated focus list has consistently netted winning trades of 40%+.