noel bennett/iStock Editorial via Getty Images

It's earnings day for Dufry (OTCPK:DUFRY) (OTCPK:DFRYF). For a few weeks now, we have been analyzing travel & leisure recovery and the Swiss group came up in our internal screening. Considering macro and micro reasons, our positive view was based on:

- Strategic M&A during COVID-19;

- Structural cost savings achieved during the pandemic outbreaks which were not priced in;

- Partnership with Alibaba and Hainan to invest together in some opportunities in China (mainland and islands) to develop the travel retail business in the country (where Dufry has a marginal presence) and also to strengthen the company's digital transformation.

A new potential business combination

There are rumors of a possible merger with Autogrill (OTC:ATGSF; ATGSY) and Dufry recently announced that it is interested in evaluating various strategic opportunities in the sector. In the past, Autogrill's main shareholder has indicated that it is open to diluting its stake below 50%, especially in the event of a transformation involving a merger with one of its main competitors. Although there might be other players interested in Autogrill such as the English SSP or the French group Lagardere (OTCPK:LGDDF), our internal team believes a deal with Dufry is more likely to happen, also because Hudson, recently de-listed by Dufry, one of the largest travel retail operators in North America with 2019 revenues of around €2 billion has always been the natural target for Autogrill. Synergies in North America would be significant. This deal would create a global company with €12.5 billion in sales in 2019, very diversified at geographical level but also by business lines and by channel (Autogrill sales: 65% airports, 50% USA, almost 100% Food & Beverage. Dufry sales: 88% airports, 40% Americas with an important market share in Brazil, 60-40% Duty-free / Duty-paid) Our preliminarily estimated value of the combined synergies at the EBITDA level: $80-$100 million when fully operational or 0.7 / 0.9% of the combined cost base in 2019.

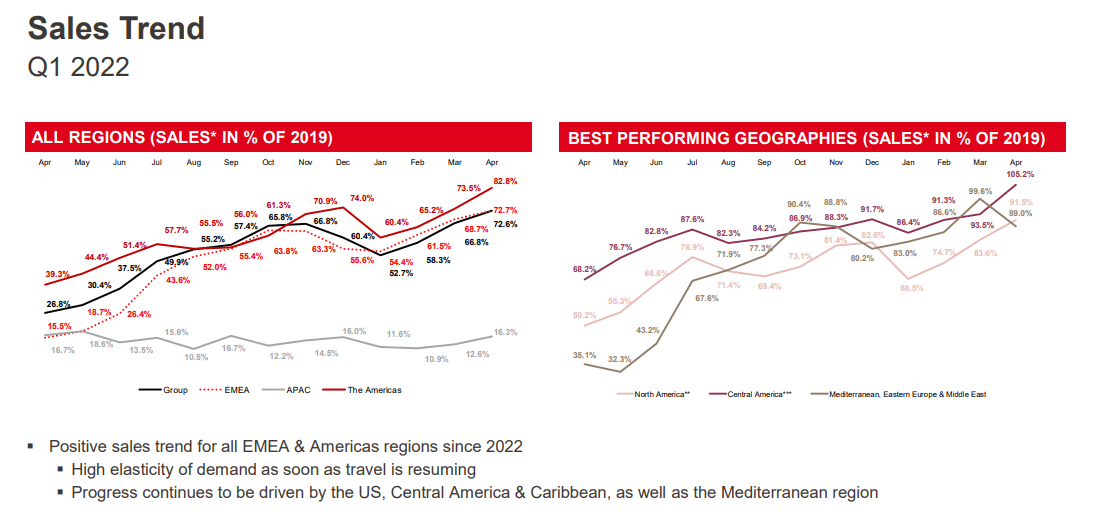

Q1 results

Financially speaking, today Dufry released its quarterly statement. Q1 results were driven by EMEA progress and by a positive contribution to the American region. As we expected, despite most geographical areas recovering, APAC countries with their zero COVID tolerance policy continue to lag. Here below is the comparison of Q1 2022 versus Q1 2021 and Q1 2019.

Dufry Q1 Sales (Q1 Press Release)

Dufry is progressing with recovering sales and most importantly, FCF. From a seasonal point of view, we can note that FCF stood at CHF -86.8 million in Q1 2022 a strong performance even compared to the pre-COVID-19 impact in Q1 2019 when the company was also in negative territory at CHF -123.0 million. This was due to the structural cost saving that the company has undertaken over the last two years.

Dufry Q1 FCF (Q1 Results)

Valuation

Our internal team believes that Dufry is better positioned to navigate short-term turbulences. Thanks to the cost management improvement, the company is also more profitable than in the pre-COVID-19 era. We are not adjusting our estimates on a potential deal with Autogrill, even if we see this as a positive catalyst. Sales trends are positive and we expect a pretty strong summer season.

Dufry Q1 Sales Trends (Q1 Results)

Thus, we maintain our target price of CHF 50 based on a three-stage DCF model with a WACC of 8% and a long-term growth rate of 2%. More details about the valuation and risks are in our previous publication.