Pascal Le Segretain/Getty Images Entertainment

Company Description

LVMH Moët Hennessy Louis Vuitton (OTCPK:LVMHF) (OTCPK:LVMUY), known simply as LVMH, is a multinational French conglomerate, specializing in all things luxury. LVMH is generally considered to be the premier luxury fashion house.

LVMH operates 60 subsidiaries and 75 brands across its 5,500 worldwide stores.

LVMH categorizes its brands under the following groups:

- Fashion & Leather Goods, notable brands include Louis Vuitton

- Wines & Spirits, notable brands include Hennessy

- Perfumes & Cosmetics, notable brands include Christian Dior

- Watches & Jewelry, notable brands include Tag Heuer

- Selective Retailing, notable brands include Sephora

- Other Activities

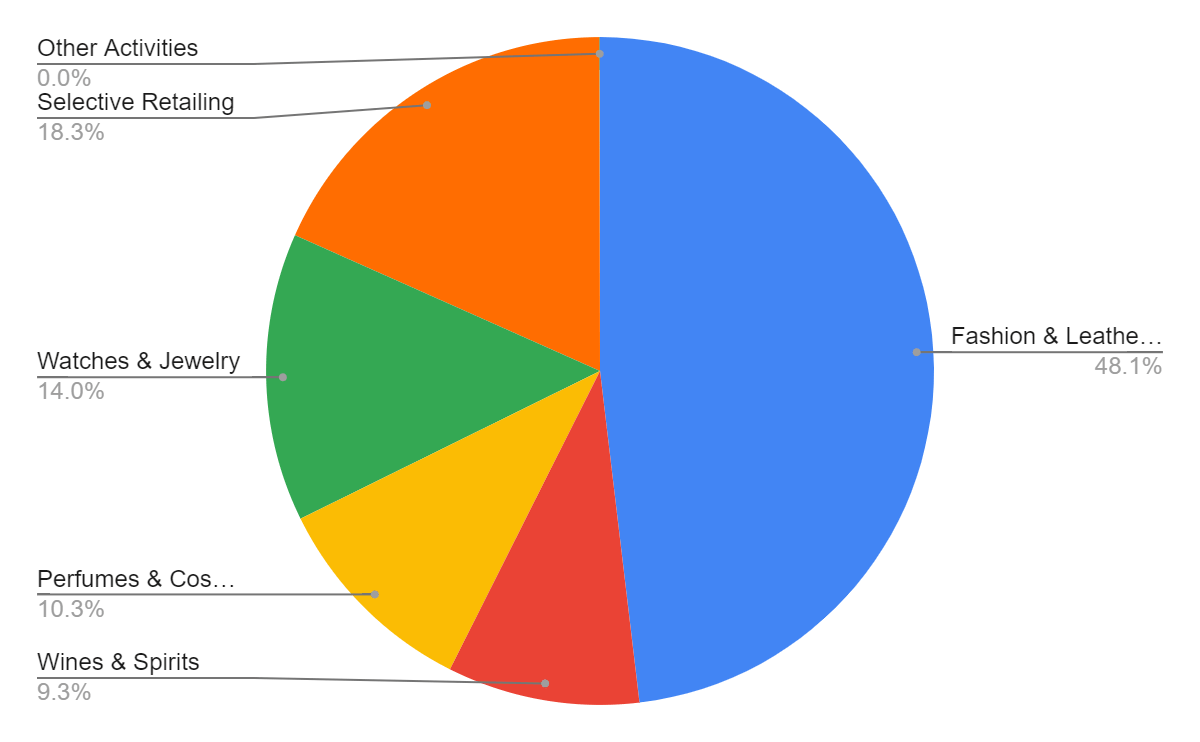

The revenue split between these is as follows:

Revenue by business line (2021) (LVMH)

As we can see, the majority of their revenue comes from their leather goods and fashion, which are the products that made LVMH so popular. Watches and Jewelry saw revenues double in 2022 and is now the 3rd largest group. This is a reflection of the boom in the Watch market over the last 2 years.

LVMH's CEO and majority owner is Bernard Arnault and his family. The story of modern day LVMH is heavily linked to the vision of Bernard and many of the brands within LVMH have family members within their management.

Investment Thesis

We see LVMH as an all-weather investment. Contrary to what may be believed, LVMH is more than capable of performing well during difficult economic conditions. Q1 2022 numbers were fantastic and is evidence of LVMH's ability to continue growing all areas of its business.

Furthermore, LVMH has been quite aggressively sold off with markets spooked by the threat of stagflation, falling 18.8% YTD. Most businesses which have retreated by such a degree have done so because of weakening performance/guidance. LVMH, as we have identified, is performing superbly.

The biggest selling point for us, however, and the reason we are suggesting this in all conditions, is LVMH's strategy and execution. LVMH is one of the best businesses in the world at marketing its products. A lot of credit can be attributed to management and means there is no reliance on any one brand/product. This should mean continued growth in the medium term and further successful expansion via M&A.

With the recent pullback in share price, LVMH's valuation has finally become indisputably attractive. Historically, LVMH has traded at a premium and rightfully so, but is currently trading below its peers. This gives prospective investors a comfortable degree of margin.

We will now consider the reasons we are so bullish on LVMH in detail, including considerations around macro factors.

Sector Analysis

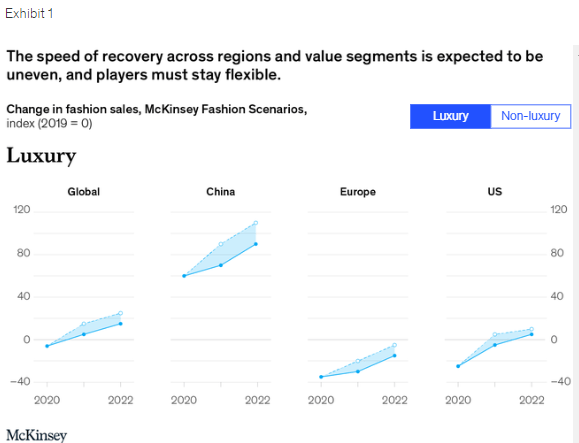

The luxury fashion industry is turbulent at the best of times, as many brands vie for consumers' attention (and wallets) with extravagant catwalk designs. The last few years have been more eventful than most. As lockdowns swept the world, retail footfall nosedived and consumers had little reason to shop luxuries. For a short time, things just stopped. However, the following year shocked most. We saw a bounce back like never before and extremely robust demand. As McKinsey's diagram below shows, China led the way.

Recovery in fashion sales (McKinsey)

According to McKinsey, there are a few key criteria to succeed in 2022. Firstly, developing a strong online presence, which was previously neglected by luxury brands who focused on the quality of their in-store experience. We note that LVMH has been growing its online presence well, opting for selective distributions in order to drive traffic to their websites.

Further, brands must continue to innovate their designs to reflect consumers' change in taste. Contrary to popular belief, luxury brands struggle with customer attrition. They are constantly under pressure to produce socially relevant designs during the two fashion cycles of the year. LVMH is in a unique position of owning brands with large market share, who are seen more so as trend setters than trend followers.

The size of the brands within LVMH thus creates their competitive advantage. They are able to 'decide' what is cool and are able to forgo short-term profits through distributors, in order to secure long-term higher margin sales. Therefore, it is illogical to bet against LVMH's brands remaining highly competitive going forward.

Economic Analysis

Macroeconomic conditions are deteriorating currently. We are seeing economic growth fall globally, likely on the back of rising interest rates and increasing cost of living.

This is problematic as if consumers have less discretionary income remaining after paying for essentials, they are less likely to spend on luxuries. With inflation remaining persistent, this is likely to be an issue for at least most of 2022.

Additionally, certain areas in China, including Shanghai, have recently returned to lockdowns. This is due to China's 'zero COVID-19' policy. This will further stifle demand in a geography which leads demand for luxuries.

Therefore, it does not take an economist to surmise that luxury brands will struggle in the short-term. However, we would argue that the macro landscape is far from clear cut.

Firstly, unemployment and wage growth in the western world are at record levels. The UK is at 3.8% unemployment and the US is even lower. As a result of this, the theoretical pool of money available for consumption is larger than ever and continuing to grow.

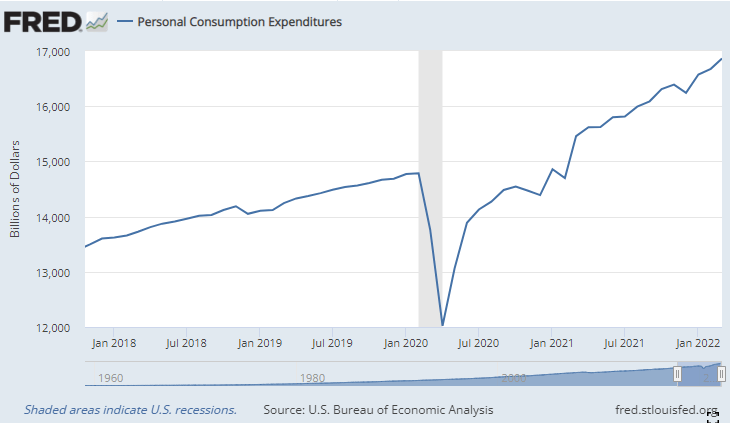

Furthermore, consumer spending remains strong and is growing, as the below shows. This does not suggest waning consumption as some suggest, although may be linked to higher prices. Given that consumption is the majority of GDP, this is an important indicator of strength within an economy.

Personal Consumption Expenditure ((FRED))

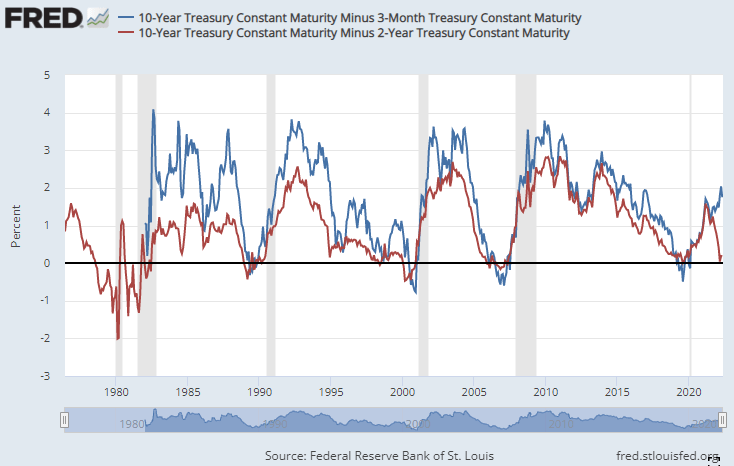

Finally, there has been much talk of a yield curve inversion, but importantly the 10Y to 3M curve has yet to invert and remains at a healthy level. Yield curves are seen as leading indicators of a recession but there is no consensus as to which one is best, most just reference the one which confirms their bias. I would argue the 10Y/3M is the best one to use for two reasons. Firstly, when compared to the 10Y/2Y curve historically, the 10Y/3M curve inverts nearer to the actual recession. This means it is better for predicting an imminent recession, when following a 10Y/2Y inversion. Secondly, inflation has muddied the economic waters and caused real uncertainty. As a result of this, 3M Treasury bills better reflect current market conditions than the 2Y, which includes market expectations for future FED rate changes.

10Y minus 3M and 10Y minus 2Y Yield Curves overlaid ((FRED))

LVMH has been fairly resilient during past economic downturns and bear markets. LVMH's revenue fell less during 2020 than its closest peer Kering (OTCPK:PPRUF), it grew double-digits in 2017 when many struggled, and only saw -0.8% growth in 2009.

This section of the analysis is not to be the last bull in the market, it is instead to consider the factors which contradict the general market sentiment. I would argue that given the contradicting information and LVMH's resilience in bear markets, we are better off assessing the fundamentals of LVMH, rather than putting significant weight into the macro analysis.

LVMH Understands You

In early 2021, LVMH acquired Tiffany & Co. Since then, we have seen heightened marketing to the general public, culminating in Tiffany's announcement that they would be releasing a limited run of Tiffany-stamped Patek Philippe 5711s. 1 of these watches, which retails for around £27k, sold at auction for $6.5MN. Within days, much of the western media were abuzz with the news. The modernization of Tiffany is in full swing, with performance impressive so far.

In January 2017, LVMH partnered with Supreme (VFC), one of the most popular brands in the world, which it ironically issued with a cease and desist 16 years previously. Since then, LVMH has noticeably pivoted towards a younger demographic, with great success.

There are many such examples of the above, and they all show LVMH successfully executing their marketing strategy. It is far from copy/paste, but clearly LVMH's management have an impeccable ability to draw attention to what their brands are doing and convert this into sales. This is personified by their purchase of high-end hotel chain Belmond. LVMH are confident they can sell anything luxury.

This deep understanding of the market has allowed LVMH to acquire good businesses and improve them within the group. Management's strategy is clear. They target businesses with powerful brands who have a healthy market share, but, for whatever reason, are not executing to their potential. Management's task then is to leverage LVMH's capabilities, alongside the strengths of the company, to propel it forward. So far, their track record is exemplary. Success stories include Rimowa, Dior and Fendi.

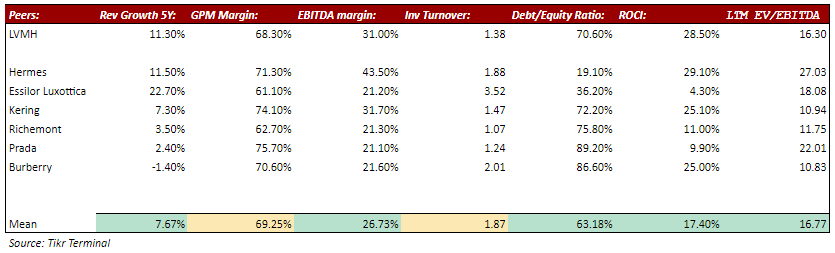

Peer Comparison

As we have mentioned, the fashion industry is highly competitive. This said, a few key players own most of the brands we know and love. Below is a financial comparison of them.

LVMH performance relative to peers (Tikr Terminal)

As the above shows, LVMH is the benchmark within its industry. It has grown faster, with superior bottom-line earnings while being more conservatively financed. Given the growth across sectors and brands within LVMH, it is clear this success is attributable to management. Therefore, we are not concerned about this superiority eroding into the future. What is surprising to us is that LVMH is cheaper than the average of its peers, even without Hermes, LVMH is cheaper.

Financial Analysis

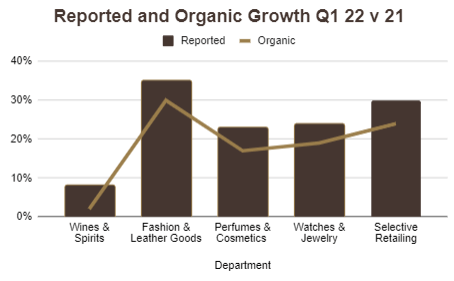

LVMH described their start to the year as 'good'. I would say 29% reported growth (23% of which is organic) is fantastic. Moreover, every department has performed well, even those that are deemed mature, like leather goods.

Q1 2022 Revenue Growth By Department v. 2021 (LVMH 2022 Investor Deck)

LVMH's core brands LV, Dior and Fendi all saw record revenue, with China and the US driving the growth.

What we believe is most impressive is the organic growth, it is clear LVMH's strategic management of its brands is market-leading. They are continually able to offer consumers what they want, across a host of different luxury segments, while fiercely competing for those sales. This is important for investors to understand as the level of M&A transactions LVMH conducts could give the impression they are bolting-on their growth.

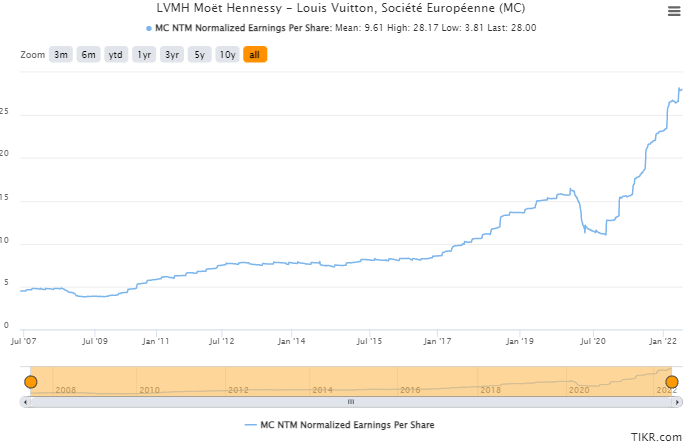

Operationally, LVMH is quite impressive. They are able to leverage their expertise across their brands and maximize economies of scale. This has allowed them to absorb much of the growth in revenue. This is visualized in the graph below.

LVMH Normalized EPS over time (Tikr Terminal)

We note that LVMH is conservatively financed and has a bullet-proof balance sheet. There are no liquidity risks.

Forward guidance looks very attractive in today's market. Analyst consensus estimates have top-line revenue growth at 15.9% and EBITDA at 11.7%, according to Tikr Terminal. This may be re-rated slightly based on macro developments but regardless, we see positive growth in 2022. When you consider this alongside the fact LVMH is down c.25% since the turn of the year, LVMH certainly looks attractive.

Valuation

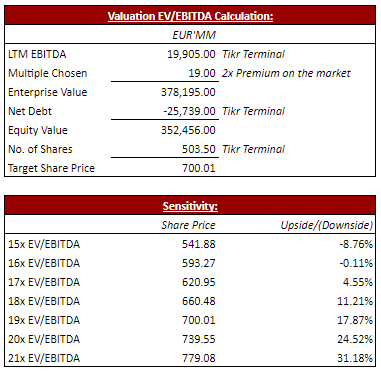

Generally, our approach is to value a business using at least 2 methodologies. However, it is difficult to apply a market-based model to LVMH as it is one of the few companies in the world which is vastly superior to its peers. LVMH should not be trading at the average of its comp set for the reasons above, although it is highly judgmental as to what premium is appropriate.

As the above table shows, peers are trading in the region of 17x their LTM EBITDA. To be prudent, we have applied a slight premium to this, to reflect LVMH's competitive advantage. One could certainly argue a larger premium than 2x. Based on this, we come to a target share price of 700.01, implying an upside of c.18%.

Market-based Valuation (Author's own calculation (Tikr Terminal))

Considering the fall we have experienced in the market, one could argue this is not an attractive return, but we are considering this from a risk-adjusted perspective. LVMH has very strong cash flows, a low beta and will likely grow its top-line in 2022. When factoring this in, I believe an 18% upside is attractive.

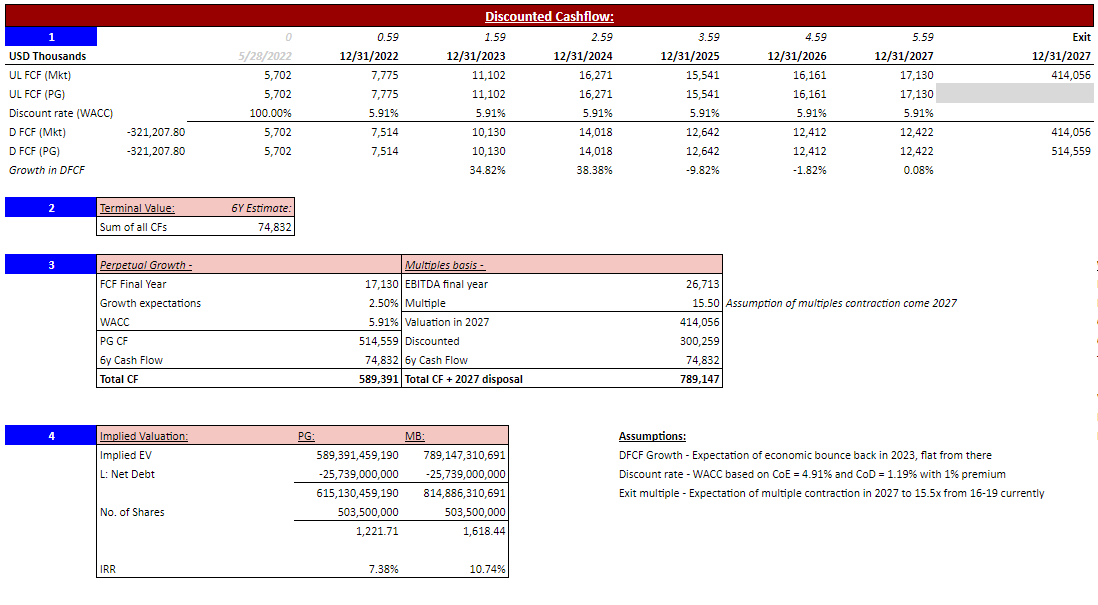

We have also considered the valuation of LVMH on a longer-term basis. We have discounted the cash flows, assuming an improvement in FCF from 2023 onwards, once economic conditions improve and LVMH benefits further from its online and direct-to-consumer push.

LVMH discounted cash flow valuation (Author's own calculation)

This implies a price target of 1,222-1,618 in 2027, representing an IRR of 7.4%-11%. Once again, this is nothing astounding, but when adjusted for the risks of this investment, we believe it to be quite attractive.

Arnault Family

We cannot have a write-up on LVMH without mentioning the Arnault family. Although it is anecdotal, many attribute the marketing and growth success we outlined above to the family members. They are arguably LVMH's greatest asset.

Bernard serves as the CEO, but all 5 of his children are senior members of the group. This includes Alexandre who led Rimowa and is now a VP at Tiffany, and Frédéric, who runs TAG Heuer.

When we look at the TAG's 329% growth e-commerce in 2020 under Frédéric, it mirrors that of Rimowa years early, which itself mirrors LVMH. Although the details will be brand-specific, the overarching strategy is in the same vein as Bernard.

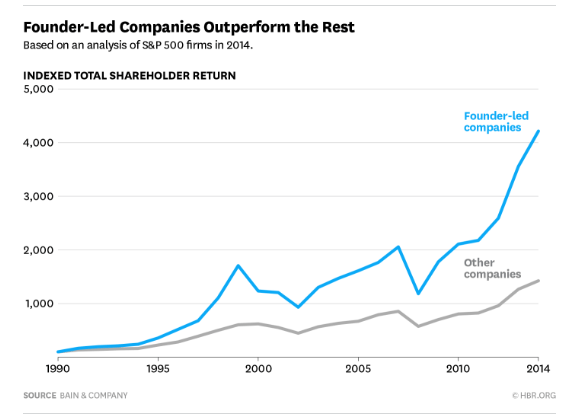

As Bain has identified, founder-led companies outperform the market, and not by a small portion.

Founder-led Companies outperform the rest (Bain)

Bain's research identifies many reasons for this but the one that resonates most with LVMH is the idea of treating the businesses money as if it is their own. Bernard takes a long-term view of his brands (and invests in this), not being concerned by short-term rewards for shareholders or pressure upon himself to impress shareholders. This contrasts most businesses where you have management acting in their own interest and shareholders demanding results now.

Investment Risks

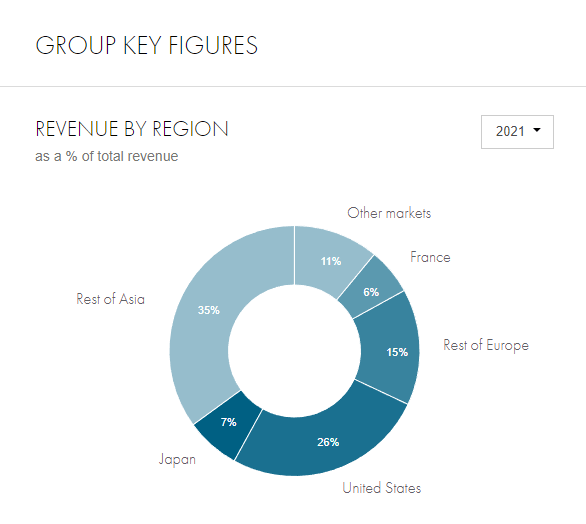

LVMH is a truly global business, generating its revenue across the world. As a result of this, there are always FX risks when converting to their functional currency. This could give the impression of falling metrics, if an adverse change in FX occurs. As the chart below shows, they are highly susceptible.

LVMH sales by region (LVMH)

At least in the short-term, however, there will likely be FX tailwinds. We are currently seeing foreign currencies strengthening against the Euro. This will mean a greater number of Euros purchased with their foreign income. See two of LVMH's most important foreign currencies below.

USD to EUR (GoogleFinance) CNY to EUR (GoogleFinance)

Furthermore, Xi Jinping, the leader of China, spoke of "common prosperity" which sent chills around the fashion world. The Chinese market is one of the largest and a key driver of growth. Although nothing has been stated to suggest a ban, for example, prospective investors should certainly follow the developments in China should they begin disincentivizing the purchase of western luxuries.

Final Thoughts

LVMH should be the definition of an economically-cyclical business. When people's wealth is growing, they should perform, and when things are bad, they should struggle. The reality, however, is very different. The Arnault family have built a business, which continues to grow strongly in-spite of what the world is doing and outperforms in most medium-term periods.

LVMH's advantage comes from the partnership between their strong brands and their strategies to grow them. Management have an unbelievable understanding of the market and are in a position to dictate tastes.

This is not a short-term investment, just like Arnault, you must invest into LVMH for the long-term. Over the decades, there have been several years of low growth, but every time the business has remained focused on its strategy and followed with strong growth.

For these reasons, we are big fans of LVMH. With economic conditions becoming more questionable, one should invest in value propositions with the ability to grow healthily, LVMH represents this. We, therefore, rate LVMH a buy.