naphtalina/iStock via Getty Images

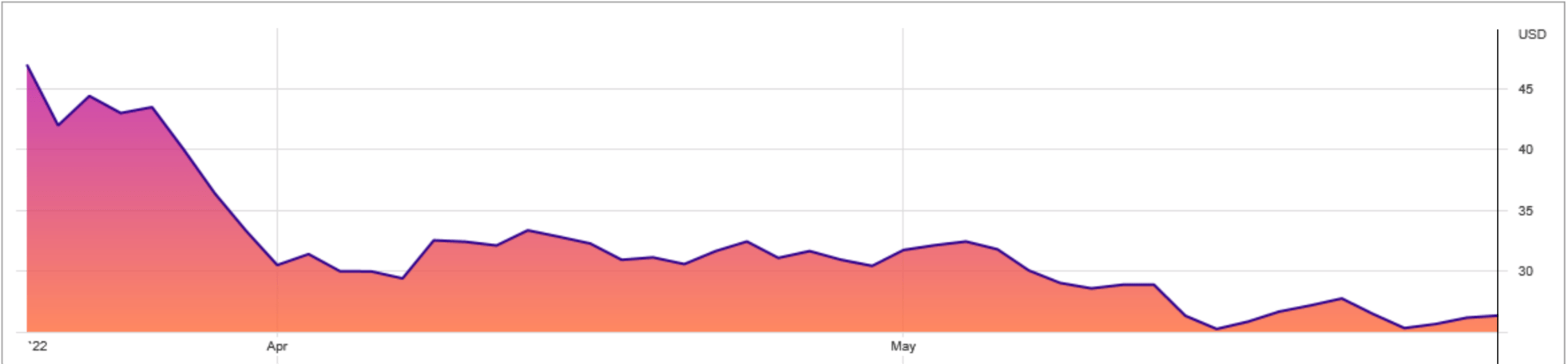

Medical devices maker BD (Becton, Dickinson and Company) (BDX) spun off its diabetes care business, Embecta Corp. (NASDAQ:EMBC), on April 1 of this year, to create one of the biggest pure-play diabetes management firms in the world, with leadership in insulin delivery. The company has a 67% market share globally in conventional pen needles. Although the spinoff is recent, the company has an established brand that spans over 100 years. In the last decade, the company has entered a period of stability in which it has reliably earned significant free cash flows (FCF) at very fat margins, and top tier returns on invested capital (ROIC). Embecta has a significant runway for stable earnings given the growing importance of diabetes in the United States and the rest of the world. Yet, despite the strong underlying business, the share price has fallen nearly 44% since the company's listing. Embecta is significantly undervalued and is a very attractive proposition.

Source: Embecta Corp.

Embecta is a Strong Performer

Between 2019 and 2021, Embecta grew revenue from just over $1.1 billion to nearly $1.17 billion, at a 3-year compound annual growth rate (CAGR) of 1.66%. Conventional pen needles are responsible for about 70% of the company's revenues, with conventional insulin syringes making up 15%, safety injection devices making up around 10% and accessories making up 5% of revenue. The company's annual manufacturing and supply agreement with BD will result in an additional revenue stream that will add $23 million to last year's revenue once they are rebased.

Operating income declined from $502 million in 2019 to $492 million in 2021, and, in tandem, net income declined from $432 million to $415 million. In that time, the company enjoyed elite-level gross margins, which declined marginally from 70.87% to 68.67%. FCF declined from $439 million in 2019 to $419 million in 2021. FCF margins in 2019 were 39.59%, declining to a still-high 35.97% in 2021. The company's ROIC has been extremely impressive, starting off at 74.83% in 2019 and declining to 74.21% in 2021.

The company's cash generation allows it to have a generous dividend payout ratio of ~20% of GAAP net income.

The company's strong, stable financial performance gives it the ability to invest credibly by partnering with pharmacies so that treatments are adhered to; bolstering their omnichannel and e-commerce business; increasing their research and development budget to drive innovation; buying or developing next-generation technologies such as an insulin patch pump. As a sign of this, the company has increased its research and development expenditure by 19.3% to $16.7 million in Q1 2022, compared to Q1 2021, according to the company's Q1 2022 10-Q filing.

The company's growth can be financed, therefore, without the company risking its capital structure. The company has built up a war chest of $265 million in cash and cash equivalents and maintained a conservative capital structure, earning Ba3/B+ credit ratings from Moody's and S&P, ensuring its Term Loan N and Senior Secured notes have an extended maturity profile and that the company has a net leverage of around 2.8x.

According to Embecta's Q2 earnings report, the company expects revenue to decline by 7% in the last six months of the year compared to the last six months of 2021. The company's report has caused the share price to decline further, but this ignores the long-term fundamentals at play, which provide support for the company's revenue, profitability and cash flow generation.

Diabetes Is a Growing Problem

According to the National Diabetes Statistics Report, 1 in 10 Americans have diabetes, with 1 in 5 who have diabetes not knowing that they have it. In addition, over 1 in 3 Americans have prediabetes, with 8 in 10 who have prediabetes not knowing that they have it. Globally, the World Health Organization reports that the number of people with diabetes grew from 108 million in 1980 in 1980 to 422 million in 2014, with prevalence growing especially among emerging countries. Diabetes is the ninth leading cause of death in the world and rates of diagnosis have been rising, and along with it, the need for treatment care. The growth of diabetes across the world is driven by lifestyle factors, demographic changes and greater access to care -which means that more people are being diagnosed with diabetes and seeking treatment.

Being diagnosed with diabetes means that the patient will have to seek treatment for the rest of their lives. So, those people with diabetes that use insulin, will have to use it for the rest of their lives.

Consequently, Embecta's position as the leading provider of diabetes solutions in the world, means that it will have a good chance of getting a good chunk of those lifetime customers. This provides a high degree of security for the company and a base for revenues.

Geographically, the United States is marginally more important to the company than the international market. Embecta's significant international presence is important given that 75% of people with diabetes are in emerging markets.

Source: 2022 10-Q

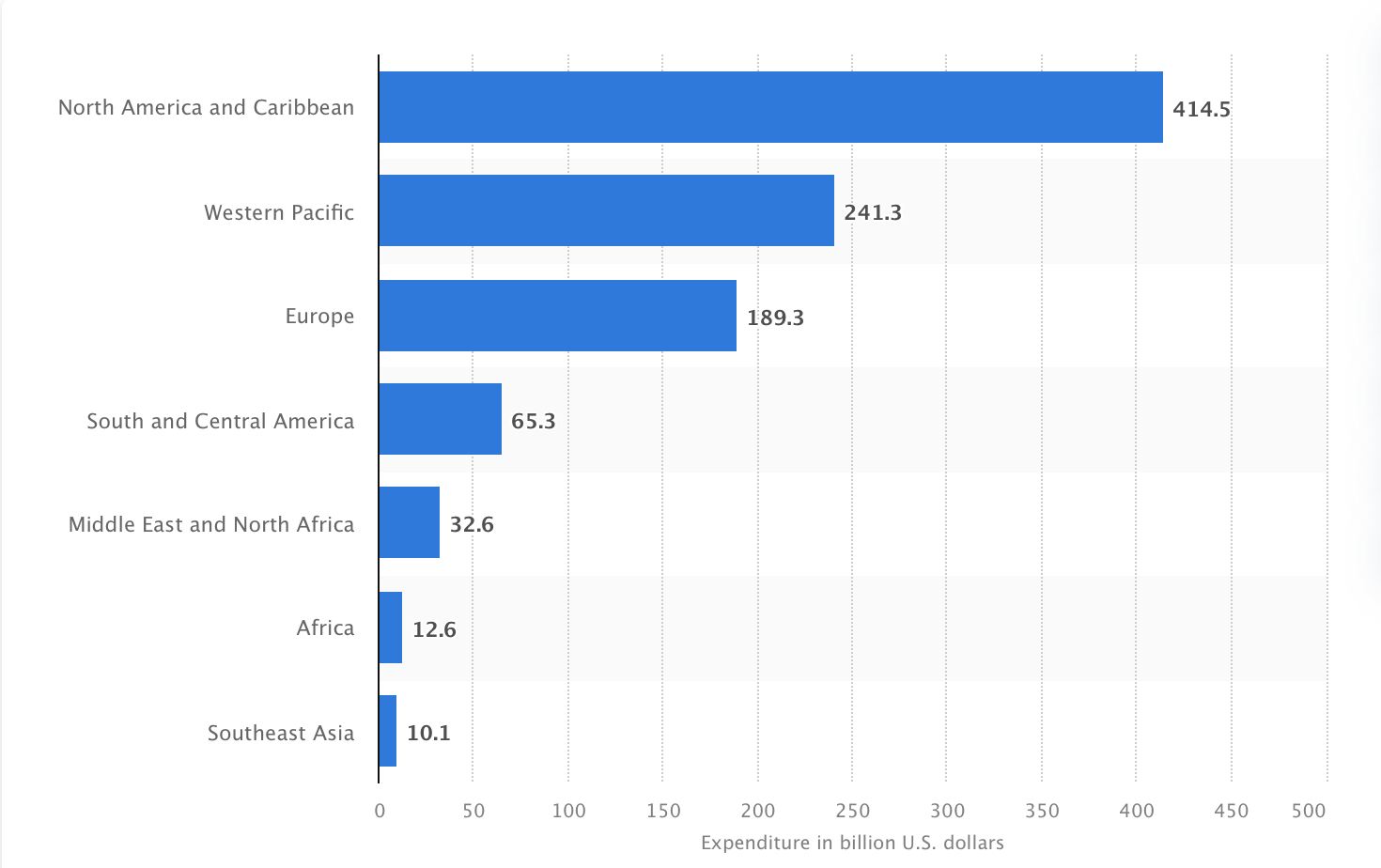

According to Statista, the global cost of diabetes was $966 billion in 2021, growing by 316% in the last 15 years. This is already ahead of past estimates which had predicted a global cost of diabetes of $845 billion by 2030.

Source: Statista

Researchers at the King's College, London, estimate that the global cost of diabetes will reach $2.5 trillion by 2030. That rate of growth would make the volatility 75 index go haywire. Diabetes is growing and that will prove to be a huge market opportunity for Embecta.

Valuation

With an FCF of $419 million in 2021, and an enterprise value of $2.78 billion, Embecta has a very attractive FCF yield of over 15%. For context, the average FCF yield of the 2,000 largest companies in the United States is 1.6%. This shows that the company's FCF are hugely undervalued compared to those of the market.

In addition, the company has a PE ratio of 3.77, compared to the S&P 500's PE multiple of 20.92.

Conclusion

Embecta is a solid performer in an industry in which it is the largest, most important player. Diabetes is a very serious and growing problem, not just in the United States, but in the world. The need for a lifetime of treatment for diabetes means that there is a lot of support for the company's revenues, profitability and returns. Investors should look past the company's recent revenue declines and take a long-term view of the company. That long-term view, allied with the economics of the company, and the company's discounted value, mean that this is a huge opportunity for investors.