Oselote

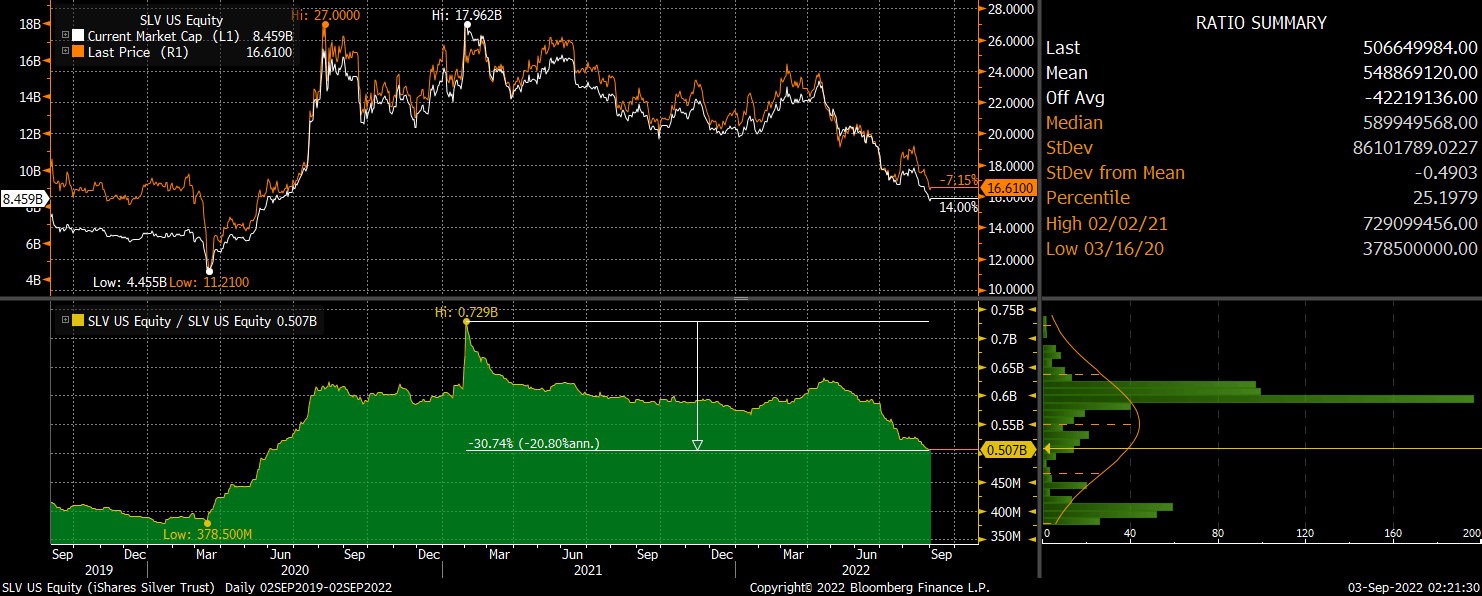

The Fed's tightening cycle has kicked the legs from underneath silver prices, which have underperformed gold and the commodity complex to a record extent over the past four months. However, there are now some signs of possible capitulation in the metal, and I am using the opportunity to add to my long positions via the iShares Silver Trust ETF (NYSEARCA:SLV). The ETF which has tracked the spot price with a median 12-month tracking error of just 0.48%, should continue to offer investors direct exposure to the metal. With an expense fee of 0.50%, this is far lower than the spreads on buying the physical metal. SLV is the largest and most liquid silver ETF, but has a slightly higher expense ratio relative to others such as the Aberdeen Standard Physical Silver Shares ETF (SIVR). Since the recent peak in April, SLV has seen a 20% decline in the number of ounces under management, highlighting the extent of the decline in speculative demand for the metal.

SLV Price Vs SLV Assets Under Management (Bloomberg)

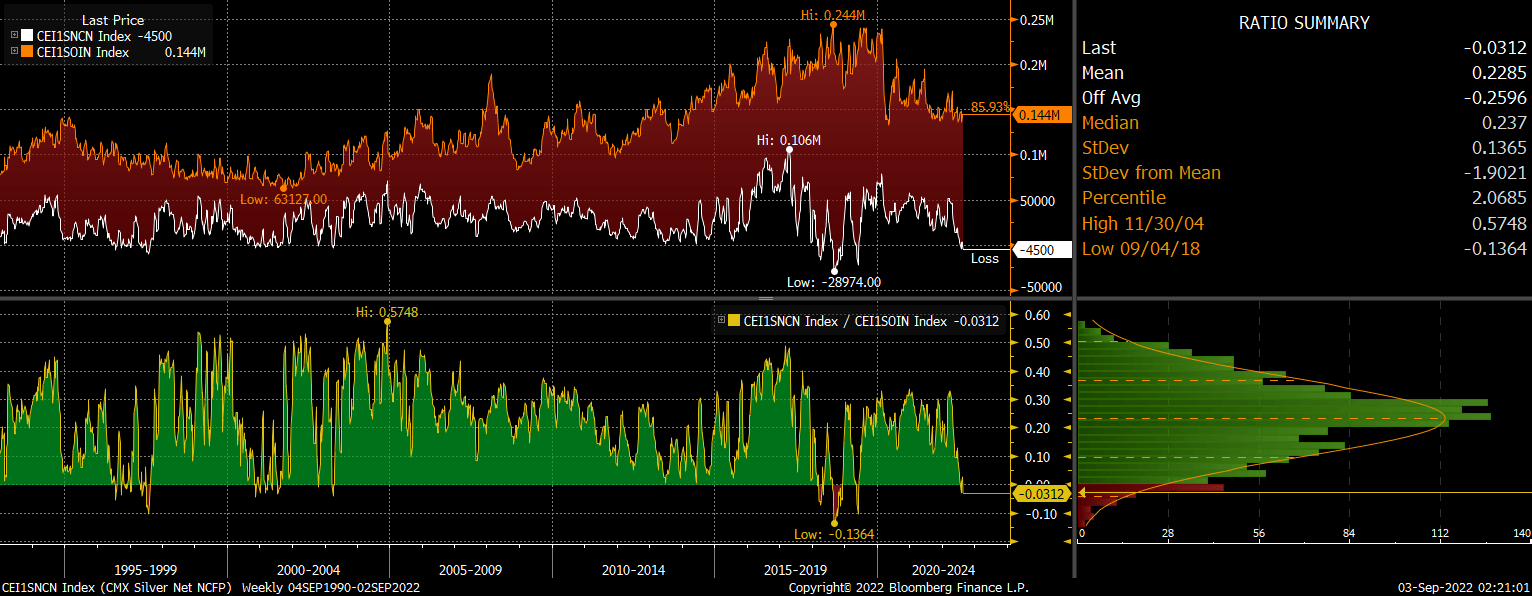

Speculators Are Bearish, Which Is A Contrarian Signal

Net non-commercial positioning on silver is now negative, which is something that has only occurred around 6% of the time over the past 30 years. While not a perfect contrarian indicator, there is certainly evidence to suggest that bearish speculative positioning tends to lead to strong subsequent returns. Of the 84 occasions when net specs have been negative over the past 30 years, the average 12-month return has been just over 12%. This compares to annual returns of 9% on all occasions. Furthermore, the maximum 12-month gain has been 82% while the maximum 12-month loss has been just 15%. Evidence suggests therefore that bearish speculative positioning is a reasonable contrarian indicator which points to a strong improvement in the risk-reward outlook for the metal.

Silver Net Non-Commercial Positioning (Bloomberg, CFTC)

Valuations Are At Rock Bottom

Another positive sign for silver is how cheap the metal has become relative to both gold prices and the broader commodity complex. As the chart below shows, over the past 20 years there has been an incredibly strong correlation between the price of silver and a 50:50 basket of gold and the Bloomberg commodity index. Over the past year this correlation has broken down, with silver selling off sharply even as gold prices have remained relatively high, and the commodity complex has risen significantly. In part this may reflect supply issues in other industrial commodity markets, which have a more pronounced impact on prices relative to silver given the latter's high stocks-to-use ratio.

Bloomberg, Author's calculations

Regardless, I continue to expect the long-term correlation to reassert itself. Given how elevated commodity prices in general have become, and the headwinds facing gold from the Fed's tightening cycle, there is of course the risk that gold and commodity prices 'catch down' to silver prices, and further silver price weakness cannot be ruled out. This is particularly the case if we see a market panic and a scramble for cash as we saw during the global financial crisis of 2008.

Monetary Conditions Becoming Too Tight For The Fed To Ignore

However, I strongly believe that any further signs of disinflation are likely to be met by a reversal in Fed policy in favor of supporting asset markets. While it may not seem like it based on the huge gap between trailing CPI and the current Fed funds rate, monetary policy is now very tight. As I wrote about in 'STIP: 3 Reasons To Lock In These Real Yields', the ongoing rise in short-term rates has been accompanied by a collapse in inflation expectations, resulting in the highest short-term real yields since the height of the Covid crisis. Any sign that the Fed is willing to ease up on its tightening campaign is not only likely to cause bond yields to fall, but is also likely to cause inflation expectations to recover, which would cause real yields to fall sharply. I would not be surprised to see real bond yields fall back to negative territory by year-end as the economic damage caused by tighter policy becomes increasingly clear, which would be highly supportive of demand for silver as a store of value.

Summary

The SLV has taken a beating over the past few months and speculators are betting on continued weakness as the Fed continued to tighten liquidity. Negative net non-commercial positioning has been a strong contrarian indicator of silver price strength over the subsequent 12 months, and when combined with how cheap the metal has become, I believe that the risk-reward outlook is highly favorable here. Much will depend on how long the Fed can continue to tighten amid growing signs of disinflation and economic weakness. However, my view is that we are at or near the peak of the tightening cycle and any sign that the Fed is shifting towards prioritizing asset prices over inflation could lead to a major short squeeze in silver and by extension the SLV.