Joey Ingelhart

Thesis

The Adams Natural Resources Fund (NYSE:PEO) is a closed end fund focused on energy and materials equities. The fund seeks long-term capital appreciation and has been in the market for over 50 years. The vehicle invests mostly in energy equities, with materials making up only 20% of the holdings. The fund has very robust long-term results, outperforming a much better-known name in the space, namely the Blackrock Energy and Resources Trust (BGR).

Up over 31% year to date, PEO has benefited from the energy shares rally. The fund has two very concentrated positions in Exxon (XOM) and Chevron (CVX), which account for over 32% of the portfolio. The fund tends to disburse capital gains at the end of the year, via one-time distributions. In the years where there are no equity gains to be had, the vehicle sticks to its committed 6% dividend distribution policy.

PEO has traded solely at discounts to NAV in the past decade. We prefer PEO over BGR given its better performance and risk/reward ratio, but an investor needs to keep in mind that neither CEF has outperformed the index.

Holdings

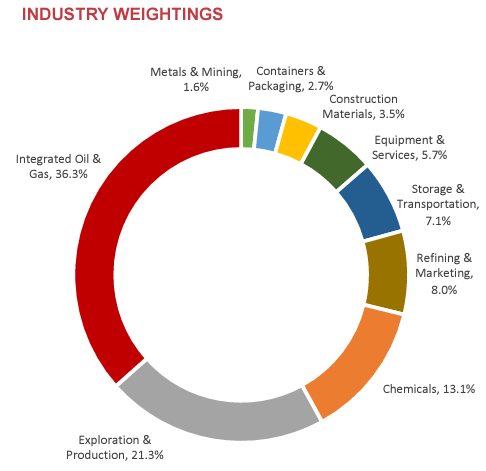

The fund is composed of energy and materials equities:

Industries (Fund Fact Sheet)

We can see from the sectoral table that Integrated Oil & Gas Majors account for 36% of the portfolio, followed closely by Exploration and Production companies which clock in at 21%. In effect most of the fund is energy, with the exception of the Chemicals sector at 13%, the Construction Materials industry slice at 3.5% and Containers & Packaging at 2.7%. That amounts to almost 20%.

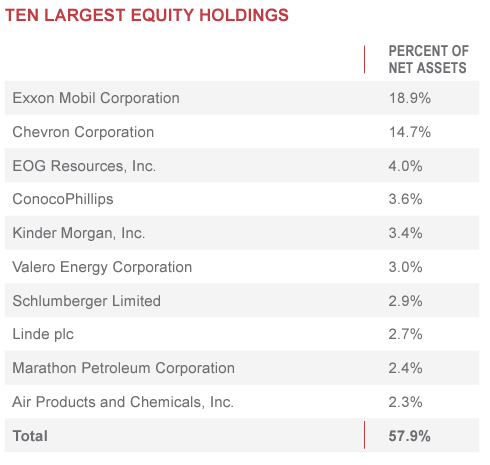

The top holdings are a reflection on the preponderance of energy equities:

Holdings (Fund Fact Sheet)

We can see the two largest U.S. integrated majors accounting for over 32% of the portfolio. The fund tends to concentrate on large cap equities in its composition:

Portfolio Type (Morningstar)

Performance

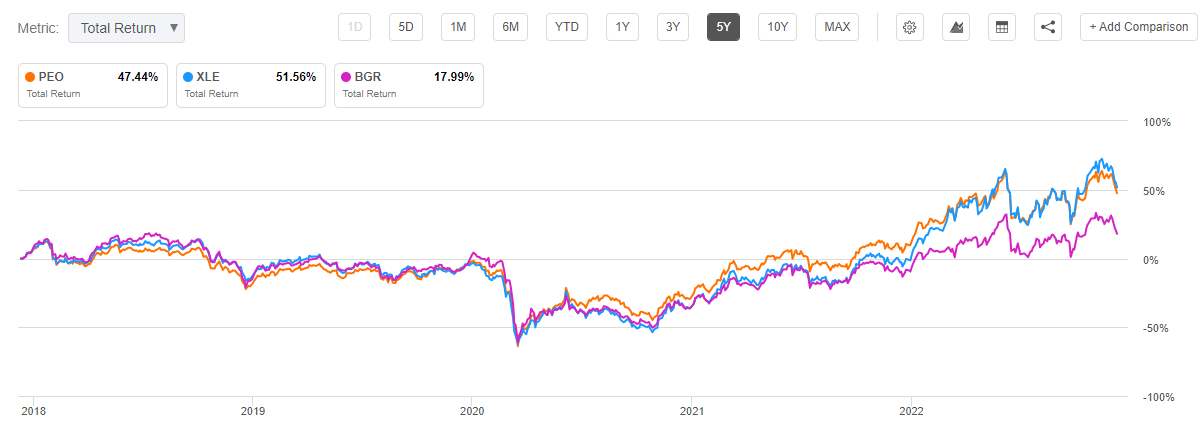

The CEF has managed to outperform long-term its much better-known peer in the space, namely the Blackrock Energy and Resources Trust (BGR):

Total Return (Seeking Alpha)

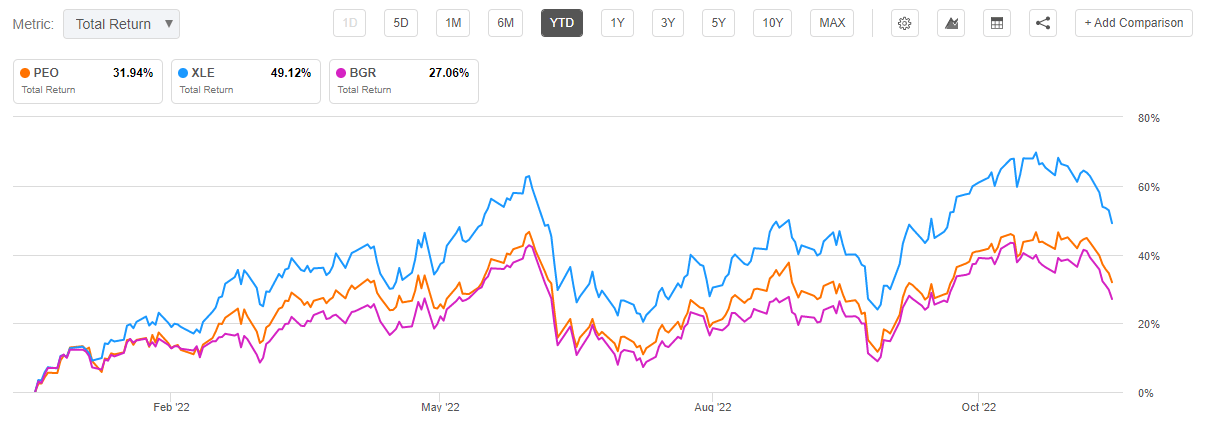

On a 5-year period PEO's total return closely matches what XLE has posted, while BGR lags substantially. On a year-to-date basis, XLE outperforms both CEFs:

Total Return (Seeking Alpha)

We usually like to see a CEF match or outperform an index. It makes the structure justify its fees. At the end of the day, for equities funds, the CEF wrapper only provides for active management and the transformation of capital gains into dividend distributions. If an investor is not pressed to see monthly or quarterly dividends, then he or she is much better suited to buying an index outright in most instances.

Premium / Discount to NAV

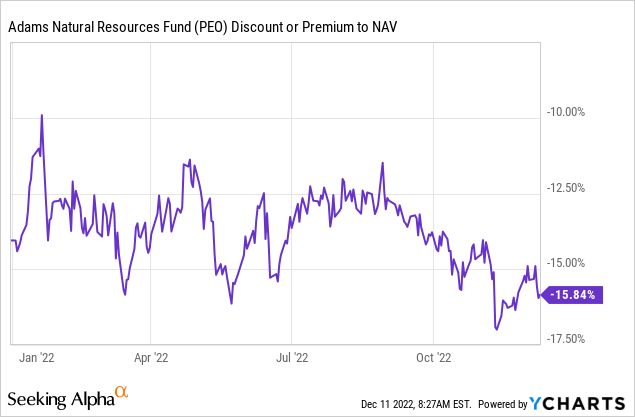

The fund has historically traded with a discount to net asset value:

Premium / Discount to NAV (Morningstar)

We can observe a sea of green above! That basically means that this fund never traded at a premium to NAV in the past decade. It is a bit surprising given its performance and size.

On a year-to-date basis the fund's discount to NAV has traded in a fairly tight range. It exposes a basis to overall energy markets rather than the S&P 500.

Distributions

The fund has a targeted 6% distribution rate:

Distribution (Fund Fact Sheet)

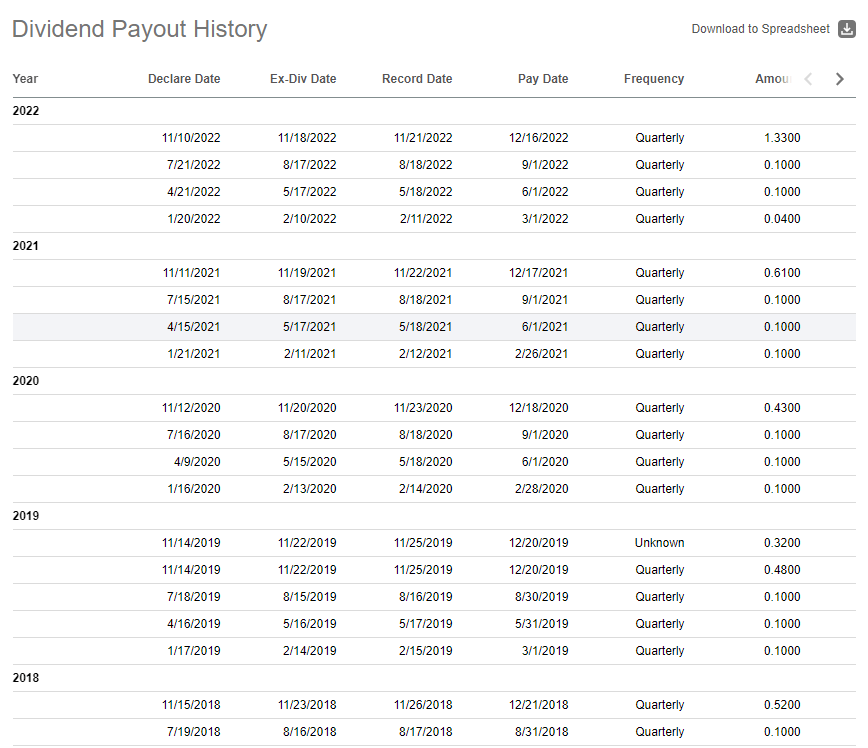

This translates into quarterly distributions of $0.1:

Dividend History (Seeking Alpha)

However, the CEF tends to have year-end one-time disbursements of capital gains. We can see a large one occurring in 2022, as the underlying equities have gained in value. We can observe from the historic table above that during the Covid crash in 2020 the fund stuck with only the committed distribution, since there were no equity capital gains to be had.

Expect more of the same. If the underlying portfolio performs healthily, then the fund will distribute at year end the gains. Conversely, in years with poor performances for energy equities, fund holders will only get $0.1 per quarter (and implicitly a lower NAV figure). The fund has done a good job at tracking XLE from a total return perspective, so long term, it works.

Conclusion

PEO is a closed end fund focused on energy and materials equities. The vehicle is up more than 31% year-to-date on a total return basis given its large concentration in Exxon and Chevron. The fund has a 6% managed dividend policy but tends to distribute capital gains annually via one-time distributions. In lean years, it sticks with the managed dividend policy. Long term, PEO closely matches the total return exhibited by XLE, and has managed to beat the performance of the much better-known CEF in the space BGR. The fund is currently trading with a -16% discount to NAV, but it tends to gravitate around -10% discounts to net asset value. We feel energy will be under pressure going into year end, but an investor looking to enter the space next year would be better suited to choose PEO versus BGR.