winhorse/iStock Unreleased via Getty Images

Mizuho Financial Group (NYSE:MFG) stock has suffered prolonged underperformance relative to the other Japanese megabanks in recent years. A key drag has been the implementation of the Bank of Japan’s (BoJ) negative interest rate policy, which has hit MFG particularly hard given its less diversified operations. Things have changed, however, with the recent monetary policy decision to expand the ‘yield curve control’ band, paving the way for a rate move back above the zero bound. Its relatively higher exposure to Japan and its shorter duration portfolio should see MFG benefit to a greater extent from a tighter policy, signaling a positive impact on lending spreads and portfolio yields ahead.

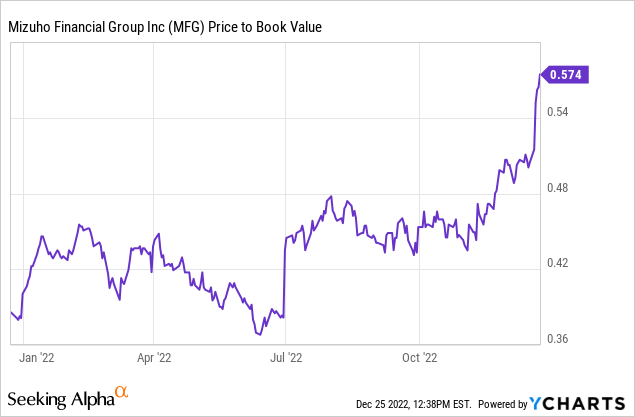

More broadly, lower risk premiums and a more favorable cost of capital for Japanese banks bode well for the P/B valuation multiples. With MFG stock still trading at a 40-50% discount to book (the cheapest among the Japanese megabanks), the risk/reward is compelling.

BoJ’s YCC Adjustment is a Game Changer

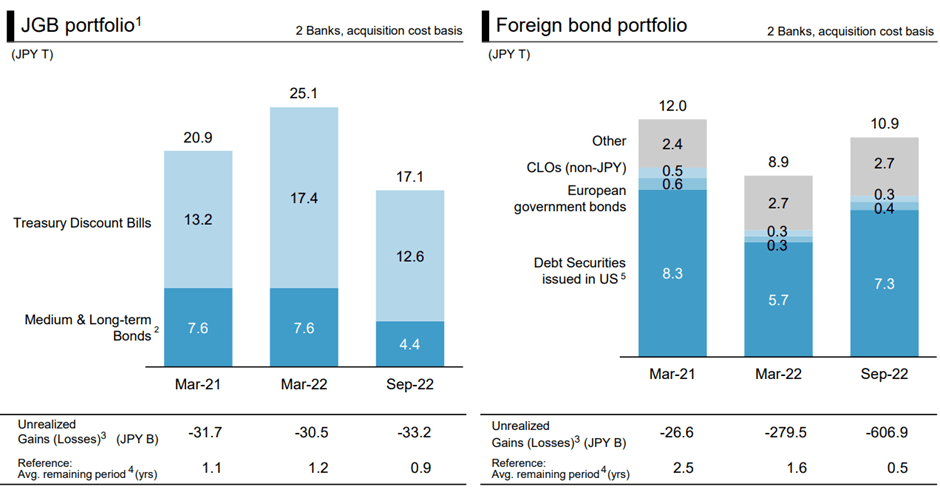

The BoJ adjusted its ‘yield curve control’ policy at last week’s monetary policy meeting, expanding the band for ten-year sovereign yields to +/-0.5% (up from +/-0.25% previously). This means higher long-term interest rates and, by extension, higher investment yields for the megabanks. MFG, in particular, stands to benefit – having prioritized minimum interest rate risk in its portfolio management policy, the company currently has the shortest duration JGBs and domestic bond portfolio at <1 year. In effect, the bank will be able to reinvest more of its portfolio at higher yields without realizing losses. Given the persistence of inflation in Japan (CPI >3%) as well, any P&L benefit is likely to be recurring (vs. a one-off factor).

Mizuho Financial Group

The biggest P&L impact will come from the domestic lending business - following years of negative rates, even slightly above-zero rates should result in significantly increased net interest income and better margins with minimal lag. Much of the benefit will come from the long end of the curve, though loans linked to short-term interest rates could also see widening spreads to base rates relative to QQE-impacted (i.e., qualitative and quantitative easing) levels. Elsewhere, a higher rate environment could also drive a reallocation toward investments (over savings) following years of declining interest income under the negative interest rate regime. In turn, this should drive higher assets under management (AUM) for MFG, supporting growth in fee-related income over time.

A Clear Re-Rating Pathway

The Japanese megabanks have long suffered from wide discounts to their book value, as the prolonged negative interest rate policy had placed the onus for a P/B re-rating firmly on higher ROEs. Yet, below-zero rates had made it extremely challenging for banks to drive profitability improvement via organic growth or opex cuts, forcing many of the megabanks to shift their business and loan portfolio mix to compensate. Of the three banks, MFG has the most domestically concentrated portfolio, so the BOJ’s decision to expand the YCC band could mean a sharper reversal relative to its peers.

Depending on how far and for how long the new monetary policy stance lasts, I wouldn’t be surprised to see a reversion to 1x P/Book over time. The rally last week has closed some of the gap, but with MFG still at a 40-50% discount to book, there remains ample upside potential ahead. In essence, I suspect the market is pricing in a one-time EPS gain rather than a mid-term ROE uplift or a sustained decline in the cost of capital; any upgrades at the next mid-term strategy update could, thus, catalyze a further re-rating.

Higher Dividend but Inorganic Growth Likely a Priority Over Buybacks

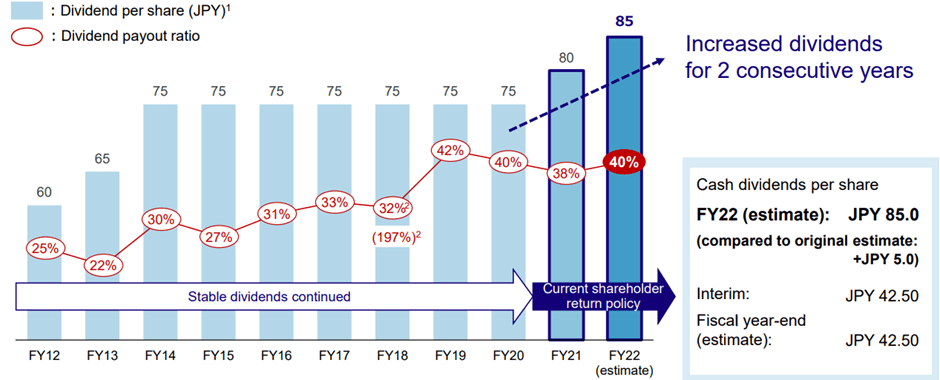

Coming off a dividend raise announcement in H1, the increasingly favorable backdrop should allow for more steady dividend hikes and potentially also a higher payout ratio. The CET1 ratio isn’t industry-leading at 9.0-9.5% but is already well within management’s target range, so capitalization should be no issue.

Mizuho Financial Group

On the other hand, buybacks likely won’t be on the agenda anytime soon. MFG has been clear in its commitment to deploying capital for inorganic growth across the online banking and brokerage businesses, as well as diversifying its presence in Asia. In essence, management is playing catch up to the other Japanese megabanks, having held firm while the others were making major investments in these areas. In the last two years, the company has only acquired minor stakes in the Vietnamese fintech app MoMo and the Philippines digital bank Tonik Financial, so there remains ample room for more global expansion.

Benefiting From a New Monetary Policy Regime

Coming off a strong H1 and a mid-year dividend hike, I see ample room for higher earnings and a steady increase in the dividend payout over time. Hopes for a buyback are probably misplaced, though, given the relatively low CET1 ratio compared to the other megabanks at 9.0-9.5%. Plus, the capital allocation framework is clearly tilted toward inorganic growth as MFG looks to catch up with its peers via equity investments in online banking and brokerage across Asia.

Still, MFG stands to benefit the most from a tighter domestic monetary policy stance – not only does it have a larger lending business in Japan, but its conservatively managed portfolio also allows it to roll over investment proceeds at higher yields (without realizing losses). While a slight relative discount is perhaps warranted given the bank’s higher cost of equity capital, the 40-50% discount to book value seems too wide given the prospect of sustainably higher ROEs over the mid-term.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.