biffspandex/E+ via Getty Images

The past three years have seen immense volatility in the market and economic trends. The initial shock from pandemic lockdowns led to a significant economic downturn that was relatively short-lived due to enormous government stimulus (deficit spending, global QE, etc.). Of course, the massive increase in the money supply, and decline in economic output, led to significant inflation that peaked last year at record levels. The inflationary boom is arguably the primary factor weighing economic growth today since it is causing strain on real wages (and corporate profit margins).

2022 saw a resurgence in negative market trends as this factor weighed on the economy. The year ended with much higher interest rates, moderately lower stock valuations, and higher corporate bond spreads - all indicating a restrictive investing environment. However, 2023 started with a generally upbeat tone. Yields have not risen in months, and real yields (after inflation) appear to decline. Many stocks rose quickly during the first month of 2023 as earnings and a solid initial GDP report. Both US and global inflation indications are seemingly declining, and China's reopening points to a total end to pandemic-related economic strain.

In light of improved expectations, many investors are flocking to higher-risk assets with abnormal yields. Ultra-high yield assets are generally hazardous but can deliver strong returns, mainly as market "fear" falls from elevated levels. One such stock is Eagle Point Credit Company (NYSE:ECC), a CLO investment company with a staggering 15.6% forward yield. ECC is among the highest-yielding stocks on the market, excluding those with inconsistent dividends, making it a go-to pick for investors looking for high "steady" income streams. However, while interest in ECC is resurging, underlying economic fundamentals threaten its capacity to deliver returns. I believe a resurgence in financial risk perception could quickly cause ECC to lose most of its value - potentially permanently.

Eagle Point Credit Company's Business Model

Eagle Point's model can be seen as "too complicated," causing some investors to overlook its strategy and instead focus on its high yield and historical performance. While these indicate its future, ECC's structure can obfuscate its true risk profile. The CEF falls into the category of investments I call "Escalator-to-Elevator bets." In "normal" periods, it delivers relatively steady positive returns. In downturns, it suffers catastrophic losses that could wipe out its value entirely. A short-lived downturn, such as that of 2020 (in which most corporations were effectively bailed out), may only bring 20-40% losses that are quickly recouped, but a significant or prolonged downturn could theoretically cause ECC to lose most or all, of its value. In my opinion, this makes ECC's risk-return profile somewhat similar to a "Martingale" betting system, where the risk of eventual rapid catastrophic loss is high but obfuscated by otherwise consistent returns.

In reality, Eagle Point's model is not too complicated. The investment company buys collateralized loan obligations on corporate loans, primarily the highest-risk "equity tranche" of CLOs. Most of Eagle Point's CLOs focus on B-rated senior secured corporate loans. Eagle Point's CLO's underlying assets are similar to the Invesco Senior Loan ETF (BKLN), which carries a similar weighted-average credit rating. Senior secured corporate loans are not too risky and pay a 5-7% yield that typically moves with interest rates (giving them no duration risk). If they default, then losses can be offset by secured assets. Generally, B-rated loans carry an average one-year default rate of around 13.8%, so even assets like BKLN tend to lose value over time; of course, their default rate is often much higher during recessionary (or similar) periods and low during regular periods.

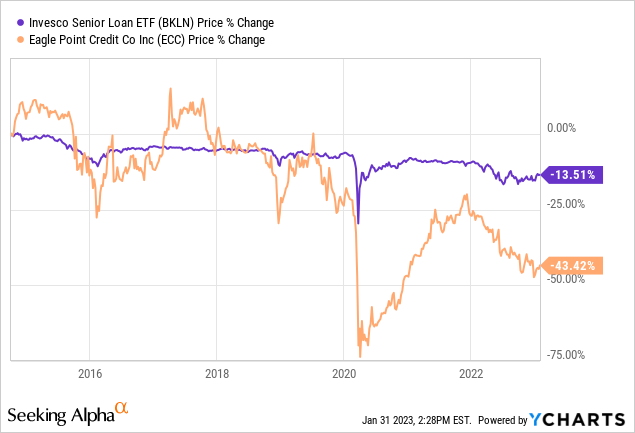

ECC is effectively a highly levered version of BKLN since it primarily owns the "Equity tranche" of CLOs. Typically, around 65% of a CLO is in the "AAA" tranche, 4-12% in the intermediate "Mezzanine" tranche," and around 8-10% in the "equity tranche." Thus, investing in an equity tranche CLO is akin to purchasing a senior secured loan with 5-10X leverage. As you can see, ECC is closely correlated to BKLN, but ECC is around 5X as volatile on an annual basis:

For investors looking to understand ECC's risk-reward profile simply, I would state it is like BKLN with around 5X leverage, though not 5X the yield due to interest-rate effects (around 2-3X the yield).

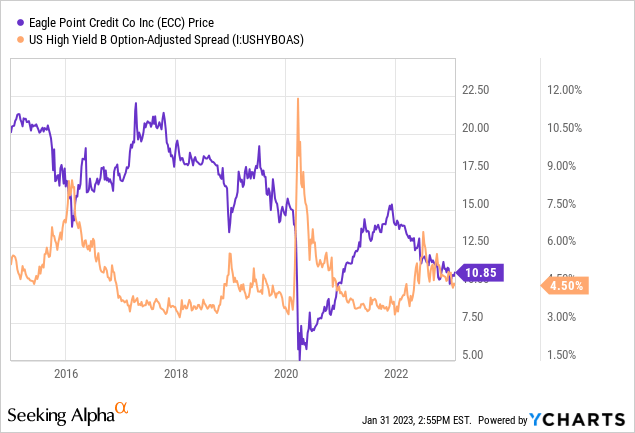

Of course, for investors looking to understand ECC more deeply, that may be an oversimplification. More technically, the equity tranche of CLOs is paid last and the first to realize losses. Since it carries the most risk, it also has a higher yield. For example, if 5% of companies in a corporate leveraged loan pool default, then a CLO equity would lose around 50% of its income. ECC's income would fall slightly further because it is further subordinated to the company's various preferred equities. If the default rate rises to 10%, ECC is liable to lose all its income. Historically, it is common for B-rated corporate bonds to experience a default rate of over 10% in a recession, wiping out ECC's income. This pattern also significantly impacts ECC's price compared to spreads on B-rated corporate debt. In 2015, a ~4% rise in B-rated spreads caused ECC's price to decline by roughly a third. In 2020, a ~8% rise in B-rated spreads caused ECC's price to drop by around two-thirds. See below:

In 2015 and 2020, many companies that experienced default returned to paying status, causing ECC to recoup most losses and continue to pay a high return. However, neither scenario saw a significant increase in corporate bankruptcies, and in fact, bankruptcies fell considerably in 2020 due to the stimulus impact. If a recession occurs that is met with a rise in bankruptcies, then I believe ECC would likely permanently lose most, if not all, of its current value due to the intrinsic leverage in its business model.

ECC Is For Speculators, Not Retirees

In my experience, investments like ECC often attract investors looking for high steady income streams; too usually, that means retired people who cannot afford to lose a substantial portion of their equity or cash flow. It is true that Eagle Point has paid a solid dividend through a tumultuous economic period. Still, in 2020, risks within the credit market were obfuscated by substantial government stimulus to corporations and the impact of QE. Looking at ECC's historical risk is a very poor indicator of its risk since it was never traded during a period of sustained high corporate credit spreads, unemployment, or a rise in bankruptcies.

A speculator may reasonably suggest that the risk of such a recessionary scenario in 2023 seems to be on the decline now that inflation data is normalizing. Thus, a speculator could argue that ECC is a good investment since its yield is high and its value could rise as risk fades within the corporate credit space. However, that does not change the fact that when corporate credit risks do return (bankruptcies, etc.), ECC is liable to lose most of its current value and income today permanently. Historically, a broad rise in corporate bankruptcies or unemployment is inevitable.

In my opinion, people seeking stable income streams with capital preservation should not invest in assets at risk of permanent 50%+ permanent losses. "Equity tranche" CLOs are typically invested in speculative Hedge Funds, BDCs, and specialty credit funds, not banks, insurance, or pensions seeking dependability and capital preservation. This is not to say Eagle Point is a "bad" investment - its managers fulfill its role quite well - just that it is unsuitable for most investors due to its high risk of eventual catastrophic loss.

The Bottom Line

ECC is a decent option for those with a high-risk tolerance who firmly believe the economy will rebound after a challenging 2022. However, the fund trades at a nearly 15% premium to NAV, so I would not invest in it even if I were bullish on its underlying assets. Further, I am not bullish on ECC's underlying assets and believe the odds of ECC losing most of its value this year are far higher than the market currently appreciates.

While it is true that some indications of a recession have faded, I believe the impending bankruptcy of Bed Bath & Beyond (BBBY) may be a "canary in the coal mine" for other bankruptcies. PMI data continues to be below 50, pointing toward an economic contraction. Mass layoffs at large technology companies also indicate a broader business slowdown. I believe the "improvement" in economic data over the past two months is primarily associated with a sharp decline in natural gas and crude oil prices and China's reopening. Those factors certainly improve the global economic outlook, but I do not believe they will alter the fundamental "stagflation" trend.

ECC will likely lose most of its income if the economy enters a recession in 2023 and more companies face default or bankruptcy. In 2020, such an occurrence was met with immense stimulus from the Federal government and central banks, causing most large corporations to avoid bankruptcy, so ECC recouped most of its 2020 losses. However, if a recession occurs again, I doubt the Federal Reserve will make a dovish shift so quickly due to the overarching inflation concern. Thus, I believe ECC may see a similar loss as it had in 2020, but without a recovery, as some companies face financial restructuring and are unlikely to be bailed out.

Overall, I am bearish on ECC today, primarily due to my speculative view of the economy. However, even if I had a bullish speculative view of the economy, I do not believe ECC is suitable for most personal investors looking for a stable income stream. ECC is not a stable asset due to its nature. Although senior-secured leveraged loans are generally safe, ECC makes them far riskier due to its equity-tranche positioning. Further, now that interest rates are elevated, income-seeking investors can find far less risky options, such as BKLN, that still pay solid yields (BKLN's is ~7.3% today). ECC offers twice that yield but with 5X+ the risk (depending on calculation), making it a generally weak risk-reward trade-off today.