franz12

This past week began with two 300-point-plus gains for the DJIA. The shotgun wedding last weekend between UBS and CS seemed to have calmed the nerves of investors in a very nervous market. Despite the shareholders and depositors of CS being rescued, the bondholders were wiped out. PIMCO will write off over $300 million in bonds that are now worth a few pennies on the dollar.

With that wreck on the freeway now in the rear-view mirror and most of the broken glass cleaned up, it was time to start worrying about what Jerome Powell would say after the big Fed decision on Wednesday. The expectations had been ratcheted down from a possible 50-basis point hike (due to stubborn inflation) to just a 25-point hike instead, due to several messes that needed cleaning up in the Financial aisle of the Wall St. supermarket.

Not only did Chairman Powell deliver the expected 25-basis point hike, but he also said that there would be more than likely just one more rate hike this year. The market initially celebrated this news, but then the DJIA sold off by 530 points after Powell said not to expect any rate cuts this year. He also warned investors to expect a looming tightening of the credit markets.

The credit markets are one of the biggest sources of fuel that help to drive the economy. This statement by Powell is probably the one that we should be worried about most. It has been said that “A credit crunch is when your bank won't lend to you. A credit crisis is when banks won't lend to each other.” He did not predict a credit crisis, but we have recently seen several banks that have had big holes in their balance sheets that could bring this about.

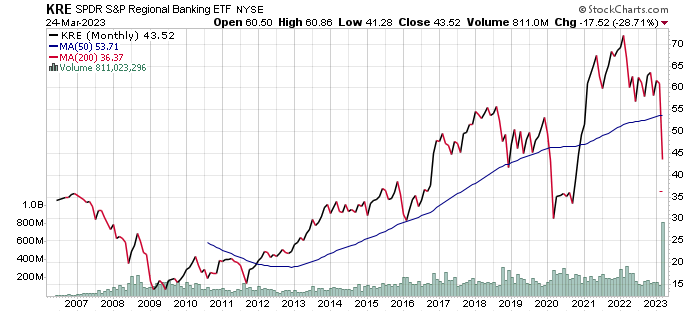

The chart below is not a good chart of the Regional Banking ETF (KRE). It is now down 38.9% since early last year. Look at the recent volume in this ETF! It is looking about the same as it did during the COVID year of 2020 and the Financial Crisis of 2008-2009. Hopefully, it will turn around soon.

Stockcharts.com |

Did the regional banks get caught up in the speculative investing that took place in 2020 also? That was the year that bitcoin hit 66,000 and Cathie Wood’s ARKK fund was up over 100%. Hopefully, this recent turmoil in the banking sector will be limited to just a few bad actors. Janet Yellen (our current Treasury Secretary), Christine Lagarde (President of the ECB), and Peter Oppenheimer, (Goldman Sachs), all stated this past week that the banking issues are not systemic.

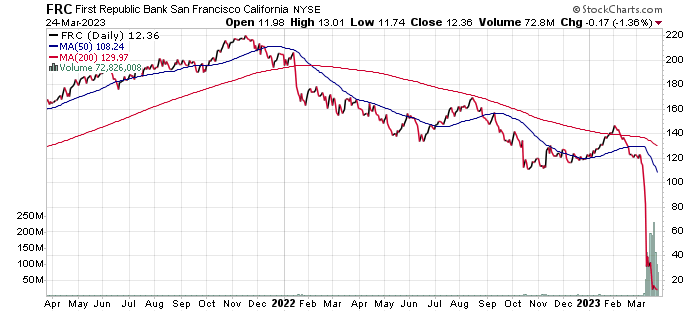

In the meantime, FDIC insurance will remain at $250,000 for your deposits at the bank, even though this limit was thrown out the window when Silicon Valley Bank (SIVB) collapsed. Don’t forget, we still have First Republic Bank (FRC) and a few others to worry about, however.

Stockcharts.com

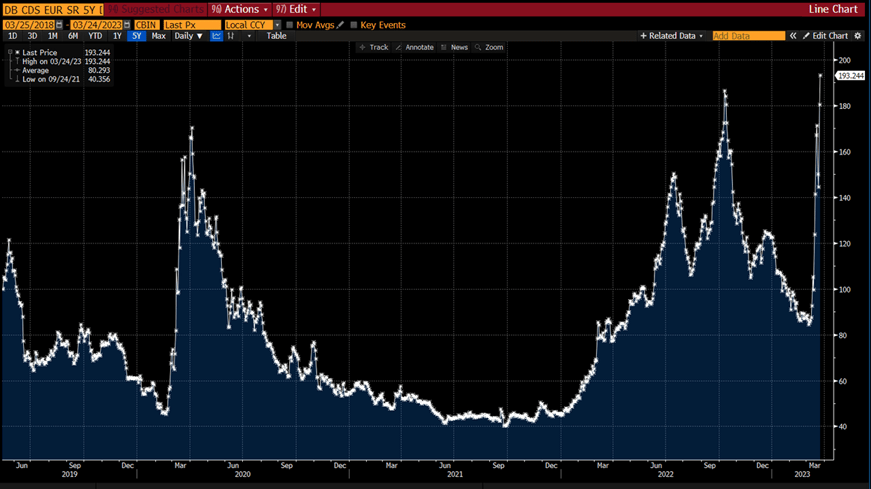

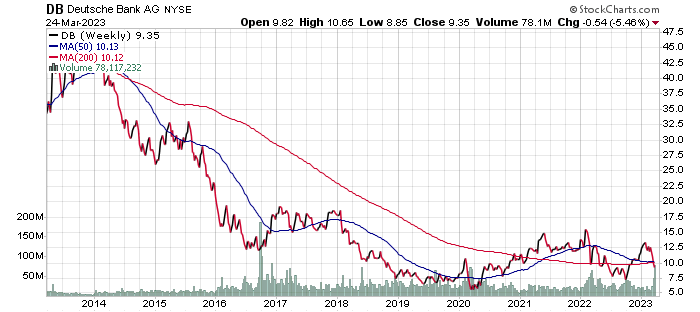

We also learned of a new possible problem child in Deutsche Bank (DB) on Friday as the price of their Credit Default Swaps (CDS) soared.

Refinitiv/Eikon

Deutsche has been an unhealthy bank for many years.

Stockcharts.com

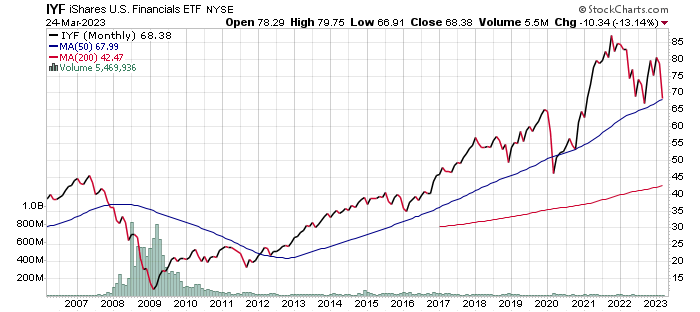

The issues at the banks are also showing up in the Financial Sector somewhat, but not nearly as bad as in the Regional Banking Sector.

Stockcharts.com

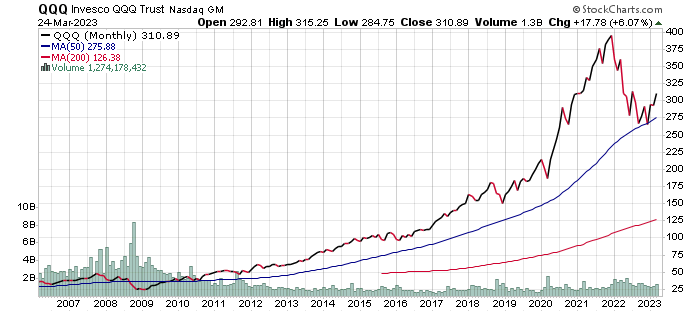

In the meantime, several perceived “safe havens” have cropped up in places like the Technology Sector, Gold, and in the Bond Market.

I wrote an entire article on the recent "golden cross" in the Nasdaq last week. Despite a little sell-off in the chip and software stocks on Friday, it has been the strongest sector in the market by far in 2023. You can see from the chart below how rising interest rates reigned in the tech sector in 2022, and how falling interest rates are now boosting it in 2023. These falling interest rates have only been helped along even more by the banking crisis and the fairly “dovish” decision by the Fed this past week.

Stockcharts.com

You can see from the chart below this big reversal in interest rates that began when they peaked last October. This is also about the same time that the Nasdaq started putting in a bottom. We stated that the bottom in the Nasdaq was complete in an article that was published back on January 6th of this year.

Stockcharts.com

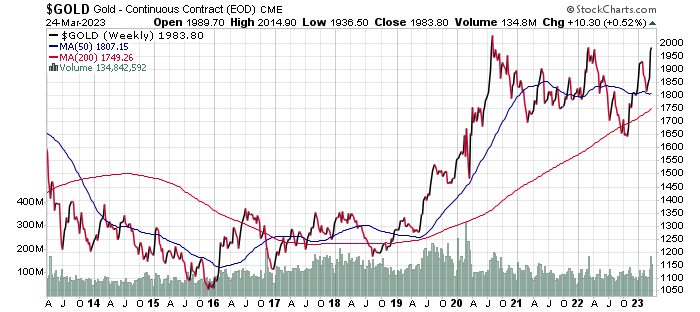

Gold has also been on the receiving end of money flow recently. Gold does not think that the Fed is doing enough to get inflation under control and many obviously perceive it has a more secure store of value than a deposit of over $250K at the bank. The chart below is much healthier than the banking sector right now. Gold was actually above $2,000 per ounce for a short while this past week. This has not happened since the COVID year of 2020.

Stockcharts.com |

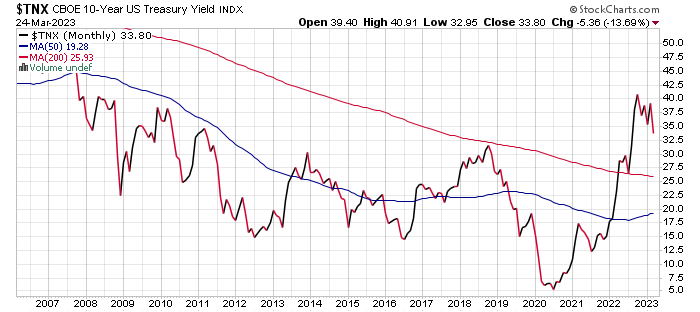

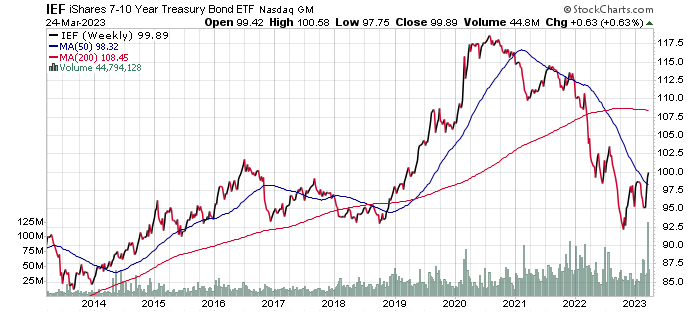

And last but not least, the bond market has also seen a major flow of money into it recently with the turmoil in the banks which has also caused a big drop in interest rates. U.S. treasuries are also currently seen as a safer place for money than in the banks. The yield curve has now narrowed from an inversion of 109 basis points just two weeks ago to Friday’s close of just 38 basis points! This has been mostly caused by a flight to safety as opposed to a lessening fear of a recession.

Stockcharts.com |

Despite the recent turmoil in the markets we continue to like big tech and individual bonds in this current environment as long as more dominoes in the banking sector do not continue to fall.

Best Stocks Now Premium gives you access to Bill Gunderson, professional money manager & analyst with 23 years of experience.

You get Bill's daily "live" buys and sells in his five portfolios: Emerging Growth, Ultra-Growth, Premier Growth, Best ETFs Now, and Dividend & Growth.

JOIN NOW to get daily "live" buys and sells, weekly in-depth market-timing newsletter, access to Bill's proprietary database with daily rankings on over 6,000 securities, and a daily live radio show!