FangXiaNuo

Investment Thesis

JD.com (NASDAQ:JD) is one of China's largest online retailers. The company serves essentially every single region across the nation and has become one of the fastest delivering retailers in the world.

Their unique vertical integration of a logistics network into their core online retail business has proven to be a source of significant economic moat for the firm.

A lackluster FY21 left investors reeling and sent shares plummeting to what is now a 52-week low for the company. It seems a solid FY22 combined with what looks to be an outstanding start to FY23 has gone ignored by Mr. Market.

At current valuations, I believe shares are 61% undervalued. That is mega deep value territory if you ask me.

Company Background

JD FY22 Annual Report

JD.com also known as "Jingdong" is a Chinese e-commerce company headquartered in Beijing. The company is the largest retailer in the country (by transaction volume and revenue) with their business operations spanning across a multitude of retail segments.

JD has been an online retailer since 2004 with the firm becoming one of the main players in the market sharing the space with rivals such as Alibaba (BABA) and Pinduoduo (PDD). The company is often described as a technology-driven e-commerce company with a significant focus resting on developing new and innovative retail solutions to further drive sales.

While Alibaba and JD initially seem similar, JD has a markedly different business model to its closest rival. JD focuses on self-owned inventory and self-built logistics solutions instead of Alibaba’s third-party focused retail solution (Alibaba being much like Amazon (AMZN) in this regard).

The company’s historic growth in net revenues and margins experienced a slowdown in late 2021/early 2022 leading to share prices plummeting over 38% YoY. When combined with a difficult macroeconomic environment, the overwhelming market sentiment has soured for the Chinese retail giant.

While margins remain strong and growth seems to be resuming, the unrelenting headwinds currently facing consumer discretionary retailers creates significant uncertainty for JD.

Therefore, a fundamental company analysis and intrinsic value calculation must be completed to fully understand what sort of investment opportunity may exist in JD.com from a value perspective.

Economic Moat – In Depth Analysis

JD has a wide economic moat which primarily stems from their high-quality first-party (1P) business model which places trust and quality at the forefront of their business model. Significant moatiness is also derived from the tight integration between their sales site (JD.com) and their logistics subsidiary (JD Logistics).

Instead of relying as an intermediary sales medium to help third-party retailers sell their goods online (much like Alibaba or Amazon), JD.com is focused on selling their own self-owned inventories of stock and products along with vertically integrating JD Logistics into this endeavor.

This significantly increases the reliability consumers can expect when purchasing products from JD as compared to Alibaba since JD is directly responsible for taking payment, dispatching and shipping the products to its customers.

While their overall selection of products is smaller than a third-party oriented seller, JD can offer customers much faster shipping times and greater levels of trust when making purchases. This can significantly increase the psychological levels of satisfaction felt by consumers in the purchasing process which in-turn, increases the probability of repeat business from these customers.

While JD.com in itself is a moaty business thanks to its more hands-on approach to selling merchandise, what really drives JD’s moat from narrow to wide is the extent of their vertical integration between their JD.com and JD Logistics.

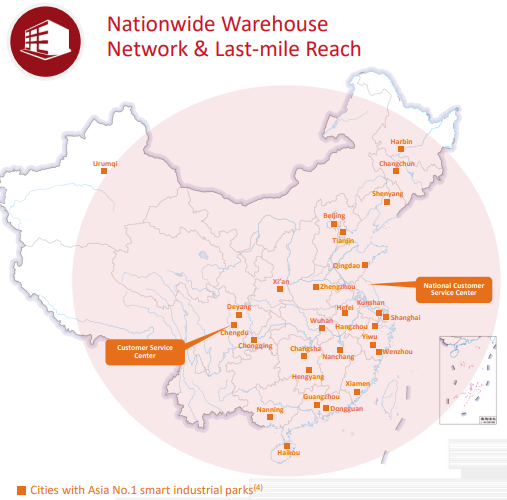

The synergies this tight-knit integration creates for the company are almost unrivalled within China. JD Logistics has created a proprietary logistics network which focuses on providing customers with not only a reliable system, but one which is incredibly fast.

JD.com FY22 Annual Report

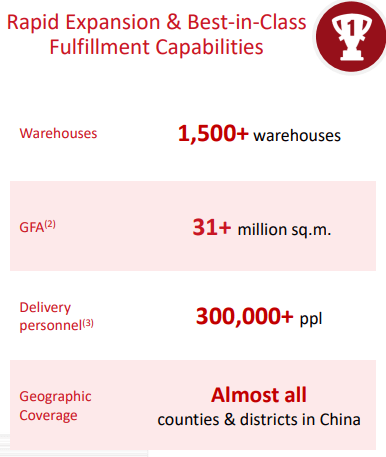

JD Logistics has created a huge network of warehouses with over 1,500 such locations covering the vast majority of the People’s Republic of China. When combined with over 300,000 delivery personnel, this allows JD to achieve incredibly fast delivery times on the vast majority of their products.

JD.com FY22 Annual Report

To put this into context, in 2021 (as this is the most recently published data regarding this matter from the firm), 90% of online retail orders placed through JD.com were delivered on the same day or next day after order placement.

The incredible speed JD offers consumers highlights the truly world-class logistics network JD has created to complement their retail platform. Quite simply, such a network is unrivalled not only in the PRC, but across the globe.

This transport efficiency allows JD.com to quickly turnover their inventory of products which significantly increases the revenue generation potential of the business. In 2022, their inventory turnover was just 31.2 days. Given the huge scale and wide range of products offered by the retailer, this figure is very impressive indeed.

During the COVID-19 pandemic, JD Logistics was able to help the Chinese government in supply critical medicinal supplies and vaccines to provinces such as Wuhan thanks to the incredibly speed their transport network was capable of achieving.

JD.com also complements their 1P business with a small secondary service, offering third-party retailers the opportunity to list products on their site. However, the lack of tight integration with JD logistics services makes this business segment significantly less attractive to both consumers and 3P retailers alike.

The management at JD seems acutely aware of this which is probably why their utmost dedication remains on expanding their 1P service along with further development of JD Logistics.

JD Logistics is constantly innovating with novel logistics solutions such as AI driven data analytics and drone delivery in certain regions of the PRC. The company’s constant desire to offer customers with even faster and more effective delivery solutions further drives the company’s image in the public sphere thus increasing the likelihood of their services being recommended by customers to other potential consumers.

Overall, while the high-quality 1P retail business JD.com operates drives an undoubted economic moat through the trust and reliability offered to customers, the real moat-driver comes in the form of JD.com’s integration with JD Logistics. Their unrivalled logistics network creates a holistic service for consumers which simply cannot be matched by any of JD’s rivals.

While the potential for some of JD’s competitors such as Cainiao or Pinduoduo to further develop their own 1P retail solutions exists, the significant time and resources required to match JD’s unrivalled holistic product offering is simply too great for any real competitive threat to be presented at the moment in my opinion.

I believe JD also stands to continuously benefit from increasing economies of scale in their operations which could help increase margins moving forwards. Therefore, I believe JD is a true mega-moat business with enough of a competitive advantage at present to maintain this moat for at least the next 10 years.

Financial Situation

At first glance, JD has had a reasonably unimpressive fiscal history over the last 5Y. Their 5Y average ROIC is a respectable 7.71% combined with a healthy ROE for the same period of 10.18%. Unfortunately, their 5Y gross, operating and net margins respectively have been just 14.2%, 0.98% and 1.70%.

Initially, these rather constricted margins may sound alarming to investors. However, the real key here lies in their most recent turnaround towards significant profitability which has largely been hidden by the COVID-19 pandemic and current 2023 macroeconomic headwinds.

In 2019 and 2020, JD managed ROICs of 12.89% and 29.92% respectively. While these figures were largely inflated by the strict coronavirus restrictions in China forcing more consumers to purchase goods online, I believe these two years are more representative of what JD is capable of.

JD’s ultimate potential lies in their ability to tap into significant economies of scale. Given the constant growth the company has achieved over the last ten years, it seems apparent that JD is finally reaching the critical point of scale where significant margin growth can begin to be unlocked.

The increasing scale of JD’s operations also allows JD to have significantly more bargaining power when it comes to product purchasing as evidenced by their 61.1 days payables metric in FY22. Given that their days sales outstanding is just 4.92 days, JD is able to create a significant time-lag between paying for their retail products and receiving cash from customers.

While 2021 was a difficult year for the company, FY22 was already a very positive step in the right direction for the firm. The company achieved strong ROA, ROE and ROIC rebounds from FY21 low single digit negative values to 1.90%, 4.92% and 3.01% respectively in FY22.

JD.com FY22 Annual Report

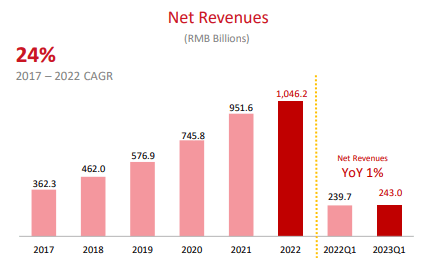

The company also grew net revenues from ¥951.6B in 2021 to over ¥1.46T in 2022. This represents a 10% growth which, while slower than 2020-2021, is still a very healthy figure.

JD.com FY22 Annual Report

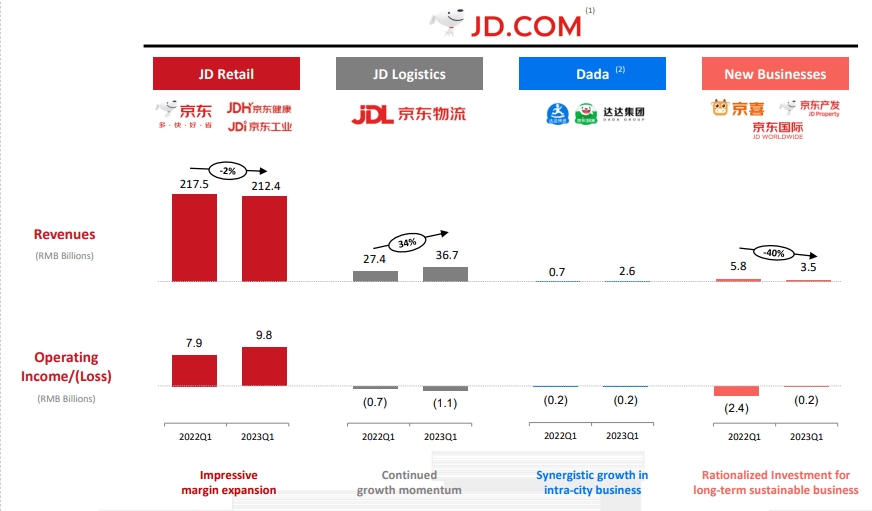

Most importantly, in the same period between FY21-FY22, JD managed to increase the profitability of their JD Retail business by 24% despite gross revenues actually decreasing 2% YoY. This highlights the significant margin expansion achieved by JD suggesting their current turnaround plan is working effectively.

While the gross revenues from JD logistics grew significantly through FY21-FY22, overall profitability was harmed by rising transportation costs driven largely by the continuous inflation even the PRC was not immune to.

Therefore, I fully expect their logistics division to return to break-even or even marginal profitability in the short-midterm future.

FCF also grew significantly in FY22 to over ¥35.6B representing a YoY growth of over 35%.

Importantly, these significant operational improvements achieved in FY22 seem to only be the very start of JD’s march towards operational excellence.

JD.com FY22 Annual Report

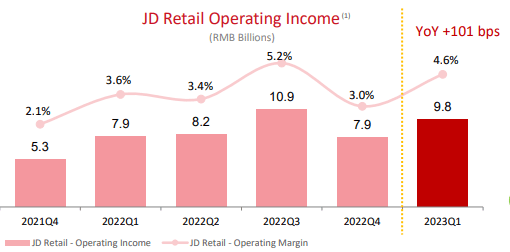

The start to FY23 has been very positive with operating income in Q1 FY23 increased +101bps YoY. This has resulted in operating margins increasing from just 3.6% in Q1 FY22 to over 4.6% in Q1 FY23.

Similar growth has also been seen in non-GAAP net profits which have increased a whopping +144bps YoY resulting in net margins increasing from just 1.7% in Q1 FY22 to just over 3% in Q1 FY23.

I believe these huge margin improvements are proof that JD’s robust business model is capable of providing significant margins to the company and thus, great shareholder returns for investors.

I await excitedly for the FY23 Q2 results and ultimately, to see how the entirety of 2023 plays-out for the Chinese retail giant. Already, it is clear to me that significant operational proficiency improvements have been achieved despite the relentless macroeconomic environment plaguing global economies.

Seeking Alpha | JD | Profitability

Seeking Alpha’s quant assigns JD with an "A" profitability rating. I believe that this rating is a representative snapshot illustration of the company’s overall profit generating prowess.

JD’s balance sheet looks to be in healthy shape too. The company currently has $44.4B in total current assets while total current liabilities only amount to just $32.6B. This illustrates the relatively conservative fiscal strategy being pursued by management with regards to their growth strategies. For investors, such a well-managed and liquid company is excellent news.

The company has a debt/equity ratio of just 0.31x which again is fantastic to see from an investor perspective. Their quick ratio (current assets minus inventory divided by current liabilities) is 0.97x.

JD.com FY22 Annual Report

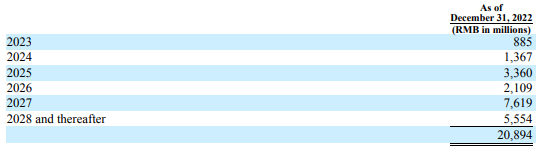

JD has ¥20.89B in long-term debt with a majority of debentures maturing after 2027. While the company has ¥2.2B maturing in 2023/2024, JD’s strong FCF and return to profitability should allow the company to pay-off these debts without any issues.

JD operates with a financial leverage of just 2.29 which is fantastic to see, especially given the overleveraged nature of many retail companies.

Overall, it is clear that the management at JD is laser focused on returning the business to significant levels of profitability in the near future. JD’s unique business model and outstanding vertical integration of logistics services into their retail business provides the company with a solid foundation to continue increasing their margins into the future.

Valuation

Seeking Alpha | JD | Valuation

Seeking Alpha’s Quant has assigned JD with a "B" Valuation rating. I find this valuation to be a far too pessimistic overview of JD’s current valuation. I believe JD is trading at a truly staggering discount to its intrinsic value.

The firm is currently trading at P/E GAAP FWD ratio of 16.15x and a P/CF TTM ratio of 9.36x. Their FWD EV/EBITDA of 7.52x is quite low in my opinion, along with their EV/Sales TTM of just 0.29x.

Let me emphasize this point, JD is currently trading at roughly 1/3 of its total FY22 sales.

I believe these figures alone suggest that JD could be trading at a significant undervaluation compared to the intrinsic and future value present in the firm.

Seeking Alpha | JD | Summary Chart

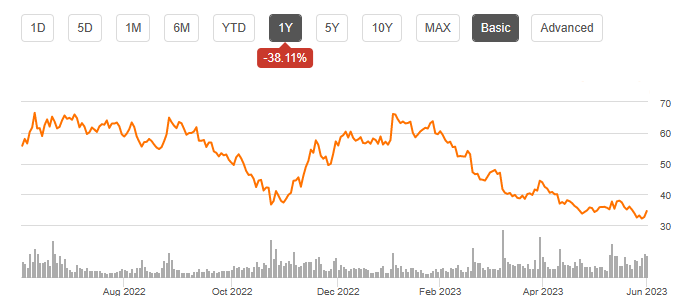

From an absolute perspective, JD shares are trading at what seems to be a very low price. JD shares are currently at a 52-week low with YoY valuations having fallen a whopping 38%.

The significant market “correction” that took place after a weak FY21 and slow start to FY22 is unwarranted at current time and seems excessive to me.

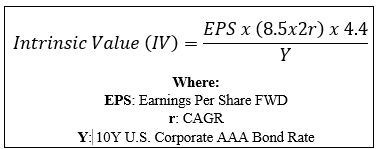

By accomplishing a simple financial valuation based on the calculation below and using the estimated 2023EPS of $3 a conservative r value of 0.10 (10%) and the current Moody’s Seasoned AAA Corporate Bond Yield, we can derive a base-case IV for JD of $89.10.

The Value Corner

Even when using this conservative CAGR value for r, JD appears to be undervalued by huge 61%.

When using a more optimistic CAGR value of 0.12 (12%), shares are valued at around the $100 mark, which would represent a 66% undervaluation.

Therefore, I believe JD as a company is currently sitting soundly in the mega deep value range. If the firm is able to harness the expected growth in margins and the resulting net incomes, I think the potential for FY23 results to outperform even the current management expectations is real.

In the short term (3-10 months) it is difficult to say exactly what the stock will do. Much depends on the prevailing macroeconomic conditions and how reluctant investor sentiment will be to react to the great news coming from the company.

In the long term (2-4 years) I expect their position as the most reliable and fast online retailer in the PRC to become even stronger. Their unique and differentiated approach to online retail combined with tight vertical integrations provides JD a moat which is not only robust, but one which could be efficient at providing real margins for the company’s business operations.

I believe current share prices represent a massive mistake by Mr. Market. A base-case 61% undervaluation is simply too large to ignore.

Risks Facing JD

JD’s primary risk stems from the competition it faces in the PRC along with potential governmental risks arising from the increasingly authoritarian activates pursued by the nation’s leaders.

While competitors such as AliExpress and Pinduoduo cannot compete directly with JD’s product offering, they still account for a huge number of online retail sales in China. The lower prices these competitors can often provide consumers could leave some customers switching to these less secure and efficient retail sites especially in the case of a recession.

While the growing middle class in China does support the business case of JD’s slightly more premium offering, a recession which limits consumer discretionary spending could see the tides switch in favor of JD’s slightly more budget oriented competitors.

The increasingly restrictive approach to free-market business the PRC’s government headed by Xi Jinping could also cause issues for JD stakeholders. The strong belief that no corporation should hold more power (be it soft or economic) than the government could essentially place a cap on JD’s ultimate growth potential.

From an ESG perspective, the risk of poor business ethics arise when discussing JD’s extensive business operations. Within China, rising awareness of workers' rights, employment conditions and overtime pay could harm JD’s reputation along with significantly increasing personnel expenses.

Environmental sustainability is also questionable with a significant portion of JD’s logistics solutions revolving around traditional carbon-emitting technologies. However, the company has begun a dedicated push towards electrification and the reduction of greenhouse gas emission from its business operations.

Summary

JD offers customers in the PRC a unique and highly attractive way to shop online. Their incredibly fast delivery network combined with a great catalogue of products on offer has built the company a substantial economic moat which looks set to provide the company with potential margin growth for many years to come.

A turnaround from lackluster FY21 results to significant profitability and future margin expansion potential in FY22 has recently been complemented by a strong Q1 of FY23. While 2023 still looks a little uncertain from a macroeconomic perspective, JD’s robust set of revenue streams and solid profitability even at their current scale should help the company retain value for shareholders even in the event of a recession.

Given the massive discount currently present in the valuations of this solid business, I gladly award JD.com with a Strong Buy rating thanks to huge 61% undervaluation currently present in shares. I believe now is the time to buy a high-quality business at a truly remarkable price.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.