Joe Raedle

Introduction

It's time to talk about the Lennar Corporation (NYSE:LEN). America's second-largest homebuilder, with a market cap of roughly $37 billion, is about to report its second-quarter earnings tomorrow. That's not just interesting for people who own and follow the LEN ticker but also for investors seeking valuable homebuilding intel. Lennar is the first homebuilder to report industry trends for May in a market that shows extremely unusual demand trends.

While pressure on housing is building, homebuilders remain in a fantastic spot, thanks to dwindling existing housing supply and expectations that a Fed pivot might further fuel demand.

In this article, we'll assess why Lennar is trading at an all-time high and what it means for the risk/reward going into earnings.

So, let's get to it!

Why Homebuilders Are Doing So Well

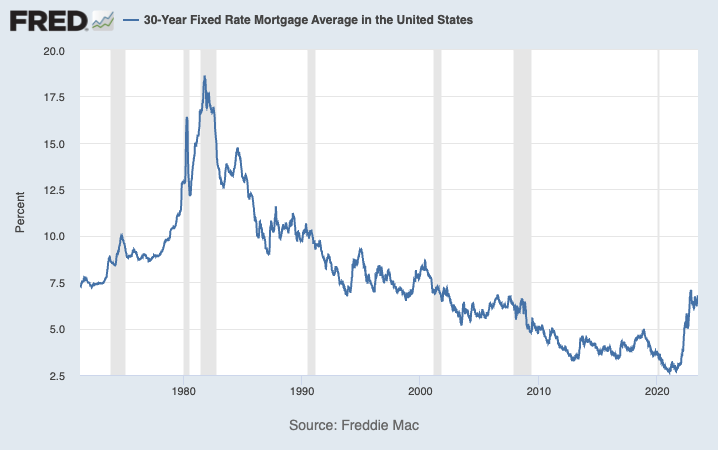

In the United States, the average 30-year fixed mortgage rate is now back at 6.7%, which means it has been hovering close to 7% since September of last year. While this is nothing compared to what borrowers were dealing with in the 1970s and 1980s, it's above levels the market witnessed prior to the Great Financial Crisis.

Federal Reserve Bank of St. Louis

Nonetheless, homebuilders are booming.

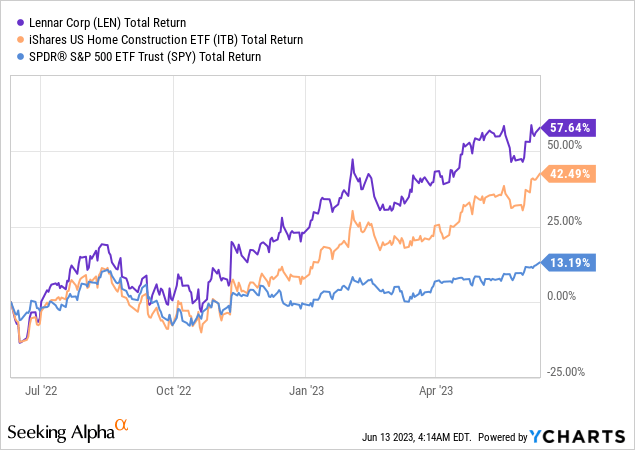

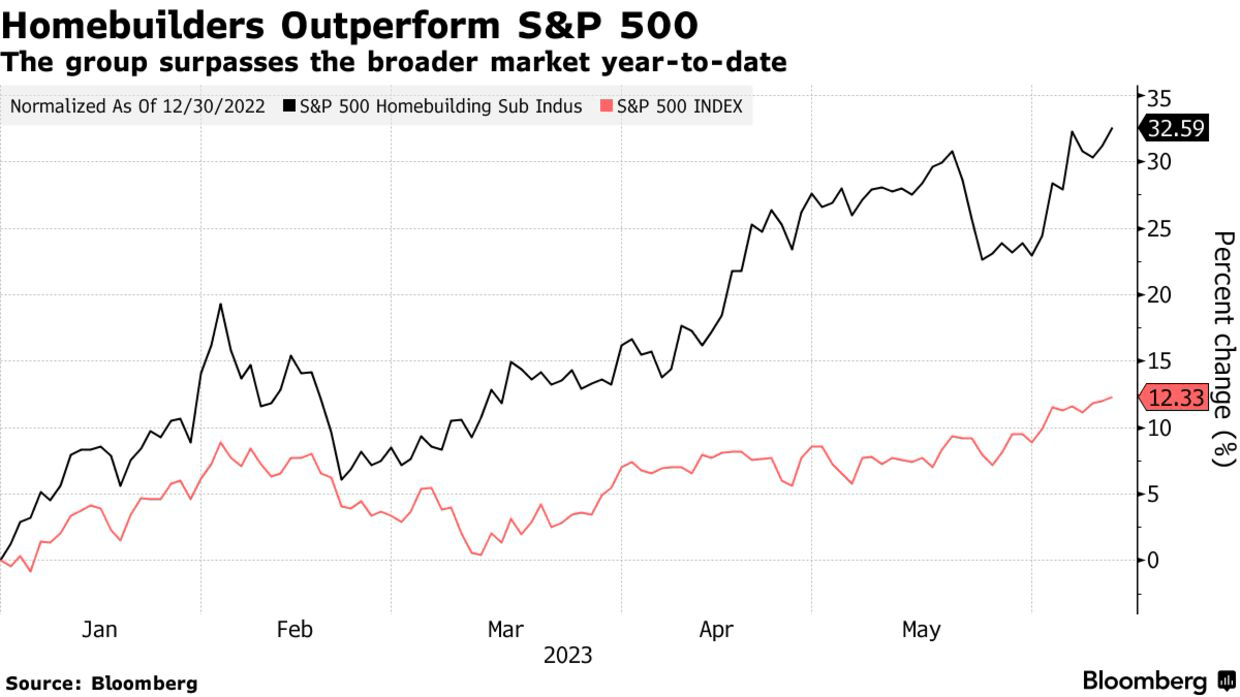

Over the past 12 months, homebuilders (ITB) have returned 42%, beating the S&P 500 by almost 30 points. Lennar shares have risen by almost 60% during this period.

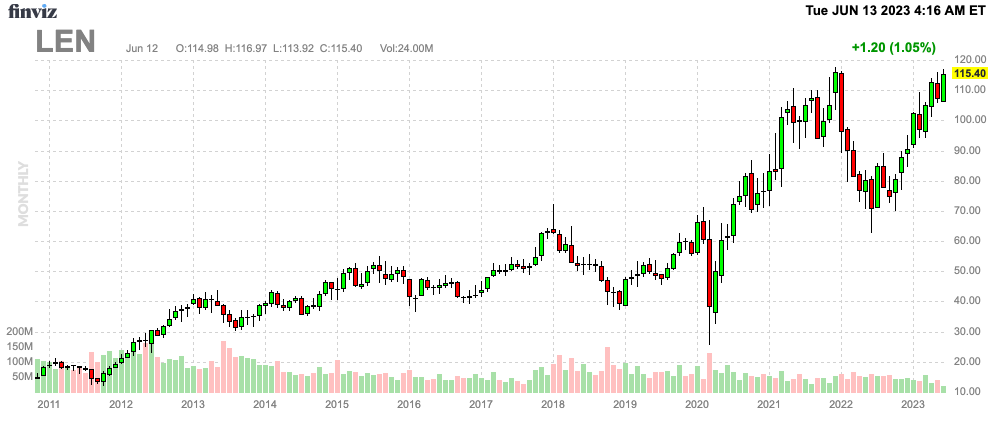

After rising by almost 28% year-to-date and 85% from their lows, Lennar shares are now back at their all-time high, going into a very important earnings call.

FINVIZ

What we're dealing with here is a fascinating trend caused by an unexpected factor: unaffordable rates.

Last month, I wrote an article titled Homebuilders: This Bubble Could Pop. In that article, I highlighted a widening divergence between existing and new home sales.

After all, rising rates, terrible consumer sentiment, and declining economic growth impact housing demand. Just not the way the market initially expected.

Because of elevated rates, people aren't selling their homes. Selling would potentially mean moving into a more expensive home, which comes with new financial obligations. This time at higher rates. This is especially bad for people who used very low rates in the past few years to finance their purchases.

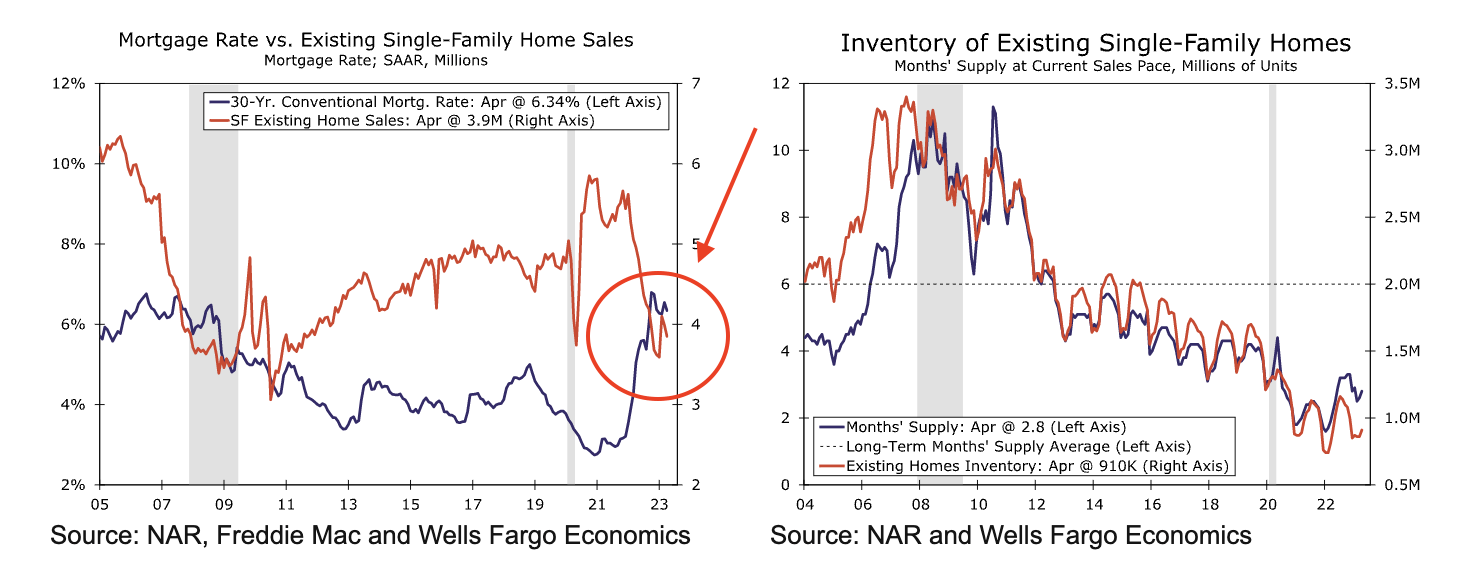

So, looking at the chart below, we see that existing single-family home sales are well below the levels witnessed between 2010 and 2021. The relationship with rising rates is clearly visible.

Wells Fargo (Author Annotations)

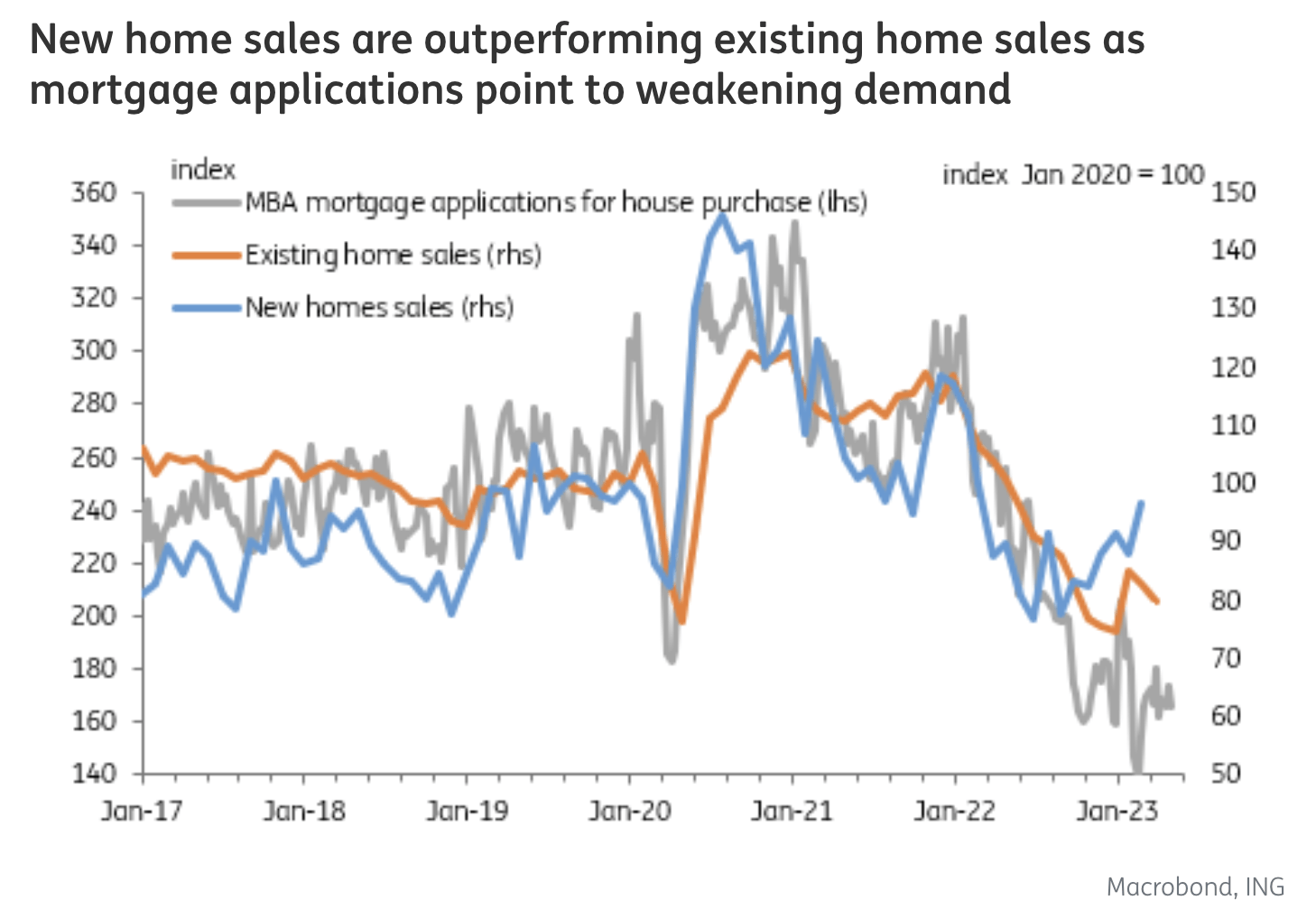

The chart below also shows existing home sales. However, the chart also shows new home sales, which are increasing despite high mortgage rates.

ING

As a result, slightly more than a third of all single-family home sales are new home sales. The longer-term median is close to 15%.

So, essentially, homebuilders are benefitting from:

- People refuse to sell their homes in a high-rate market while secular demand for homes remains high.

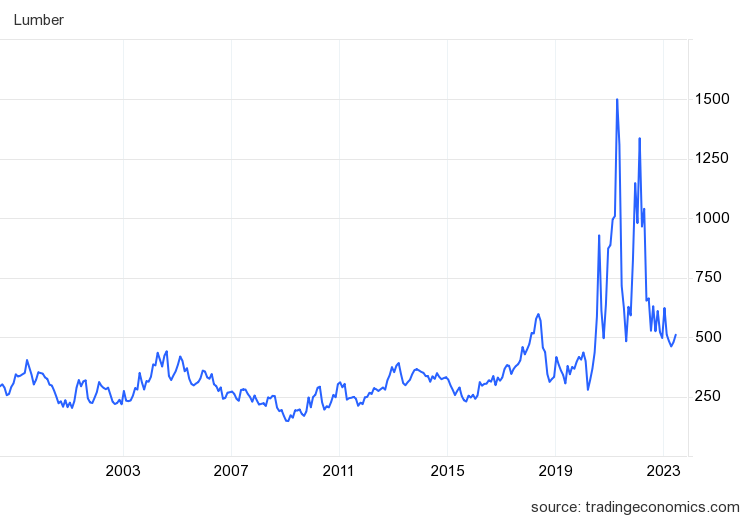

- Falling inflation, which makes building homes more profitable. As the chart below shows, lumber prices have come down significantly from their recent highs.

TradingEconomics

But wait, there's more.

Why Analysts Are Betting On Homebuilders

Analysts are now adding a new part to the bull case, consisting of an expected Fed pause. On June 12, Bloomberg published an article highlighting why analysts like Citigroup are expecting things to get even better for the nation's largest homebuilders.

Bloomberg

Essentially, the analysts, led by Anthony Pettinari, believe that the homebuilding sector has the potential to benefit from underappreciated price increases, larger builders gaining market share from existing homes and smaller private companies, as well as the expansion of multiples as housing forecasts are revised upward.

In a note published on Monday, they highlighted that net orders for the top three builders - D.R. Horton (DHI), Lennar Corp., and PulteGroup (PHM) - have remained relatively stable but are expected to experience further acceleration in the second half of the year due to favorable volume compositions.

In contrast, net orders declined by 23% year-over-year during the second half of 2022. While much of this growth is likely already priced into the stocks, Citi analysts consider the execution of volume growth as a positive catalyst for the remainder of the year.

Bloomberg

Furthermore, analysts also noted that there is potential for a recovery in builder sales prices that has not been fully reflected in the stocks. Builders have been cautiously increasing prices and reducing incentives in select markets, which could add unexpected sales and margin tailwinds in the upcoming earnings season.

It also needs to be said that the big guys are dealing with potential market share tailwinds.

- A limited inventory of existing homes available for resale has created an opportunity for new home inventories to expand without causing oversupply.

- Large public homebuilders, benefiting from greater resources compared to smaller competitors and private builders, have successfully navigated supply chain disruptions caused by the pandemic and the recent credit tightening resulting from the Silicon Valley Bank collapse.

- As a result, the top three public builders have experienced a significant increase in new home sales, accounting for 30% of total new home sales compared to 25% before the pandemic and 14% following the global financial crisis.

So, what to expect from Lennar?

Lennar's Upcoming Earnings

Tomorrow (Wednesday, June 14), Lennar will report its earnings after the market close. While we can only guess what these numbers might look like, one thing is for sure, Lennar is the first homebuilder to formally report homebuilding trends for the month of May.

All eyes will be on:

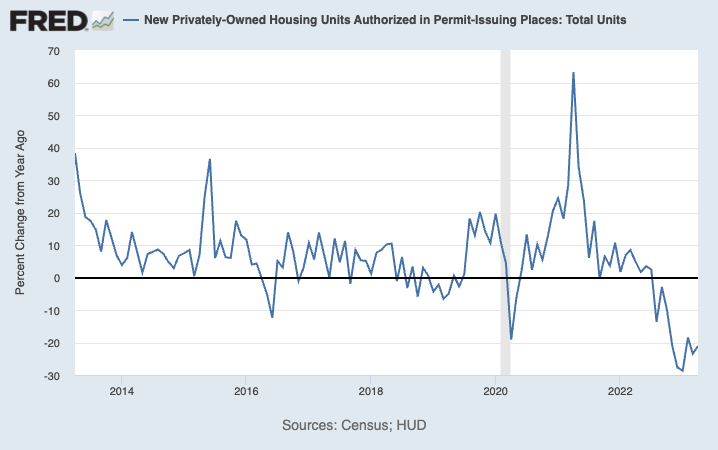

- Investors are likely looking for strong new orders as a result of the tight existing housing supply. When assessing these numbers, we also need to look for the cancellation rate, which is likely to remain elevated, as some people cannot take the elevated rates anymore. Also, in light of these developments, it needs to be said that building permits (until April) were still down. I expect the company's new orders to beat the contraction in new orders. In this case, I'm incorporating the likelihood of market share gains.

Federal Reserve Bank of St. Louis

This is what the company said in the first quarter with regard to orders and cancellation rates:

Our first quarter cancellation rate improved to 21.5%. While this is higher than the 10.2% last year, it is decidedly lower than the 26% last quarter and has been falling in each consecutive month. While our new orders were down some 10% year-over-year, that result has compared favorably to reported market conditions and enabled us to maintain a strong start pace that enables us to increase our expected closings for the year to a range of 62,000 to 66,000 homes delivered.

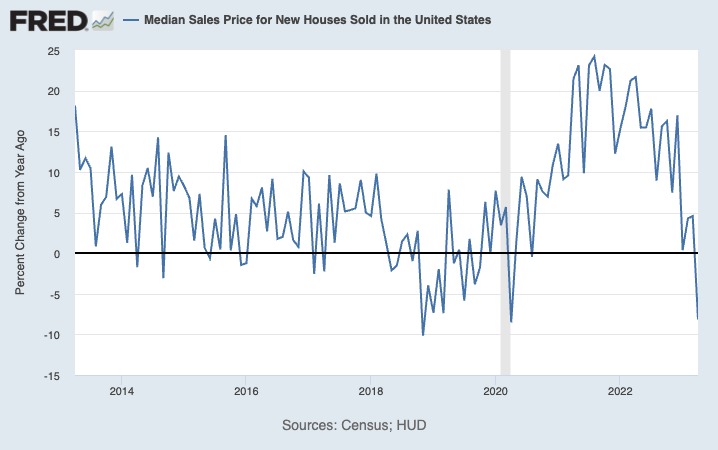

- Investors will be interested in margins, as lower lumber and material costs, on top of easing supply chain headwinds, should provide the company with higher margins. However, I believe that margins could be pressured by lower selling prices. The median sales price of a new home in the United States fell by 8% in April, making it one of the steepest slumps in the past ten years.

Federal Reserve Bank of St. Louis

In other words, while we're dealing with secular tailwinds like slow existing home supply and potential margin improvements, the situation is far from perfect, which is why I distrust the company's all-time highs.

With all of this in mind, here's a cheat sheet based on the company's own comments in 1Q23.

- Lennar anticipates new orders for Q2 to be between 16,000 and 17,000 homes, while their ending community count is projected to remain relatively stable or experience slight growth compared to the previous year.

- As for Q2 deliveries, they expect to deliver approximately 15,000 to 16,000 homes, with an average sales price ranging from $435,000 to $445,000, reflecting their strategy to align prices with the market.

- Lennar foresees gross margins in the range of 21% to 21.5% for Q2, and their selling, general, and administrative expenses (SG&A) are expected to fall within the range of 7.2% to 7.4%.

- Lennar estimates that its earnings per share result for the second quarter will fall within the range of $2.10 to $2.55.

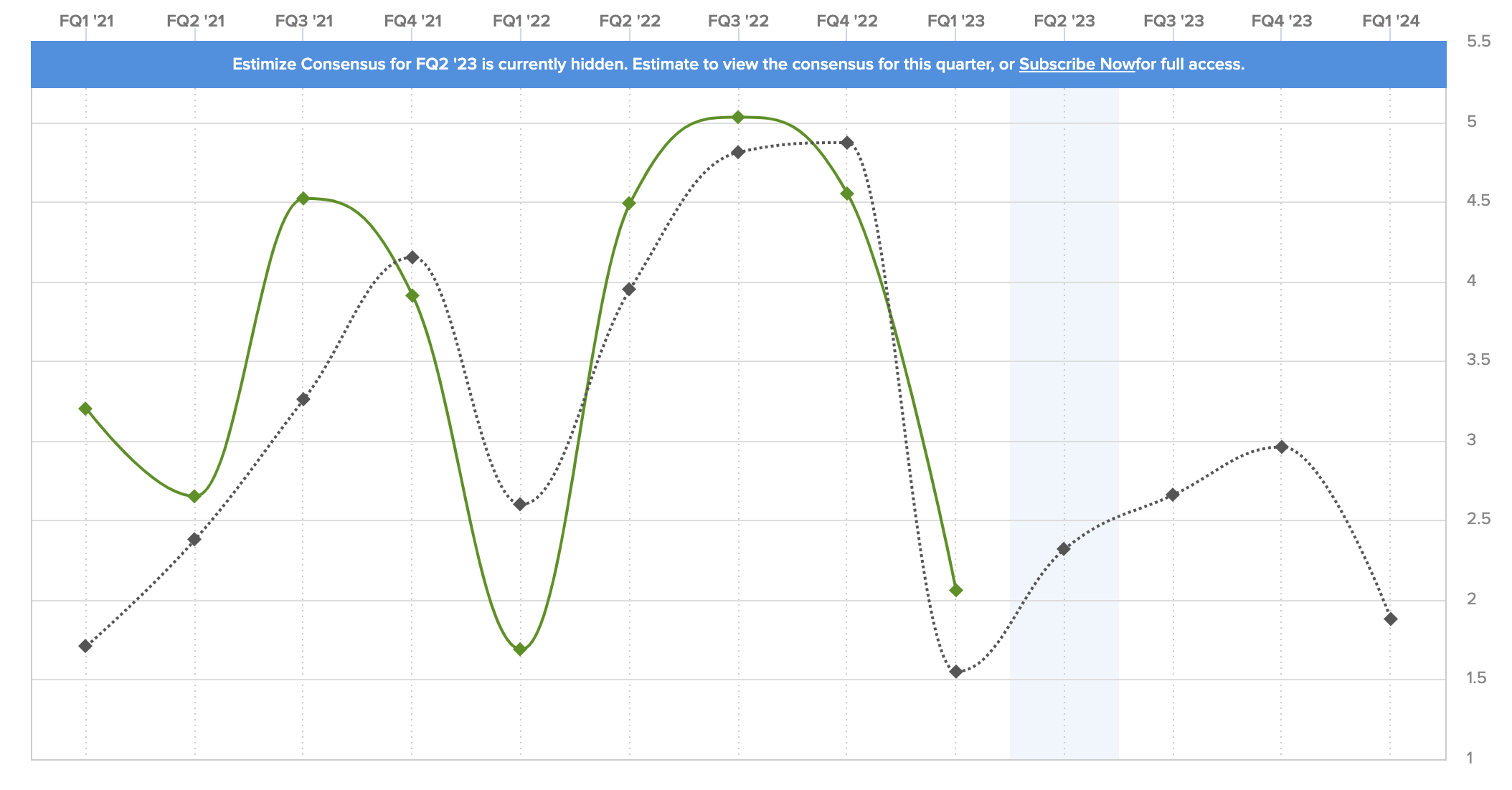

Seeking Alpha reported that the consensus EPS number is $2.30, which is roughly the midpoint of the company's own guidance.

This is what the visualization of past and future EPS expectations and actual results looks like:

Estimize

With all of this in mind, I urge investors to be careful. While LEN might report strong earnings and hint at even stronger growth, causing its stock price to rally, I do not like the risk/reward.

As I wrote in my prior homebuilding article:

While the current market conditions appear favorable for homebuilders, there are mounting risks that make the risk/reward of investing in homebuilding stocks less favorable in the long term. A potential shift in unemployment could have a significant impact on the housing market, causing higher default rates, increased supply, falling property prices, and a decline in new home construction.

The ongoing hiking cycle and the potential need for aggressive rate cuts in the future due to weakening economic growth could exacerbate these risks.

I reiterated my stance in a recent article on the Fed and my expectations that rates will likely remain elevated longer than the market expects.

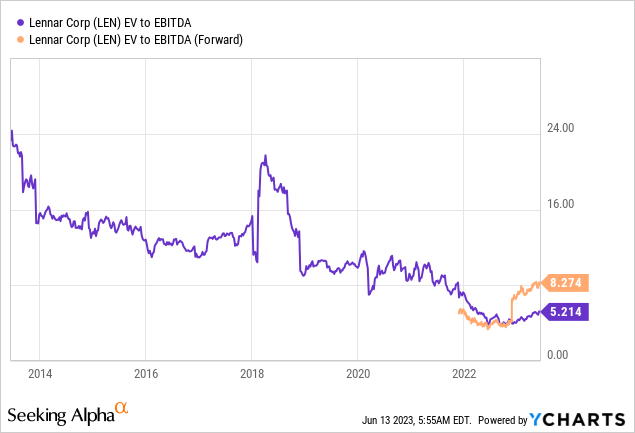

Moreover, while 8.3x NTM EBITDA isn't overvalued, I believe it supports my case that the risk/reward is far from perfect at this point.

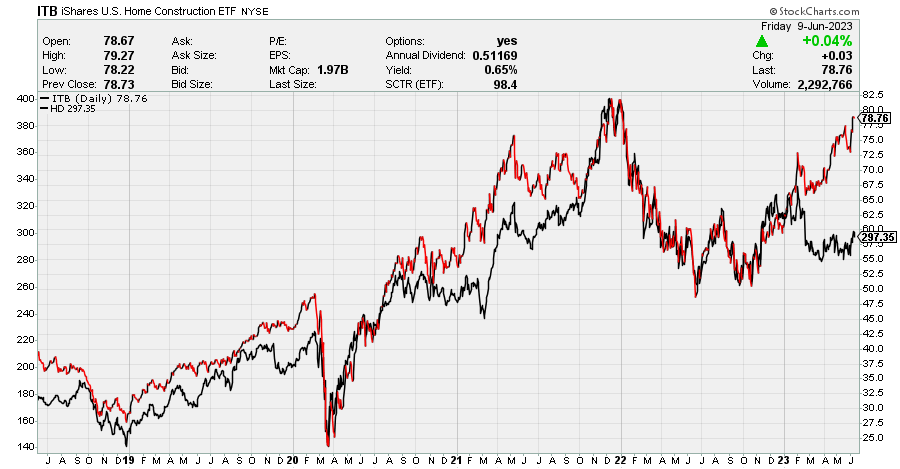

Additionally, we're seeing that building-related stocks like Home Depot (HD) aren't buying the homebuilding rally. Usually, HD does well when homebuilders are thriving. This time, that's not the case, as the homebuilding rally is mainly driven by a low supply of existing homes. Also, retailers like HD suffer from poor consumer sentiment (which drives homebuilder cancellation rates).

StockCharts (Black = HD, Black/Red = ITB)

So, to reiterate my view, I dislike homebuilders at current levels, despite voices getting stronger than a more dovish Fed could fuel the rally even further.

Lennar's upcoming earnings report will likely show if we're dealing with deeper cracks in the bull case or if everything is as peachy as the market lets us believe.

Takeaway

Lennar Corporation, America's second-largest homebuilder, is set to report its second-quarter earnings amid a housing market that continues to defy expectations. Despite rising mortgage rates, homebuilders have experienced significant success, with Lennar's stock reaching an all-time high.

The key driver behind this trend is unaffordable rates, which have led homeowners to hold onto their properties rather than sell, resulting in a tight existing housing supply.

Additionally, factors such as falling inflation, lower material costs, and potential market share gains have contributed to the positive outlook for homebuilders.

However, caution is advised as risks loom, including a potential shift in unemployment rates and the impact of rising interest rates. It remains to be seen whether Lennar's upcoming earnings report will reinforce the bullish sentiment or reveal underlying weaknesses in the market.