Michael M. Santiago

By and large, in spite of recent volatility driven by interest rate fears, the market this year has still been quite kind to most tech stocks. And while many enterprise-facing companies are facing post-pandemic demand weakness as companies cut budgets and spend, a lot of consumer-facing tech is still enjoying bountiful tailwinds.

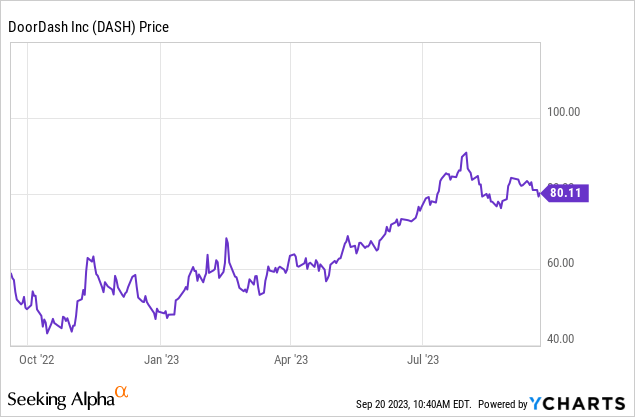

DoorDash (NASDAQ:DASH), the well-known food delivery app, is still enjoying double-digit growth in revenue and bookings after the initial pandemic lift. Year to date, shares have jumped more than 60%: but in spite of this strength, I still think there's plenty of upside ahead.

I'm initiating coverage on DoorDash as bullish. In my view, here are the core drivers of the bullish thesis for DoorDash:

- Prominent brand and broad market coverage in U.S. restaurants - Though smaller than Uber Eats, DoorDash is broadly available nationwide and continues to grow. Through acquisitions, DoorDash also has operations overseas, giving it a massive TAM.

- Subscription program to drive recurring revenue and loyalty - The $10/month DashPass program offers free delivery fees and discounted pickup orders, encouraging not only a buildup of recurring revenue but also driving more frequent orders among DoorDash's most ardent customer base.

- Growth via partnerships - DoorDash has inked a number of prominent partnerships with a variety of companies, including banks (a number of premium credit cards offer DashPass at a discount or free). It has also expanded its convenience/delivery business by opening its network to a wide array of retail chains.

- Favorable margin profile - Though its delivery business is at a smaller revenue scale than Uber's, it has a favorable adjusted EBITDA margin profile.

- Cash rich - The company has more than $4 billion in net cash, unencumbered of debt, sitting on its balance sheet, providing for ample financial flexibility.

There's a lot to like here, especially after a recent fall from the $90s notched in July. As DoorDash continues to dip, look for a buying opportunity.

Sustained double-digit growth

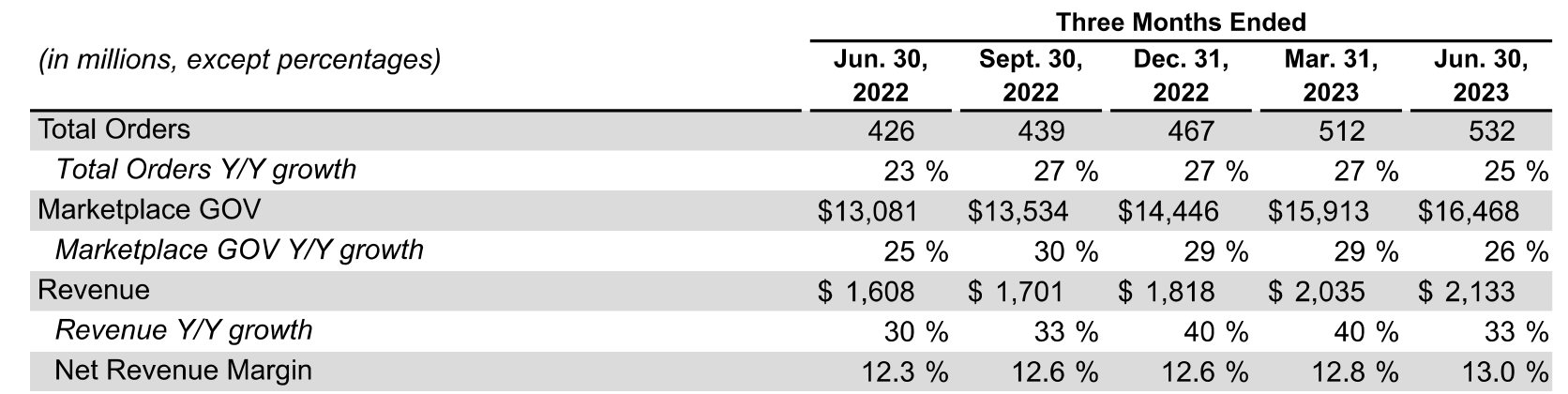

One of the core reassuring factors here is that DoorDash continues to grow aggressively post-pandemic. In the most recent quarter (Q2), DoorDash achieved 25% y/y growth in order volume, 26% y/y growth in marketplace gross order value (bookings) to $16.47 billion, and revenue grew 33% y/y to $2.13 billion, exceeding Wall Street's expectations of $2.06 billion (+28% y/y).

DoorDash top line metrics (DoorDash Q2 earnings release)

Consumers prefer convenience and the fact that many of us have reallocated time to commuting to the office, this preference has continued to prop up delivery demand post-pandemic, against the consensus of most market-watchers at the time who thought that Uber Eats and DoorDash enjoyed one-time benefits during COVID.

It's worth noting as well that DoorDash's offerings have diversified broadly across retail and grocery, which is a specific focus of the management team. Per CEO Tony Xu's remarks during the Q&A portion of the Q2 earnings call, detailing the evolution of the non-restaurant categories:

And I think when it comes to a lot of these categories outside of restaurants, I think you saw a lot of that growth for us happened in the first couple of years of the pandemic in which we launched with third-party convenience retailers, whether they be the likes of Walgreens, CVS, 711, and many, many others. But then, over the last 2.5 years, we built a multibillion dollar grocery business from scratch. And it was really ready for primetime exposure. And that's one of the things that you saw, as we now have more non-restaurant stores on the platform in North America versus any other platform. We're growing faster than every other platform and gaining share dramatically in virtually all categories. And certainly -- and very specifically also in grocery.

You also see this in retail. We've seen a lot of growth in categories that is even outside of food, whether that be in sporting goods with Dick's Sporting Goods, or office supplies with Office Depot and OfficeMax, or the pet category with PetSmart and Petco, or the Health and Beauty category with Sephora. So a lot of this is happening. And we found ourselves in a position where not only were we seeing very resilient growth in the core U.S restaurants category, at all-time high frequencies, which gives us just more shots and goal to introduce a lot of these new categories. But we also saw the readiness in terms of product market fit from a selection, quality of service and affordability perspective, when it came to our grocery and our retail offerings. And that's why we made the announcement and why we shipped the features that we did in June."

Expansion in non-restaurant categories, as well as continuing to fulfill gradual international expansion ambitions, will be key to growth going forward.

Favorable margin profile versus Uber

We should also take note of the fact that DoorDash's margin profile has continued to improve.

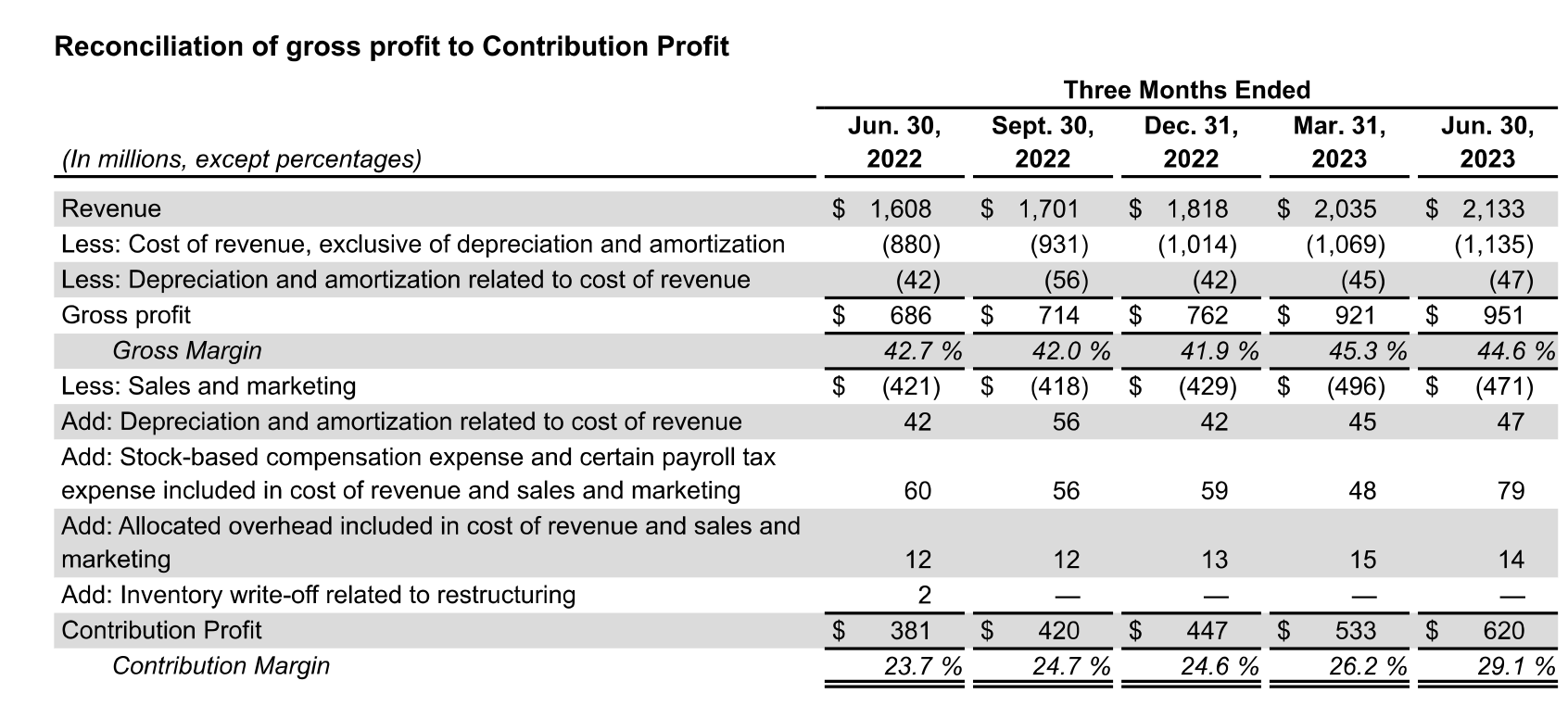

Marketplace take rates shot up to an all-time high of 13.0% in Q2, up 20bps sequentially and up 80bps y/y, which helped to drive order contribution margins to a high of 29.1%, up 540bps y/y:

DoorDash contribution margin (DoorDash Q2 earnings release)

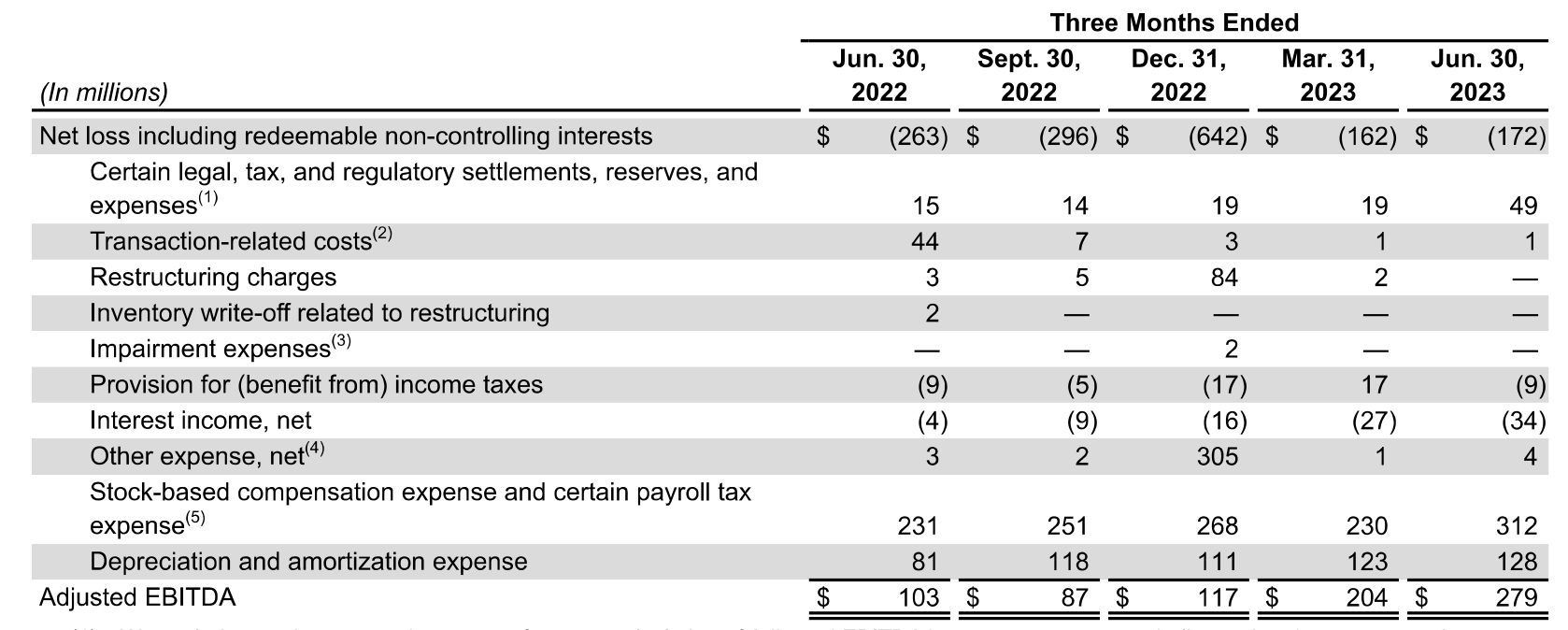

In turn, DoorDash has also scaled its adjusted EBITDA to $279 million: up 2.7x y/y, and representing a 13.1% margin of revenue or 1.7% of marketplace bookings.

DoorDash adjusted EBITDA (DoorDash Q2 earnings release)

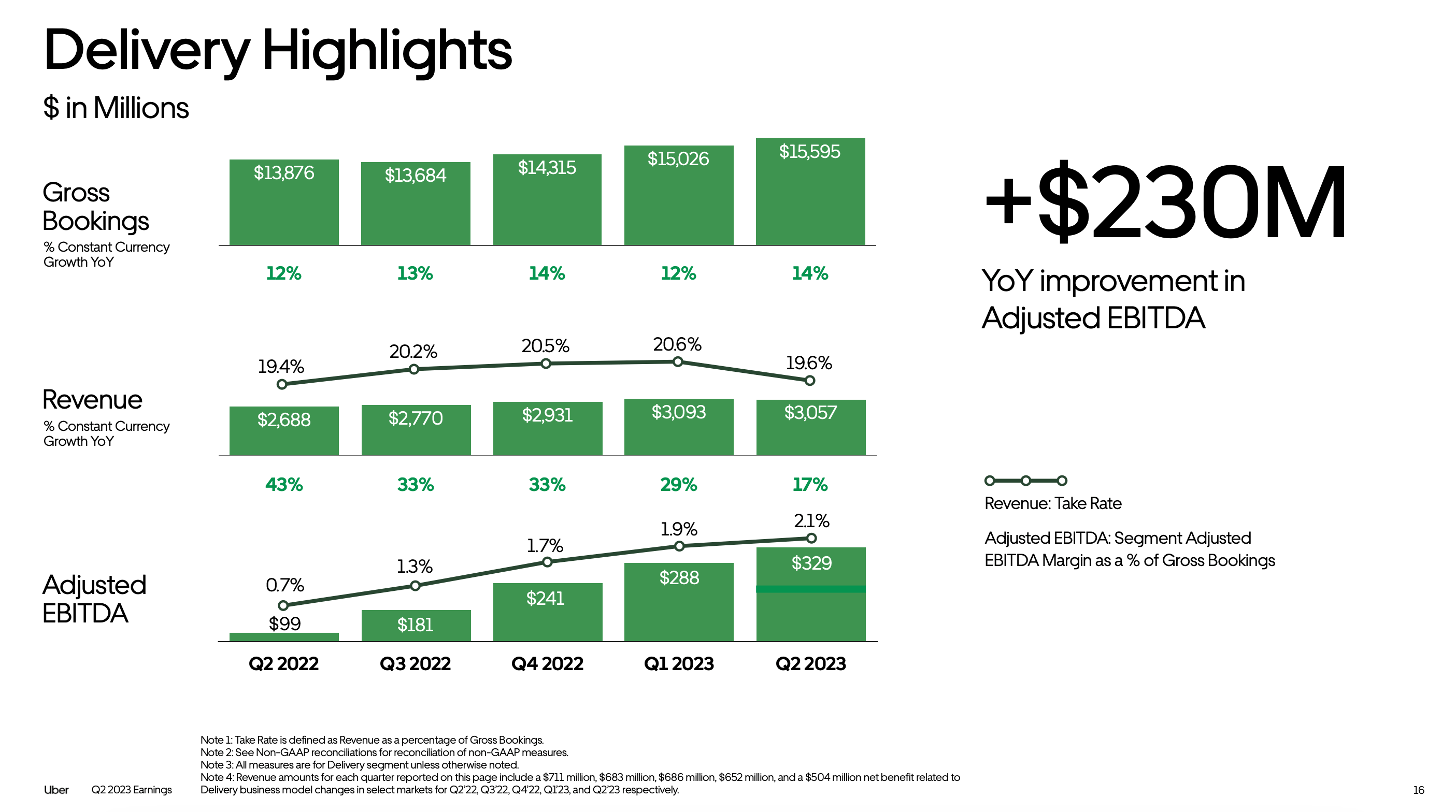

You'll note that as a percentage of revenue, DoorDash's adjusted EBITDA margin of 13.1% is better than Uber's at 10.8% (see chart below):

Uber comparison (Uber Q2 earnings release)

This is in spite of DoorDash's revenue scale being at approximately two-thirds of Uber's scale. Note that Uber's Delivery segment has a 19.7% take rate on gross bookings, whereas DoorDash's stands at only 13.1%. This is a matter of pricing and fees charged - to me, this indicates that either DoorDash has room to boost fees to match Uber, or it will continue to see superior growth to Uber driven by better pricing.

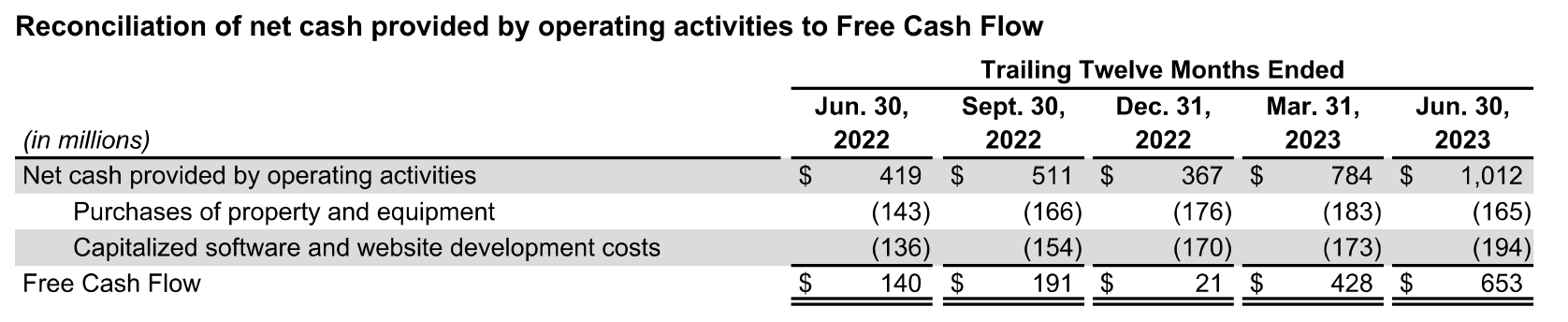

It's also worth noting that year to date, DoorDash has generated over $1 billion in free cash flow:

DoorDash FCF (DoorDash Q2 earnings release)

Valuation and key takeaways

Needless to say, DoorDash isn't cheap after this year's run. At current share prices near $80, the company trades at a market cap of $31.41 billion. After we net off the $4.13 billion of cash on the company's most recent balance sheet, DoorDash's resulting enterprise value is $27.28 billion.

Meanwhile, for next year FY24, Wall Street analysts are expecting DoorDash to generate $9.84 billion in revenue, up 17% y/y - putting DoorDash's revenue multiple at 2.8x EV/FY24 revenue. If we conservatively assume the current 13% adjusted EBITDA margins hold on next year's revenue, the company's adjusted EBITDA multiple is 21.1x EV/FY24 adjusted EBITDA.

Considering DoorDash's growth premium, its recent streak of solid margin gains, and broad market opportunity, I'd say this is a bet worth making.