Susan Vineyard

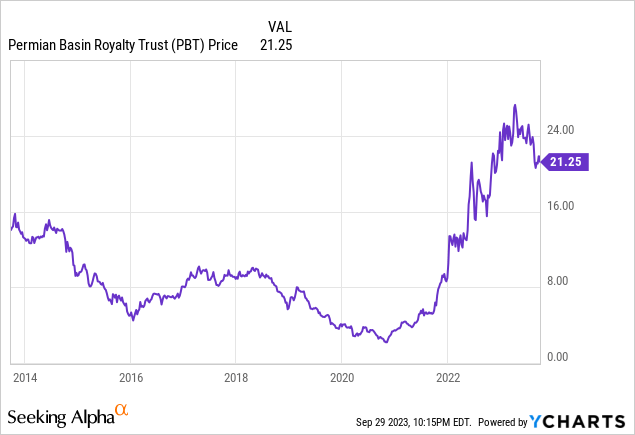

Permian Basin Royalty Trust (NYSE:PBT) has dropped more than 20% since my April sell recommendation article, and I still consider it a sell. Production at the Waddell Ranch has been somewhat disappointing given very high capex over the last 2-3 years. Oil and natural gas production is being sold at prices that are lower than last year, and PBT investors are being negatively impacted because the trust can't hedge against lower prices. This trust, which has effectively become an E&P energy company, is a risky way to invest in the energy industry.

Waddell Ranch - Large Capex and Oil/Gas Production

This is an update to my April 19 article on Permian Basin Royalty Trust, which is approximately 87% oil and 13% natural gas based on the latest quarterly revenue figures. My focus will be mostly on the Waddell Ranch, which is located in Crane County, Texas, production results after the massive increase in capex over the last three years. The production still trends slightly higher this year after a dramatic increase in the prior two years, but PBT investors wonder when they will finally get a monthly distribution from Waddell Ranch because capex remains so large. Investors look mostly at Waddell Ranch because Texas Royalty Properties are only a relatively modest amount, and their production just continues to slowly decline.

Waddell Ranch

Production (gross) and Capex (gross)

Writers combination of data from trustee (pbt-permian.com)

2023 Monthly Production (gross) Capex (gross) and Prices

Writers combination of data from trustee (pbt-permian)

Because monthly capex has often been greater than the monthly net profit interest, there have been no distributions from Waddell Ranch in the last few years. The very modest PBT distributions have been from Texas Royalty Properties. With higher energy prices and higher production, the Waddell Ranch results from July produced a net profit interest - NPI of $1,548,797, which reduced the cumulative deficit to $(213,227).

Going forward, in order to produce an NPI that enables a "normalized" monthly distribution from Waddell Ranch, production has to increase, oil/gas prices have to increase, capex has to decrease, or some combination of these factors. PBT investors might be able to make some rational near-term estimates for production and prices, but capex is a big unknown. What are privately held Blackbeard Operating's capex plans for next year and the year after? We don't know.

According to the January distribution press release, the planned capex for 2023 was going to be $135 million (net to the trust) with a "projection of about 55.5 new drill wells and 45 recompletions along with about 37.5 plug and abandoned wells." That was reduced to $122 million and 48.75 wells in the February press release and further reduced to $96.8 million and 30.75 new wells in the March release. According to that press release: "This revision of the previously announced budget is the result of reviewing the current and future activity of the industrial environment of the Waddell Ranch." It's unclear if these changes were made because the other wells no longer were expected to be profitable, or they were just deferring the planned drilling to sometime in the future.

PBT investors have to remember that Blackbeard Operating has no fiduciary responsibility to maximize profits for PBT investors. The trust only has a 75% net overriding royalty interest in Waddell Ranch. I assume that Blackbeard hedged some of the current production at much higher oil/gas prices last year and is, therefore, making a very large profit. Because the trust can't hedge, PBT investors are not. The question remains: When is Blackbeard going to reduce capex? When do energy prices drop? When drilling and workovers are no longer producing profitable results for this mature field? We don't know. Usually, capex plans are announced in monthly distribution press releases in January or February for that year.

A major factor in capex decisions is actual recent results. I was able to find some recent information in a non-subscription source (copyright issues), High Plains Observer, for Blackbeard Operating in a different field in Texas that was rather disappointing:

Week of September 18-24, 2023 Gas Completions HEMPHILL (BUFFALO WALLOW, Granite Wash) Blackbeard Operating, LLC, #2H Meek 238, 18 mi SW from Canadian, Sec 238, Blk C, G&MMB&A Surv, A-606, spud 7-17-2011, compl 10-6-2011, tested 8-16-2023, potential 76 mcf, 3 bbls cond, 17 bbls wtr, 169# ftp, 640# SIWHP, TVD 10935', MD 15725' API 42-211-34890, Horizontal Recompletion Reclass Oil to Gas.

Since this is not for Waddell Ranch or even in Crane County, it may not be indicative of the capex decision-making process for Waddell Ranch. It does, however, raise some concerns about their ability to select capex projects, in my opinion.

Monthly Distributions

The latest monthly distribution payable on Oct. 16 is $0.022414 per unit, which is from Texas Royalty Properties only because Waddell Ranch still has a deficit. Assuming no capex for Waddell Ranch, the total distribution would have been approximately $0.26 (total NPI of $12,228,596). For the sake of discussion, annualize this $0.26 monthly amount to get a total annual distribution of $3.12, which implies PBT is trading with a 14.7% yield using the latest $21.25 PBT price. With an annual distribution of $3.12 and a yield of 8%, PBT would trade at $39. The reality is that with no capex, oil/gas production would drop significantly going forward and so would the distributions. It is, however, interesting to look at.

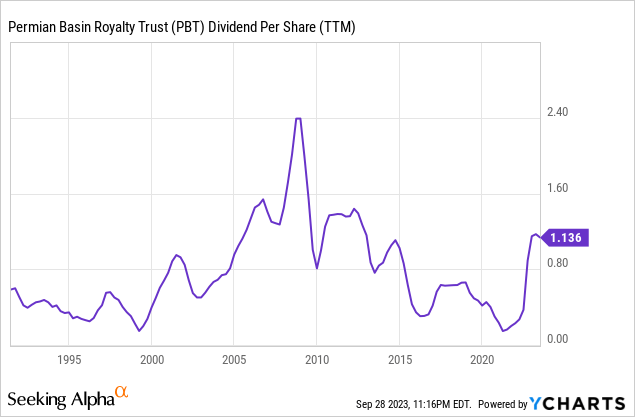

(Note: The chart states "dividend" - it is actually a distribution per unit.)

Since PBT trades on potential future distributions and the resulting yields compared to U.S. treasuries, the significantly higher yields over the last 20 months had a negative impact on PBT price. Yield changes can have a dramatic impact on PBT prices. Just for the sake of illustration, assume the annual distribution is $1.20 (also ignoring any tax impacts), with a 6% yield, PBT would trade at $20.00; and with an 8% yield, it would trade at $15. With U.S. 10-year notes currently yielding about 4.6%, the difference between a PBT yield of 8% is only 340 basis points and the difference with a two-year Treasury is only 296 basis points, which is not enough to justify the risk of owning PBT, in my opinion.

Given the level of high interest rates currently and because PBT is a risky investment, I think a "normalized" distribution yield of at least 8.5% would be appropriate. This would imply a "normalized" total annual distribution of $1.80 based on the latest $21.25 PBT price. Most of my annual distribution estimates are below $1.80 using a combination of a number of different variables. At this point, the biggest wildcard remains Blackbeard's planned CAPEX next year and going forward.

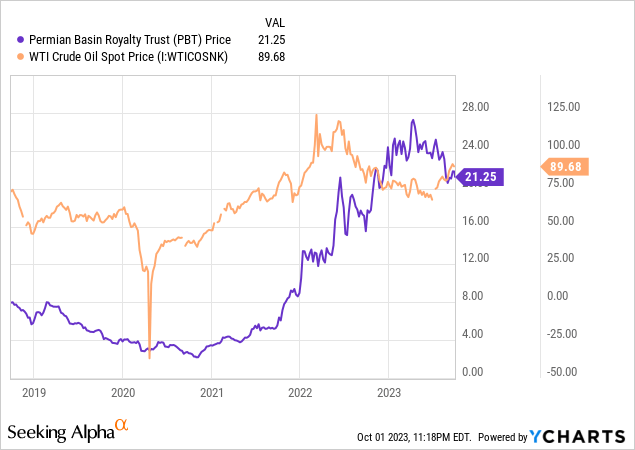

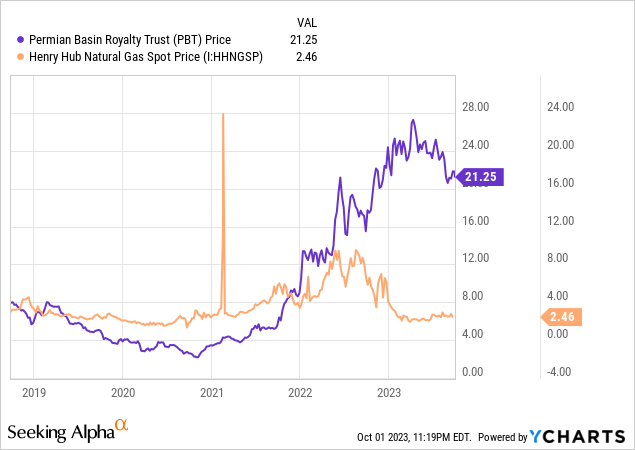

WTI Crude Oil and Henry Hub Natural Gas Spot Prices

Conclusion

PBT already had a spectacular run-up in price as both energy prices and capex increased sharply. Now, reality has settled in, and it seems that the oil/gas production is beginning to level off. How much can capex decline in order to allow for a normalized monthly distribution without dramatically reducing production? I think PBT investors are caught in a trap, especially since the trust can't hedge against lower energy prices and Blackbeard can.

They're currently selling the significant increase in oil/gas production from larger capex at lower prices than last year. Since I just don't see how the monthly distributions can be increased to a level that justifies the latest PBT price given the high level of interest rates, I consider PBT a sell.