enot-poloskun

Ecovyst Inc. (NYSE:ECVT) has seen a recent share price pullback due to weaker-than-expected earnings and a risky balance sheet. Even with this in mind, I believe that Ecovyst is currently a buy due to the firm's ability to foster innovation through partnerships, EPS growth improving its financial position, and undervaluation assuming my DCF figures.

Business Overview

Specialty catalysts and services are the focus of Ecovyst Inc., which operates both domestically and abroad, notably in the Netherlands and the United Kingdom. Ecoservices and Catalyst Technologies are the two main divisions that make up the business.

They provide essential services like recycling sulfuric acid and thorough logistics for alkylate production at refineries under the Ecoservices sector. Additionally, they offer virgin sulfuric acid, which is necessary for many industrial, mining, and water treatment applications.

The Catalyst Technologies division, on the other hand, focuses on specialized catalyst materials and process solutions for manufacturers and licensors involved in the production of polyethylene and methyl methacrylate. Their catalysts are crucial in the creation of plastics used in a variety of items, such as packaging, containers, and molded goods. This section also provides zeolite-based emission control catalysts, which are essential for lowering nitrogen oxide emissions from diesel engines and removing sulfur dioxide during fuel refining.

Ecovyst

Financials

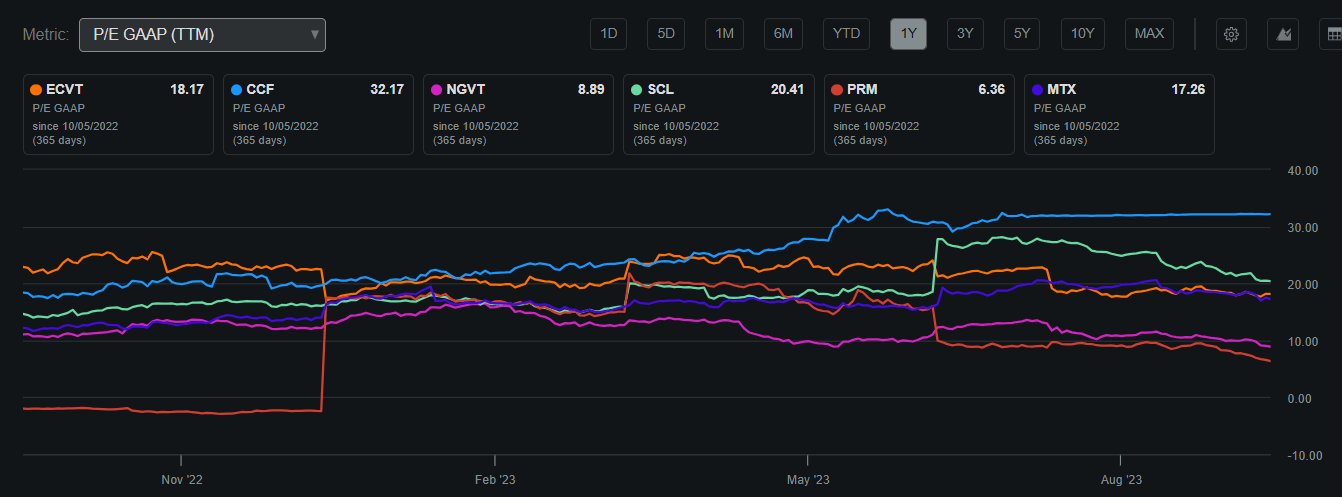

Ecovyst is currently valued at around $1.14 billion with a Return on Invested Capital of 5%. The stock is presently priced at $9.80 per share, slightly below its 50-day moving average of $10.21. Ecovyst also holds a P/E GAAP of 18.17, which is slightly below the average of its peers, demonstrating that the firm is slightly undervalued on a relative basis.

Ecovyst P/E GAAP Compared to Peers (Seeking Alpha) Share Performance (Seeking Alpha)

Earnings

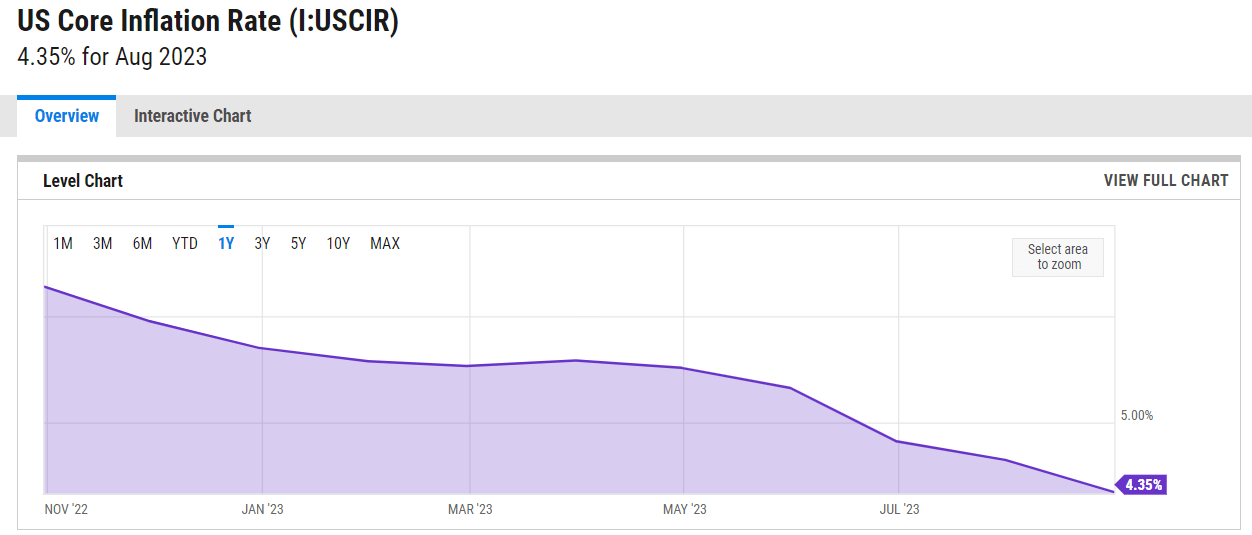

Ecovyst's Q2 2023 earnings came in mixed with a $0.01 beat on EPS at $0.29 and a $12.91 million miss on revenues at $184.1 million showing a -18.3% YoY decline. This demonstrates the strain macro headwinds such as inflation and high interest rates are having on volume for Ecovyst demonstrated through missed revenues. But, with excellent growth in EPS in 2024 and 2025, the firm will see solid growth in cash flow which could lead to solid growth in the medium term. I agree with these current projections as the firm's cost-cutting strategies coupled with core business expansion as mentioned later in this article will create synergies resulting in greater FCF to pay down debts. This is because as core inflation continues to decline as shown below, coupled with future rate declines, I believe that volume will begin to improve due to less commodity volatility. This will result in greater sales and profitability from client purchasing power which will enhance the firm's ability to pay down its leveraged position will result in reduced borrowing costs while interest rates will begin to fall resulting in a stronger long-term position.

Core Inflation (YCharts) Earnings Estimates (Seeking Alpha)

Performance Compared to the Broader Market

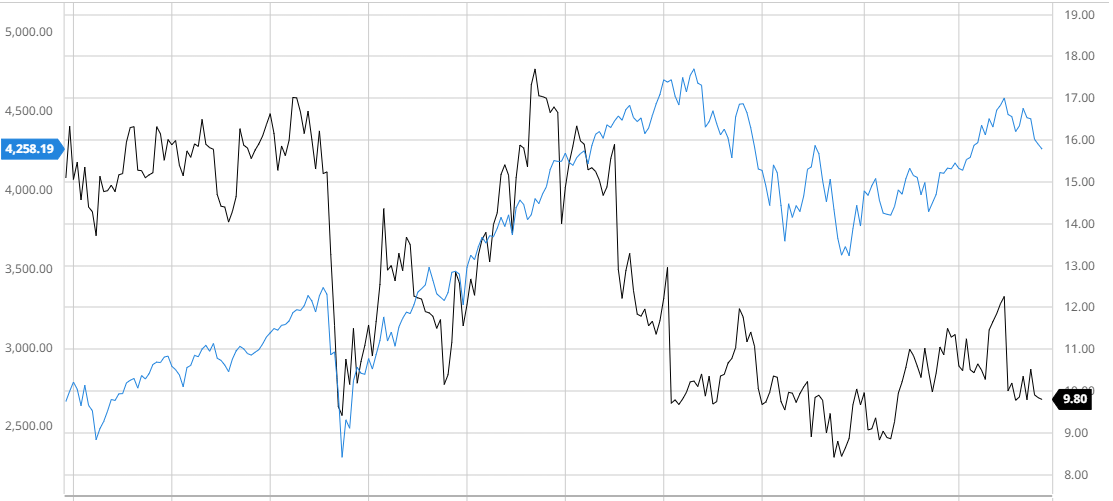

In the last 5 years, Ecovyst has significantly underperformed the S&P 500 which is recently due to the firm's underperformance in earnings along with its weak balance sheet in tough macro headwinds as mentioned later in this article.

Ecovyst Compared to the S&P 500 5Y (Created by author using Bar Charts)

Analyst Consensus

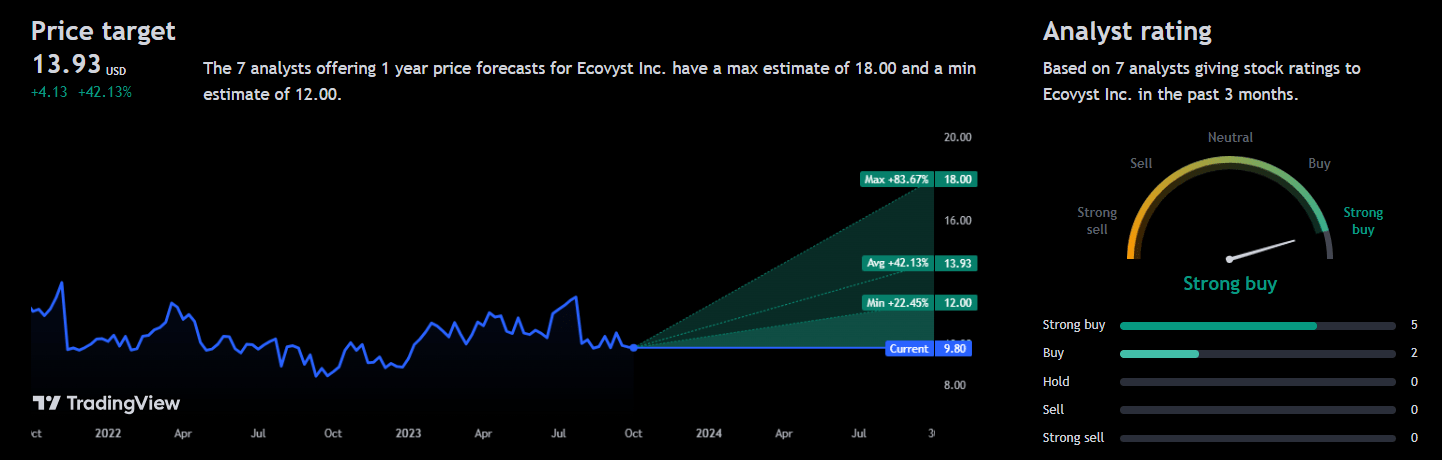

Analysts currently rate Ecovyst as a "strong buy" with an average 1-year price target of $13.93 presenting a potential 42.13% upside. This demonstrates analysts' bullish view on the firm's ability to improve cash flows to recover from its leveraged position.

Analyst Consensus (Trading View)

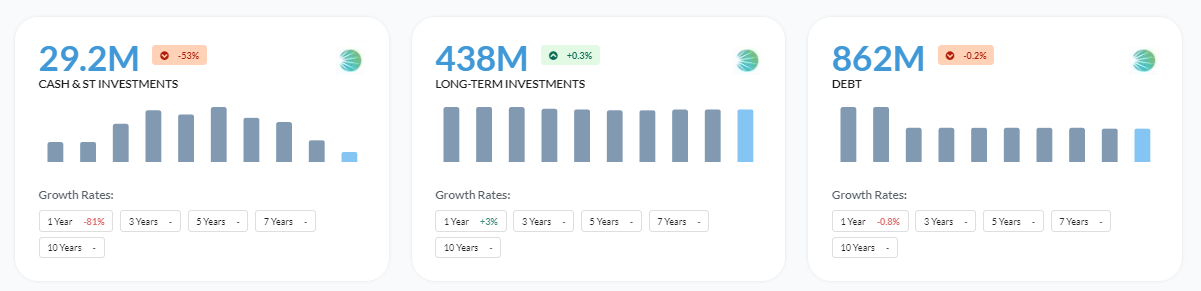

Balance Sheet

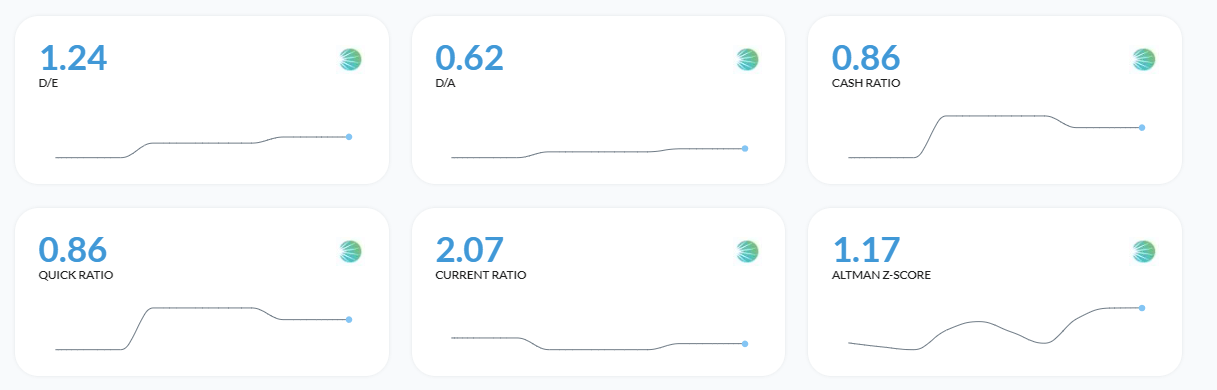

Ecovyst's balance sheet is more leveraged than I would have liked with debt remaining stagnant and an interest coverage of 3.1. With EPS recovering in 2024 and 2025, Ecovyst must utilize cash flows in order to pay down debts and deleverage to provide a more consistent and stable form of FCF. With a Current Ratio of 2.07 and an Altman-Z-Score of 1.17, Ecovyst must improve its balance sheet to prove they are solvent in the medium term.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

Valuation

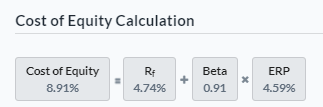

Before finding Ecovyst's fair value, I calculated the Cost of Equity for Ecovyst using the Capital Asset Pricing Model. Using a risk-free rate of 4.74% based on the 10-year treasury yield, Ecovyst's Cost of Equity is 8.91%. This demonstrates the return demanded in return for holding Ecovyst's equity.

Cost of Equity Calculation (Created by author using Alpha Spread)

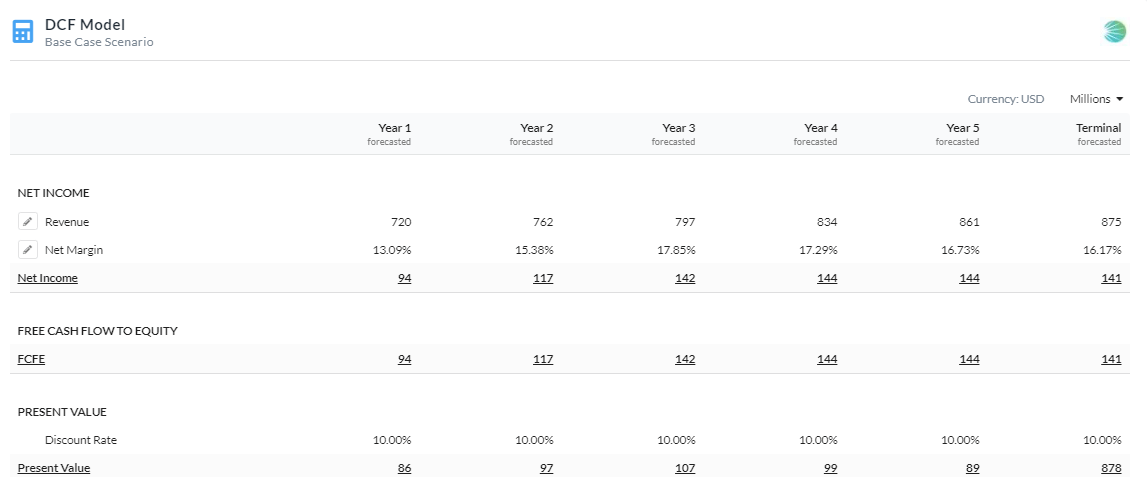

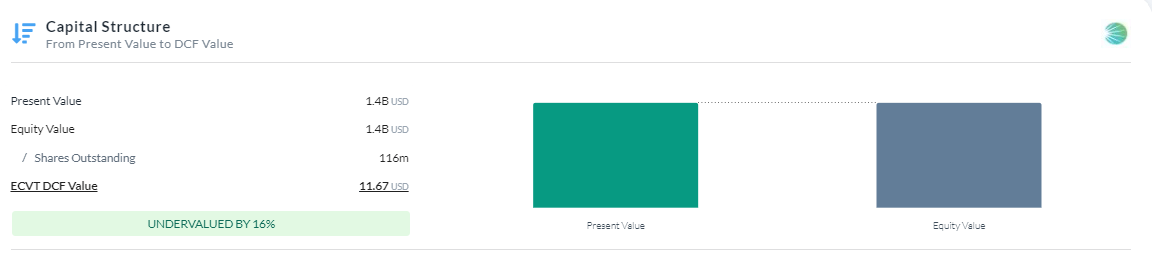

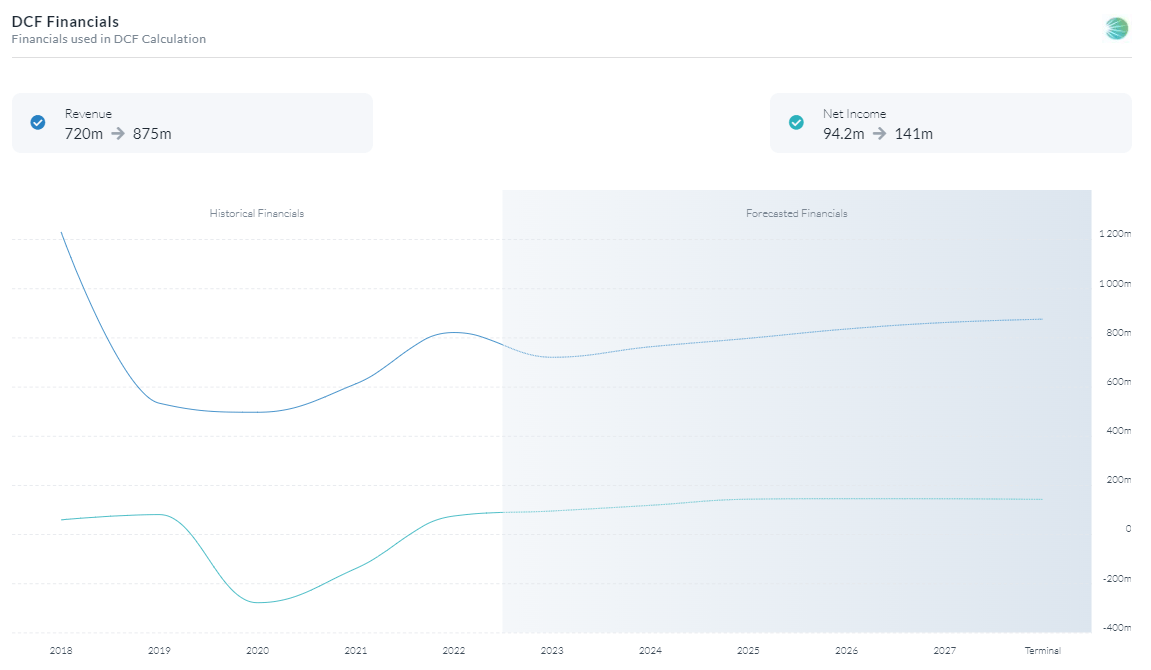

Now that I have calculated an accurate Cost of Equity for Ecovyst, I used a 5-year Equity Model DCF via net income. Assuming a discount rate of 10% indicating a 1.09% risk premium, Ecovyst is currently undervalued by 16% with a fair value of ~$11.67. I decided to add a risk premium of 1.09% in order to account for balance sheet risks in the case that EPS does not improve to expected levels due to a potential recession in 2024. I also estimated revenues and margins to continue growing in line with estimates.

5Y Equity Model DCF Using Net Income (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Strategic Partnerships Resulting in Compounding Growth

With its business for catalysts and chemicals in particular, Ecovyst has strategically made investments in innovation. Their collaboration with Shell Catalysts & Technologies, for instance, is an illustration of their innovative approach. Ecovyst created new Fluid Catalytic Cracking catalysts with the intention of improving refiners' propylene yields and generating financial gains.

This decision was crucial financially. A highly sought-after substance called propylene is essential for making plastics and other chemicals. By concentrating on creating catalysts that would increase propylene yields, Ecovyst put itself in a position to meet a growing market need. better propylene yields translate into more supply to fulfill demand, which will lead to better revenue and sales.

Additionally, Ecovyst's market reputation and competitiveness are improved by leading the way in novel petrochemical solutions. It can draw collaborations, partnerships, and contracts that have a favorable, significant influence on the company's income sources. This resulted in margin expansion due to greater pricing power and volume output leading to greater cash flows. I believe that partnerships or expansions such as the recent Kansas City project will enable future growth and improved cash flows in the long-term resulting in shareholder value appreciating from its current stagnant performance.

Risks

Regulatory Compliance and Environmental Risks: The chemical sector is subject to strict regulation. The operations and expenses of Ecovyst may be impacted by modifications to rules governing emissions, waste management, or other environmental considerations.

Supply Chain Disruptions: The production and distribution of the firm may be negatively impacted by any supply chain disruptions, whether they are brought on by natural catastrophes, geopolitical unrest, or other circumstances.

Conclusion

To summarize, I believe that Ecovyst is currently a buy due to the firm's ability to foster innovation through partnerships, EPS growth improving its financial position, and undervaluation assuming my DCF figures.