taikrixel

ALLETE (NYSE:ALE) has recently had a price recovery following solid earnings. Even with this price increase, I believe that ALLETE is currently a buy due to its solid outperformance in regard to earnings in challenging times, solid acquisitions for the long run, generous dividend, and undervaluation assuming my DCF figures.

Business Overview

ALLETE, Inc. functions as an energy company, operating through distinct segments: Regulated Operations, ALLETE Clean Energy, and Corporate and Other. The firm uses a variety of energy-generating techniques, such as wind, solar, hydropower, and biomass co-fired with natural gas, coal-fired, and hydroelectric power. About 15,000 electric consumers, 13,000 natural gas customers, and 10,000 water customers in northwest Wisconsin are served by ALLETE's Regulated Operations utilities. It also provides services to fourteen non-affiliated municipal customers and over 150,000 retail customers in northeastern Minnesota.

Electric transmission assets in Illinois, Wisconsin, Michigan, Minnesota, and Minnesota are owned and operated by ALLETE. The corporation possesses around 1,300 megawatts of wind energy-producing facilities and is actively involved in the development, acquisition, and management of clean and renewable energy projects. In addition to coal mining, ALLETE also engages in real estate investing in Florida and North Dakota. Owning 162 substations with a combined 10,116 megavolt ampere capacity, ALLETE serves a variety of businesses, such as pipeline, secondary wood products, paper, pulp, taconite mining, and more.

ALLETE

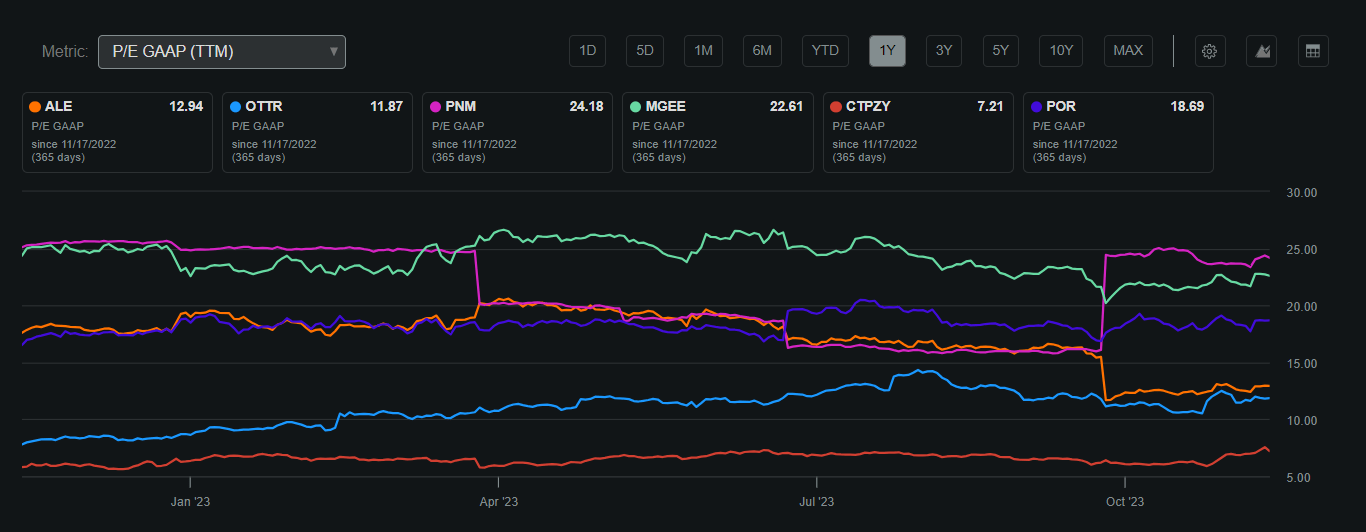

ALLETE is valued at a market capitalization of $3.2 billion and demonstrates a 3% Return on Invested Capital. In the last 52 weeks, its stock has fluctuated between a high of $67.45 and a low of $49.29. The current stock price stands at $55.44, accompanied by a P/E GAAP ratio of 12.94, placing ALLETE in proximity to its 50-day moving average of $54.21. Notably, in comparison to its industry counterparts, the company's P/E ratio is notably lower, suggesting potential value relative to others in the industry. This indicates a promising position for investors seeking relative value within the sector.

ALLETE P/E GAAP Compared to Peers (Seeking Alpha)

The firm also pays a dividend of 4.86%, representing a payout ratio of 62.23%. This generous dividend demonstrates the consistent income shareholders receive to create value. With only a 3% ROIC, ALLETE has recognized that utilizing FCF to grow is rather unproductive, and distributing a fair share of FCF while also investing in growth would be the best course of action. I agree with this method of value creation as the firm is already well established and can focus on income investors rather than burn cash attempting to scale, especially with the current macro headwinds.

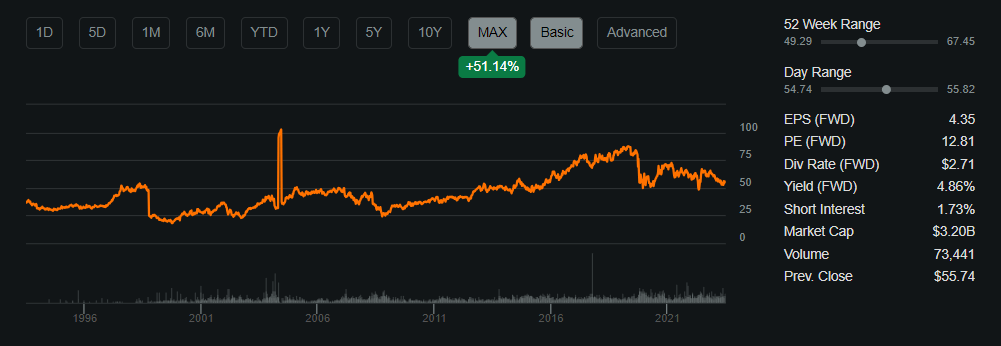

Share Performance (Seeking Alpha)

Performance Compared to the Broader Market

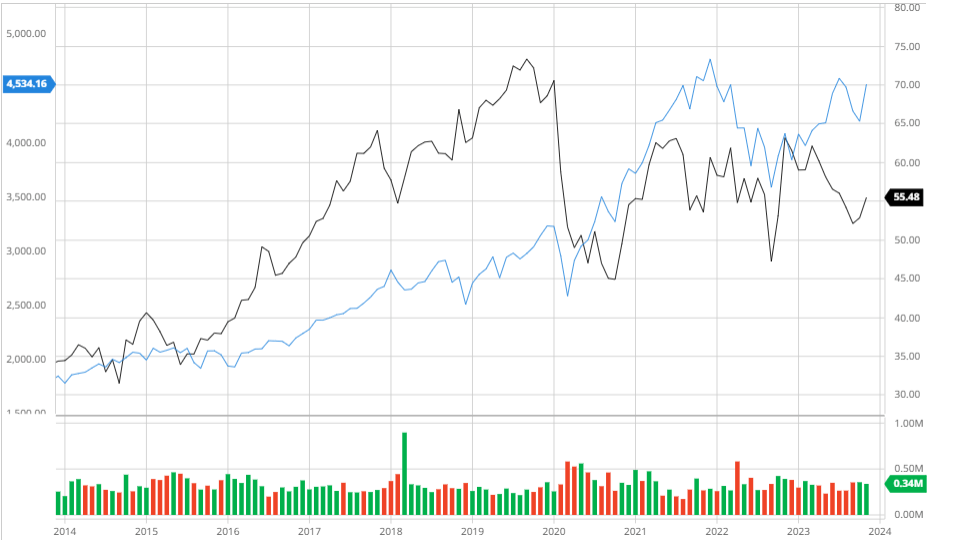

Over the past 10 years, ALLETE has underperformed the S&P 500 when adjusting for dividends. This is due to the recent pullback in price from high rates which are especially impacting utilities due to opportunity cost compared to bonds. I believe that although bonds seem relatively attractive as of now, recent price declines have made utilities attractive from a valuation standpoint without many operational failures in its core business making a solid long-term hold.

ALLETE Compared to the S&P 500 10Y (Created by author using Bar Charts)

Balance Sheet

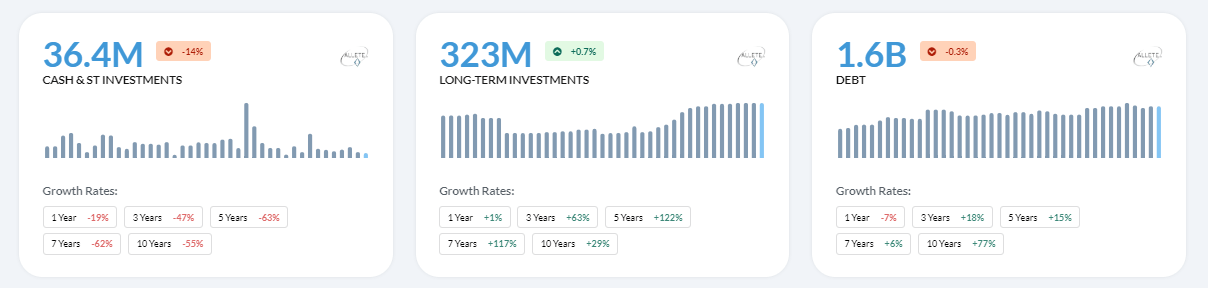

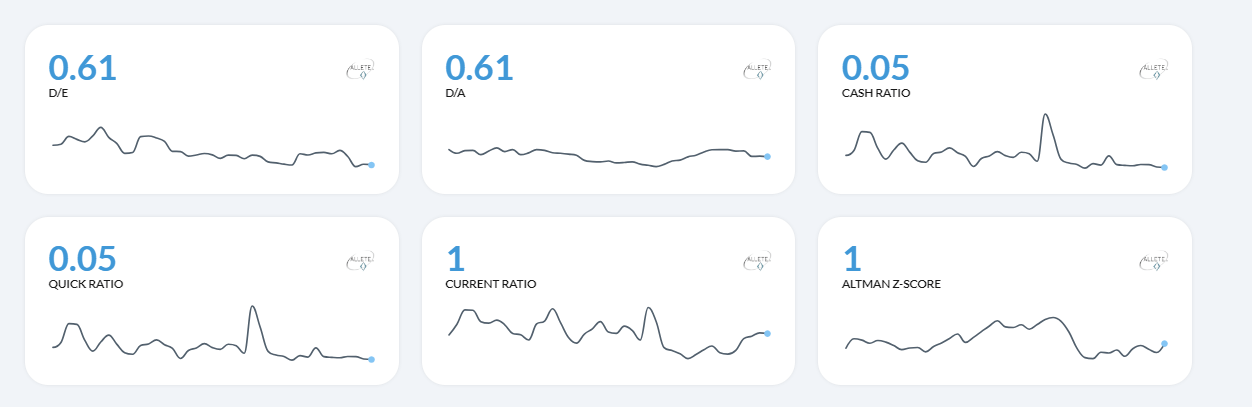

When examining ALLETE's balance sheet, it is evident that the firm is safely leveraged. With debt increasing 18% in the last 3 years and the firm's interest coverage dropping to 1.88, I feel that ALLETE should begin to focus on decreasing debt with remaining FCF without cutting the dividend in order to maintain long-term income. This would decrease interest payments and give the firm more FCF to either capitalize on expansion or payout as income over the coming years, which would be beneficial for shareholders. Lastly, with a Current Ratio of 1 and Altman-Z-Score of 1, the firm should remain solvent in the short term.

Financial Position (Alpha Spread) Interest Coverage (Alpha Spread) Solvency Ratios (Alpha Spread)

Q3 Earnings

ALLETE also reported solid Q3 2023 earnings with EPS surpassing estimates by $0.84 at $1.49 and missing revenues by only $18.45 million at $378.8 million showing a -2.4% YoY decline. Although revenues slightly missed, the firm raised guidance on EPS to $4.30 to $4.40 for the year and has created solid income in times of macro headwinds. Guidance for the upcoming years seems relatively flat with a decline in 2024 and then a recovery in 2025. I believe that although there may be a slight pullback due to high rates hindering expansion, the company is still an excellent long-term hold and will retain this year's large gains to create solid value.

Earnings Estimates (Seeking Alpha)

Analyst Consensus

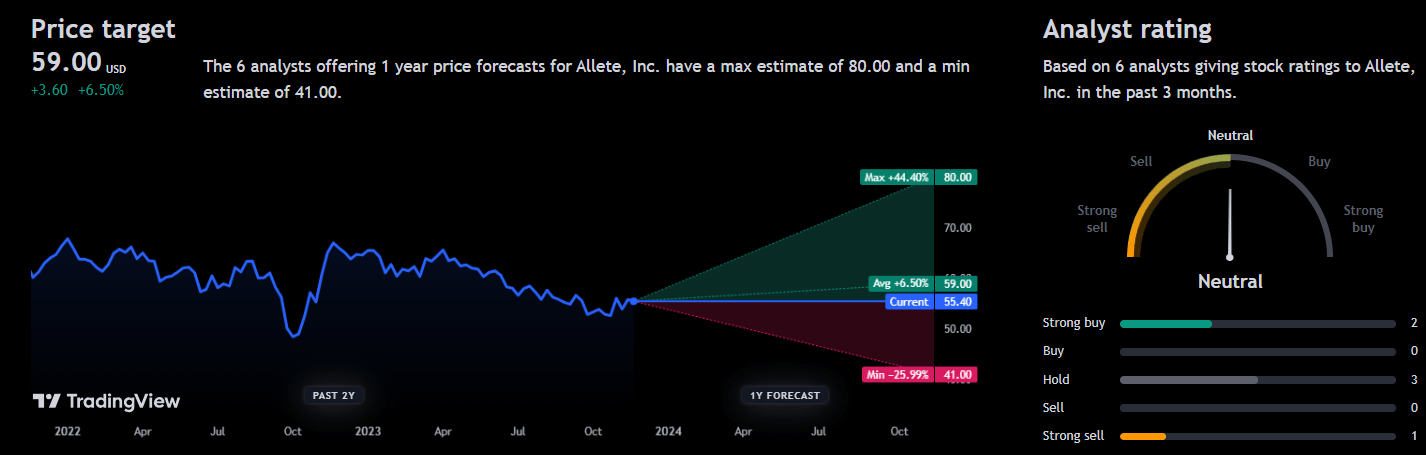

Analysts currently rate ALLETE as a "hold" with an average 1-year price target of $59 representing a potential 6.56% upside. This, combined with the dividend, will create a solid upside in the short term if analysts are correct which depends upon interest rates.

Analyst Consensus (TradingView)

Valuation

Before calculating ALLETE's fair value, I calculated a Cost of Equity for the firm using the Capital Asset Pricing Model. Using a risk-free rate of 4.46% based on the 10-year treasury yield and a beta of 0.72, ALLETE's Cost of Equity is 7.68%.

Cost of Equity (Created by author using Alpha Spread)

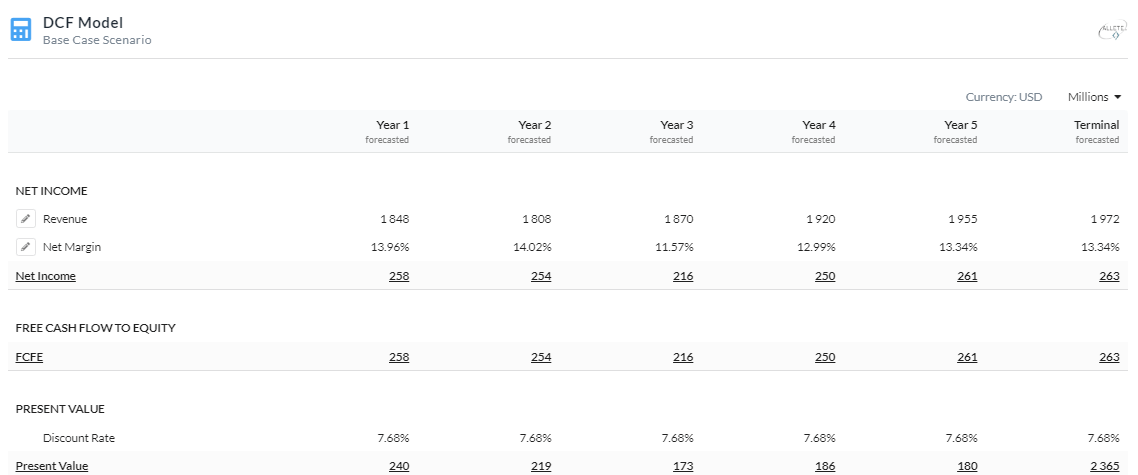

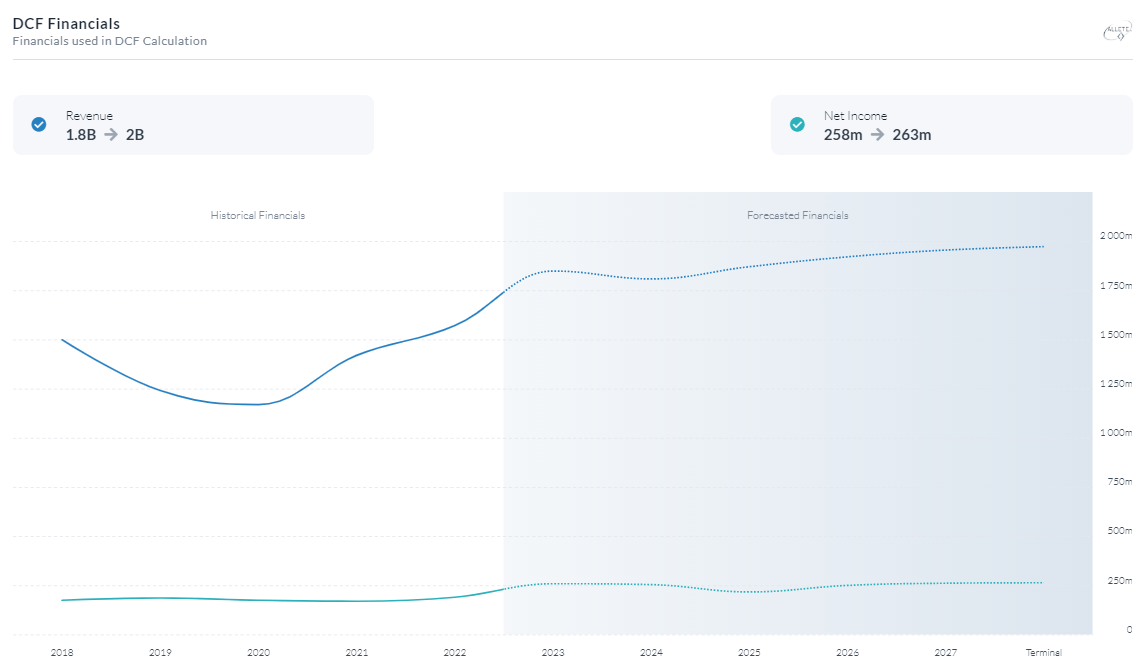

After finding an accurate discount rate, I used a 5-year Equity Model DCF based on net income to find a fair value for ALLETE. For this DCF, I used a discount rate of 7.68% which is in line with my Cost of Equity calculations. I decided to not add a risk premium for my discount as utility companies are relatively stable and receive rather undisturbed income throughout the cycles compared to other industries. In regards to my revenue and margin estimates, I assumed in line with analysts which is rather conservative when examining the firm's outperformance of these metrics recently. This resulted in a fair value of $58.5 presenting a 5% upside. I believe that the slight undervaluation along with the solid dividend makes this a buy due to its long-term income opportunity along with share price appreciation.

5Y Equity Model DCF Using Net Income (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

Strategic Acquisitions Resulting in Compounding Growth

To expand its footprint and strengthen its competencies in the energy industry, ALLETE Inc. has used a strategic acquisitions approach. The Diamond Spring Wind Project, a wind energy project in southern Oklahoma, was purchased by ALLETE Clean Energy in 2019. ALLETE's portfolio of renewable energy now includes 303 megawatts of wind production capacity thanks to this smart purchase. ALLETE sought to take advantage of the rising demand for clean and sustainable energy sources by increasing its footprint in the wind energy industry. A prime example of ALLETE's approach to carefully choosing assets that complement its dedication to sustainable development and renewable energy is the Diamond Spring Wind Project. These purchases support the company's overall expansion and placement within the ever-changing and dynamic energy sector.

I believe that these acquisitions will not only diversify the firm's portfolio but also position it in a market that has great long-term opportunities. This will create solid growth in regard to profitability as well once renewables become mainstream which would improve the scalability of these acquisitions and create unique pricing power in the regions of operation. This will also enable ALLETE to capitalize on government tax credits thus making initial contributions minimal compared to other forms of expansion. This would allow the firm to work around its heavy debt load to spark improved cash flows and thus decrease its cost of debt in the long run.

With EPS growing by a significant margin, I believe that once ALLETE pays off more of its debt, the firm will continue to utilize these acquisitions in order to create synergies with its core business. Once macro headwinds subside and the cost of debt declines, the firm will be able to effectively leverage to purchase these opportunities and will improve strength in the core business.

Risks

Regulatory Risks: Because ALLETE works in a highly regulated sector, alterations to laws, ordinances, or rate structures may have an effect on the company's operations and financial performance.

Energy Price Volatility: The cost of energy commodities such as electricity affects ALLETE's earnings. The profitability of the firm may be impacted by price volatility.

Conclusion

To summarize, I believe that ALLETE is currently a buy due to its solid outperformance in regard to earnings in challenging times, solid acquisitions for the long run, generous dividend, and undervaluation assuming my DCF figures. I believe that monitoring interest rates and their impact on ALLETE's debt load payments will be prudent as further rate hikes may alter my thesis due to solvency concerns.