Poca Wander Stock

With the markets set to rally again on optimism for cooling inflation and interest rate cuts, it’s a great time to re-invest into early-stage, phenomenal growth stories - particularly in industries that have not yet been dramatically influenced by technology yet.

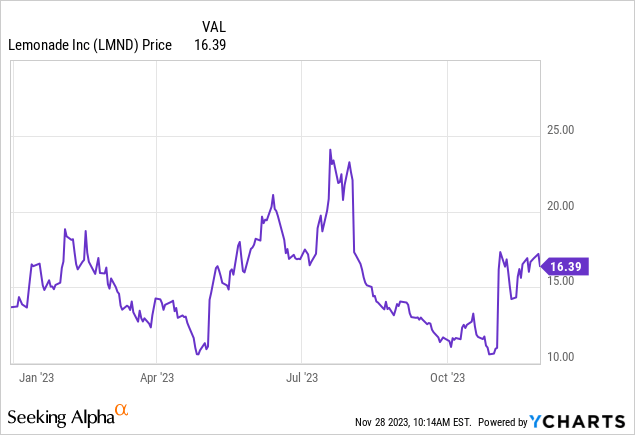

Lemonade (NYSE:LMND) is a great choice here. The online insurance company is set to disrupt the legacy insurance industry - with its human sales offices and paper policies - with its digital-first customer acquisition approach, AI-based claims handling, and ever-diversifying portfolio of offerings. Year to date, the stock is up ~20%, but I think there’s more room for Lemonade to keep rallying next year.

The bull case for Lemonade looks bright at 2 million customers and counting

I last wrote a bullish article on Lemonade in August, when the stock was trading closer to $16 per share. Since then, the company has released excellent fiscal Q3 results, while also pulling in its expectations for both free cash flow and adjusted EBITDA breakeven. The company has also announced that a lot of its filings for rate increases have been approved and are set to start earning in, particularly for its auto insurance line in California (where the state makes up more than 50% of its overall auto insurance book). All in all, I remain quite bullish on Lemonade and think there are a number of catalysts that can keep pushing the stock northward.

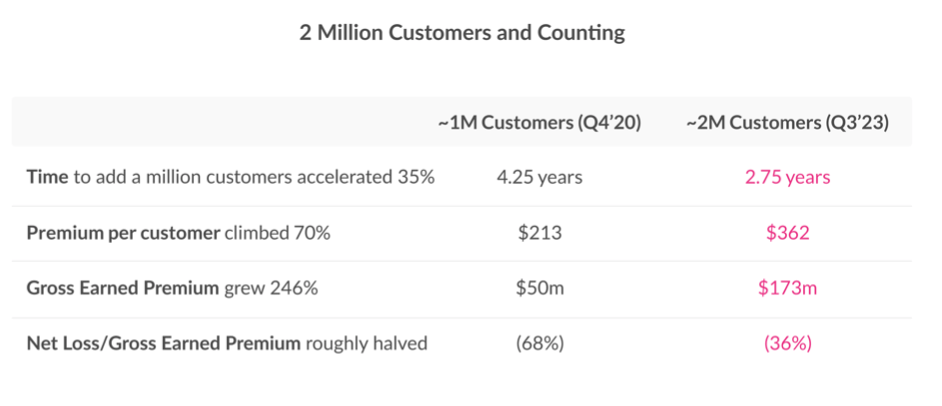

Lemonade also recently crossed the 2 million customer threshold, as shown in the chart below:

Lemonade customer metrics (Lemonade Q3 shareholder letter)

The snapshot above doesn’t just demonstrate Lemonade’s sheer scale, but the economies of scale that come with it. It’s worth noting that it took Lemonade about ~50% less time to acquire its second million customers than the first - a function of both scale as well as the diversity of offerings now under Lemonade’s umbrella. It’s worth noting as well that its net loss ratio, as a percentage of gross earned premium, is now about half of where it was when Lemonade crossed its first million customer mark - a trend that will continue to improve as Lemonade scales.

As a reminder to investors for what I believe to be the long-term bull case for this company:

- Enormous growth rates showcase the largesse of its market opportunity. Lemonade is nearly doubling its revenue on a y/y basis. And though the current market is very nonchalant about impressive growth rates, to me, this shows a business that is still very much in its nascency and able to scale to much greater heights.

- Lemonade is the new way to buy insurance. Gone are old-school insurance agencies and insurance agents; nowadays, just like everything else, we buy insurance online. As the new generation of tech-savvy millennials and younger cohorts dominate the consumer base, insurtech vendors like Lemonade will gain market share versus their legacy counterparts.

- Building a full insurance flywheel. When it started out, Lemonade just offered home and renters insurance. Now, the company is also offering bundles with pet insurance and car insurance as well (the latter through its acquisition of Metromile). Perhaps in no other industry is diversification more vital than in insurance, so Lemonade's ability to continue growing into other insurance streams will be critical to its success.

- Loss ratios are set to improve. Lemonade is already on a positive trajectory for loss ratios, driven by both increased scale as well as efficiency of its AI bot for paying off small, legitimate claims. Progress toward regulatory approval for rate changes will help to accelerate the trajectory of loss ratio improvements as well.

The bottom line here: there continues to be quite an upswell of positive drivers for Lemonade heading into 2024. Stay long here and ride the recent upward momentum.

Q3 download

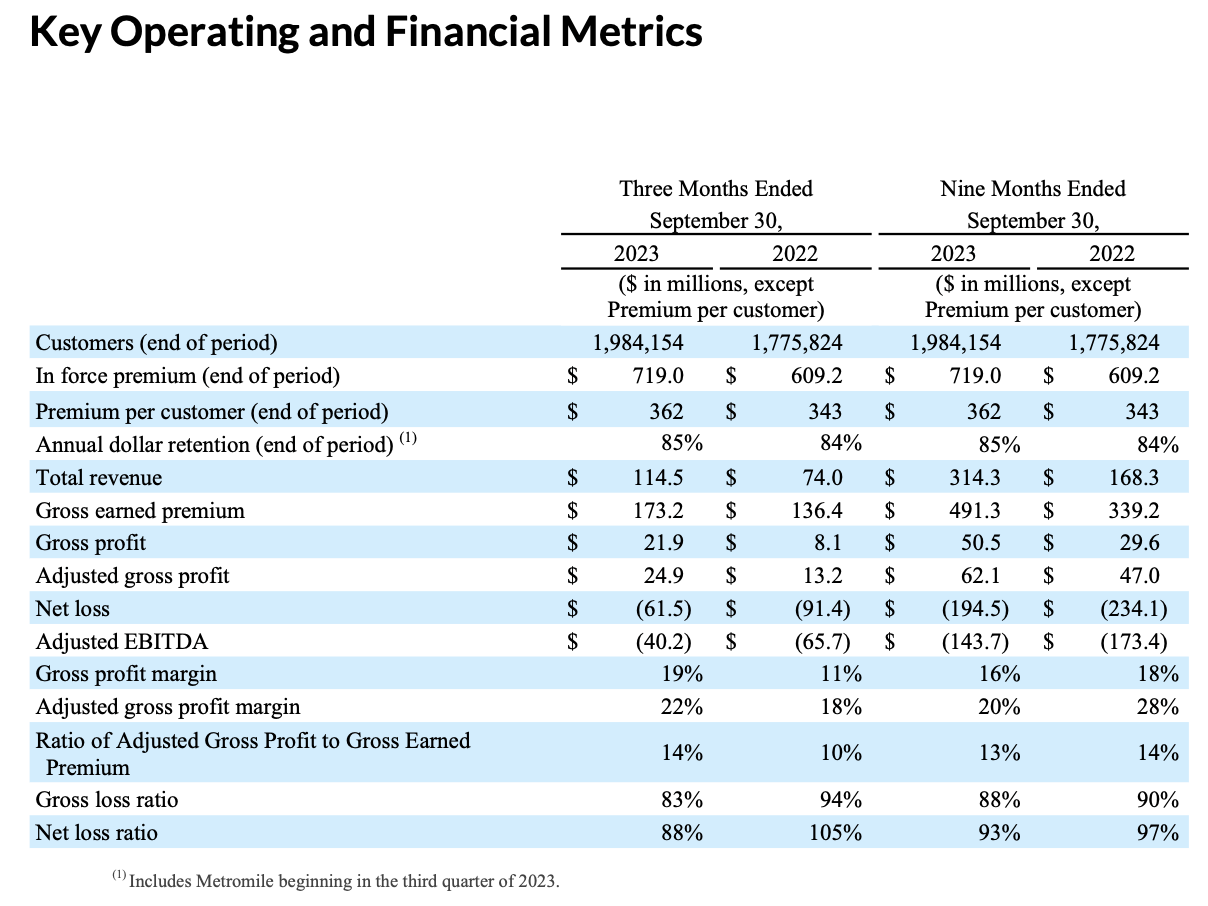

Let’s now go through Lemonade’s latest Q3 results in greater detail. The Q3 earnings results are shown below:

Lemonade Q3 highlights (Lemonade Q3 shareholder letter)

Lemonade’s in-force premium (IFP), a measure of total premiums paid by insurance customers before remitting share to re-insurers, grew 19% y/y to $701.6 million in the quarter. This did decelerate from 50% y/y growth in Q2, but do note that Q3 is the first quarter in which last year’s acquisition of Metromile is fully comped. Sequentially, the company added ~$32 million of net-new IFP in the quarter. Premium per customer of $362 also grew 6% y/y, reflecting the higher rate of cross-sell that Lemonade has throughout its fuller suite of insurance products.

Revenue, meanwhile, grew 55% y/y to $114.5 million. This was driven in part by the increase in IFP, but also due to higher interest rates and higher investment income on float balances. Note that the company is expecting a wave of approved premium increases to start kicking in. Per the company’s Q3 shareholder letter:

Inflation has swelled the severity of claims across the industry, and disproportionately so for home and car claims. Backlogs in getting inflation- adjusted-rates approved, coupled with growing CAT and an extraordinarily ‘hard’ reinsurance market, have driven marquee insurers into record losses, leading to unprecedented withdrawals of the best known insurers in the US from some of its largest insurance markets. There’s been nothing quite like it in living memory.

We’re not impervious to these forces, of course, and our response to them has been a massive increase in our pace and scope of rate filings. As of Q3 2023, we have earned about $45m in premium from our new rates, with a further $120m online but yet to earn in. Further rates await regulatory approval, so that during 2024 we expect to earn an additional >$100m from increased rates.

The actions we’ve taken and plan to sustain will, we believe, yield a return to healthy loss ratios, though the nature of the file-approval-implement-earn- in-cycle is such that it may be 18-24 months (depending on inflation rates, and approval rates) before we’re fully caught up.”

This includes the aforementioned approval in car insurance rate increases in California, which, as a reminder, makes up 50% of the company’s auto insurance book.

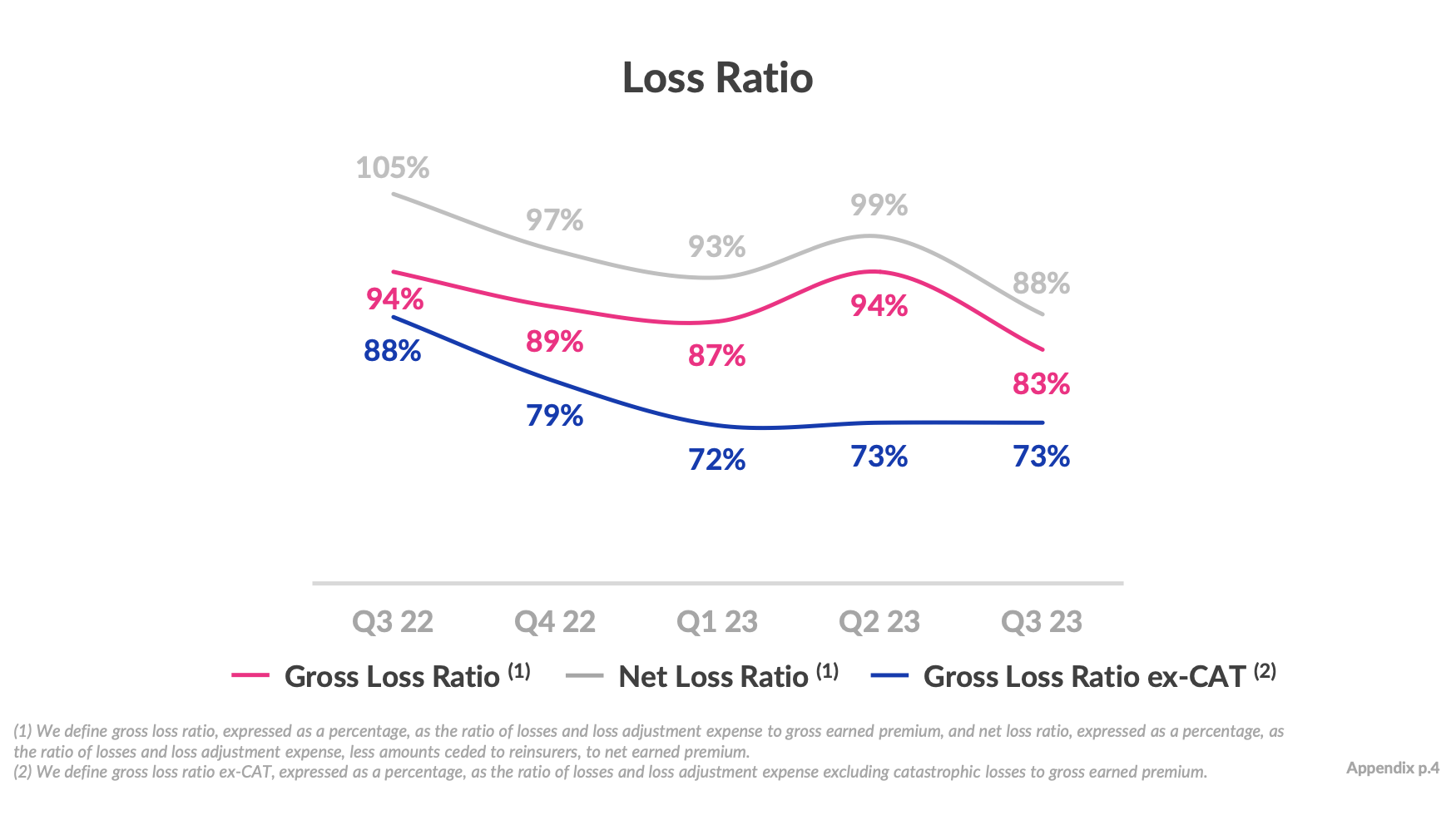

Gross and net loss ratios, meanwhile, continue to trend downward.

Lemonade loss ratio trends (Lemonade Q3 highlights)

Gross loss ratios in the quarter hit a multi-year low of 83% this quarter, after spiking in Q2 due to extreme weather events in the quarter. Similarly, net loss ratio of 88% is 11 points better sequentially than 99% in Q2 and 17 points better y/y relative to 105% in the year-ago Q3.

This, in turn, has helped the company achieve a multi-year high in adjusted EBITDA of -$40.2 million, which is a 25% smaller loss versus Q2 and 39% less versus Q3 of the prior year. Slower opex growth, improving loss ratios, and the approval for rate increases have all helped the company to boost its confidence in its breakeven timeline. As it wrote in its shareholder letter:

We’re happy to share that we now expect to turn cash-flow positive in late 2025 - considerably sooner than we had indicated last year - and expect to get there with hundreds of millions in unrestricted cash in the bank. Given the favorable cash flow dynamics of insurance (customers pay us before we pay them), Adjusted EBITDA profitability is expected to follow in 2026, a few quarters after our cash-flow turns positive.”

The company additionally called out that it expects “material” improvement to adjusted EBITDA losses in FY24, versus its expected range of a $186-$188 million loss this year.

Key takeaways

In Lemonade, I continue to see an early stage, well-equipped insurance company taking on the goliaths of a legacy industry that is slower to adopt technology and AI into its processes. While Lemonade’s losses now look ghastly due to its small scale, its rapidly reducing adjusted EBITDA losses give us confidence that the company is building profitability as it scales. Stay long here.