JHVEPhoto/iStock Editorial via Getty Images

Company Snapshot

Still early in the trading week, and so I'm jumping back into the energy sector in today's research note with coverage of energy giant ConocoPhillips (NYSE:COP).

Some quick facts about this company are that they operate in 13 countries, produce oil and natural gas which includes exploration and transportation, based in Houston Texas and trades its stock on the NYSE.

A fun fact is that the company's Optimized Cascade process provides more than 110 million metric tons per year of the world’s LNG (liquid natural gas) supply capacity.

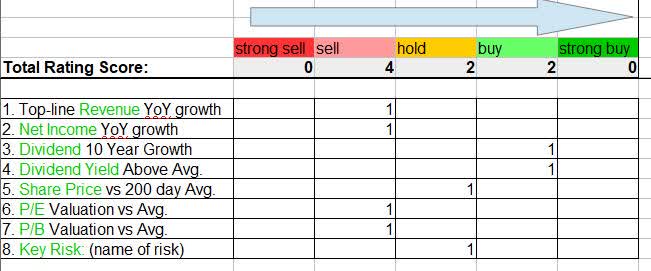

Total Rating Score

Conoco Phillips - score matrix (author analysis)

Based on the score total in today's note, I'm rating this stock a sell.

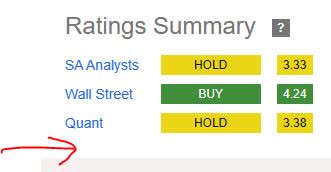

Comparing my rating to the consensus on Seeking Alpha today, my rating is more bearish than the consensus:

Conoco - rating consensus (Seeking Alpha)

Rating Methodology

My simplified and straightforward 8-point approach focuses on a few core areas such as revenue and earnings growth, dividend income opportunity, undervaluation opportunity, a share price presenting a value-buying potential, and identifying a key risk of the company as well as its potential impact to an investor, with a focus on data from the accounting statements.

Top-Line Revenue YoY Growth

I am looking for any positive revenue growth on a YoY basis, and here is what I found:

In the quarter ending Sept 2023 total revenue was $14.6B, vs $21.57B in Sept 2022, a 32% YoY decline.

On a positive note, though, looking forward according to the Q3 release we can expect Conoco to achieve additional global production growth:

"In October, several international projects reached first production, positioning us for 2024 and beyond. And today we announced a 14% increase in our quarterly ordinary dividend, consistent with our long-term objective to deliver top quartile growth relative to the S&P 500."

However, with the current slide in oil prices, which I will talk about in the next section, I am on the fence about the near-term revenue growth potential here, so I will add a point to the sell side of my scoring matrix.

Net Income YoY Growth

I am looking for any positive net income growth on a YoY basis, and here is what I found:

This Sept 2023 net income was $2.79B, vs $4.52B in Sept 2022, a 38% YoY decline.

The impact of oil prices on net earnings must be mentioned.

For example, here is what the company said in their Q3 release:

"Earnings and adjusted earnings decreased from the third quarter of 2022 primarily due to lower prices. The company’s total average realized price was $60.05 per BOE, 28% lower than the $83.07 per BOE realized in the third quarter of 2022."

Before investing in this type of business, therefore, I would consider the impact that oil/gas prices have on a company like this, and the fluctuating nature of oil supply and prices. Remember not that long ago when energy prices fell so much that several oil wells had to be taken offline as it was not economically viable to keep them running.

Consider that a December 5th article by Axios highlighted the trend of declining oil prices right now:

"U.S. benchmark oil prices are down nearly 20% in the fourth quarter, to below $75 a barrel. American production is part of the reason that recent efforts by OPEC — and its strategic ally, Russia — haven't been able to end the slide in global oil prices."

Again, this makes my sentiment edge towards a "sell" of this stock right now while it is still trending above its moving average, however a "hold" would probably make more sense than a buy right now.

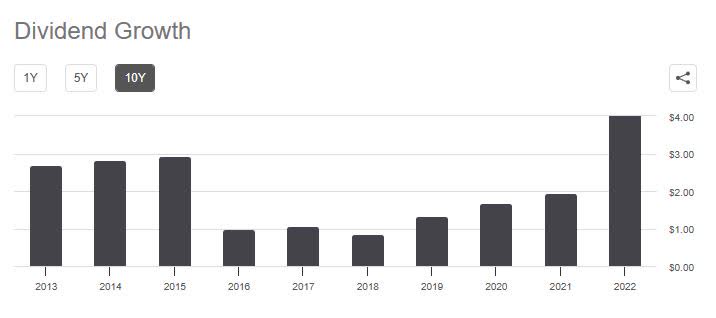

Dividend 10 Year Growth

I am looking for dividend 10 year growth trends, and here is what I found:

ConocoPhillips - dividend 10 yr growth (Seeking Alpha)

In looking at the 10 year chart above, the data story it tells is that the annual dividend went from $2.70 in 2013 to $4.99 in 2022. So, although there was a period where the dividend "dipped" so to speak, it rebounded quite nicely after taking that hit between 2016 - 2019. The net growth in dividends therefore is around 85% when comparing 2013 with 2022.

I think this presents an interesting opportunity for a dividend investor to take advantage of, particularly with a payout of $0.58/share, so I am adding a point to the buy side for this reason.

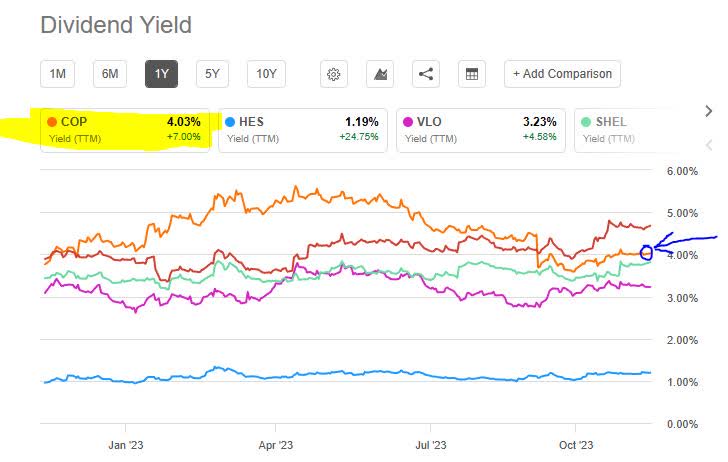

Dividend Yield Above Average

I am looking for a dividend yield above its sector average, and here is what I found:

ConocoPhillips - div yield vs peers (Seeking Alpha)

In the chart above using dividend yield data, I am comparing my focus stock Conoco vs a few of its peers in the global energy sector such as Hess (HES), Valero (VLO), Shell (SHEL), and BP (BP).

Of this peer group, the best dividend yield opportunity comes from BP, with a trailing twelve month dividend yield of 4.68%, while my focus stock is slightly behind it at 4.03%. Note that its forward yield is closer to 2%, though, while BP's is around 4.9%.

However, from looking at the dividend history of Conoco you can see that besides a regular quarterly dividend it also pays 3 "special/other" dividends throughout the year. This is significant to note as I do not find a lot of companies here that do so, so for that reason I will add a point to the buy side and add this stock to my dividend quick-picks of the week.

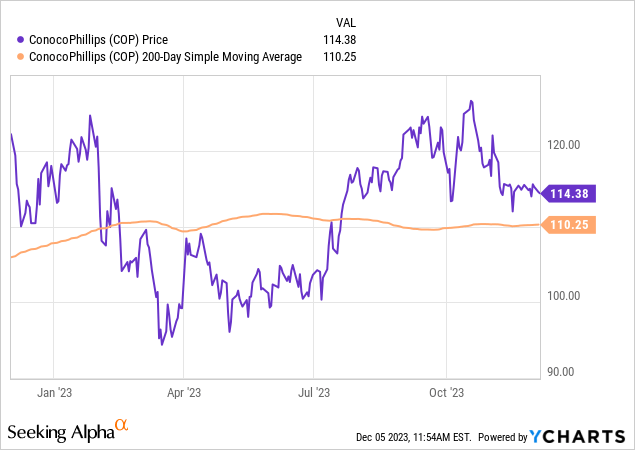

Share Price vs 200-day Average

My portfolio strategy prefers dip-buying opportunities when the share price falls below the 200-day simple moving average, so here is what I found:

When looking at this price chart, as a value-buyer I see an important dip-buying opportunity was missed in the spring and early summer for those that did not take advantage of it, as it rebounded quite nicely and has been trading above its 200-day simple moving average (orange line) for several months now, and currently hovering around $114.38.

Based on this current price range, combined with the declines in revenue and earnings, make me lean more towards a hold rather than a buy in this case.

P/E Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-earnings, and here is what I found from valuation data:

The forward P/E ratio of 12.63 is +17% above the sector average.

In tying this multiple back to the financials and share price I discussed, I think what is driving this valuation is the bullish share price combined with a significant +30% earnings decline, causing the nearly 13x price multiple to earnings.

I will call this overvalued because the market is being overly bullish on a company with declining earnings. If you look again at the income statement you can see that after June 2022 earnings have generally been on the decline from that quarter when the firm saw $4.5B in net income.

So, I will add a point to the sell side of the score for this reason.

P/B Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-book value, and here is what I found from valuation data:

The forward P/B ratio of 2.82 is +71% vs the sector average.

In tying this multiple to the share price discussed as well as the equity/book value in the balance sheet, we can see that while the share price has been bullish and trading well above the 200-day moving average for a while at the same time the equity declined to $47.7B in Sept 2023 from $49.07B in Sept 2022, a nearly 3% YoY decline. Further after Jun 2022 the equity/book value has generally been on the decline. One factor could be the increasing trend in the long-term debt, which can impact book value.

For this reason, I will call this overvalued and add a point to the sell column.

Key Risk

We already mentioned the risk impact of falling global oil prices on a company like this, however I do believe the global energy demand will continue to exist but it will just be less profitable in this environment. According to the company's Q3 release and outlook, "fourth-quarter 2023 production is expected to be 1.86 to 1.90 million barrels of oil equivalent per day (MMBOED)."

With expected hits to profitability, I am concerned about rising interest expenses (in this high rate environment) along with rising debt.

When looking at the income statement again, though, we see quarterly interest expense dropped to $194MM from $199MM in Sept 2022, a 2.5% YoY drop. At the same time, however, long-term debt rose to $17.02B from $15.01B in Sept 2022, a 13% rise.

One should also consider that it is a very capital intensive industry, and it is expected to need lots of debt financing I think. What is a positive offsetting factor is that it has posted positive cash flow in the last 5 quarters. It is also a company that holds $93.6B in total assets.

So, I will be putting a point in the hold column of my score matrix for this reason, rising debt levels offset by dropping interest expense and positive cash flow.

Wrap-Up

To summarize, this is my first sell rating of the month and the drivers of my bearish sentiment include declines in revenue and earnings, downside potential for oil prices, overvaluation, and a high share price.

Some positive offsetting factors include a +4% trailing dividend yield along with proven 10 year dividend growth.

The risk of rising debt is offset by decreasing interest expenses and a really strong cash flow and assets.

If this stock was in my portfolio I would sell now to gain from the March or July lows when it was around $95, assuming I had bought then, and now I can nail a $19/share capital gain. Then I would wait for the next price dip below the 200-day average, to grab some shares again. However, I would do so only if I also have some exposure to other energy stocks too like Valero (VLO), another stock I recently covered and gave a buy rating to.