maybefalse/iStock Unreleased via Getty Images

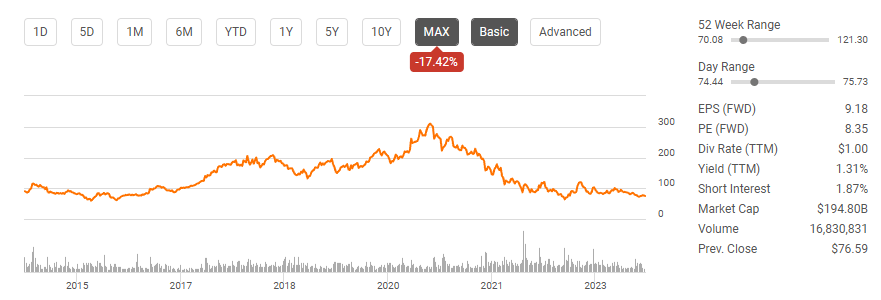

What else can I say about Alibaba (NYSE:BABA)? It's been one of my worst-performing holdings. Over the past several years, the China growth story didn't play out how I thought it would as geopolitical and macroeconomic headwinds drastically impacted the investment narrative. Shares of BABA peaked at around $309.92 on October 19th, 2020, and just over 3 years later, BABA has fallen -75.91% (-$235.26). I don't get everything correct, and I have watched shares of BABA drastically decline in disbelief. I started a position in the winter of 2021 as shares were initially declining. Since starting the position, I have paid approximately as much as $250 for shares and recently as low as $75. I've gotten my cost basis to around $144, and I am considering adding enough shares while its share price is under $80 to get my cost basis to around $100. This is the exact reason why I am highly diversified and keep cash on the sidelines. I went into BABA knowing that things could go wrong and that shares may not rebound anytime soon. There hasn't been a minute of lost sleep over the unrealized loss as BABA is a relatively small position for me, and I could add more capital anytime I wanted. While I have been completely incorrect on how this investment would turn out, BABA is a strong company with significant growth on the horizon. I am not throwing in the towel and am making a decision to endure whatever comes next, as BABA has the potential to still be a good investment for me.

Seeking Alpha

Following up on my previous article about Alibaba

My last article about BABA was published on May 19th, 2023 (can be read here), and since then, shares have declined -10.96% from $83.95. I discussed how BABA was looking to unlock shareholder value through several spinoffs while discussing their fiscal year and valuation at the time. Since then, shares have continued to decline a bit, and from an investment perspective, investors are still in the doghouse. I recently added to my position, and I wanted to write a new article discussing why I am willing to add more capital to this investment rather than exiting the position and utilizing the loss for tax loss harvesting purposes.

Alibaba has been a destroyer of capital for me, but I am not willing to cut my losses

I have never met a single person who enjoys losing, but I know many people who have held on to a losing hand for much longer than they should have. While I have exited positions that have allowed me to book a large profit and exited positions in the red because my investment thesis was no longer intact, BABA, just like AT&T (T) is a company I still believe can turn things around. I could be 100% incorrect, and BABA could continue to see share value deteriorate, but I am staying in the position with open eyes and understanding the risks.

I can only lose what I invest, and I am making sure that I won't be upset if an unwanted scenario continues to get worse. I am highly diversified, and BABA is a very small position in my overall portfolio. While every position is important as it represents hard-earned capital, there is a big difference between being down -48% and being down -48% in a position that represents significantly less than 1% of your portfolio. I have certainly lost out on opportunity cost along the way, as I could have sold BABA and reallocated the capital to positions such as Amazon (AMZN), Alphabet (GOOGL), or Meta Platforms (META) when I last added to those positions. I would be willing to sell BABA tomorrow if I thought my investment thesis was broken, but that isn't the case. I don't see BABA disappearing, I am not necessarily concerned about their financials being inaccurate, I have as much time as I deem necessary to stay in this investment, the current unrealized loss is insignificant compared to my overall portfolio and investment mix, and I think I can manufacture substantial upside by dollar cost averaging and waiting for sentiment to change as BABA is extremely profitable and there is substantial growth on the horizon. Ultimately, my investment thesis could be wrong, and I could see an unrealized loss continue to grow, but the capital I am investing in BABA fits within my risk threshold, and the investment makes sense for me.

Alibaba continues to trade at a ridiculously low valuation

BABA is a Chinese company that reports in RMB. I will be using their financials from Seeking Alpha (can be found here), which have been converted into USD. Investors allocate capital for many different reasons, but when you purchase even just one share of a company, you're paying the current market value for all of the future cash flow they are going to generate. You're purchasing shares in a revenue-generating, income-producing business, and valuations matter. I am usually extremely cheap when allocating capital and want to pay the best possible price for a company's future profits. In some cases, I am willing to look past how I would normally evaluate a company and pay a much higher multiple. Palantir (PLTR) is a perfect example, as I have been a shareholder since the direct listing, I have added shares since my original block, and it's a company I want to be a shareholder of for decades to come. I knew I was paying a premium for PLTR, and I was okay with it for many reasons. BABA, on the other hand, is a more mature company, and I am looking at it the way I would look at a traditional investment.

First, I am going to start with the balance sheet. BABA has $33.38 billion in cash on hand, with another $45.29 billion parked in short-term investments. Their total cash and short-term investments puts their on-hand liquidity at $78.67 billion. BABA has an additional $62.47 billion in long-term investments. Their total assets equal $248.13 billion, and when I subtract goodwill, they amount to $211.6 billion. On the liabilities side, BABA has $87.87 billion in total liabilities, with $21.71 billion in long-term debt and its largest liability of $39.26 billion in accrued expenses. BABA has a total of $27.18 billion of debt on the books with the ability to write a check to eliminate it tomorrow without having to touch its short or long-term assets. From a financial health perspective, BABA is top-notch with a negative net debt position of -$51.49 billion.

Steven Fiorillo, Seeking Alpha

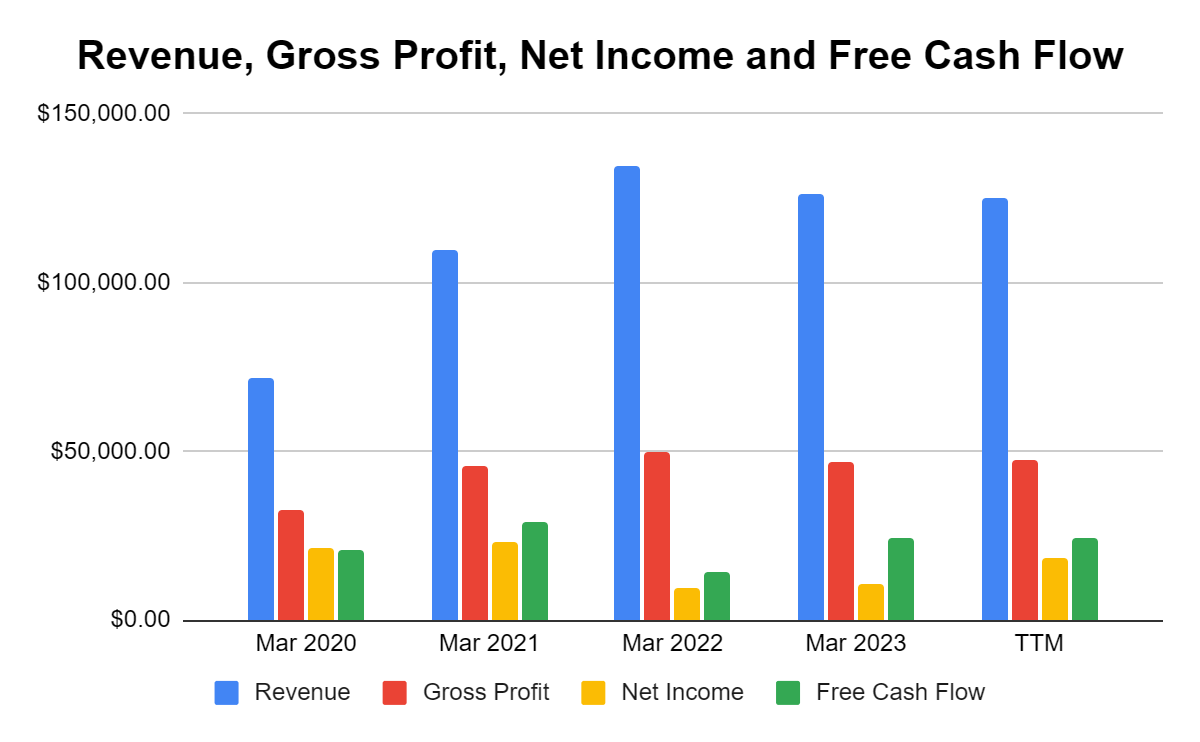

Shares of BABA are trading for roughly $75, and you're getting an underlying business with $13.16 in cash per share, with a book value of $55.87 per share. On top of the net assets, you are purchasing shares of one of the largest income-producing businesses in China. In the TTM, (BABA) has generated $125.31 billion in revenue, $47.28 billion in gross profit, $18.17 billion in net income, and $24.51 billion in FCF. BABA operates at a 37.73% gross profit margin, a 14.5% profit margin, and a 19.56% FCF yield. When I look at the past 5-years, BABA has generated over $500 billion in revenue, $2.66 billion in net income, and $112.66 billion in FCF. When I put the noise aside, I am looking at a company that has a stellar balance sheet generating tens of billions in profits.

Steven Fiorillo, Seeking Alpha

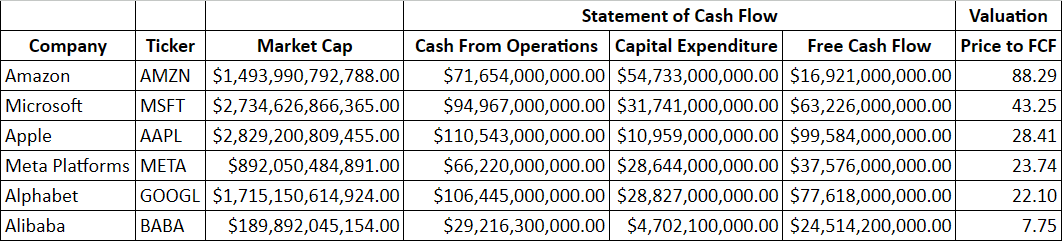

When I look at BABA's valuation against U.S. big tech, it's astonishing how inexpensive the multiple is. BABA is trading at 7.75x its FCF, which means that if all its shares were acquired, it would pay back 100% of the investment in less than 8 years. This is one of the lowest valuations I have seen, and it looks more like a tobacco company than a tech company. The other thing is that BABA's numbers aren't a fluke, unless every year has been an inaccurate account of what has occurred within their business operations.

When I look at this from an EPS perspective, BABA trades at 7.53x 2024 earnings and 6.72x 2025 earnings. The cheapest any of U.S. big tech trades for is 19.95x 2024 earnings and 17.51x 2025 earnings. BABA is trading as a company that has seen its best days decades ago, and this is a compelling reason why I am remaining bullish on BABA, even if I have to wait years for the story to unfold.

Steven Fiorillo, Seeking Alpha

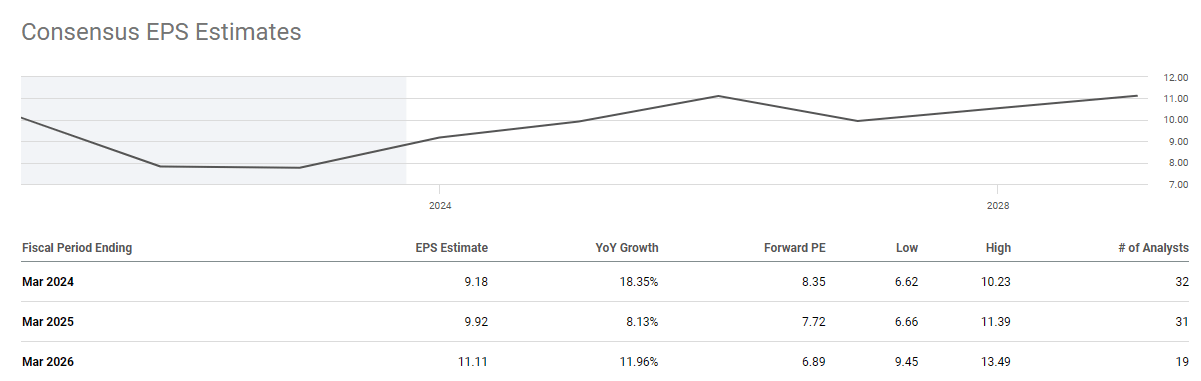

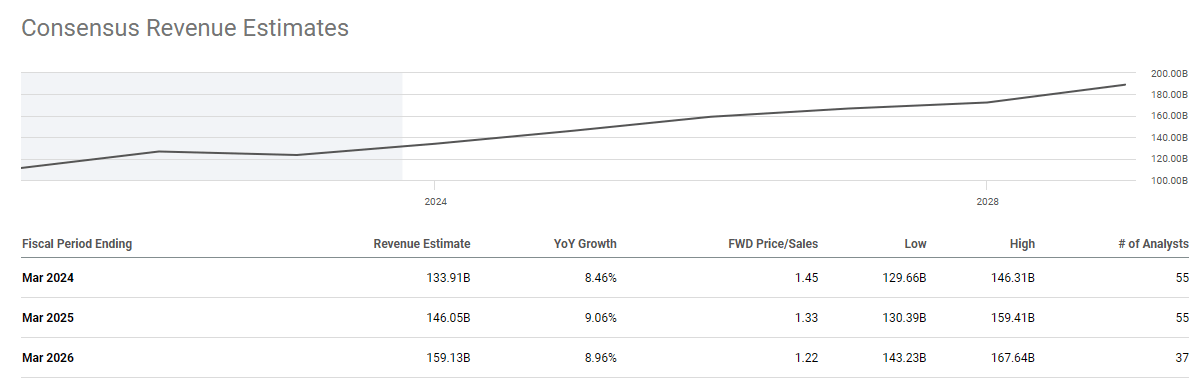

When I look at the consensus estimates, both EPS and revenue have a long runway ahead of them. There are 37 analysts who see BABA generating $159.13 billion of revenue in 2025 as BABA is projected to generate high-single-digit revenue growth. There are also 19 analysts that have BABA generating $11.11 in EPS for 2025. The analyst community is expecting significant growth on the top and bottom line, yet BABA is priced as if its best days are behind them.

Seeking Alpha

Seeking Alpha

Alibaba is rewarding shareholders through buybacks and now a dividend

An SEC filing came out (can be read here) that during 2023, BABA repurchased a total of 897.9 million ordinary shares (equivalent of 112.2 million ADSs) for a total of US$9.5 billion. The share repurchase program resulted in a net reduction of 3.3% in BABA's outstanding shares. BABA still has $11.7 billion remaining under its board authorization for buybacks through March of 2025. Based on today's market cap of $194.8 billion, BABA would be authorized to repurchase 6% of the outstanding shares while having enough capital to increase its buyback program significantly.

BABA has also implemented a dividend program and is paying $1 per share. While this is a lower yield at 1.31%, BABA is serious about returning capital to shareholders. As time progresses, BABA would have no problem providing annual dividend increases to shareholders and making the dividend more substantial. Investors are now being rewarded for waiting as BABA is aggressively buying back shares and distributing a portion of the profits as income to shareholders. If BABA establishes an annualized dividend increase and continues to generate EPS growth, it could become an enticing dividend stock for income investors.

Seeking Alpha

Risks to my investment thesis

There are so many risks to investing in BABA, and as we all have seen, shares continue to decline in value. Geopolitical tensions continue to remain high, and if an unfortunate escalation between China and Taiwan occurs, there is no telling what chain of events could be unleashed and how BABA would be impacted. BABA's cloud growth hasn't moved the needle as enterprise demand hasn't ramped up the way it has stateside. PDD's Temu has emerged as a strong competitor to BABA as its growth has been rapid in the U.S. and Europe. There is also no telling what political pressures will be passed on to BABA or if growth and innovation will be met with opposition. Shares always have the risk of being delisted in the U.S. if geopolitical tensions increase. U.S. investors may ultimately choose to stay away from BABA as there are many quality choices domestically to invest in. Investing in BABA isn't for the faint of heart, as there is a lot that can go wrong, and as we have seen, the market hasn't cared much about the underlying financials that BABA has produced.

Conclusion

I have had several opportunities to exit my position in BABA, but I see too much value to be unlocked. As I indicated earlier, I could be 100% incorrect, and shares may continue to decline as BABA is a very risky investment. In my investment thesis, the positives outweigh the risks as BABA has growth on the horizon and trades at largely discounted valuations to U.S. big tech. BABA will never become a big position or even a significant position in my portfolio due to my own diversification parameters, but I do think there is an opportunity for me to generate a significant return if I continue to lower my cost basis and wait things out. My goal will be to get my cost basis down to around $100 and hopefully exit between $150 and $200. If shares continue to decline, I would have to reassess my investment thesis at around $50 and determine if it's time to throw in the towel.